allanswart/iStock via Getty Images

Investors can soon say good riddance to the historically challenging 2022, although we see several reasons to turn positive on the S&P 500 (NYSEARCA:SPY) heading into the new year. From what has been a mixed bag of indicators in recent months and the recurring volatility, our message is that the equities market is alive and well with the potential for positive returns going forward. Stock market doom-and-gloomers have been making a lot of noise lately, but today we want to highlight a series of charts that support a more bullish case for stocks.

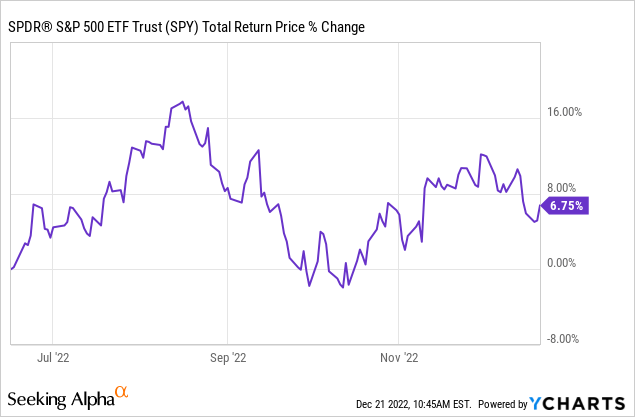

Stocks Are Up From Levels In June

The first chart today serves as some food for thought as we close out 2022. Simply put, the S&P 500 is up 7% from its level in June and also 11% higher compared to the brief intraday low in October. For all the bearish calls about a “big crash lower”, the trading action really hasn’t reflected an apocalyptic scenario or developing stock market crash.

Sure, the S&P 500 is on track to end the year down by double digits near a bear market, but by all indications, the bulls have had some momentum on their side over the last several months. Investors don’t have much to celebrate this year, but outside of short sellers that made the move early in Q1, bears should consider re-corking that champagne bottle with the bigger risk that we ultimately break out higher, in our opinion.

Inflation Is Crashing

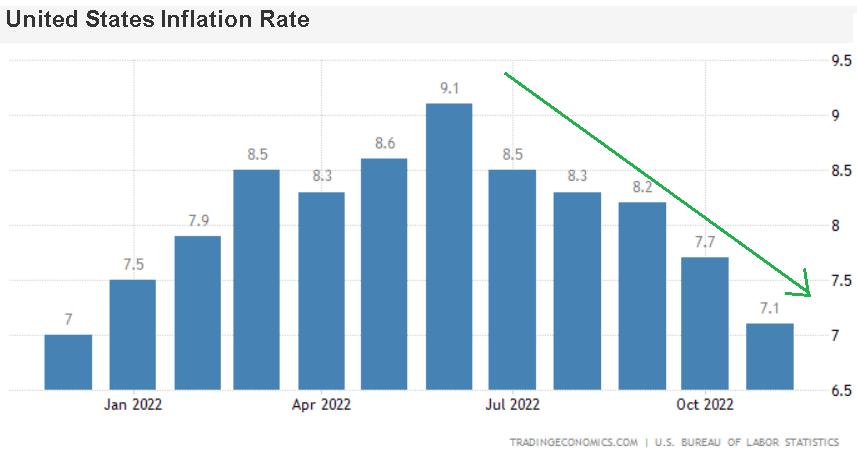

By all accounts, the latest November CPI inflation rate at 7.1% is alarming and even an embarrassment to the Fed that held onto the “transitory” messaging for too long in 2021. On the other hand, the bigger point is that the setup has improved significantly from where we were back in Q2 when the CPI hit 9.1% and there were significant uncertainties related to the key components of the consumer price basket.

The figure to watch is the month-over-month rate that was last reported at +0.1% in November and has averaged just 0.2% since June. This implies a forward inflation rate near 2.4% which is getting close to that mythical 2% Fed target.

The main drivers of inflation being commodity and energy prices, along with global supply chain disruptions, have nearly completely reversed which is a much more favorable backdrop into 2023. Think back to the early stages of the Russia-Ukraine conflict in Q1 when calls for oil (USO) at +$200 a barrel were taken seriously. Get WTI crude back above $120 and then we have a problem.

source: tradingeconomics

Incredibly, the national average for a gallon of gasoline is down over the past year which now represents a tailwind for consumer spending and even corporate margins. In many ways, this apparent windfall helps to balance out the impact of higher interest rates. With those cost constraints easing, the urgency for companies to keep raising prices gets brushed aside.

We’ve written before how the Fed is playing it extra cautious, in an attempt to rebuild its credibility, which has translated into the uber hawkish messaging. That said, over the next few months as the headline inflation rate adjusts lower to reality, the long-awaited pivot to a more dovish approach will be justified based on the inflation data as a positive tailwind for stocks. This is different from a shift in policy if the economy was collapsing.

Consider that the inflation rate between January and March of 2022 was exceptionally strong, accelerating from 7% to 8.5% at the time. The result is that the tough comparison period will make a meaningful impact on driving the headline annual rate lower through the base effect. Sentiment should get a boost as the annual rate trends under 5%. Again, “prices” are never going back to pre-pandemic levels, but the success in just stabilizing as part of the Fed mandate may be a very strong catalyst for risk assets into 2023.

The Job Market Is Stable

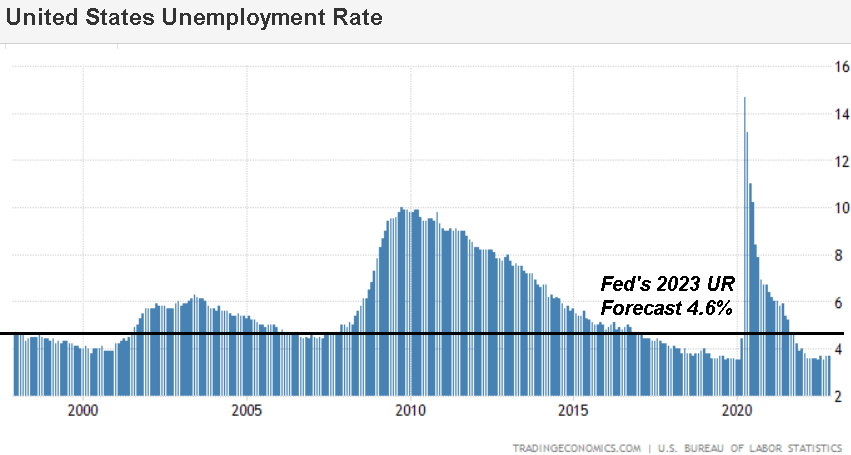

If we wanted to put together a bearish case for stocks going forward, the thesis would likely start with an outlook for a complete deterioration of economic activity accompanied by a surge in unemployment. Indeed, payrolls have outperformed in recent months which is a far cry from fears of widespread layoffs. Beyond headlines of specific and high-profile companies looking to cut costs and reduce headcount, there isn’t any indication of a labor market crisis.

Even the Fed’s forecast for the unemployment rate to tick higher in 2023 to 4.6% from a current 3.6% is still at a historically low level. Consider that some of that dynamic will include an expected rising participation rate with more people reentering the labor market from the pandemic exit, and not necessarily implying “millions” of job losses.

The current consensus for December payrolls stands at +200k jobs, to be reported the first week of January, compares to the average monthly jobs increase of +164k for 2019 as a pre-pandemic benchmark. The way we see it, the job market has been normalizing compared to historically tight conditions in 2021, which also ends up being favorable to inflation dynamics.

source: tradingeconomics

Anyone waiting for breadlines to form down the main street as a signal corporate earnings are collapsing will need to keep moving that goalpost. Our argument against the oft-repeated line that the Fed has never hiked interest rates to bring down inflation, without starting a recession is that the connection suffers from a very limited time series that hardly suggests a statistical significance. It’s fair to say that the circumstance this year is different.

All this plays into the scenario of a soft landing for the U.S. economy where economic activity at least remains resilient, despite higher interest rates. The outlook for inflation trending sharply lower will lead to an entirely new narrative over the coming months.

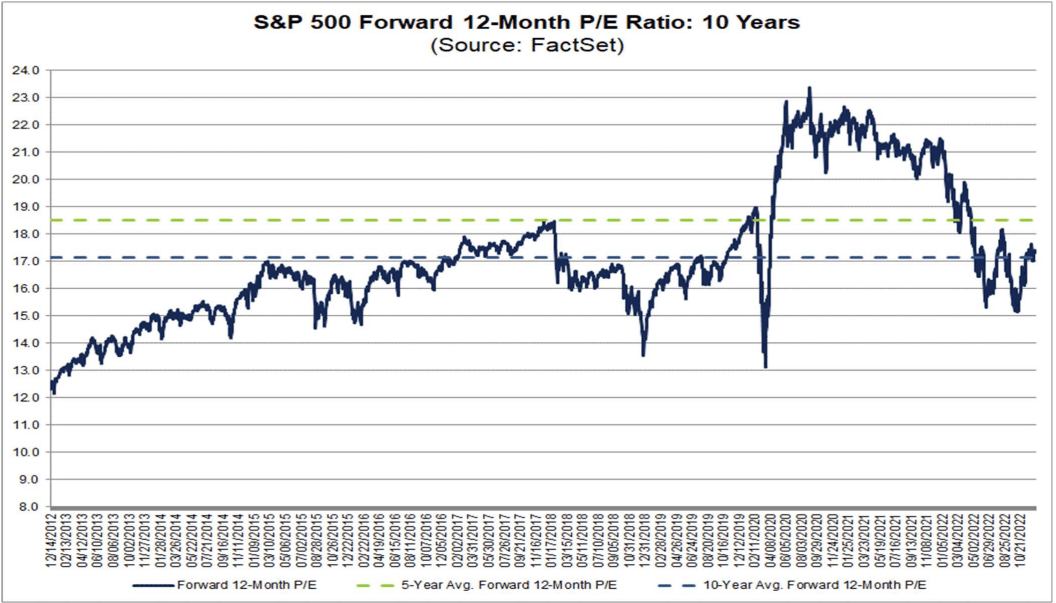

Valuations Are Cheap

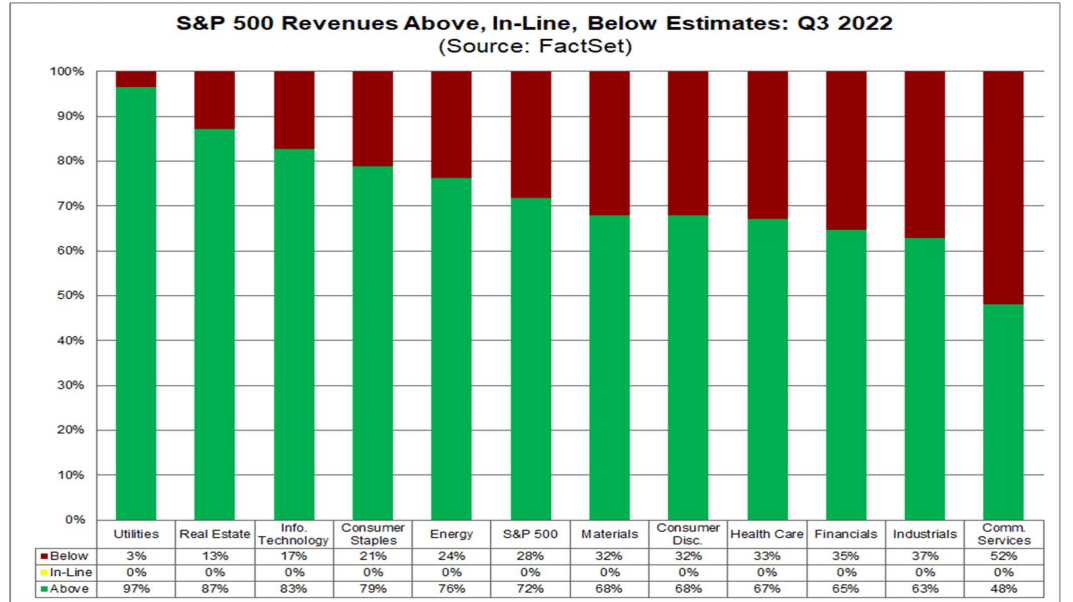

Continuing with our theme, any call for stocks to crash lower and effectively make a new cycle low will have to contend with an expectation of rising earnings into next year and otherwise compelling valuations. A theme from the Q3 earnings season was that 70% of companies across most sectors were able to beat EPS expectations.

source: factset

That trend has continued with the latest results from names like Nike Inc (NKE) and FedEx Corp (FDX) which just reported this week and surprised to the upside. The bears need this earnings momentum to reverse which isn’t happening. Going back to the inflation trends, lower costs are positive for margins as a new tailwind into 2023 compared to results that were more pressured at the start of 2022.

According to the consensus, S&P 500 bottoms-up EPS, as an aggregate of all the underlying index companies, is seen climbing 5% to $231. Considering the current index level of just under 3,900, the setup implies a forward P/E of 16.9x which is below the five and ten-year average for the metric.

Within the S&P 500, a major component like Amazon.com Inc (AMZN) capturing a wave of stronger economic data while benefiting from rising margins over 2022 can lead the index higher. This is one stock we are particularly bullish on that is well-positioned to outperform in 2023.

One takeaway here is that stocks are far from being “a bubble”, which may have been the case at the end of 2021, although the selloff has largely corrected that imbalance. A setup where interest rates stabilize and inflation surprises lower will make stocks appear increasingly cheap, particularly if economic indicators and corporate earnings continue humming along.

source: FactSet

Downside To Interest Rates

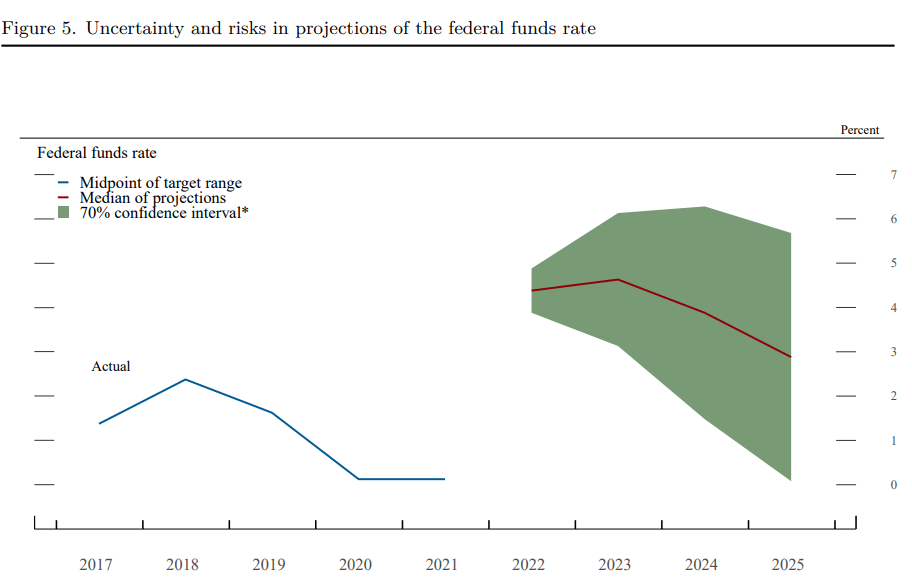

Following the string of 75 basis point rate hikes since Q2, the December FOMC last week featured a moderation to a 50 basis point hike. A big discussion in the market right now is how high the Fed will go with further increases and that uncertainty explains some of the recent market volatility.

Our message here is to keep in mind that all Fed forecasts and messaging are “dynamic” meaning they constantly evolve based on the latest data. In this regard, we believe some bears may be making the mistake to read every Fed speak sentence as if it were written in stone or not recognizing the potential for a more favorable outcome. Bears are probably also wrong to dismiss the possibility that inflation surprises lower.

Specifically, the key data point the market appears to be fixated on was the updated “median of projections” to the Fed Funds Rate moving to 5.1% as a terminal rate. That said, notice that the Fed’s own materials include room for a downside to this point estimate within a 70% confidence interval.

In our view, another “cold” CPI print for the December and January data below expectations could be a game changer in terms of resetting the messaging and getting that holy grail red line to tick lower. Again, this not because the economy is collapsing, but because of the better-than-expected inflation trajectory confirms success in bringing down inflation.

source: St. Louis Fed

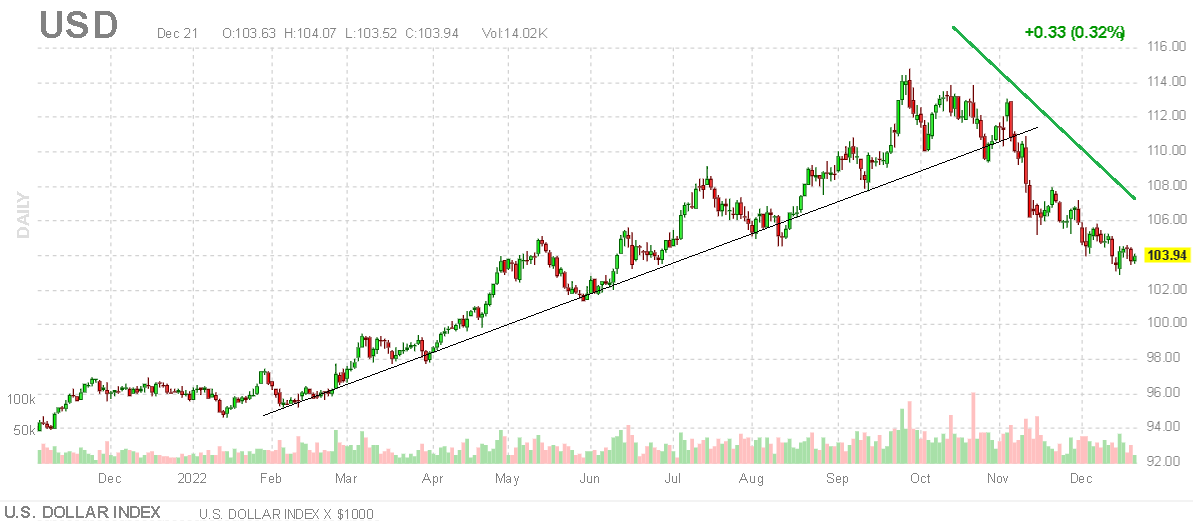

It’s telling that long-term interest rates like the 10-Year Treasury yield have corrected lower in recent weeks to a current level at 3.6%, down from a cycle peak of 4.3% in late October. Our interpretation is that the market is recognizing the lower long-term inflation expectation that will provide room for the Fed to eventually cut rates. This scenario would be positive for equities and risk assets into a new regime towards 2024.

The action is already playing out in the U.S. Dollar Index, which has made a major move lower since peaking in September also corresponding to a rally in the Euro and Japanese Yen. This development is positive for global financial conditions and trade activity that highlights an improving scenario heading into 2023. Finally, we can point to the end of “zero-Covid” policies in China as an encouraging turn of events that is positive for the broader global economy.

source: finviz

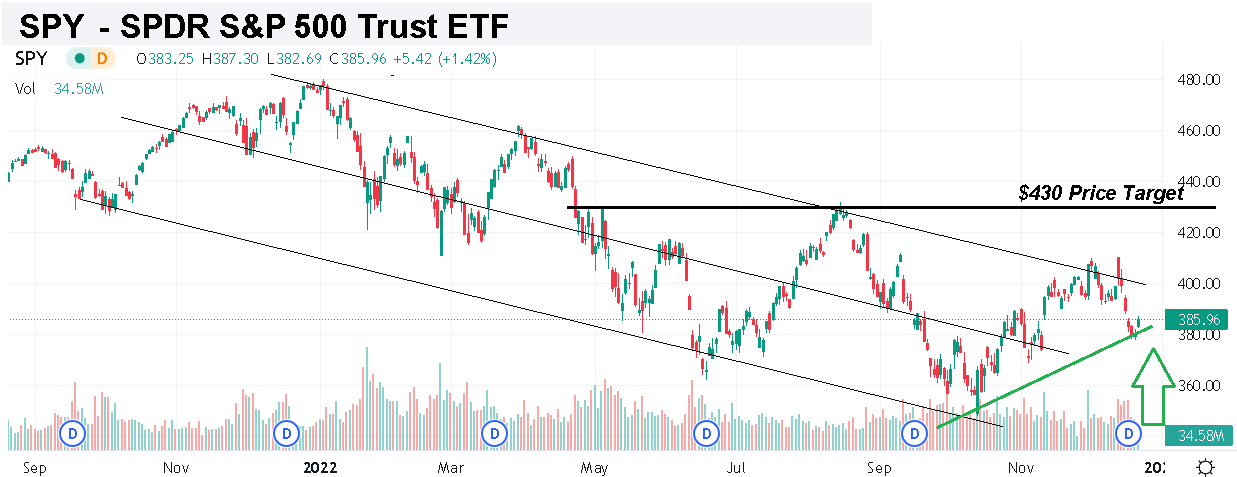

SPY Price Forecast

Ultimately, inflation is the most important indicator that will set the stage for the next steps in Fed policy and macro sentiment as the drive for stocks. We reiterate a price target for the S&P 500 at 4,300, corresponding to around $430 for the ETF over the next six months.

We don’t claim to have a crystal ball but our bullish call on the S&P 500 is simply based on a conviction that the SPY ETF will be trading higher over the next year with a greater than 66% chance. As a tactical or strategic trade, we’ll take those odds every day. Within the underlying holdings, the best opportunities are likely in tech and high-growth segments that have been beaten down but are well-positioned to reprice higher.

In terms of risk, all eyes are on the situation in Ukraine which remains volatile. The baseline for the ongoing imbroglio to continue at least generates less uncertainty. On the other hand, a scenario where the conflict escalates into Europe would force a complete reassessment of the outlook, which we still view as unlikely. Notably, the possibility that crude oil sharply rebounds to levels above $120 per barrel would also drive a resurgence of inflation undermining the bullish case for stocks.

Seeking Alpha

Be the first to comment