S&P 500, FOMC, Dollar, USDCNH, EURUSD and USDCAD Talking Points:

- The Market Perspective: USDJPY Bearish Below 141.50; Gold Bearish Below 1,680

- Both the London and Tokyo markets were offline for holidays Monday, but that wouldn’t curb volatility from the likes of the S&P 500 which gapped lower and ended with a close

- Volatility is likely moving into Tuesday with a handful of high profile events on tap, but the market will not likely run until the FOMC has its say on Wednesday

Recommended by John Kicklighter

How Should Traders Approach the Coming FOMC Decision?

Lightning In a Bottle on Risk Trends Until the FOMC has Its Say

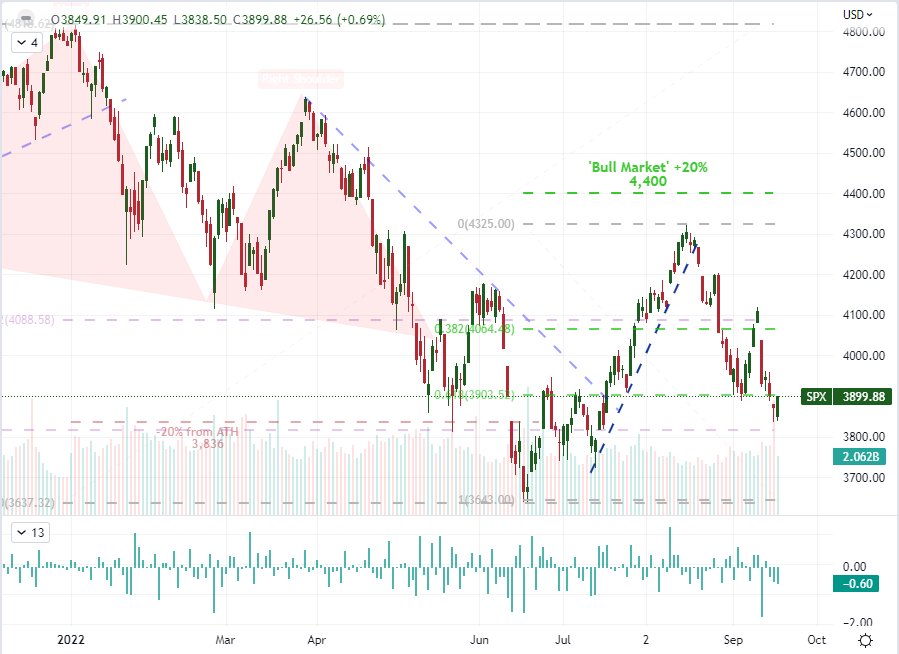

It is natural that risk trends would struggle to start this trading week – even if we were riding out the worst slide in three months the week before. With a FOMC rate decision ahead that can end in with an extraordinary third meeting with a 75 basis point (bp) hike or possibly shock with a 100bp jump, it seems more than reasonable than reasonable that the speculative rank will hold off on making a systemic all. That said, volatility is not so readily curbed. With liquidity concentrated due to the London and Tokyo markets offline, the carry over of Friday’s drop registered quickly for the S&P 500 with an intensified gap lower on Monday’s open. The commitment in that move was as dubious as the subsequent rebound through the active session. There is plenty of expected volatility to draw on, but follow through requires the conviction of the crowd. And, that is unlikely to find until such a critical hurdle is passed. So how will markets trade until that milestone is passed?

Chart of S&P 500 with Volume, 20 and 200-Day- SMAs with COT Net Spec Positioning (Daily)

{kind=link}

Chart Created on Tradingview Platform

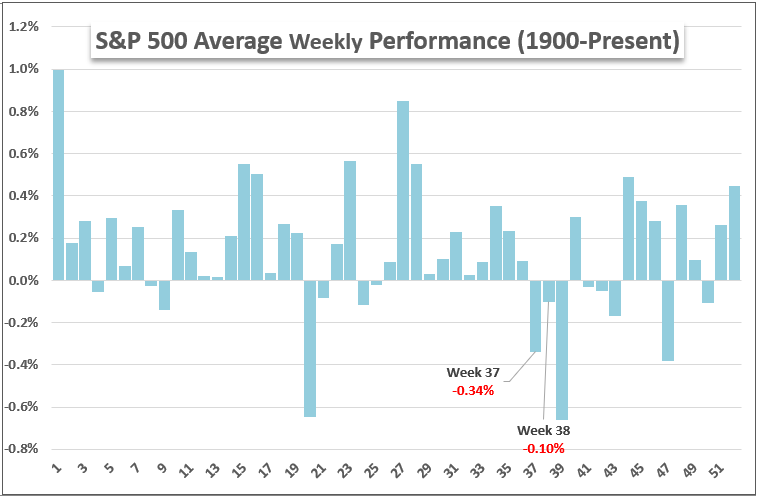

There are serious, unique circumstances to unpack this year passing through the 38th week of the year. With the FOMC rate decision kicking off an avalanche of developed and developing world policy updates, there is as much a rumble in global risk trends ahead as there is through relative monetary policy considerations. Historically-speaking, the S&P 500 typically registers a loss through this week on average, but it is a notable moderation relative to the 37th and 39th weeks. While the Fed’s decision mid-week could trigger a serious market response, it is just as likely that the fundamental relief will shift our focus right back into an unresolve fundamental mix that includes recession fears. Volatility is a probable market characteristic moving forward, but be mindful of assuming a clear trend.

Chart of S&P 500 Performance by Calendar Week Averaged from 1900 to Present

Chart Created on Tradingview Platform

Digesting Anticipation: USDCAD, USDCNH and Macro Event Risk

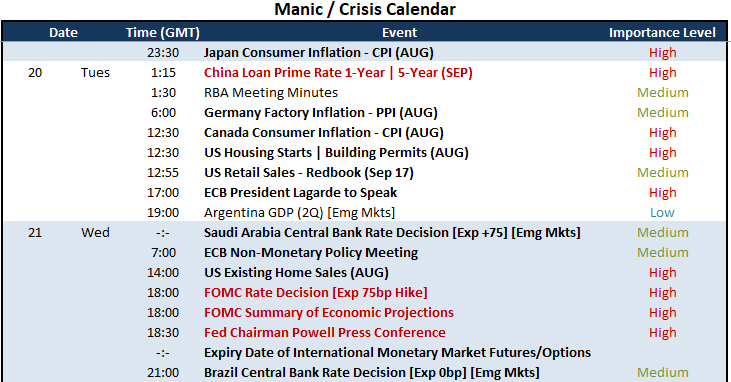

As we deal with the chop that precedes a critical event risk like the FOMC decision on Wednesday, it is important to not lose sight of the volatility that can readily stir from the targeted event risk. This past session absorbed the news that China had cut its short-term repo rates to combat economic strain while the NAHB US housing market index for September slid further into troubled territory. In a market hyper-sensitive to the threat of economic seizure the previous months’ description of a US housing market ‘recession’ were already the source of serious concern. Seeing the NAHB figure drop to its lowest level since the pandemic (April/May 2020) and before that the May 2014 lows, there is a natural concern to follow. As for the rate cut from the China, the increasingly dramatic contrast between the PBOC’s course and global counterparts like the Fed, BOE and even ECB adds to the pressure of USDCNH’s crest above 7.0000.

Critical Macro Event Risk on Global Economic Calendar for Next 48 Hours

Calendar Created by John Kicklighter

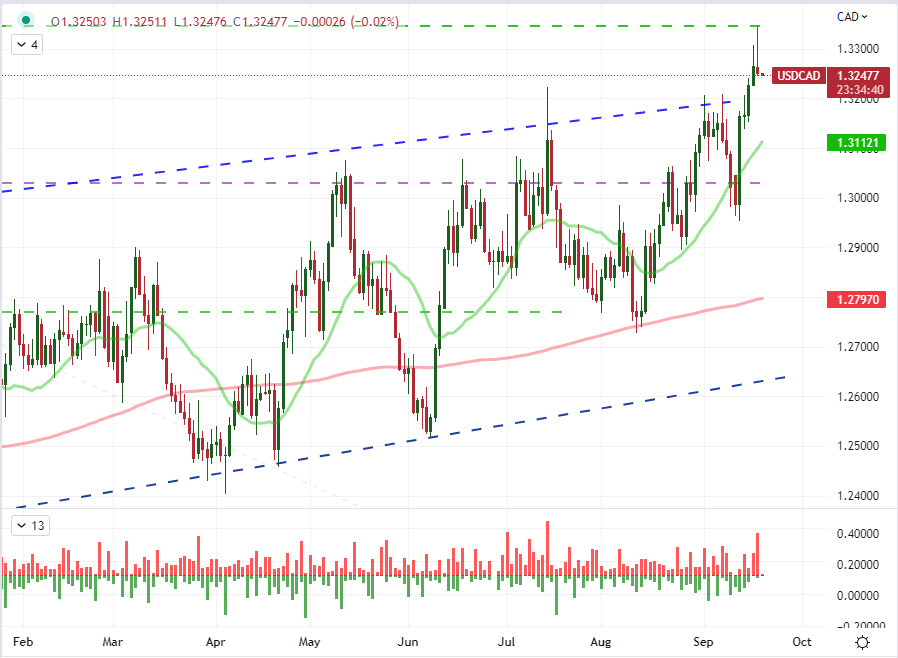

Among the dollar-based majors, an interesting cross that was fallen back in the pack of the crosses I track but warrants closer attention through the first half of this week is USDCAD. The pair extended its rally from last week to tap the midpoint of the March 2020 to May 2021 bear wave just shy of 1.3350. There was some fundamental lift to that move founded on the upstream Canadian factory and raw material inflation figures. The data did slow but at a less accommodative clip than was anticipated. Given the retreat of USDCAD, there wasn’t enough in the inflation data to forge a trend that override the FOMC focus. With the consumer inflation (CPI) stats from Canada due later today, I will be watching the second fundamental wave…but I will not think practical trend development unless it is a Loonie cross that doesn’t include the Greenback.

Chart of USDCAD with Daily ‘Wicks’ (Daily)

Chart Created on Tradingview Platform

Monetary Policy Expectations are Solidifying: Dollar, Euro and Yen

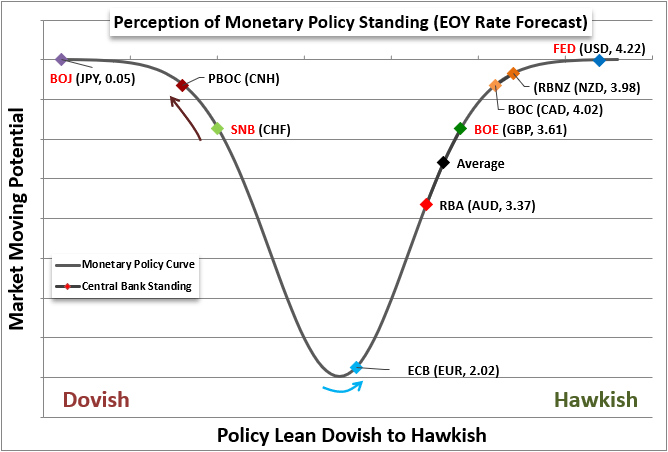

There wasn’t much in the way of favorable fundamental winds as far as the US Dollar is concerned, but that wouldn’t keep Fed rate expectations from their meteoric journey. Despite the US housing recession talk along with the Bank for International Settlements and World Bank warnings about the future, interest rate forecasts for the US central bank were still pushing an incredible 4.22 percent benchmark lending rate through year end. That is materially higher than all of the central bank’s major counterparts. That helps explain the Greenback’s loitering at multi-decade highs, but it doesn’t justify a sustained climb higher moving forward. Given the rate forecast priced in for the Dollar and catchup being mounted by counterparts like the BOC (with a year-end rate seen above 4.00 percent) and the ECB quickly ramping up its inflation fight, it is perhaps more likely that we see a disappointment than a ‘besting’ of expectations.

Chart of Relative Monetary Policy Standings Among Major Central Banks

Chart Created by John Kicklighter

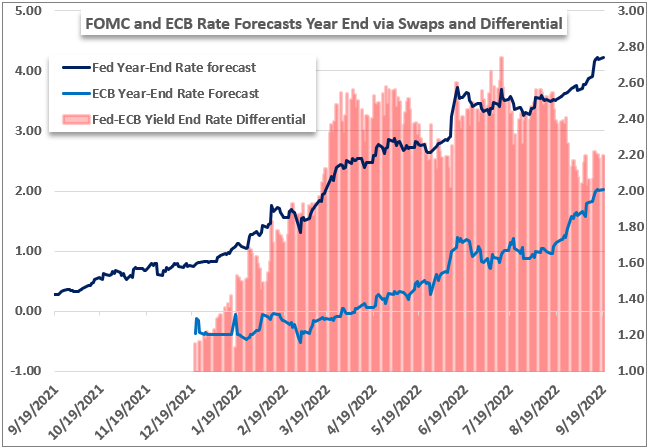

To give context to how a sizable rate hike from the Fed could still be met with ‘disappointment’ from the market, it is important to understand the influence of context. The Euro and ECB are perhaps the best counterpoint. EURUSD has bounced around parity without the ability to fully rebound and no will to make a clear cliff dive below 1.0000. If it were only the Dollar’s considerations, the equation would be easier to work out. However, the outlook for the euro plays as much of a role in the market’s balance – if not more so. Looking at the Fed and ECB year-end rate forecasts below, we can see that while the former’s forecast has charged higher with inflation and rhetoric, so too has the latter’s projections. As a differential, the ECB’s forecasts have actually improved relative to the Fed’s prospects in the past two months. For pairs like USDCAD, GBPUSD and other higher yielding crosses, that current yield gap is smaller. That is not a one dimensional consideration, however, as relative growth and safe haven appeal are both still leaning in the Dollar’s favor.

Chart of Fed an ECB Year-End 2022 Rate Forecasts from Swaps Overlaid with the Differential (Daily)

Chart Created by John Kicklighter

Trade Smarter – Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team

Subscribe to Newsletter

Be the first to comment