Scott Olson

2022 was a wild year for markets. And despite a valiant attempt at a fourth-quarter rally, stocks still ended the year deep in the red, especially as the usual holiday cheer fizzled out this year. The S&P 500 will finish the year down nearly 20%, while the tech-heavy Nasdaq lost a third of its value.

There was little relief in fixed income either as bonds slumped amid a surge in inflation and an aggressive rate hike campaign from the Federal Reserve. Most foreign stock and bond indexes also fell, giving investors little relief wherever they turned.

Looking ahead to 2023, many people seem to be anticipating another big move. The bulls are looking for a “V” bottom and move back toward the highs. After all, since 2009, buying the dip has always been the right strategy. Every correction was an opportunity to make money on the inevitable quick rebound. The early pandemic market of March 2020 was the ultimate test of that as markets plummeted but recovered all their losses within a matter of months.

Will 2023 follow that tradition? Probably not. The difference is that in the past, the Federal Reserve had the market’s back, whereas now it is on the opposite side. Before, inflation had been contained for decades and so the central banks had no fear in offering stimulus to ease financial market strains.

Now, inflation has become a central concern and so the Fed’s policy tools are more limited. Whereas in 2018 the Fed abruptly pivoted away from rate hikes the moment the S&P 500 dropped 20%, now it is continuing to hike even as the market has already fallen substantially more than that.

So, with the Fed remaining hawkish, is this the bears’ time to shine? Many folks are calling for sub 3,000 price targets in 2023 as the Fed’s tightening leads to a major recession, earnings decline, and ensuing market wipeout. It’s an easy narrative to imagine, and after such a jarring couple of years, it might feel like we’re just waiting for the next shoe to drop. It’s not hard to envision some new shock causing a wave of panic selling. China invades Taiwan. The Russian war escalates. The Chinese banking system fails. The Dollar collapses. And the list of potential catalysts goes on. However, I expect 2023 to not have that sort of cataclysm headline. Rather, I’m looking for a grueling year full of volatility, but where the S&P 500 ultimately goes approximately nowhere by year-end. Here’s why.

Average Bear Market

The S&P 500 made its all-time high of 4,818 on January 4, 2022. According to Dow Jones & Co. data, the average S&P 500 bear market decline is 33.5%, and the median decline is 33.2% with data reaching back to 1929.

Thus, both a median and mean bear market would result in the S&P 500 bottoming around 3,200. As it turns out, the S&P 500 got down to 3,492 this fall before rebounding.

That 3,492 level was a nice area for a bounce. Notably, the S&P 500 had topped out at 3,400 just prior to the start of the Covid-19 pandemic, and the index revisited that 3,400 level several times in late 2020, forming a support/resistance level there before proceeding higher.

For those inclined to technical analysis, the 3,400 level would be a perfectly logical place for this bear market to end and a new bull to being. And, given the average magnitude of historical American bear markets, this sort of decline would be in-line with expectations. As it goes, the drop to the October lows was a 28% peak-to-decline trough, and would fall well within range of what we’d look for in a normal downturn.

People’s expectations may be distorted from huge bear markets such as 1929 and 2008. However, the majority of the time, the economy has a mild recession and stocks go back to a normal valuation range rather than crashing through the absolute floorboards.

Things could obviously change if any additional big bearish catalysts emerge. But, at least so far, we appear to be muddling through a series of unprecedented but manageable shocks. Demand disappeared for a couple quarters in 2020 and then came back too fast and strong in 2021. This led to a series of unpleasant consequences, such as the current inflationary surge, but nothing that is too severe compared to other economic recessions.

There’s no systemic crisis, unlike housing in 2008 for example, that would turn this from a garden variety bear market/economic slowdown into a big one. As such, I’m looking for a roughly average market downturn.

As we already got within range of a typical 33% decline back in October, I wouldn’t be surprised if that was the ultimate bear market bottom. On the other hand, one more push down toward 3,200, followed by a sharp rally, would be my other high probability scenario. What I don’t expect to see is a drop below 3,000 or a major rally in 2023. Both seem unlikely given where valuations and earnings trends are.

S&P 500 Target

Historically analysts tend to have earnings estimates that are significantly higher than where actual results tend to come in when the final numbers are tabulated, with some studies pegging the average miss to be around 8%.

Given that earnings estimates are currently on a negative trajectory, and seem likely to continue that way given monetary tightening, the strong dollar, and continued margin pressure, I’ll go with a 10% haircut to the current consensus for 2023 earnings.

Analyst consensus is currently $230 of earnings per share for the S&P 500, so I’ll go with $207 as the earnings outlook for this upcoming year. Using a roughly historically average P/E multiple of 17.5 on that figure, I arrive at a price target of 3,622 for year-end 2023.

This would be a mid single-digits decline for the year and is likely to be an outcome which would frustrate both bulls and bears alike.

The Bottom Line

If the S&P 500 is going to be volatile in 2023 but ultimately make little progress in either direction, then what’s an investor to do?

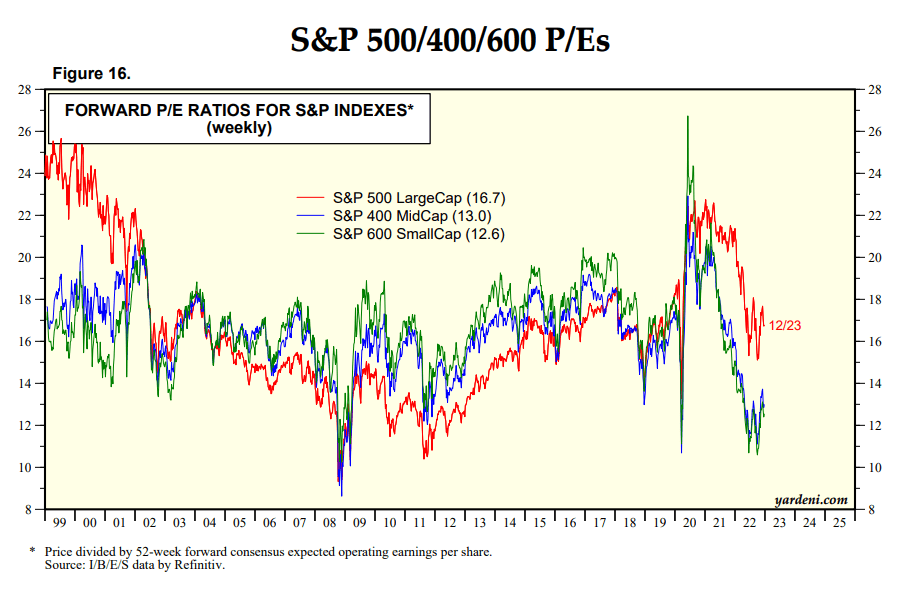

For one thing, there’s more to the stock market than just the S&P 500. I’d prefer smaller-cap American stocks to the S&P 500 in 2023. On an earnings basis, while the large-caps are around their historical average, both small and mid-caps are quite cheap:

Forward P/E ratios by market cap (Yardeni Research)

At 12.6x and 13.0x forward earnings, respectively, small-caps and mid-caps are near their 25-year lows in valuation. They are trading around the same levels now as they did in March 2020 and are only a couple of turns more expensive than their ultimate lows during the 2008 financial crisis.

This is in stark contrast to large-caps, which are still around their 25-year median valuation. For almost the entirety of 2004 through 2014, the S&P 500 traded at a lower forward P/E ratio than it trades for now. What drives this divergence?

The S&P 500 tends to become top heavy, especially after extended bull markets. In 2000, it was full of that cycle’s tech winners, such as Microsoft (MSFT), Cisco (CSCO), and AOL. In 2020, it was full of the FAANGs, Tesla (TSLA), Nvidia (NVDA) and other such glamour stocks.

After the dot-com bubble burst, it took many years for investors to come back to big tech. Companies like Microsoft grew earnings dramatically but were unable to see their share prices rise for more than a decade as investors avoided big tech.

I expect we may see a similar effect this time around. Investors that overpaid for FAANG and growth companies will likely avoid those firms, even as their valuations continue to become more and more reasonable. There’s no reason for big tech to make a “V” bottom. Valuations are coming down to more acceptable levels, but with uncertainty around future earnings growth and the interest rate environment, we could easily say valuations for big tech — and thus a large piece of the S&P 500 — stay at subdued levels for quite a while.

It’s not like big tech is a screaming bargain either. Microsoft, for example, is at 26x trailing and 22x forward earnings. That’s fine assuming it can grow at the same rate it has done so over the past decade but it’s hardly a fire sale either.

Big tech was egregiously expensive in 2021. Now it’s dropped a lot. But not so much that the pendulum has moved to obvious no-brainer long territory either. As such, expect volatility this year as the bulls talk about how far their growth stocks are off the highs while bears continue to point out that valuations aren’t nearly as low as you’d expect to see at the end of the popping of a bubble.

On the other hand, smaller American companies should be stronger given current trends such as reshoring and cheaper energy prices in America versus the rest of the world.

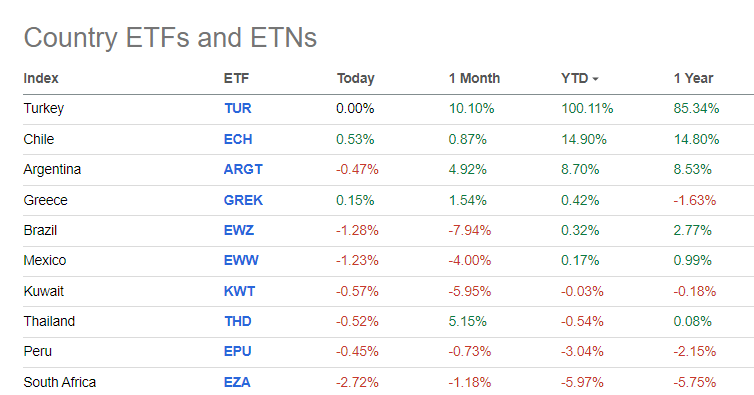

Another interesting point is with international stocks. Some smaller markets performed significantly better than the United States, Japan, and the larger European countries. Here’s Seeking Alpha’s top 10 country ETFs of 2022 (data as of Dec. 30):

Country ETFs (Seeking Alpha)

Turkey (TUR) enjoyed a massive 100% run-up as it stabilized following a major currency devaluation in late 2021.

Aside from Turkey, however, there is a notable theme to the rest of the top ten. Fully half were Latin American countries, with Chile, Argentina, Brazil, and Mexico all notching a positive return for 2022.

I expect this to be a recurring theme in the 2020s as Latin America wakes up after a brutal decade for its economies and stock markets. The return of inflation, commodity demand, and closer supply chains to North America all bode well for Latin America.

More broadly, it highlights my point that there’s more to investing than just the S&P 500. I believe investors in the major American indexes will be largely disappointed in 2023, with little ultimate change either direction after a choppy year. However, there could be considerably more opportunities for investors in other fields such as small-cap American stocks or select international markets.

As for the S&P 500, however, I see 2023 as being a difficult year, except for skilled short-term traders. Expect a lot of volatility and back-and-forth, but little ultimate change for the market as the S&P 500 declines slightly to my target of 3,622 this time next year.

Editor’s Note: This article was submitted as part of Seeking Alpha’s 2023 Market Prediction contest. Do you have a conviction view for the S&P 500 next year? If so, click here to find out more and submit your article today!

Be the first to comment