kmatija

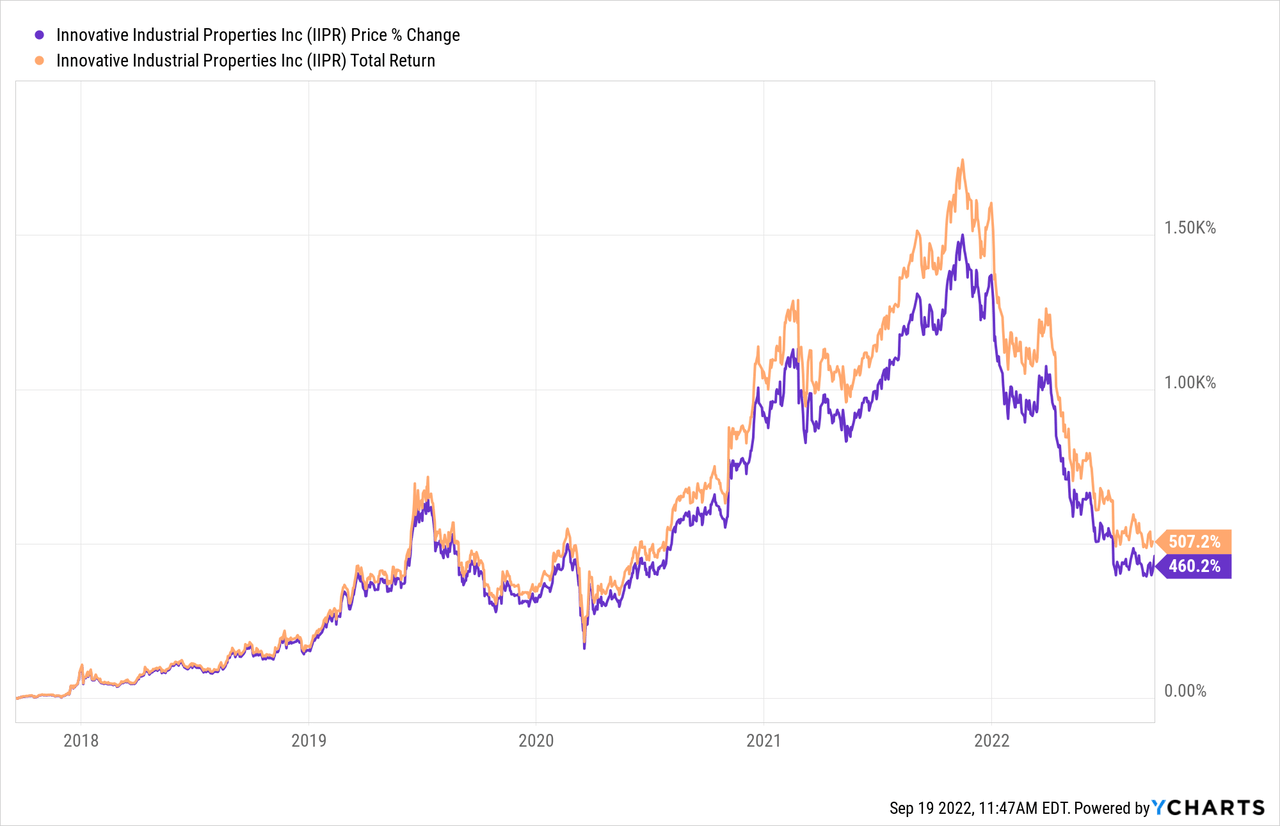

Our previous coverage of Innovative Industrial Properties (NYSE:IIPR) outlined the REIT’s secular growth attributes, which we believe will carry the security above and beyond the broader asset class. In this analysis, we reiterate our buy rating as we’ve uncovered a few additional positives pertaining to intrinsic valuation, the REIT’s income statement, asset pricing metrics, and more.

Despite numerous macroeconomic headwinds, we believe Innovative Industrial Properties could be an outlier in the financial markets and prosper.

Business Model Analysis

Positives

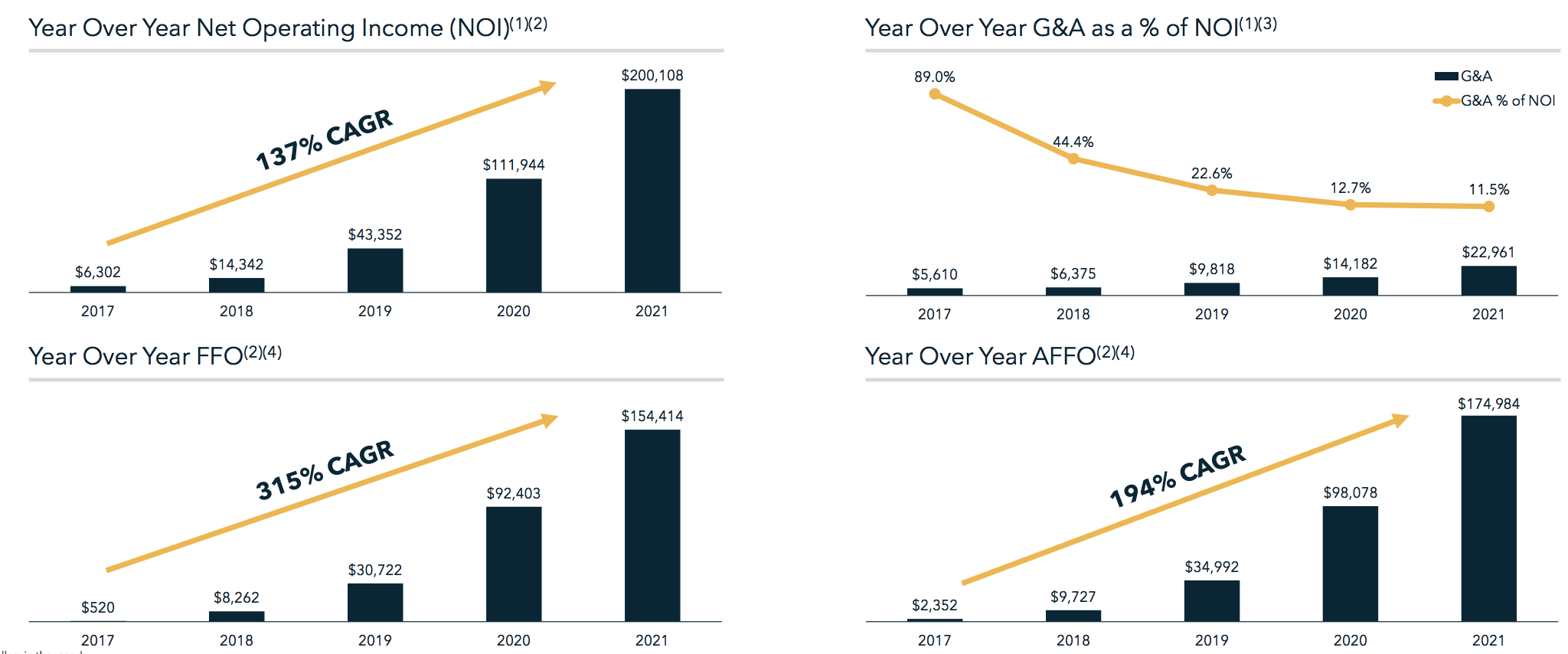

Starting with the basics, let’s look at Innovative Industrial Properties’ operational growth rates.

The Cannabis REIT’s growth rates are miraculously high, and it’s been able to achieve these rates at nearly a 100% collectibles rate, which is rare to see.

Innovative Industrial Properties’ adjusted funds from operations’ 5-year CAGR of 194% is a real standout. Adjusted funds from operations provide an economic explanation of the REIT’s income as it backs out amortization and other non-cash costs.

A key feature of Innovative industrial properties is its 100% triple-net lease agreement with its tenants, which sees it avoid maintenance CapEx and vouchers. This is highly beneficial given the current inflationary environment; therefore, one can say that Innovative Industrial Properties’ strong collection rate and its 100% net lease models grant it a competitive advantage.

Innovative Industrial Properties

The figure below shows how rapidly Innovative Industrial Properties is scaling. I don’t want to elaborate on the diagram below too much, as we covered it extensively in our previous article. However, I’d like to emphasize the rate at which the REIT’s total assets are growing while running at a collectibles rate of nearly 100%.

Innovative Industrial Properties

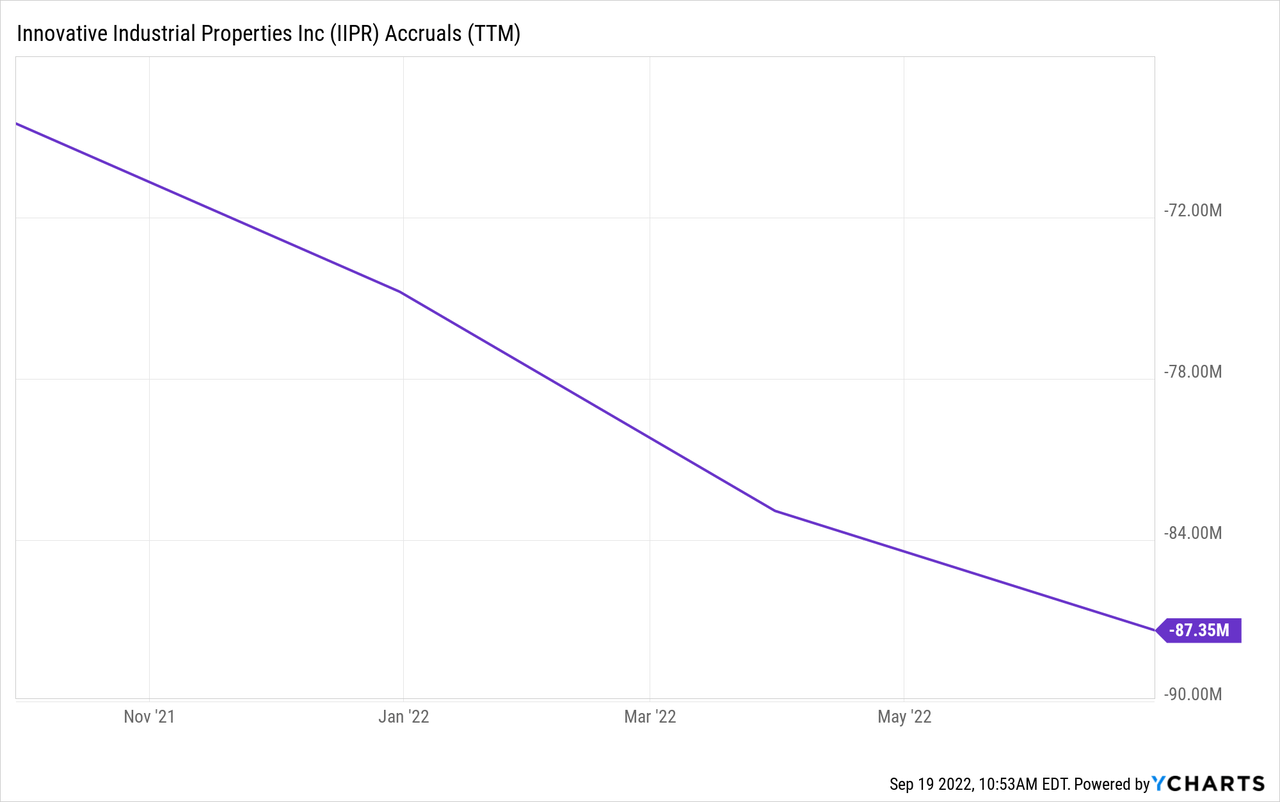

Lastly and probably most importantly. Innovative Industrial Properties generally recognizes its monetary in and outflows on a cash basis. In many instances, publicly traded companies manipulate their income statements to smooth out earnings through economic cycles. However, at face value, Innovative Industrial Properties’ income statement closely follows its cash flow statement (see the accruals ratio in the succeeding diagram).

Seeking Alpha; Innovative Industrial Properties

Negatives

I had to look at matters more holistically to juxtapose my analysis.

Innovative Industrial Properties recently suffered a credit event when its tenant, Kings Garden, defaulted on its $2.2 million per month rent. Even though Innovative Industrial Properties’ portfolio comprises credible companies, credit events are usually exogenous and inextricably linked to the global economy.

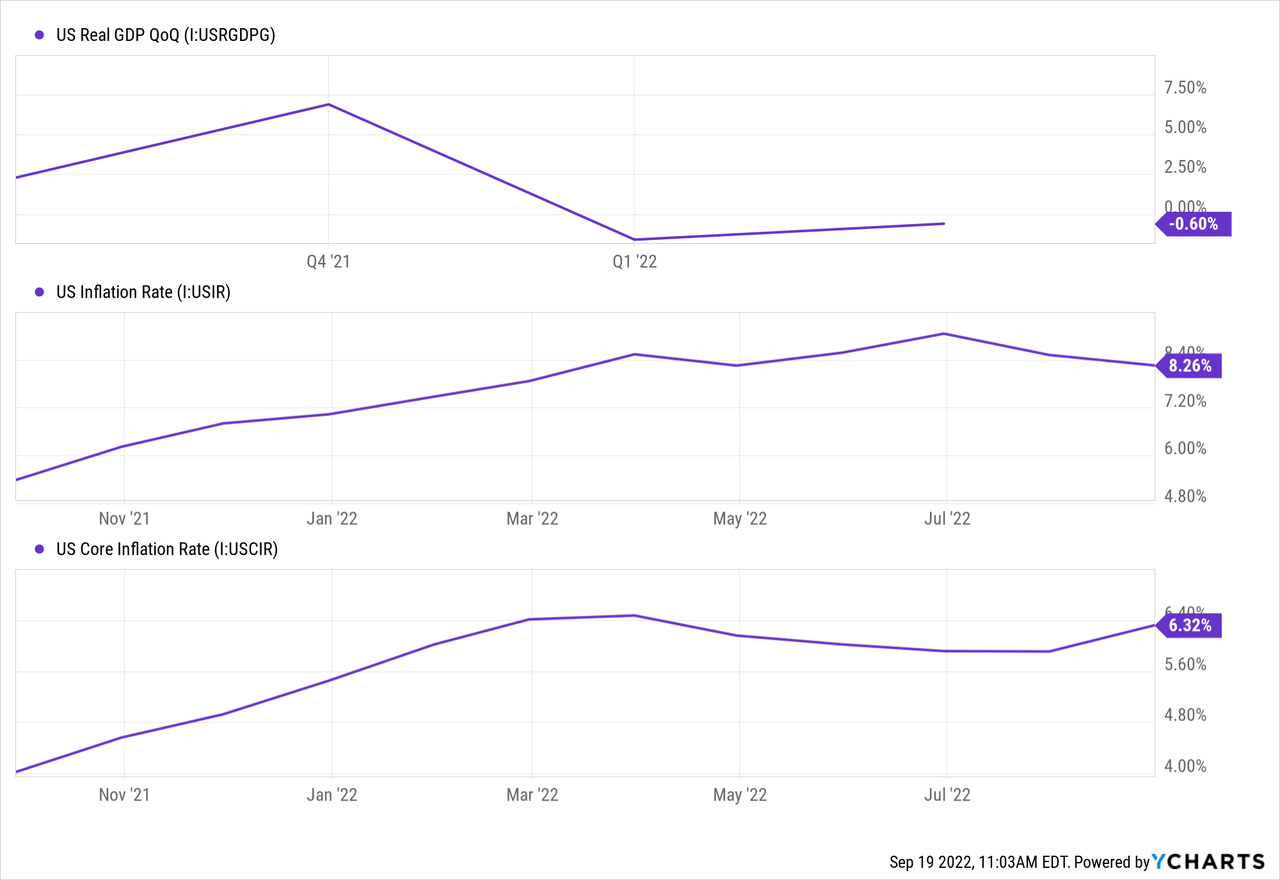

Based on recent data, the global economy is plagued with resilient inflation, negative GDP growth, and diminishing core consumption. Cannabis does resemble tobacco-esque characteristics, but it’s yet to be classified as a consumer staple good, meaning it’s a cyclical business.

Adding to the above. Innovative Industrial Properties’ tenants form part of an industry in its early development stage, meaning constituents’ income statements are vulnerable to economic softening. We see this as a potential red flag pertaining to counterparty risk.

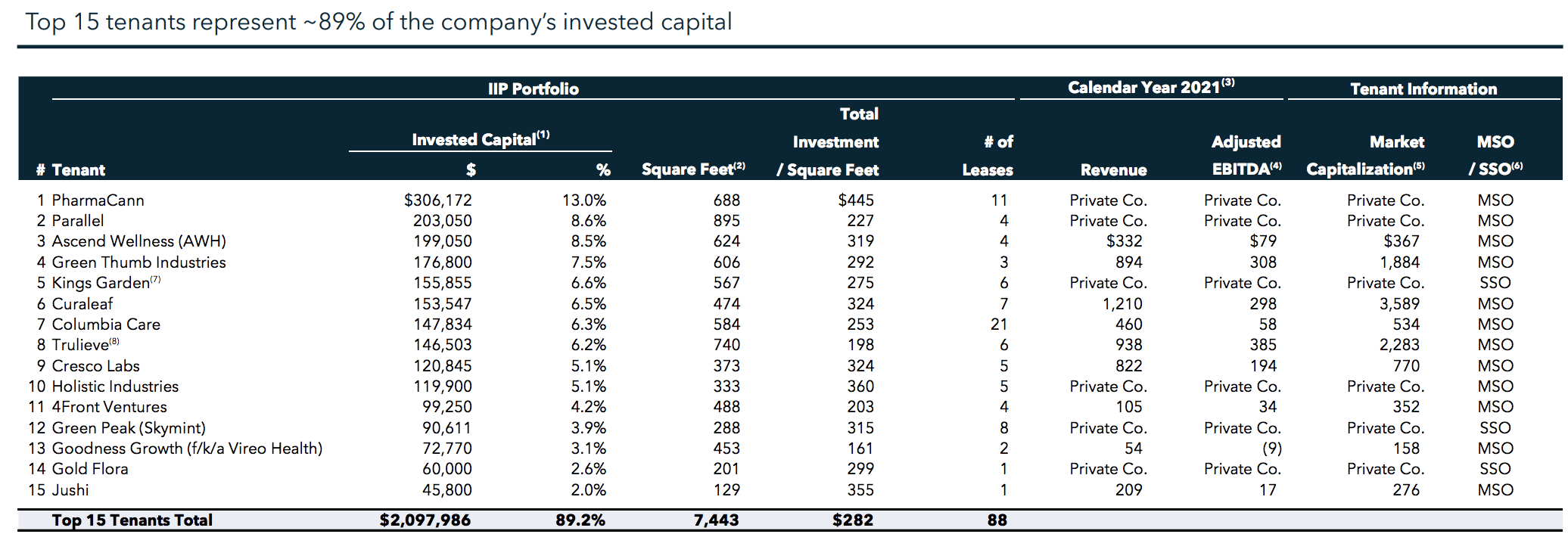

The two diagrams below display 1) Innovative Industrial Properties’ top tenants and 2) Its exchange-listed tenants’ quick ratios and EBIT margins, which are inextricably linked to counterparty risk.

Innovative Industrial Properties

Source: Seeking Alpha; Innovative Industrial Properties

To provide context on the dataset above. A firm’s quick ratio is its cash & receivables divided by its current liabilities. A quick ratio above 1.00 is generally described as acceptable. As observable in the table, Innovative Industrial Properties is exposed to various assets with low quick ratios, which poses a threat of counterparty risk. Additionally, a few of its holdings have negative EBIT margins, raising numerous red flags.

Lastly, it probably goes without saying, but the REIT’s exposed to an industry that faces constant legal disputes. The continuous battle toward “full-on” cannabis legalization adds systemic risk to the asset’s traded price.

Valuation

Dividend Discount Model

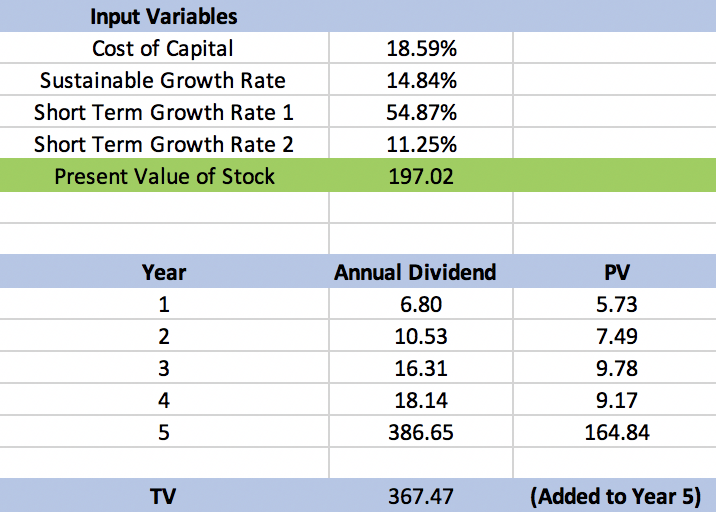

I utilized a three-stage dividend discount model to slap a valuation on Innovative Industrial Properties. The three-stage dividend discount model discounts future dividends along with a terminal value to synchronize a fair value. Because future dividend growth rates are subjective, the model should be taken with a pinch of salt; nonetheless, it’s a helpful indicator.

Based on a three-stage model, which measures three distinct periods of growth, the Innovative Industrial Properties REIT is undervalued by more than 90%.

Pearl Gray Equity and Research; Seeking Alpha

Here’s how I engineered the model.

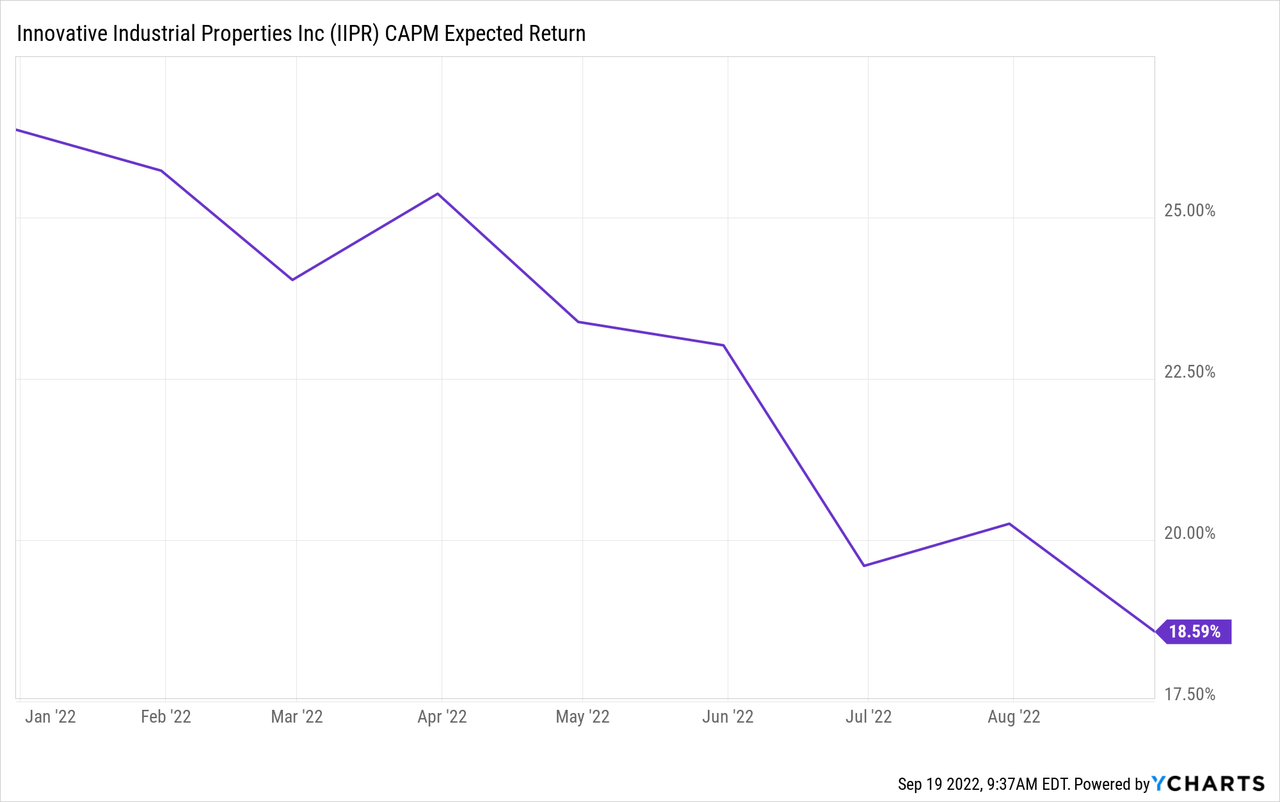

- I pulled the REIT’s cost of capital from YCharts. I then used this number to discount the cash flows.

- I parted the REIT’s future dividend growth into three stages. I utilized retrospective rates as I believe they’ll be repeatable in the REIT’s next operating cycle (5 years).

- I derived the constant growth rate by utilizing its current dividend per share growth rate (fwd). I wanted to compute a sustainable growth rate, but REITs pay high dividend-payout ratios, thus, making the computation impractical.

- I generated a terminal value by dividing the REIT’s year-5 dividend by the difference between its cost of capital and its sustainable growth rate.

- Lastly, I landed at a fair value by adding up the discounted cash flows (and the terminal value).

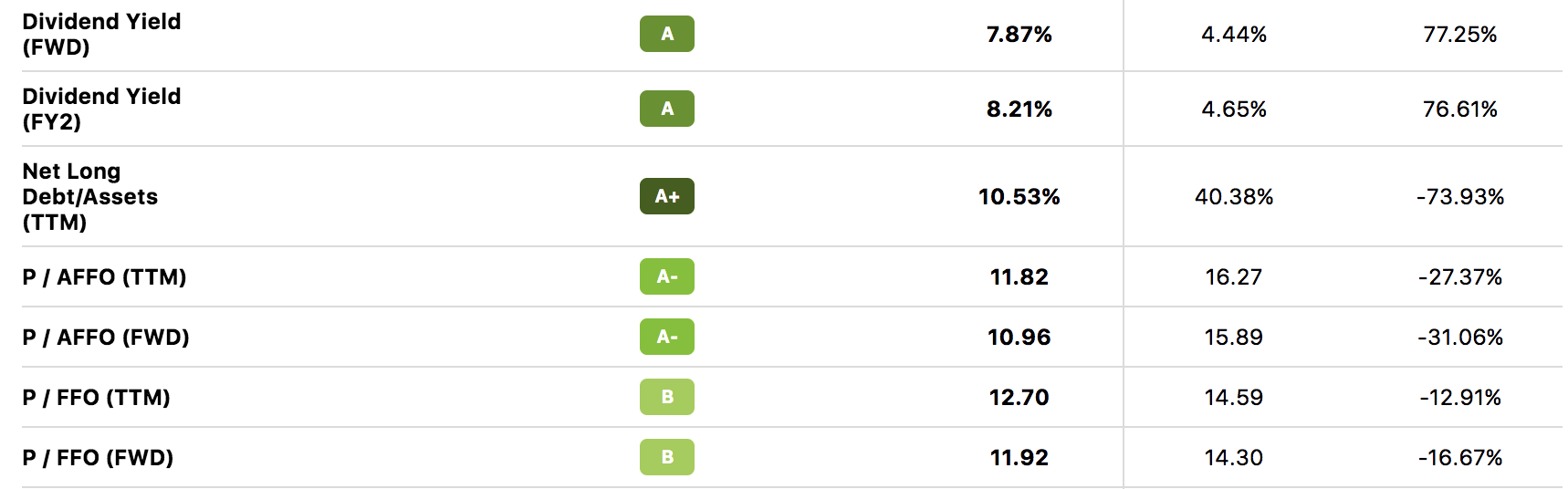

Relative Valuation Metrics

A relative valuation framework provides substance to my dividend discount model. According to Innovative Industrial Properties’ price-to-funds from operations, the REIT’s significantly undervalued as the ratios at a 12.91% normalized discount. Additionally, the REIT’s high dividend yield is desirable in today’s market, which is characterized by risk-off investor sentiment and high inflation.

Seeking Alpha

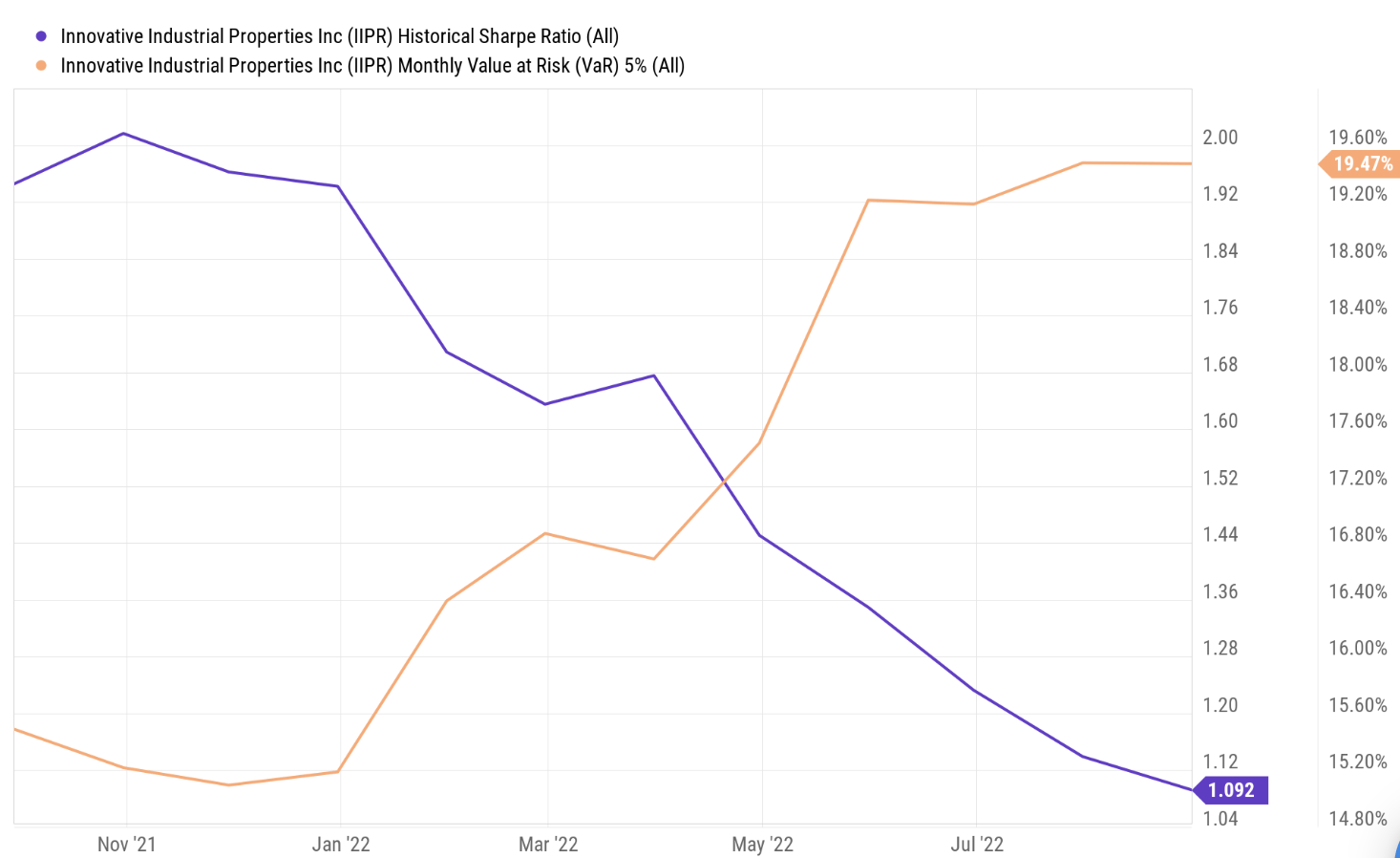

Quantitative Risk Analysis

The following pertains to asset pricing instead of valuation. Innovative Industrial Properties’ Sharpe Ratio of 1.092 shocked me in a way as it exceeds the risk/return threshold (1.00). A Sharpe Ratio measures an asset’s excess return (benchmarked to the risk-free rate) with respect to its volatility. Therefore, by exceeding 1.00, it can be claimed that the Innovative Industrial Properties REIT exhibits a favorable risk/return profile.

However, investors must note the stock’s value-at-risk, indicating that Innovative Industrial Properties tends to draw down by 19.47% or more in 5% of its traded months.

Seeking Alpha; YCharts

Final Word

Based on advanced valuation and pricing metrics, Innovative Industrial Properties is a “best-in-class” REIT. Furthermore, the REIT’s key operational metrics convey secular growth. Therefore we maintain our buy rating on the REIT.

If you’re interested in more advanced analysis, be sure to keep an eye out for our marketplace program, “The Factor Investing Hub,” which launches soon. FIH is an AI-driven “smart beta/factor investing” portfolio management concept with the goal of balancing long-term portfolios relative to “factors.”

Be the first to comment