Tim Boyle

We spent the vast majority of 2022 looking at our portfolios and adjusting for what we thought would be tough times; we added quality and exited names which did not appear to have compelling risk/reward situations. We avoided some blowups, walked into a few but overall we were lucky to have started shifting the portfolio into quality names with realistic P/E ratios and other valuation metrics when we did because it did shield us from what could have been very large and painful losses. During the last quarter of 2022, we found ourselves doing a lot of credit research into various names to get a better feeling on some speculative names in terms of going concerns, or ability to generate adequate cash flows to refinance debt or pay dividends. This work has led us to some decent returns over the last few months which are not at all correlated to the general market, but instead to certain events playing out (or having played out).

One of the names that we did research into was Hanesbrands Inc. (NYSE:HBI), which was beaten up in 2022 over concerns about its balance sheet, operating results and speculation that the dividend might not be safe. Compared to some of the other companies we were looking into at the time, Hanesbrands has a pretty simple business model which is straightforward. In a very simplistic explanation, they purchase raw materials, manufacture them into clothing and then sell to retailers. Historically, Hanesbrands and many of its peers have strong cash flows and pay rich dividends but the fear among some investors has been that a weak economic backdrop, coupled with higher interest rates might create a scenario where companies with large debt piles could be forced to make some tough decisions (such as cutting dividends, laying off workers, etc.).

So Why Are People Worried?

Of all the things that people are worried about, it all boils down to one item: Cash flow! Hanesbrands has two items that its cash flows need to cover: a large debt pile that it must service and a dividend that its investors are quite fond of. The current annual interest expense that Hanesbrands must cover is between $130 million and $160 million and the company pays out roughly $210 million in dividends per year at the current rate and share count.

This has not been a problem for the company in recent years, and even in recent quarters management felt strong enough about the company’s business to repurchase $25 million of the company’s stock (approximately 1.6 million shares) as part of a stock repurchase plan (this occurred in Q1 of 2022). However, since the start of this fiscal year, the company has seen cash from operating activities turn negative and net changes in cash turn negative on a quarterly basis as well – other than Q3 2022 when the company was $5 million+ in the positive due to some financing activities.

While all of this was happening, cash/cash equivalents were trending lower (since Q3 2021) and long-term borrowings were trending higher from Q1 2022’s low. This makes sense as the cash to fund outflows has to come from somewhere and in this case it was a mixture of cash the company already had as well as accessing debt. We think it is important to point out that Hanesbrands was still profitable during this time, but revenues were trending lower and EPS were falling at a faster pace.

So What Seems To Be The Issue?

After analyzing the company’s results, reading a few conference call transcripts and looking over its balance sheet, we arrived at the conclusion that while supply chain issues had driven up costs to impact margins, the key issue facing the company was how supply chains and demand were impacting its inventories.

Hanesbrands Inventories (Seeking Alpha)

As one can see from the above data, Hanesbrands had seen its inventories grow since results reported in January 2021 (Q4 2022 results). From January 2021 to January 2022 the quarterly trend and variances seemed normal enough. However, the company then saw a major increase in inventories of $236 million the next quarter and another nearly $271 million the following quarter. While many may not recognize this because they are looking at various other metrics, this growth in inventory is the major driver of the worries surrounding Hanesbrands right now. It is impacting cash from operating activities, net changes in cash, etc. Management appears to be aware of the issue facing them, but we are not sure that they have truly addressed and fixed the issue.

Why do we say this? The company issued a press release on January 12, 2023 which included the following paragraph:

Excerpt from Hanesbrands Press Release (Hanesbrands Inc.)

Now it is important to note that the CEO’s quote references inventory units rather than inventories – meaning that he is talking about physical items in inventory and not in dollar terms. While that could be significant for a manufacturer who has items with vastly different price points, we think it is fair to assume that (for Hanesbrands) if inventory units are below last year’s levels, then inventories (in dollar terms) are probably down as well but not near last year’s levels.

In fact, in the Q&A of last quarter’s conference call, management touched on the reduction in “inventory units” and “absolute inventory units” on a few questions. So while the reduction in SKUs and the time-outs that they took at their manufacturing facilities will help the company run down a good bit of its physical inventory buildup that occurred in 2022, the actual dollar amount of inventories will remain high in Q4. The good news is that it appears, based off of previous comments and the most recent news release, that Hanesbrands will begin to see lower input costs in the 2H of 2023 which will help lower inventory and increase cash flows.

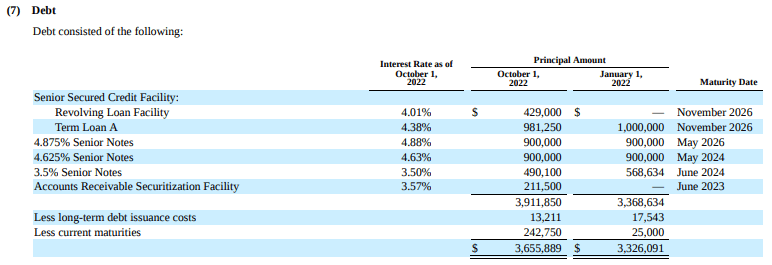

The Debt

If management is correct in their comments over the last few months that cash flows will return to normalized levels in 2023, then the debt should not be an issue. The good news for Hanesbrands is that they really do not have to face any debt maturities until 2024, as 2023’s maturities consists of an Accounts Receivable Securitization Facility (which are normally extended/amended under new terms and sometimes new spreads on the interest rate) and just over $31 million in outflows for the current portion of long-term debt.

HBI Debt Table (Hanesbrands Inc Form 10-Q)

So while it may look like the company has just over $242 million in debt repayments due in 2023, the accounts receivable balances net out and the true cash outflows are around $31 million net. It is 2024 which some see as the problem, as the company has two maturities which total just over $1.39 billion. Obviously the company will have to roll some or all of this via a refinancing, which then highlights what some see as the real issue – this is low coupon debt that will have to be refinanced at much higher rates.

The 4.625% Senior Notes are US dollar denominated, while the 3.50% Senior Notes are Euro denominated. This debt trades pretty well, with the 4.625% bonds trading at a yield of 5.927% and the 3.50% bonds trading at a yield of 5.266%. With Hanesbrands’ current credit ratings, we suspect that the company would be issuing debt for a yield of 7.50% to 8.50% to issue in the 5-7 year maturity window if they were to issue debt now in the U.S. and potentially 0.50% to 0.75% below that range to issue in Europe. On the U.S. issued paper, that would increase interest expense by over 60%, or just under $26 million annually if the company rolled the entire balance. That number jumps to nearly $42 million in additional annual interest expense if they roll the European debt as well.

This is not an issue if the company can go back to generating cash flows similar to what it used to, but even then the company might have some issues come 2026 when they will have to refinance other debt issuances as well as some loans.

Our Thoughts

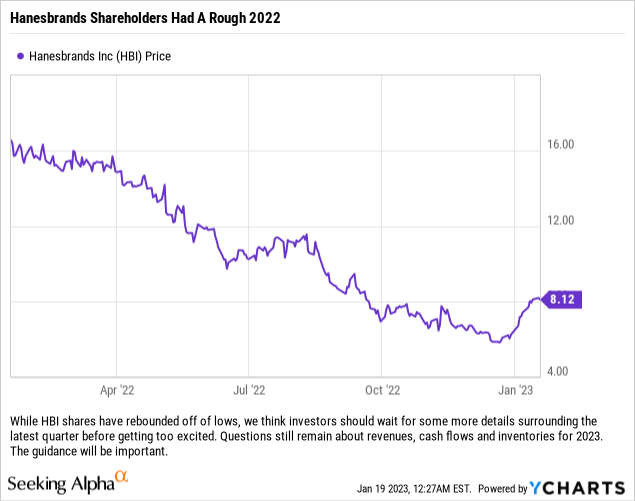

Obviously management was caught off guard with the supply chain issues in our view, otherwise they would not have been repurchasing stock and wasting $25 million. Hanesbrands will release Q4 and 2022 full year results on February 2nd which will bring a close to a wasted year for investors. Very little was accomplished in 2022 for investors, as cash flows shrank (and turned negative!), inventories ballooned and management made no significant adjustments or progress on paying down debt.

We purchased very small positions for various portfolios as Hanesbrands was trading near its 52-week lows based on valuation alone. We think that management could thread the needle on this one and manage to refinance the debt while maintaining the dividend if they can get revenues and cash flows back to historical levels. If cash flows do not fully recover to those levels, then there is good news and bad news for investors. The good news is that the company has the ability to continue as a going concern, but the bad news is that to do so might require a dividend cut (or the elimination of the dividend altogether).

Our investment thesis for the initial trades we placed was that Hanesbrands is not going out of business and is centered on total return rather than a narrower focus on the continuation of the current dividend policy and rate. We think that the business should be able to generate FCF of at least $300 million annually and up to $550 million in a best case scenario in the current economic environment. If management can achieve this level of FCF then they may be able to pay down some debt and keep annual interest expense in the same neighborhood come 2024.

At current levels we think that Hanesbrands stock is a ‘Hold’ until after Q4 results are released and we get more color from the management team on guidance for FY 2023 as it relates to revenues, cash flows and inventories. If you own the shares already, holding is the only way to play this right now, and if you do not own shares already, due to the recent 30%+ move higher we think waiting for the clarification and guidance that should be provided in the next quarterly results is the prudent move.

Be the first to comment