Klaus Vedfelt

A Quick Take On Squarespace

Squarespace, Inc. (NYSE:SQSP) reported its Q3 2022 financial results on November 8, 2022, beating revenue and meeting EPS estimates.

The firm provides users with the ability to build and manage their online website and digital presence.

Squarespace, Inc. is seeing soft consumer discretionary spending impact its gross merchandise volume growth.

I’m on Hold in the near term for SQSP.

Squarespace Overview

New York, NY-based Squarespace, Inc. was founded in 2003 to provide a suite of website hosting services to individuals and organizations around the world.

The firm is headed by founder and CEO Anthony Casalena, who graduated from the University of Maryland with a B.S. in computer science.

The company’s primary offerings include:

-

Website creation

-

Domain name

-

Marketing

-

Ecommerce

-

Unfold social media

-

Scheduling.

Squarespace markets its services to consumers and small business owners via content marketing, digital advertising, social media platforms, email marketing, word of mouth and search engine optimization.

Squarespace’s Market & Competition

According to a 2020 market research report by Grand View Research, the global market for web hosting services was an estimated $56.7 billion in 2019 and is forecast to reach $180 billion by 2027.

This represents a forecast strong CAGR of 15.5% from 2020 to 2027.

The main drivers for this expected growth are the growing number of individuals and companies seeking a web presence and an increased desire to perform more business functionality in the cloud.

Also, the onset of the COVID-19 pandemic has generated strong growth in Internet-based activity, providing a boost to the industry.

Major competitive or other industry participants include:

-

Automattic

-

Wix

-

Weebly

-

Shopify

-

BigCommerce

-

GoDaddy

-

MailChimp

-

MindBody

-

Others.

Squarespace’s Recent Financial Performance

-

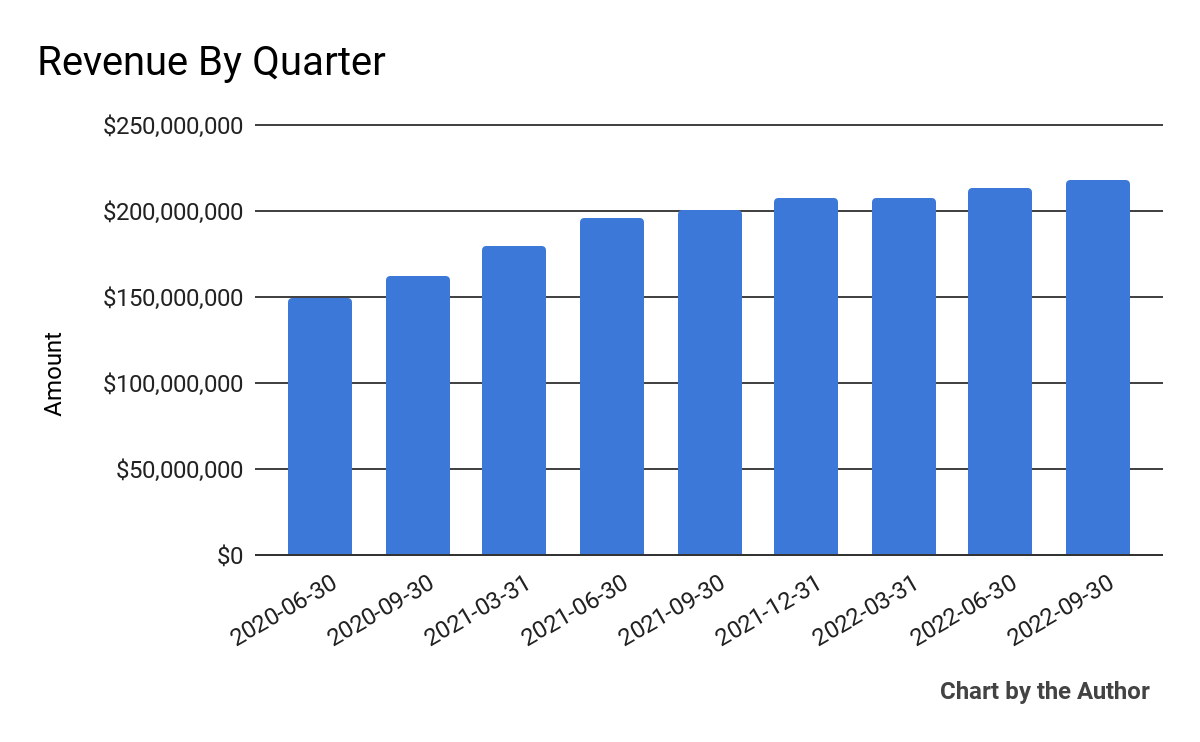

Total revenue by quarter has risen per the following chart:

9 Quarter Total Revenue (Financial Modeling Prep)

-

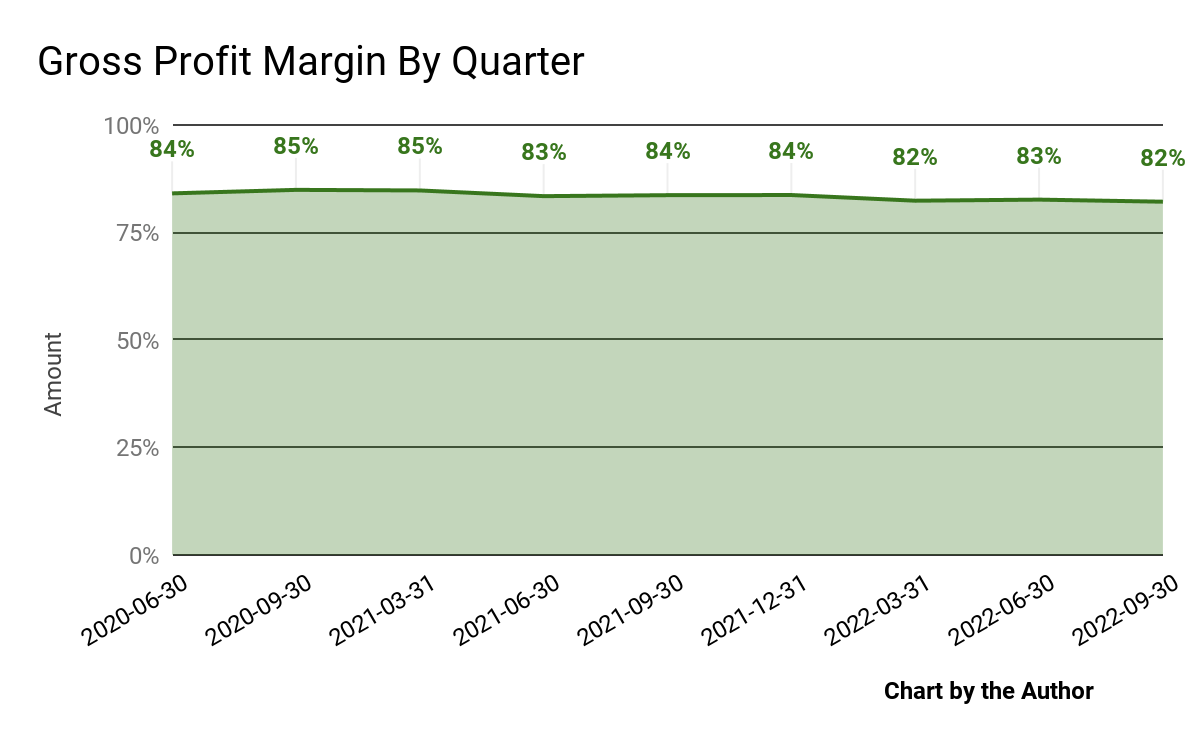

Gross profit margin by quarter has trended lower in recent reporting periods:

9 Quarter Gross Profit Margin (Financial Modeling Prep)

-

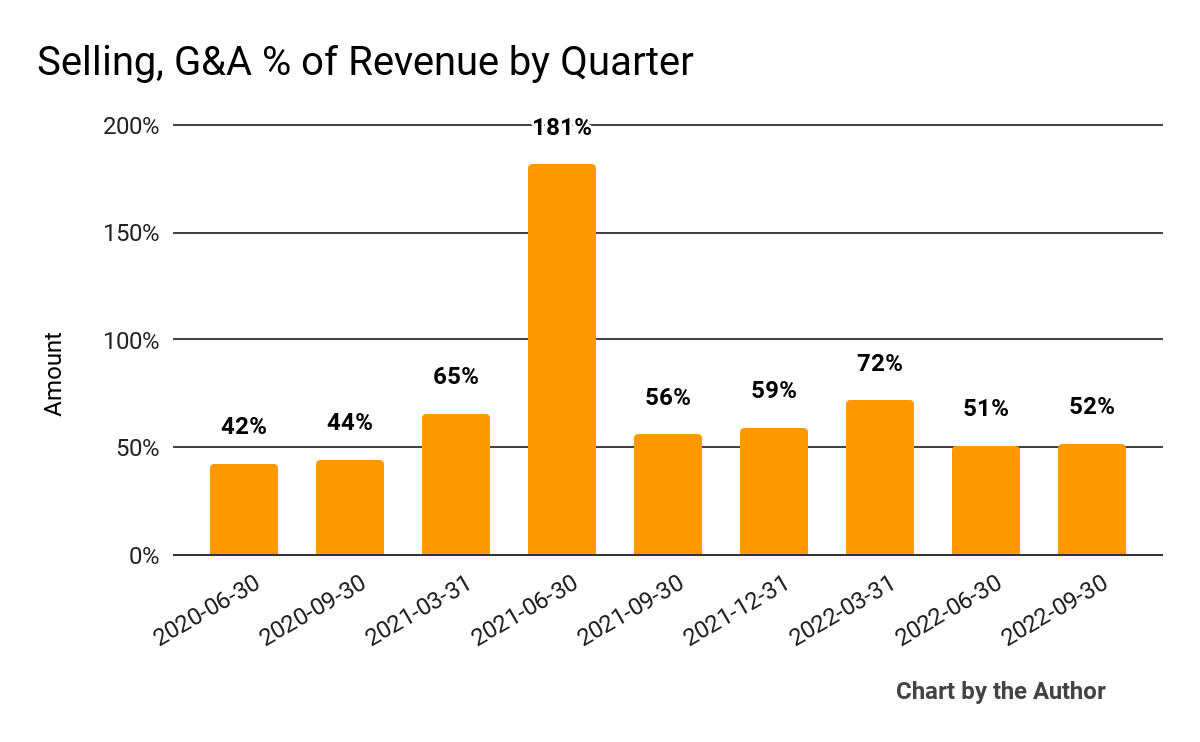

Selling, G&A expenses as a percentage of total revenue by quarter have fluctuated as follows:

9 Quarter Selling, G&A % Of Revenue (Financial Modeling Prep)

-

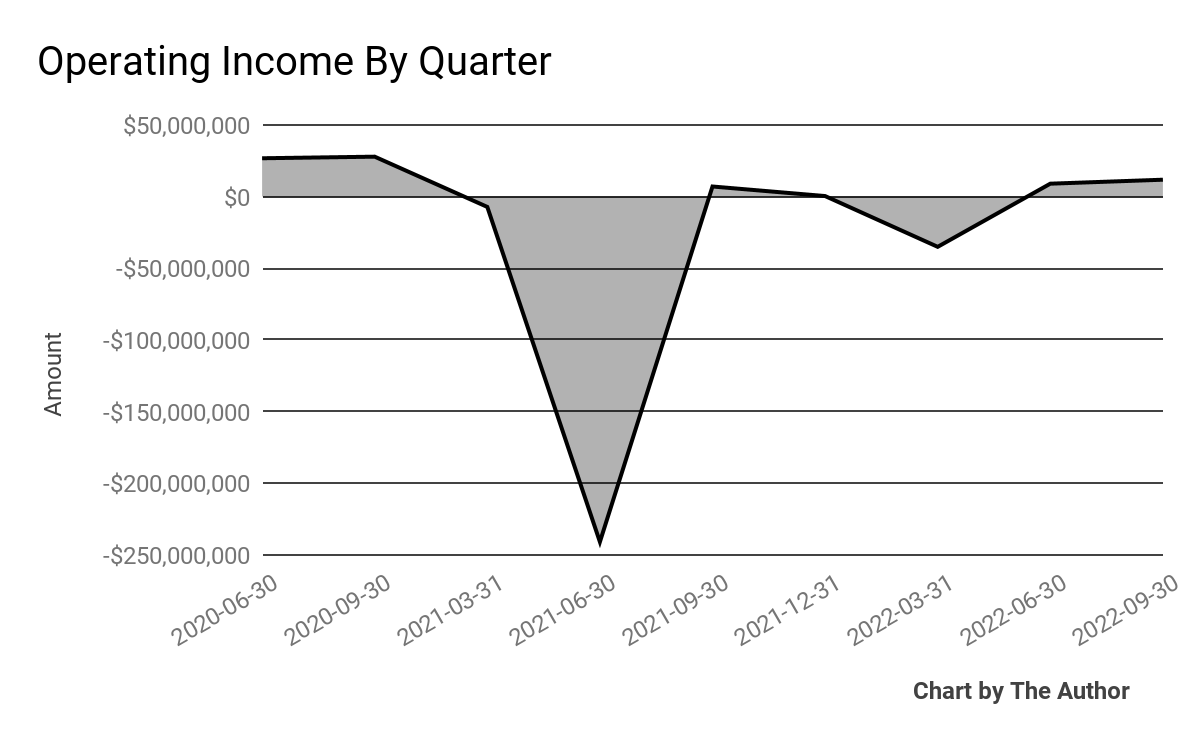

Operating income by quarter has produced the following results:

9 Quarter Operating Income (Financial Modeling Prep)

-

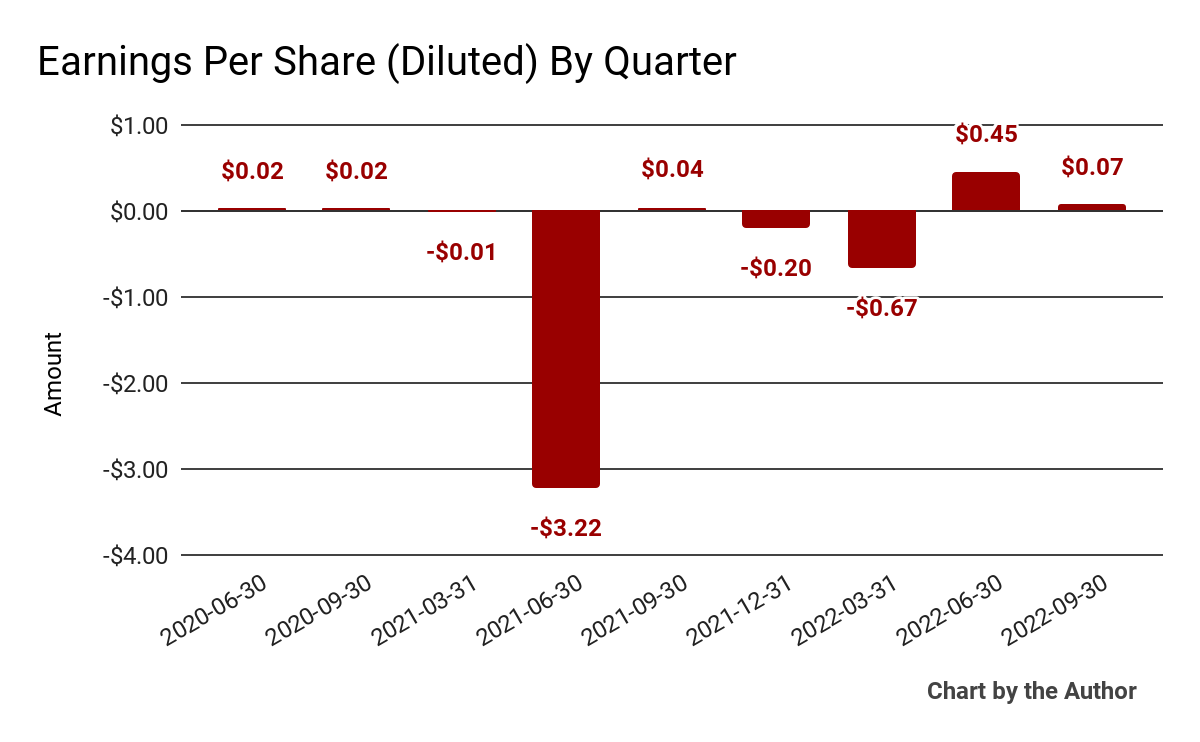

Earnings per share (Diluted) have fluctuated materially in recent quarters:

9 Quarter Earnings Per Share (Financial Modeling Prep)

(All data in the above charts is GAAP)

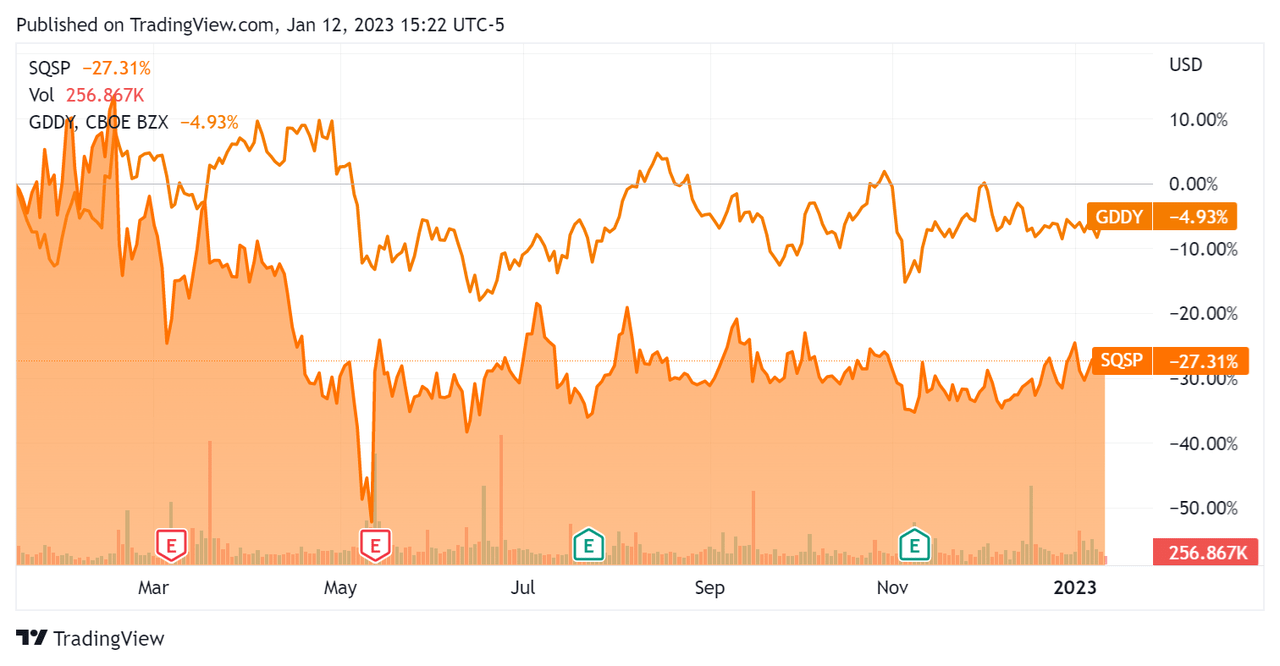

In the past 12 months, SQSP’s stock price has fallen 27.3% vs. GoDaddy’s drop of around 4.9%, as the chart below indicates:

52-Week Stock Price Comparison (Seeking Alpha)

Valuation And Other Metrics For Squarespace

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

4.1 |

|

Enterprise Value / EBITDA |

99.2 |

|

Revenue Growth Rate |

14.4% |

|

Net Income Margin |

-4.1% |

|

GAAP EBITDA % |

4.2% |

|

Market Capitalization |

$3,029,416,192 |

|

Enterprise Value |

$3,492,001,517 |

|

Operating Cash Flow |

$140,107,000 |

|

Earnings Per Share (Fully Diluted) |

-$0.35 |

(Source – Financial Modeling Prep.)

As a reference, a relevant partial public comparable would be GoDaddy Inc. (GDDY); shown below is a comparison of their primary valuation metrics:

|

Metric [TTM] |

GoDaddy |

Squarespace |

Variance |

|

Enterprise Value / Sales |

3.5 |

4.1 |

18.3% |

|

Enterprise Value / EBITDA |

19.8 |

99.2 |

401.4% |

|

Revenue Growth Rate |

10.9% |

14.4% |

32.3% |

|

Net Income Margin |

8.5% |

-4.1% |

-148.2% |

|

Operating Cash Flow |

$943,900,000 |

$140,107,000 |

-85.2% |

(Source – Seeking Alpha and Financial Modeling Prep.)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

SQSP’s most recent GAAP Rule of 40 calculation was 18.6% as of Q3 2022, so the firm needs some improvement in this regard, per the table below:

|

Rule of 40 – GAAP [TTM] |

Calculation |

|

Recent Rev. Growth % |

14.4% |

|

GAAP EBITDA % |

4.2% |

|

Total |

18.6% |

(Source – Financial Modeling Prep.)

Commentary On Squarespace

In its last earnings call (Source – Seeking Alpha), covering Q3 2022’s results, management highlighted the firm’s recent price increases as a rolling benefit from annual customer renewals as they come due.

However, the company is seeing soft demand from its Unfold social media-optimized content offering. Management plans to continue expanding the capabilities of Unfold to bolster the value added from this service.

ARPU rose 4% to $206, while the company continues to focus on international expansion through the localization of its platform.

As to its financial results, total revenue rose 8.3% but was negatively impacted by foreign exchange headwinds from a strong U.S. dollar. The dollar has weakened since the end of Q3, so these Forex headwinds should abate over time.

Management did not disclose specific company retention rate metrics other than to say churn was less than expected.

The firm’s Rule of 40 results have been mediocre, with a moderate revenue growth result helped only a little by a meager GAAP EBITDA result.

GAAP earnings have been highly variable and largely unpredictable for the company over recent quarters.

For the balance sheet, the firm ended the quarter with $228.2 million in cash, equivalents and short-term investments and $517.1 million in total debt.

Over the trailing twelve months, free cash flow was $127 million, of which capital expenditures accounted for $13.1 million. The company paid $98.9 million in stock-based compensation.

Looking ahead, management guided full-year 2022 revenue growth 9.5% at the midpoint of the range.

Regarding valuation, the market is valuing SQSP at an EV/Sales multiple of around 4.0x.

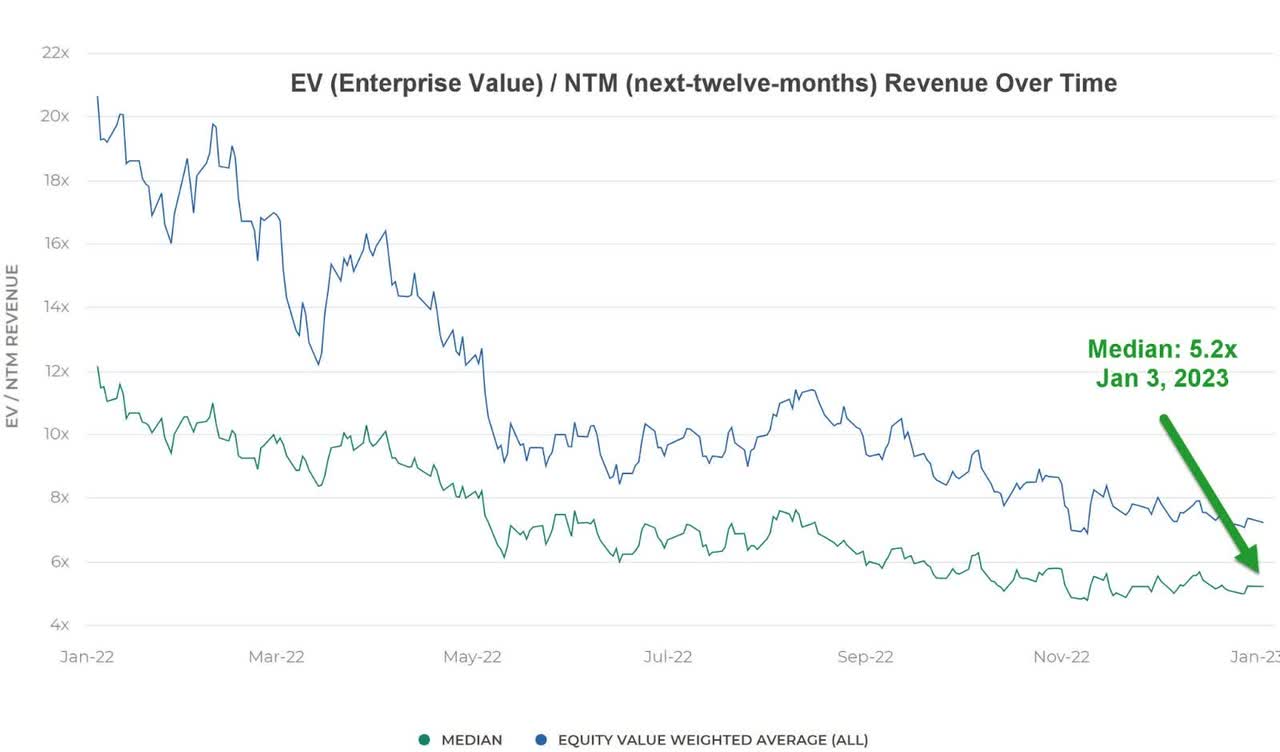

The Meritech Index of publicly held SaaS software companies showed an average forward EV/Revenue multiple of around 5.2x on January 3, 2023, as the chart shows here:

Enterprise Value / Forward Sales Multiple (Meritech Capital)

So, by comparison, SQSP is currently valued by the market at a 23% discount to the broader MeritechCapital Index, at least as of January 3, 2023.

The primary risk to the company’s outlook is an increasingly likely macroeconomic slowdown or recession, which may produce lower conversion rates and reduce its revenue growth trajectory.

A potential upside catalyst to SQSP stock could include a further uptake of its commerce and payments offerings.

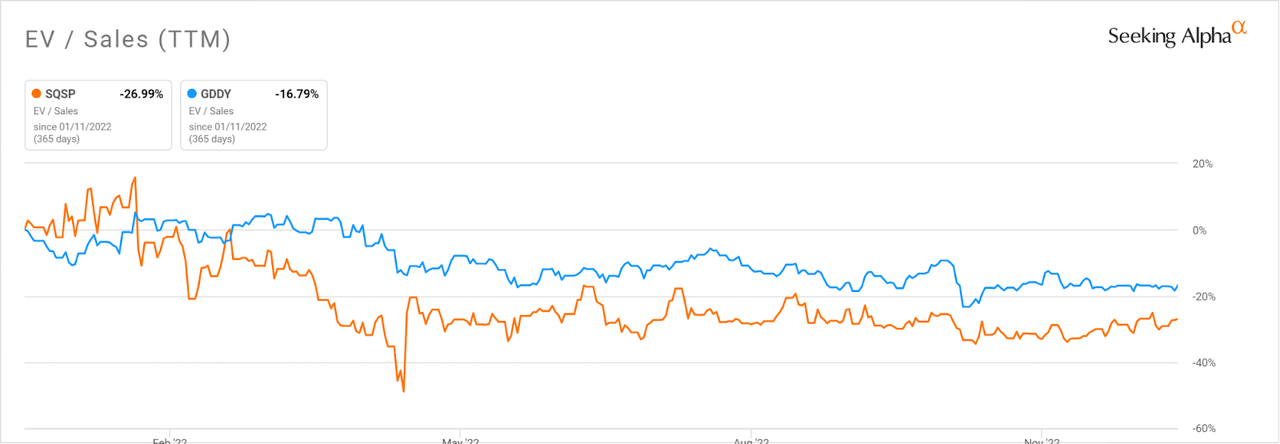

Notably, SQSP’s EV/Sales multiple [TTM] has compressed by 27.28% versus only 16.8% for GoDaddy in the past twelve months, as the Seeking Alpha comparison chart shows here:

Enterprise Value / Sales Comparison (Seeking Alpha)

With management noting a drop in discretionary income hurting the growth of gross merchandise volume [GMV] run through its platform, I’m not optimistic about Squarespace, Inc.’s growth prospects.

Heading into slowing macroeconomic conditions may not be the time to be loading up on a stock like SQSP unless you have a longer-term time horizon into 2024.

I’m on Hold for Squarespace, Inc. in the near term.

Be the first to comment