S&P 500, FOMC Rate Decision, US Dollar and USDJPY Talking Points:

- The Market Perspective: S&P 500 Eminis Bearish Below 3,900; USDJPY Bullish Above 132.00

- The market forged its way through a heavy session of event risk, but the focus remains on Wednesday’s top listing: the FOMC rate decision

- We run through the scenarios for the Fed decision, the complications for market impact and why I’m paying close attention to the S&P 500 and USDJPY

Recommended by John Kicklighter

Get Your Free USD Forecast

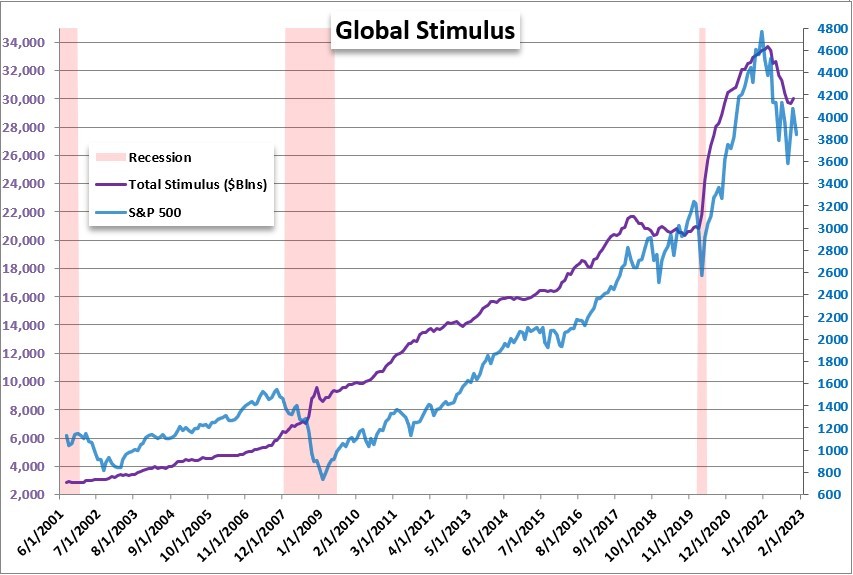

We are closing in on this week’s most closely observed, major event risk: the FOMC rate decision. Despite the market’s general view that monetary policy for the US and major central banks is near the terminus of the tightening regime, the impact of speculation around the nuance of this immediate future seems to be growing. The influence of interest rates and stimulus is so profound due to the decade-plus dive into unorthodox accommodation by the world’s largest central banks to first stabilize the world coming out of a financial crisis (the ‘Great Recession’). After three or four years of that firefighting, however, the intent began to blur. A fight against a European debt crisis and its potential contagion offered some justification to carry on, but eventually the economic impact diminished to be replaced with a passive effort to keep financial markets steady. For those that came to trading/investing in the past decade, they have never not known this aspect of the system. In turn it may be hard for these market participants not to consider stimulus a permanent ‘mean-reverting’ structure, which in turn renders skepticism against the central banks’ stated intent to unload the burden of risk back onto the market’s own shoulders. That’s the backdrop that formulates the importance of this week’s top event.

Chart of S&P 500 Overlaid with Aggregate Major Central Bank Stimulus and US Recessions (Monthly)

{kind=link}

Chart Created by John Kicklighter

Heading into the Fed decision, some of the anxiety that is naturally stoked by the scope of the event can be seen across the capital markets. I referenced the errant volatility in benchmarks like the S&P 500 below or the extremely restrictive range for the US Dollar (DXY Index). Both are indicative of a market absorbed in the range of possibilities for an exceptional fundamental event. For the DXY, a flare up of volatility wouldn’t widen the now 12-day and 1.37 percent range – the most restrictive trading in nearly a year. For the S&P 500, 1.5 percent rally was a little more unusual. While the intensity of the charge looks like a side effect of the anticipation, a build up ‘risk on’ interest before an event that could struggle to ‘pay’ for that enthusiasm is unusual. Index volume was the highest since the December 16th holiday wash while open interest in emini futures is still near its lowest levels since 2007. This is unusual activity and may add to a volatile reaction after what will likely be a ‘in-line’ outcome from the Fed.

Chart of S&P 500 with 200-day SMA, Volume, E-mini Futures Open Interest and 1-Day ROC (Daily)

Chart Created on Tradingview Platform

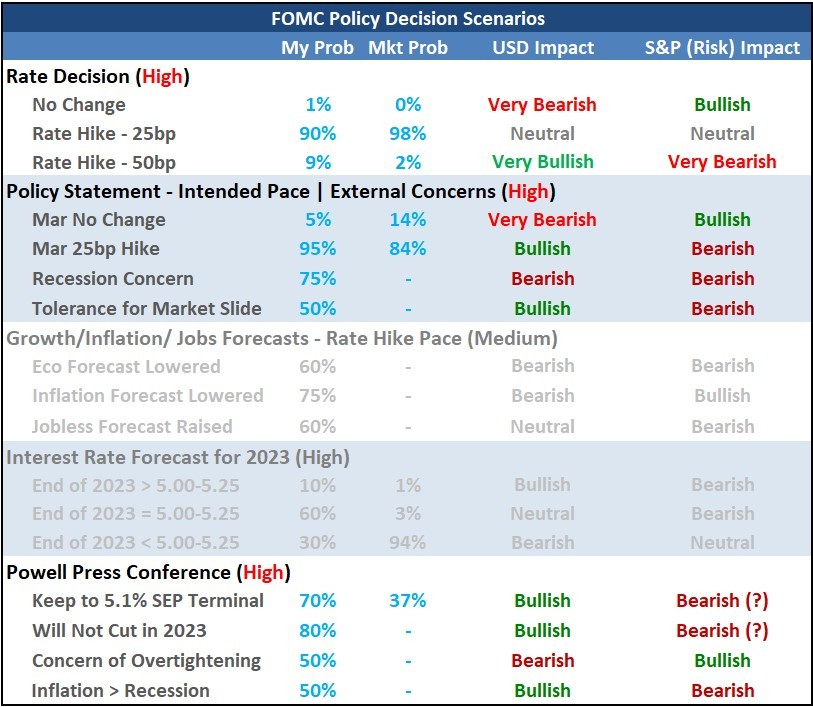

So, what are we looking for from the Federal Reserve’s first policy announcement of 2023? This is not one of the so-called quarterly meetings which offer updated forecasts for growth, inflation, employment and interest rates – also referred to as the Summary of Economic Projections. That leaves us with: the actual changes to policy; the monetary policy statement and the Chairman Jerome Powell’s press conference a half hour later. The markets are highly confident (98 percent according to Fed Fund futures) that the Fed will further step down its tempo of tightening from December’s 50 bp increase to a 25 bp move today. Given the certitude of the markets in this pricing, any deviation here would be the basis for serious volatility in repricing. Otherwise, the focus will shift to the standard for speculation as of late: how far and long will this rate hike regime extend. According to futures, the market expects only one more 25 bp hike in March which would lift the terminal rate to a range of 4.75-5.00 percent. The problem is that the Fed itself projected a terminal rate range of 5.00-5.25 (or a mid-level of 5.1 from 5.125) percent. Will the markets just continue to agree to disagree or will Powell’s remarks justify or close the gap? Therein lies the volatility potential.

FOMC Scenario Table

Table Created by John Kicklighter

Shifting gears to general ‘risk’ response to this week’s top fundamental listing to more targeted influence, USDJPY is at the top of my list. For those evaluating the Dollar’s response to the policy update, consider the scope of major event risk that will print around and after the US central bank’s update. In particular, a preferred exchange rate like EURUSD will be heavily complicated by the European Central Bank’s (ECB) own monetary policy decision on Thursday. As far as the USDJPY goes, the Japanese docket is fairly light. More importantly, the BOJ doesn’t offer much in the way of monetary policy contrast, so it is more fully a Dollar reflection. On that front exchange rate has deviated from the yield spread between the US-Japan, but the more potent factor for me is the potential of volatility. There is a strong correlation between USDJPY and VIX. And, while it is possible that the Fed event passes uneventfully such that it deflates expected volatility, the reading is already very low. The potential for further substantial retrenchment is low. Alternatively, the risk – and impact – of a flare up is high.

Chart of USDJPY Overlaid with the US-Japan 2-Year Yield Spread and VIX (Daily)

Chart Created on Tradingview Platform

Finally, it’s worth it to take a full stock of what is unfolding around the market while the volatility blinders are up and focused on the FOMC. Wednesday will also tap into US growth potential in the ISM manufacturing report. Earnings will pick up afterhours with Meta/Facebook, but hit their pinnacle tomorrow after the close with Apple, Amazon and Google. Then there are the ECB and BOE rate decisions which will shape the global picture of monetary policy.

Top Global Macro Economic Event Risk for Next Week

Calendar Created by John Kicklighter

Be the first to comment