courtneyk

Thesis

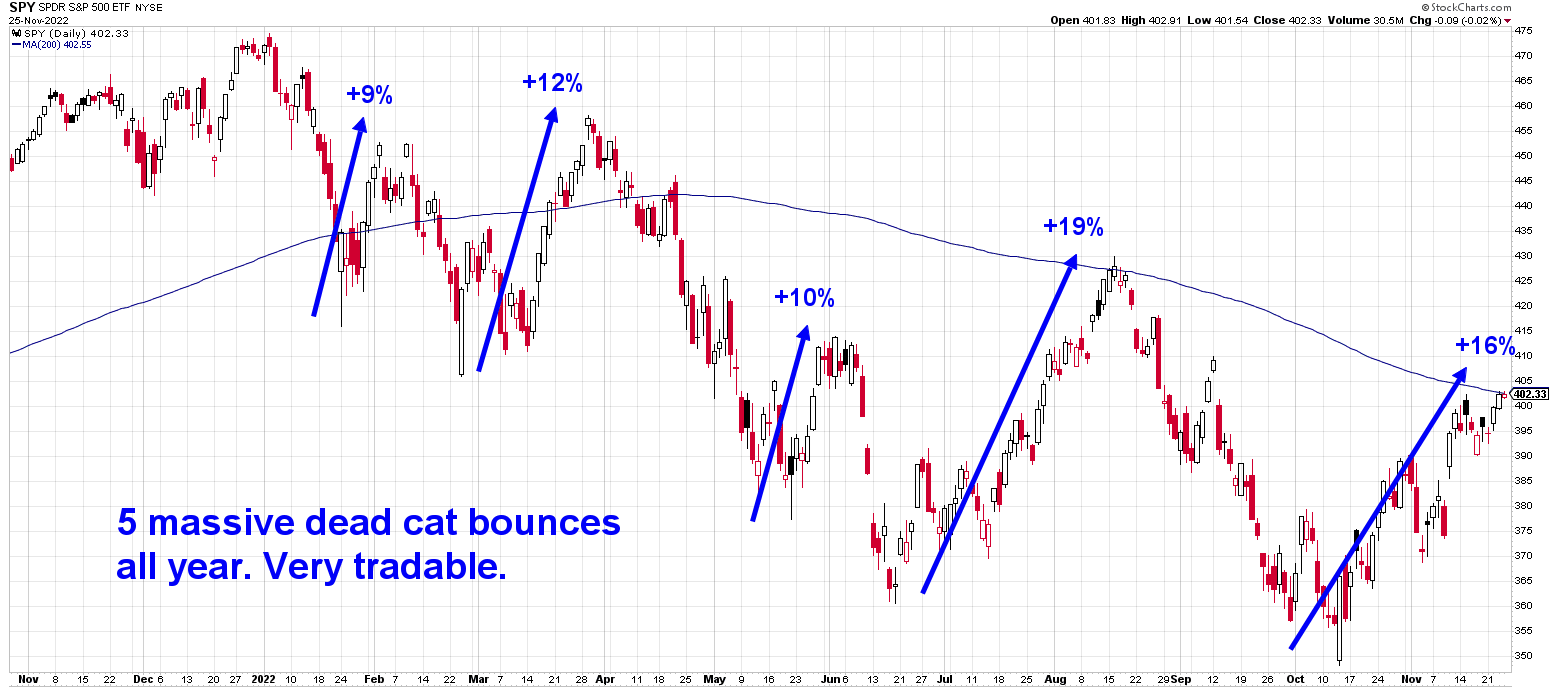

The S&P 500 has been on a roller coaster ride this year:

S&P 500 Graph (The Heisenberg)

We are in a bear market, but against retail investor expectations, a non-linear one. It would be easy to trade a linear down-trending bear market – just short the index or buy puts! Everybody would be making money, and the party would never stop. However, making money in the financial markets is not that simple (otherwise everybody would do it). A bear market develops over time, and bear market rallies are there to sow doubt in investors’ minds and create FOMO (fear of missing out). A true bear market is identified only after a couple of rallies where the market makes lower highs, and the general trend is establishing itself as being lower.

2022 has been a very tough market because just buying puts outright might have not really worked out. What do we mean? Let’s say that an investor thought in January there might be weakness in the market come the new year. And let’s assume said investor would have bought July 2022 SPY puts with a $400 strike. While the general direction would have been correct, unless monetized in time, the options would have expired worthless (the index ended July with a value above $400). The said investor would have benefited from the mark-to-market impact on the portfolio (i.e. smoother and less volatile returns), but would have not made money on the options.

The lesson to be learned here is that an investor cannot always get the timing and strike correctly, while they nonetheless have identified the general trend. So what is a retail investor to do? We believe that an active retail investor can generate positive results and achieve a lower standard deviation in their portfolios by looking at the less known component of options pricing, namely volatility. Instead of choosing the right strike for a put option, an investor can look at the market’s volatility level and decide whether it is low or high in historic terms.

What is the trade?

Instead of trying to figure out where the S&P 500 is going to be in 1-, 2- or 3-months and figure out the correct strike to use, an investor can look at the VIX component of options pricing:

VIX Range (Google Analytics)

The VIX index has exposed a very nice range this year, correlated with the bear market rallies. Volatility is the second most important input in options pricing, and a low VIX level means options have a low premium, while high VIX levels translate to expensive options.

We think volatility is unusually low and will spike at some point. Rather than guesstimate where the index price will be, an investor can speculate that volatility will be much higher come Q1 of 2023. The best way to monetize this view is with extremely out of the money options with low delta (i.e. the spot price does not affect them that much) but high vega figures:

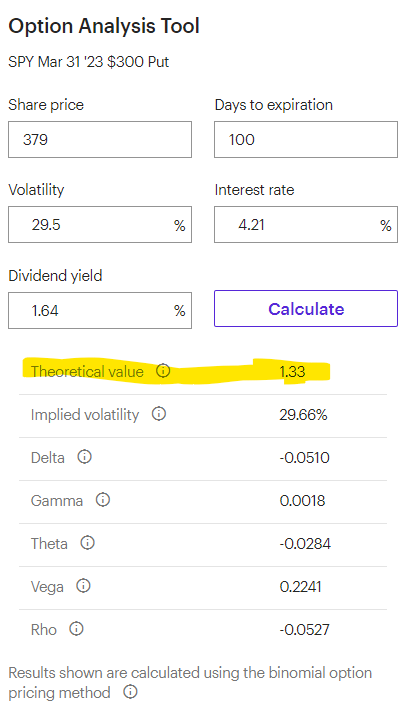

Matrix (MarketChameleon)

If we look at the March 31st, 2023 expiries for example, we can choose a round number, namely the $300 level. That represents a -21% spot level from current pricing. The respective option has a low ‘Delta’ (i.e. sensitivity to spot prices) because it is extremely out of the money. In English, this purely means that the market has to lose a lot of money in order for that option to be triggered.

Ok, then how can we profit if we don’t think the S&P 500 is going to 3000? Well, what we are saying above is that we do not need the S&P 500 to go to 3000, we just need volatility to spike in order to make money on this put option. Let us have a closer look:

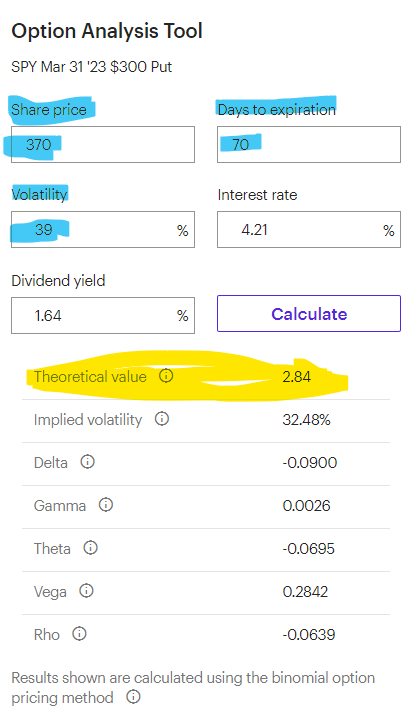

Put Pricing (Author / E-Trade)

So this is roughly how the option looks today where we pay $1.33 per contract for this maturity and strike. What we are saying here is that we do not know where exactly the index is going, but we expect volatility to spike. So let’s assume we are somewhere end of January 2023 and volatility has spiked, while the index has moved down in value only a little bit:

Put Pricing (Author / E-Trade)

In blue we have highlighted the assumptions made (market sells off by only -2.5%, days to expiration decrease to 70, but volatility spikes to 39%). We can see how the price of the option has nonetheless doubled!

We do not need to get the strike right, or the timing here! We do not really care where the index ends up end of Q1 2023, but we do think volatility right now for the index is too low and it will end up spiking higher.

An active retail investor can target 2x or 3x the premium invested as a profit utilizing this strategy, with the caveat that it is an active trading one, not a buy and hold trade.

Conclusion

The S&P 500 performance has not been linear this year, despite the ongoing bear market. The wave pattern exposed by the index in a larger downtrend, has resulted in a nice range for the VIX index. The VIX is an equity volatility index, and volatility is one of the main components for options pricing. While we do not know exactly where the S&P 500 will be at the end of Q1 2023, we do believe volatility is too low right now. A tremendous amount of money has been lost this year by trying to guess the correct timing and strike levels for the index. We are of the opinion that this is not the correct approach, and the best way to take advantage of the current bear market is via long volatility trades. The best expression of such a trade would be buying a deep out of the money put option on the S&P 500 (a $300 strike in our example) with a March 31, 2023 expiration date. An active retail investor would look for volatility to spike and for the option premium to double or triple before exiting the trade. The proposed strategy is not a buy and hold one, but a hedging trade for an active investor looking to take advantage of the unusual low levels in the VIX.

Be the first to comment