bunhill

The SPDR S&P 500 ETF (NYSEARCA:SPY) has had a solid start to 2023. We updated investors at the end of 2022, postulating that the SPY has legs in the new year, even as Wall Street strategists downplayed the potential for a new bull market.

Accordingly, the S&P rallied from its December lows of 3,765 to its recent January highs of 4,015 before the pullback, notching a gain of about 6.6% over the past three weeks.

However, with the SPY’s near-term breadth and momentum indicators surging toward overbought zones, we assessed that the SPY is due for a momentary pause before potentially marching higher.

Hence, savvy investors who capitalized on the double-bottom October lows have been duly rewarded. However, while those lows looked constructive on SPY’s price charts, pulling the trigger against extreme pessimism fanned by October’s doom and gloom headline news could have proved challenging for newer investors.

As such, we often espouse investors to not read too much into the news to make investing decisions. We believe the market is a forward discounting mechanism. By the time the media report such extreme sentiments (euphoria or capitulation), astute market operators likely have already reflected them.

So, where are we now relative to the market’s positioning?

Interestingly, while the market started with a relatively pessimistic tone pre-December CPI report in January, market sentiments have improved lately.

The IMF has turned less downbeat over its macroeconomic outlook from its previous assessment in October. Notwithstanding, the World Bank continues to see risks to its global outlook.

Despite that, Europe could potentially avoid a hard landing, with Germany possibly dodging a recession, coupled with an industrial and consumer recovery underway.

Inflation indicators have also continued to fall markedly, with BlackRock’s (BLK) Vice Chairman Philipp Hildebrand suggesting a “very, very fast” decline. Former Treasury Secretary Larry Summers has also turned less pessimistic, as he sees the US economy potentially avoiding a recession.

As such, the market has already moved to reflect an earlier-than-anticipated Fed pivot, with the 2Y and 10Y Treasury yields moving lower. Notably, the 2Y yield has decreased to 4.11%, and the 10Y yield has fallen to 3.42%. As a reminder, the Fed’s summary of economic projections suggests a median terminal rate of 5.1% to close off 2023 (no pivot) before easing toward 4.1% in 2024.

Hence, it appears that the market has anticipated that the worst of the Fed rate hikes are likely over, which should augur well for green shoots of recovery in the SPY.

As such, media headlines have also become more optimistic as market volatility has subsided.

Therefore, we believe the critical question investors need to assess is whether the current rally is sustainable?

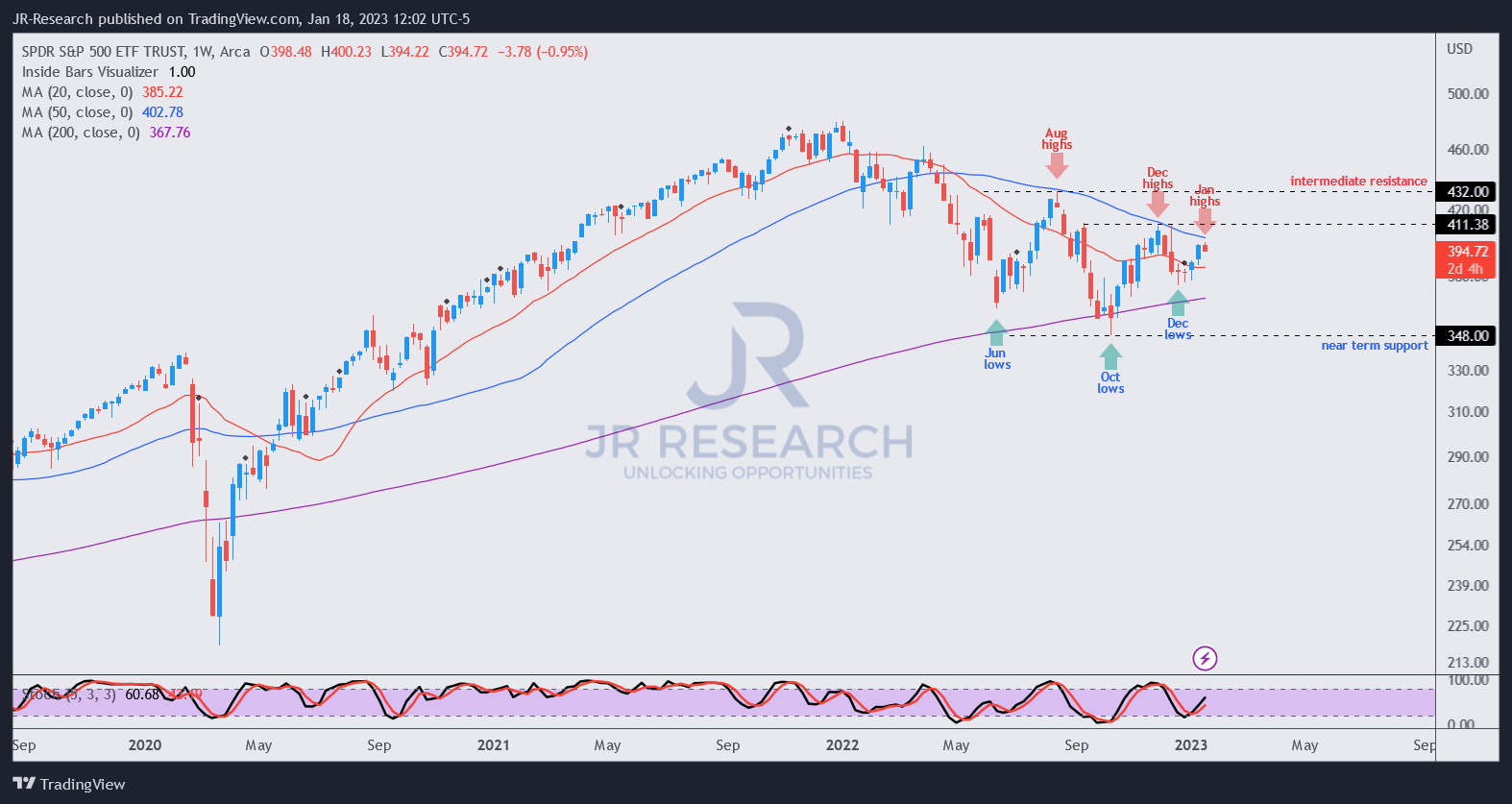

SPY price chart (weekly) (TradingView)

With the SPY hovering under its December bull trap highs, it has met resistance against its 50-week moving average (blue line). Hence, we assessed that the SPY is at a critical juncture, with buyers needing to prove their resolve to retake December highs before a re-test of August highs is possible.

Why is this zone critical? Note that with the recent upward recovery, the price action has corroborated SPY’s December lows as a higher-low price structure, affirming October’s double-bottom as a solid base. Hence, we could be in the early stages of a sustained market recovery, even though it’s likely to remain uneven.

So, what could potentially thwart this recovery, leading to another bull trap and forcing the SPY to break below its October lows decisively?

The initiative remains with the sellers, with bears leveraging the hawkish Fed thesis and believing that the inverted yield curve point to a recession, not a false dawn.

Moreover, these bears believe that China’s economic recovery could continue to stumble, with the recovery in its domestic consumption worse than expected, as consumers are expected to remain low on confidence. As such, the positive impact of the Chinese economy could have been overstated, even as China’s policymakers lift their expectations of China’s recovery prospects.

These bears argue that the Fed will likely not pivot even though the US economy could still enter a recession, as the central bank is committed to driving down inflation rates while keeping financial conditions sufficiently tight.

As such, with no Fed pivot expected until 2024, these investors believe it’s still too early to determine that the SPY has bottomed out as sellers remain in control.

Our take is shaped by what we assessed as a mild-to-moderate recession already contemplated at the SPY’s October lows.

As such, with the leading US banks corroborating our thesis of such a scenario in their recent earnings commentaries, it has increased our conviction that we have moved past the trough in SPY’s price action.

Moreover, global markets have experienced remarkable breadth thrusts in unison that are not emblematic of a continuation of bear market behavior. Coupled with a Chinese government committed to returning its economy to growth this year, the headwinds pushing the SPY back to its October lows are likely getting weaker.

Notwithstanding, we believe that a short-term pullback is imminent for the SPY before subsequently moving higher.

Investors considering an opportunity to add should consider leveraging pullbacks and avoid chasing into momentum surges.

Rating: Buy (Reiterated).

Be the first to comment