T. Pleydell/iStock via Getty Images

Trading psychology has always been a key factor separating the winners from the losers when it comes to market timing. And various studies have shown that the vast majority of traders usually end in failure. As we emerge from the bear market of 2022 accompanied by encouraging evidence of disinflation and a forceful rebound in the S&P 500 Index (SP500), it might be worthwhile to revisit and study the psychology that was prevalent during the bear market.

In this article, we shall focus on the psychological aspects of trading with an emphasis on behavioural biases. We discuss how these biases may have contributed to the overwhelming urge to time markets and lured traders into making suboptimal decisions. More specifically, we discuss why the odds are heavily stacked against the bears over time, and how the bears risk being left behind by a bull market once again.

What Separates Speculative Trading From Investing

Before we dive into a discussion on trading psychology, it might be a good idea to define what exactly separates speculative trading from disciplined investing. Because there are no existing rules that clearly separate the two, we offer our own set of criteria as a guide. We generally differentiate between speculative trading and investing based on three criteria: 1) the holding period of a position, 2) the basis for making a trade, and 3) how the expectations of returns are formed.

Generally, speculative trading involves short holding periods ranging from intraday to months, while investments usually require holding periods that stretch over multiple years in order to allow the value of an asset to grow and appreciate over time. Speculative trading also typically involves ideas that are not based on statistical evidence or economic fundamentals. This is closely linked to having short holding periods, as economic fundamentals take time to materialise while higher frequency data tend to be noisy and statistically less meaningful. Finally, the returns from an investment are usually based on expectations derived from fundamental shifts in macroeconomic trends or the future prospects of a company. And these changes also take time to materialise. The returns from speculative trading, on the other hand, are usually based on predictions of how the market will behave or react in the short term, and that behaviour tends to be more sentiment driven.

The Main Plot Driving The Pessimism

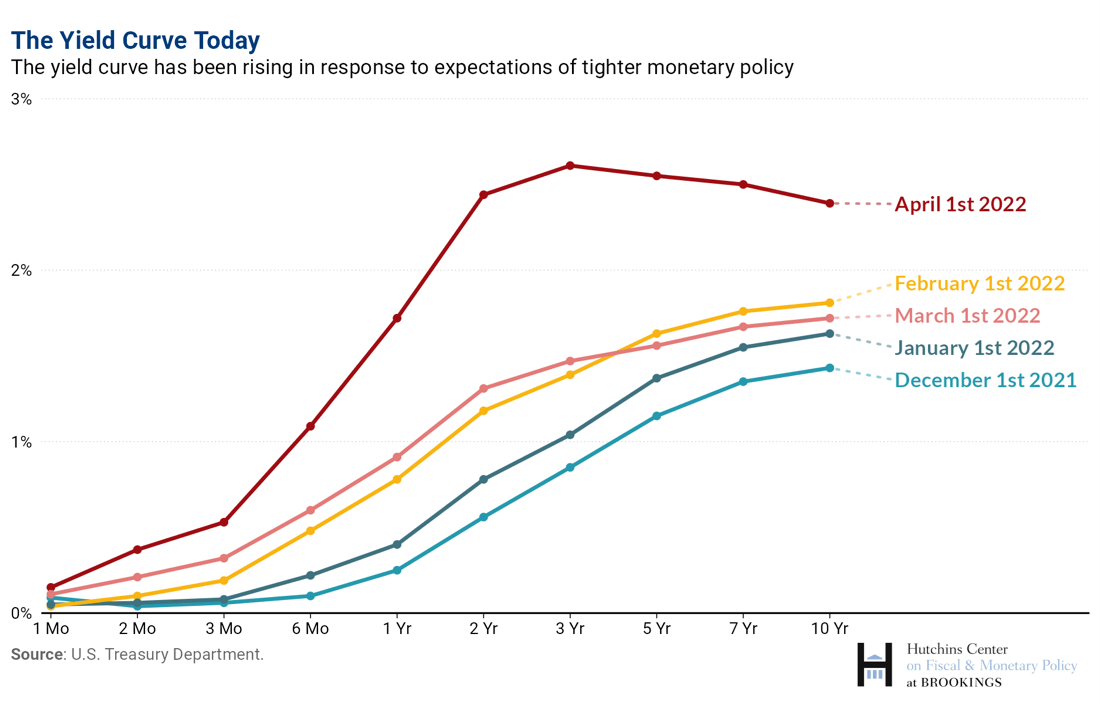

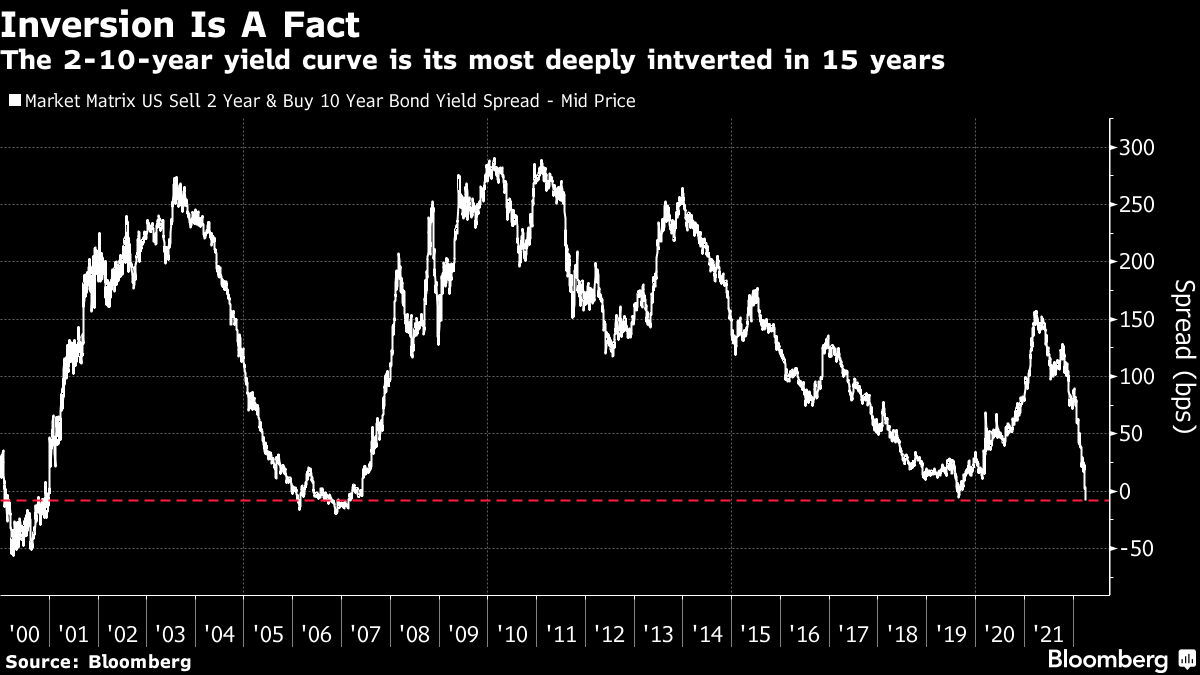

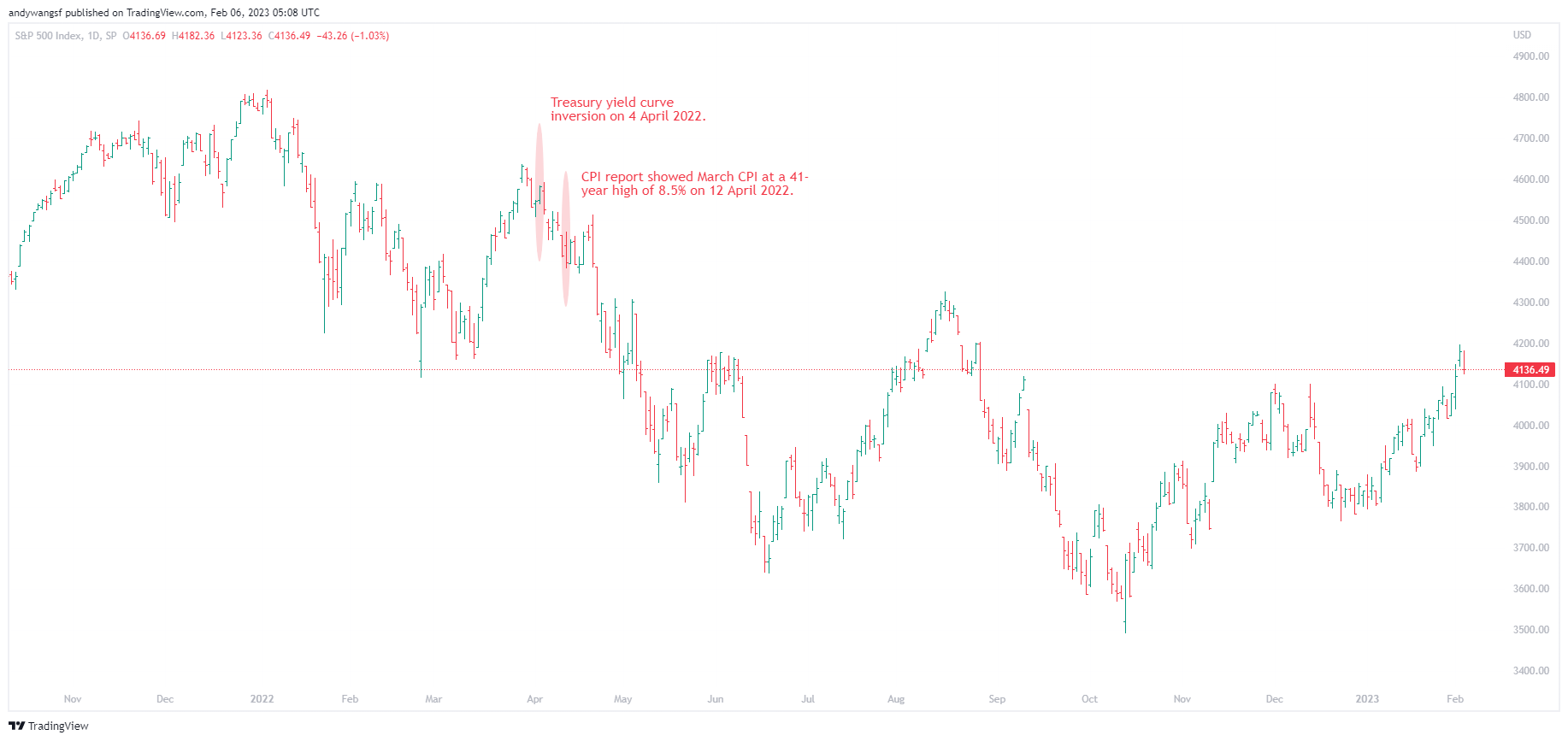

If we look back at 2022, the main reasons that encouraged the bears to dump equities were quite clear. The financial media was constantly flooding the market with news that inflation had surged to four-decade highs, evoking memories of the stagflationary era of the 1970s. There was also widespread agreement among economists that the Federal Reserve will have to hike rates aggressively to bring inflation back to its 2% target. So much monetary tightening had to be done by the Fed that the doomsayers claim that there was no chance that the U.S. economy could possibly escape a deep and painful recession. Meanwhile, the inversion of the yield curve, which has a near-perfect track record at signalling past recessions, was once again signalling a recession as early as April 2022 (see chart below).

Hutchins Center on Fiscal and Monetary Policy Bloomberg – April 4, 2022

To the pessimists’ credit, the U.S. economy was indeed in a challenging environment and warnings of a recession were strongly supported by historical evidence from past inflationary periods. Thus, the subsequent sell-off in the S&P 500 was justified given the risk of runaway inflation and that future cashflows from equities were being more heavily discounted due to the expectation of higher interest rates.

TradingView.com

The Bears Were Right On Inflation

One can imagine the immense pressure to dump equities with inflation running at four-decade highs and that the Fed was ready to hike interest rates as aggressively as needed, even at the expense of throwing the economy into a recession. Even the more bullish and optimistic analysts on Wall Street had to concede that equity valuations were overstretched in 2021 and that the downside risks could be quite substantial.

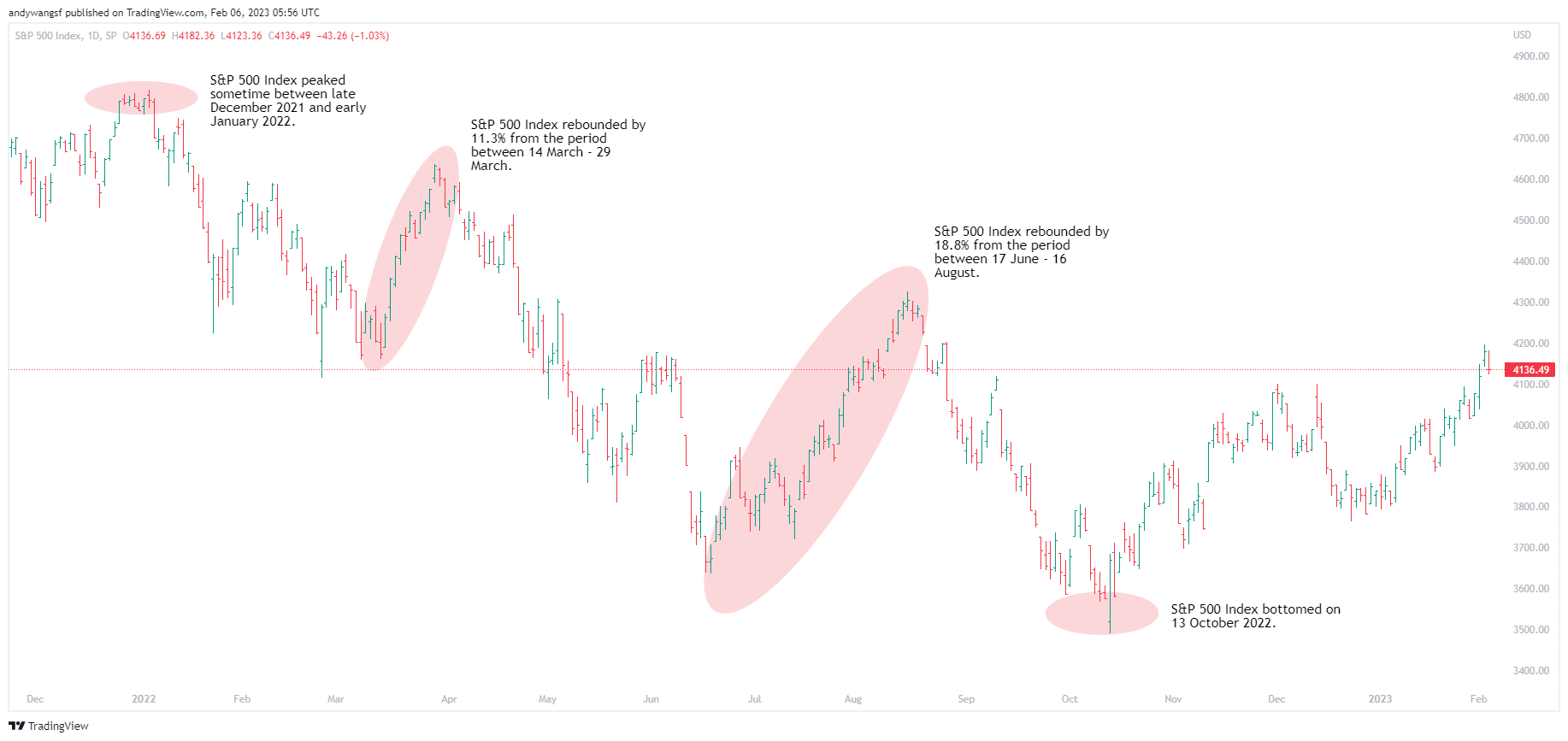

The bears who were already betting that inflation would accelerate and that the stock market would collapse were vindicated. By 12 October 2022, the S&P 500 Index had already entered into a bear market and was down -25% for the year. It was a well-deserved victory for the bears, especially given that they were right on inflation.

But The Bears Were Betting On Something Bigger

Timing the entry right is one thing, but to also time the exit right is quite another challenge. To be able to profit from that -25% move, a bear would have to sell close to the peak in January and be able to stomach the intermittent rebounds along the way. As the accompanying chart shows, maintaining a bearish position on the S&P 500 would entail having to stomach two rebounds of 11.3% and 18.8% along the way.

These rebounds were also accompanied by evidence of increased short-covering activity, which probably suggests that most of the bears did not hold onto their short positions throughout the bear market after all. More likely, there was substantial trading in and out of the market where traders would cover their short positions and attempt to short the market again on rebounds.

TradingView.com

Another point to note is that bearish analysts were calling for a deep recession as justification for taking a bearish stance on the S&P 500, often pointing to downside risks that even more aggressive rate hikes will be needed to tame inflation. Thus, there was no real reason for the bears to take profit during the bear market, especially given that the view of a deep recession had yet to materialize, corporate earnings had yet to decline significantly, and inflation was still too hot for the Fed. Certainly, bearish analysts were betting on something much bigger than the regular 10%-15% decline given the bearish arguments presented in their theses.

Judging from the narrative we have presented above, it seems like the bears were behaving in a manner that was inconsistent with their economic outlook. Or perhaps, the economic outlook had nothing to do with the bears’ decision to short the market in the first place?

Having spent quite a number of years navigating the financial markets and keeping track of calls made by various analysts and fund managers, we have learned never to simply take an analyst’s word for it. Because most traders who identify themselves as a bull or a bear at some point in time rarely maintain that same view for long. Because market sentiment is fluid and traders are free to switch their views at any time, financial markets regularly exhibit noisy price action that resembles a fickle-minded trader who can’t seem to decide to be a bull or a bear.

But if the market changes its view from day to day, then most economic analyses and arguments made in support of a trading thesis would be quite pointless. Regardless of what the economic data says, the market will behave like a voting system and prices will swing independently of fundamentals. Then again, if markets behave independently of fundamentals in the short term, why do traders even bother presenting economic arguments in support of their thesis?

The Real Problem With The Bears Is Psychology

Before we present our arguments on why traders who naturally or unknowingly lean towards being a bear will tend to underperform the bulls over the long run, we first discuss the underlying psychology that makes a trader more likely to identify as a bear.

We argue that the real problem with the bears is not so much about being a sceptic or pessimist on economic fundamentals at any point in time. Rather, it is the innate desire to seek outsized profits from sharp and sudden swings in prices that truly defines a bear. There is a stark difference in the trading psychology that drives a bull versus a bear. And this difference in psychology and approach to trading the market is what determines if a trader is more likely to identify as a bull or a bear.

We think it is reasonable to say that the vast majority of traders were originally “buy and hold” investors at the very beginning of their journey into the financial markets. At the very least, their original intention was to buy shares if a company with favourable prospects and hold those shares with the aim of selling them when prices appreciate in value. But along the way, and after witnessing how fast prices can move on the downside, many traders begin to wonder if they could “time the markets”. The idea was simple: sell when prices get expensive, and buy when prices get cheap. Successfully doing so could mean outperforming the average “buy and hold” approach several times over. Furthermore, trying to avoid losses and giving up hard-earned gains seems perfectly rational. The idea that if one is willing to do more and “work hard” at timing markets one could be more successful than others, feels like the right thing to do too.

Ultimately, it is greed and fear that makes a trader a bear. It is the idea that one could avoid losses by getting out of the market when prices peak and scooping up bargains when prices bottom.

Don’t The Bulls Play By The Same Rules Too?

To be fair, bulls are subjected to the same greed and fear just as bears do. But the incentives to act on those impulses are very different. Because of the way financial markets work, investors are not obliged to sell shares that they own at any point in time. But a short seller has to cover his/her short positions and is liable to cover dividends while they are short. Because of the potential unlimited loss associated with shorting a stock, short-sellers are also vulnerable to a short squeeze.

Even if we consider the bear who doesn’t sell short, but merely exits a long position temporarily with the intention to buy after a pullback in prices, the incentives to act are starkly different. Once again, such trades are only worthwhile if prices do actually fall, allowing the trader to pick up shares at a much lower price, essentially reducing the cost of his/her original investment. But when prices do fall, these traders still face the pressure of picking up shares at the right level. Wait too long and prices could rebound beyond the sale price, buying back shares too quickly means achieving small gains that may not adequately compensate the investor for bearing the risk of missing a rally. In either case, market timing by definition requires precision. The very act of trying to be precise in the short term when financial markets are known to exhibit noisy and random price action in the short term defies logic.

A “buy and hold” investor can hold onto their investments for as long as needed to allow prices to appreciate. Given that there is no strict deadline to sell an investment, bulls can choose to ignore any short-term fluctuations in the market and ride out the volatility, so long the underlying fundamentals of their investment have not deteriorated. Even if prices do decline, bulls have the option of holding out. Diversification also works in favour of the bulls, because by adequately diversifying one’s portfolio, one is insulated from firm-specific risks. And having a handful of underperforming stocks in a portfolio becomes an expected and normal part of investing.

Indeed, a quick survey of the history of the S&P 500 index would show that equity markets naturally drift upwards over time, the only valid reason for being a bear is that one can outperform the passive “buy and hold” investor by getting in and out of the market at the right time. To time markets, one has to become a bear, even if it means becoming one only temporarily.

Why Bears Are Destined To Lose

Behavioural finance, which has grown into a widely researched and applied branch of economics in the last few decades, has documented various psychological biases that influence the behaviours of investors. More often than not, these biases work against investors, resulting in decisions that are suboptimal and at times clearly irrational.

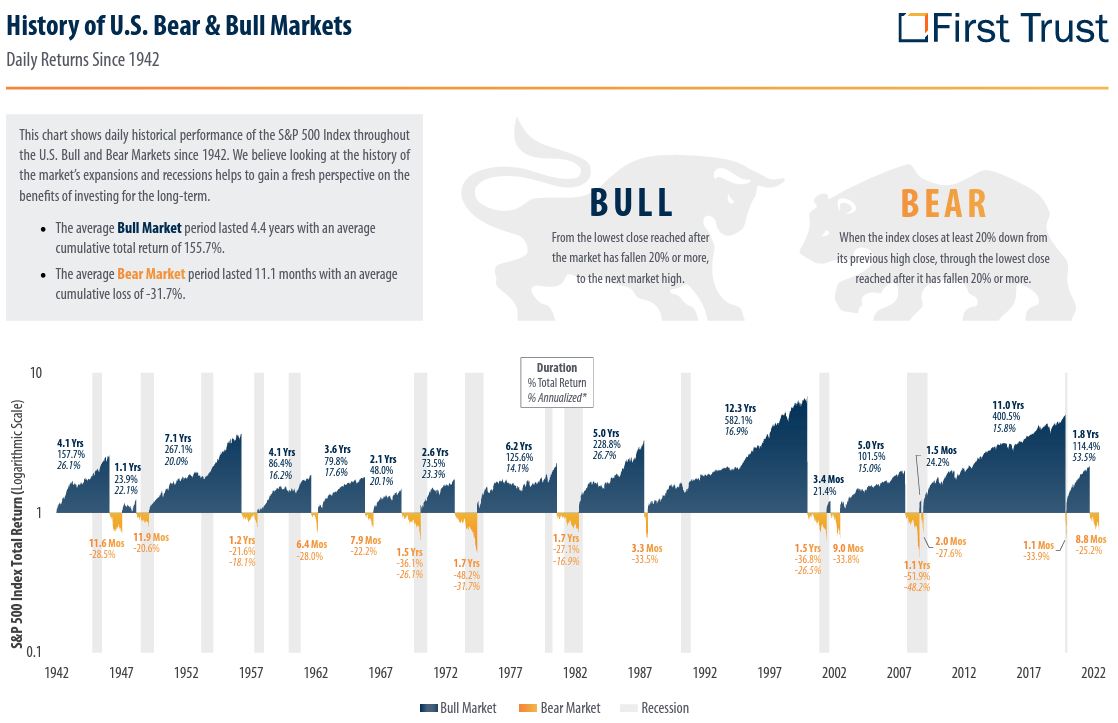

We briefly mentioned in the previous section that equity markets tend to drift higher over time. This phenomenon is driven by underlying economic fundamentals and persists because well-functioning economies grow over time and well-managed companies become more profitable. Meanwhile, poorly managed companies are quickly eliminated by competition and most companies don’t do well enough to make it to the S&P 500 index. Without having to dive into the statistics, we offer a chart below that summarises past bull and bear markets since 1942.

First Trust Advisors

Since 1942, bull markets on average lasted 4.4 years while bear markets on average lasted 11.1 months. Furthermore, the cumulative total return for bull markets averages 155.7% while bear markets average a cumulative loss of -37.1%. One can imagine why it takes a genius to be a successful bear, or perhaps serious dumb luck.

Despite evidence that equity markets persistently trend upward over time and that bear markets are exceptionally difficult to predict, bears continue to attempt to time markets because of greed. From the perspective of behavioural finance, many well-documented examples of biases can offer an interesting explanation for such behaviour. But we shall focus on the most popular ones such as availability and anchoring bias.

Availability and Anchoring Bias

Almost every trader at some point in time, or by choice, is subjected to a constant flood of news from the financial media. The major selling point of the financial media is that it promises to deliver timely relevant news even whether it truly matters to investors or not. This constant flood of news, while useful and relevant from time to time, nonetheless makes investors exceptionally susceptible to availability bias.

The availability bias refers to the tendency for traders to rely on information that comes readily to mind when evaluating a problem or making a decision. When inflation surged to a four-decade high back in July 2022, it was difficult not to come across articles evoking memories of the stagflationary era of the 1970s. The financial media was laser focused on what could possibly go wrong and highlighted similarities between 2022 and the 1970s. The financial media was behaving rationally, flooding the market with news that provided insights into the worst-case scenarios and attracting readers desperate to learn more about the potential disaster ahead. It made little sense to publish articles arguing how inflation would ultimately be transitory and cool towards the low 2% levels, even if any analyst was actually willing to make that call and stake their career on the view.

This, however, made “stagflation” and “recession” the most readily available information in every trader’s mind. It created an overwhelming feeling of pessimism and urged every investor to start dumping stocks. Very few with the discipline, honed over many years of experience in the financial markets, ignored all the pessimism and continued to buy when the markets went down. Warren Buffett was such an exception, going on a shopping spree buying up stocks to the tune of US$3.8 billion during the period between April and June 2022. For good measure, Buffett also bought back US$1 billion worth of Berkshire Hathaway stock.

The anchoring bias is another common culprit responsible for poor investment decisions. Anchoring bias occurs when people rely too much on pre-existing information or the first information they find when making decisions. A good example is recent memories of key index levels or stock price levels. When inflation was showing early signs of getting out of control, the immediate memory of an inflation crisis was the 1970s. And when investors questioned how far could equities fall in a bear market, the immediate memory available was the most recent bear market (2020) or the most painful one that occurred in recent times (2009). Therefore, it was not surprising that the S&P 500 index eventually witnessed a decline that quite closely matched the previous bear market in magnitude. And some of the most bearish analysts on Wall Street were setting bearish price targets for the S&P 500 that would match the bear market of 2009, which equates to a drop of around 50% from the peak.

We suspect that this anchoring bias was also responsible for the overwhelming pessimism surrounding the real estate market, where homebuilder stocks and some REITs, in particular, have become deeply oversold with valuations becoming abnormally cheap despite resilient earnings. After all, the last real estate crisis in 2008-2009 was exceptionally painful and real estate prices have also surged to new heights in 2021.

What Is In Store For The Bears?

Despite the overwhelming evidence against short-term speculative trading, it is expected that some will still choose to pursue market timing as a shortcut to wealth. It doesn’t take a skilful economist with the ability to predict where inflation will go to know that challenging economic environments are more likely to pass than to escalate into a full-blown crisis. Indeed, there is also an old saying that “bull markets climb a wall of worry”, which refers to equity markets rising despite economic uncertainties and constant negative news.

Even if you ignore all fundamental economic arguments in favour of disinflation and a soft landing for the economy, just the historical track record of equity markets since 1942 would suggest that the bear market is running out of time. As the worst-case scenario of a return to the stagflationary era of the 1970s seems increasingly unlikely to materialise, the more likely that we are perhaps not in such a difficult environment after all. The market seems to understand that and has already staged a rally since the market bottomed in October 2022.

For the bears who are starting to realise they are on the wrong side of the trade, the incentive is to wait for a pullback to re-enter near the October lows. For the bears who are still hoping for an economic crisis to materialize, it could be a painful wait with no certainty of returns. But in either case, the bears are caught in a challenging dilemma. The mistake of not staying invested in the market with discipline or the decision to short the market and not covering the shorts in time is becoming increasingly difficult to bear. But giving up on the bearish view and buying up stocks now would mean buying at levels way above the October lows. What could potentially be more difficult though, is being completely sidelined while one watches another multi-year bull market in the making.

Meanwhile, the bulls can take it easy. After all, equity markets do recover every time. If anything, the sell-off in 2022 was a good outcome. It presented a rare opportunity to pick up quality companies at heavily discounted prices. All the bulls have to do is wait.

Be the first to comment