whyframestudio

Investment Thesis

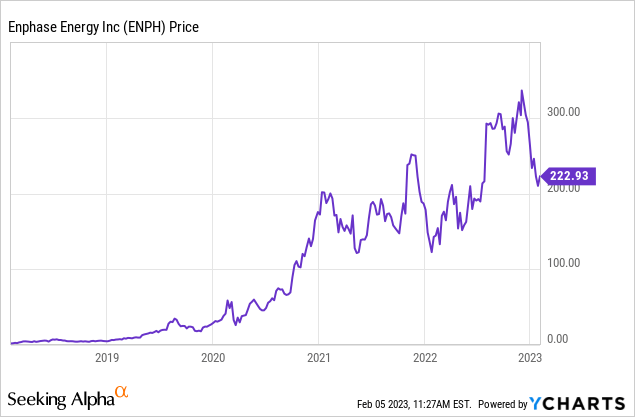

Enphase (NASDAQ:ENPH) has been one of the best-performing companies in the past 5 years, with its share price up over 9,500% during the period. Even though the broad market was down last year due to rising rates and inflation worries, the company still managed to record a 44.8% gain.

Despite having grown a lot in size, the company still manages to record exponential growth quarter after quarter. The company’s TAM (total addressable market) is huge and its penetration rate is still surprisingly low. It continues to benefit from the increasing adoption of green energy and the volatility in commodity prices. The latest result indicates strong demand led by international growth and the bottom line is also starting to see meaningful operating leverage. However, the valuation is still elevated even after the recent 30%+ drop in share price. It is priced for perfection and I do not see much upside from the current price. Therefore I rate the company as a hold and will wait for a better entry point.

Huge Market Opportunity

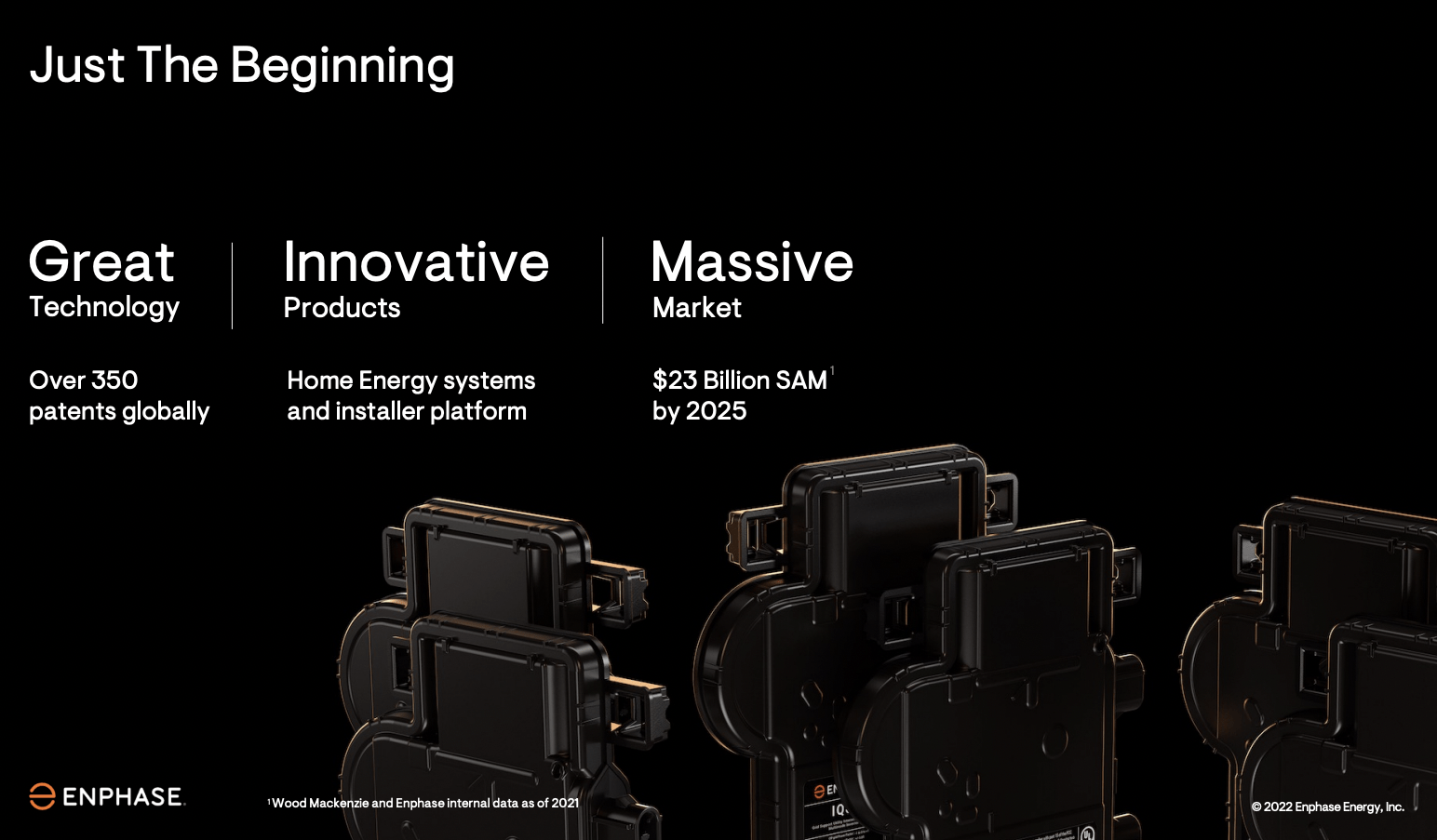

The popularity of solar energy has increased significantly in the past few years and its market is massive. According to Allied Market Research, the TAM for the global industry is forecasted to grow from $52.5 billion in 2018 to $223.3 billion by 2026, representing a CAGR (compounded annual growth rate) of 20.5%. According to Enphase, it projects the SAM (serviceable addressable market) to be $23 billion by 2025. Using its current sales, this translates to a penetration rate of only around 9.2% which is very low. In my opinion, the estimated SAM is extremely conservative as it does not include the opportunity for upcoming or potential products. For example, the newly released EV charger increased the company’s 2025 SAM by $6 billion.

The expansion in TAM is driven by multiple catalysts. The costs of solar energy systems have decreased dramatically and are expected to drop even further, which increases their affordability. The commodity price spike last year especially in Europe has made people question the reliability and affordability of traditional energy and they now want their own independent energy source. Governments are also providing incentives and tax rebates for solar energy products as they are heavily promoting renewable energy. We are still in the early innings of solar energy and there is still ample of room for further expansion.

Enphase

Increasing Share Of Wallet

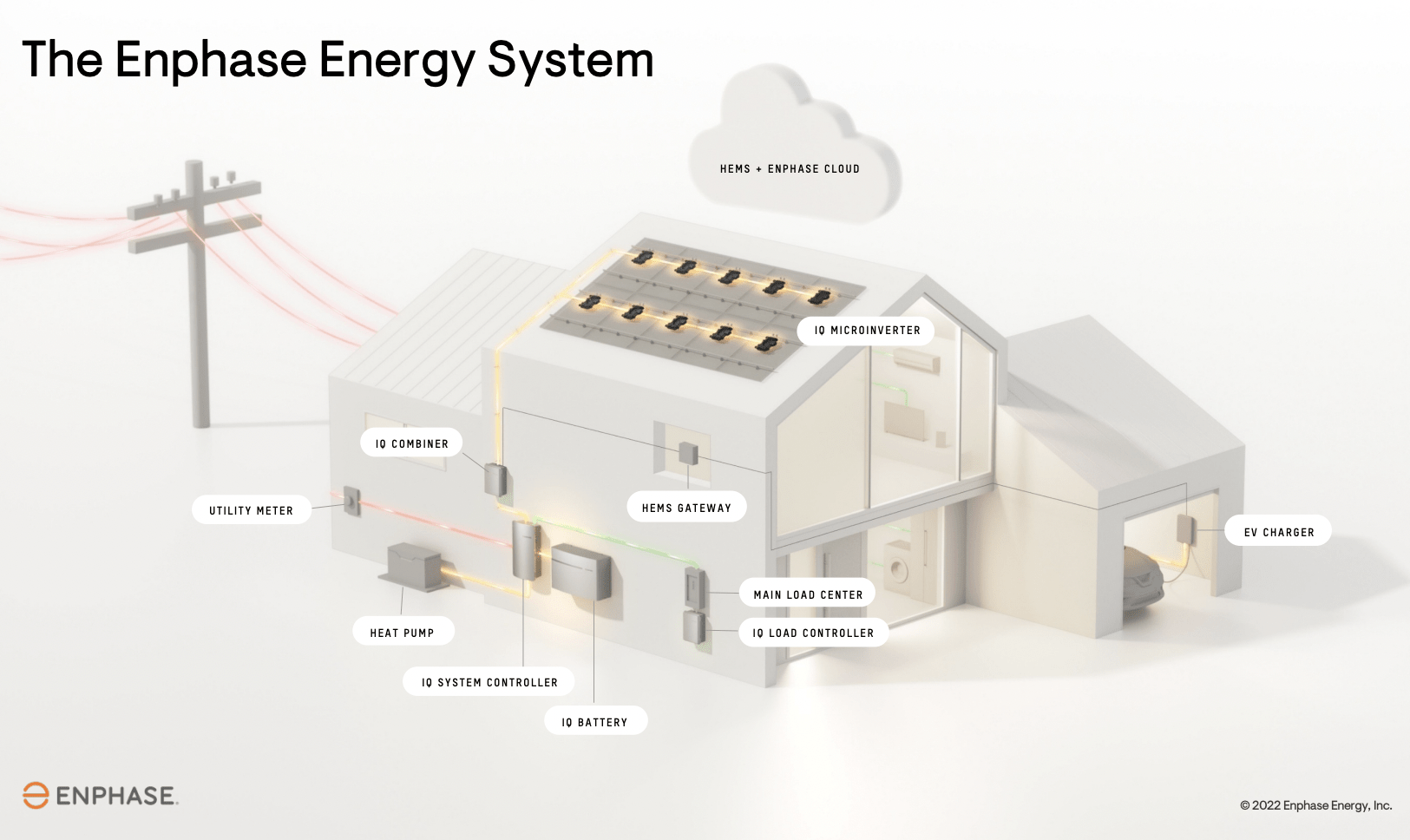

Besides the flagship microinverters, Enphase has been introducing new products in order to capture more “share of wallet”. It is aiming to build out a whole energy system built upon its product. The recent growth driver has been the IQ battery 10, an all-in-one storage system that allows users to store energy from their solar panels. It is extremely accretive to the company’s financials as the battery is much more expensive. The IQ battery 10 costs around $7,000 while microinverters only cost around $2,000. The introduction expanded the customer’s potential spending from just $2,000 to $9,000.

Another notable product includes its EV charger. I believe this will be a huge success as EV adoption continues to grow and it is estimated that 50% of vehicles will be electrical by 2030 according to S&P Global. There are also other emerging products such as Grid Services and Portable Energy Systems that could drive high spending. I believe this land and expand strategy will be an important growth driver moving forward.

Badri Kothandaraman, CEO, on EV chargers

As for new products, we expect to introduce smart EV chargers to U.S. customers in the first half of 2023 followed by Europe. We are excited about this product as it will provide connectivity and control, enabling use cases like green charging and allowing homeowners visibility into operation of their Enphase solar plus storage plus EV system through the Enphase App. We are very bullish about our EV charging business and continue to invest in it significantly.

Enphase

Excellent Financials

Enphase continues to report spectacular financials with yet another beat and raise. The company reported revenue of $634.7 million, up a whopping 80.6% YoY (year over year) compared to $351.5 million. The growth is driven by the international segment as Europe revenue was up 136% and Latin America revenue was up 129%.

Badri Kothandaraman, CEO, on Europe growth

In Europe, our revenue increased approximately 70% sequentially and 136% year-on-year led by strong demand for our microinverters in Netherlands, France, Germany, Belgium, Spain and Portugal, and for our IQ batteries in Germany and Belgium.

While the revenue growth was certainly outstanding, management teams’ discipline on cost and expense control is also very impressive, yet often overlooked by investors. I’m highlighting this because a lot of high-growth companies can churn out exponential sales growth but most fail to deliver on the bottom line.

Gross profit increased by 90.8% YoY from $140.4 million to $267.9 million as gross profit margin increased from 39.9% to 42.2%. Despite an over 80% increase in revenue, operating expenses only increased by 28.6% YoY from $103 million to $132.5 million. This demonstrates the strength of Enphase’s branding and reputation as it does not need to spend much to drive sales. This superb operating leverage resulted in operating income growing 262% YoY from $37.4 million to $134.5 million. The operating margin also doubled from 10.6% to 21.3%. This kind of economy of scale is almost unheard of and the company’s balance sheet is also very strong with $1.42 billion in cash and only $1.31 billion in debt, which provides financial flexibility for potential M&A or even share buybacks.

Q4 Earnings Expectation

Enphase is going to report its Q4 financials later today and revenue is expected to grow 70.4% while EPS is expected to be $1.26. I think the company is going to beat as usual but the guidance and profitability are going to be key. At the current valuation, any miss will likely cause a negative reaction to the stock price as expectations are high. Due to inflation, cost control is even more important and I hope gross margins can maintain at previous levels. Operating expenses are another focus to see if the company can continue to show strong operating leverage. I will be eyeing management’s commentary on overall demand to see if the slowing economy and lowered commodity prices are impacting orders. It is also important to look at the demand for new products such as EV Chargers as they play a huge role in the land and expand strategy.

Investor Takeaway

There is no doubt that Enphase is a fabulous company. The solar energy market is huge and presents massive growth opportunities. The current penetration rate of the company is still tiny and the market expansion will continue to be a strong tailwind. It is also launching new products to capture more spending from existing customers and its IQ batteries have been seeing success. Revenue growth continues to be fabulous but the level of operating leverage it has is even more impressive.

However, my only problem with the company is its valuation. The company is currently trading at a PE ratio of 108.7x which is extremely expensive. Even if we factor in its growth, the fwd PE ratio is still at 45.1x. At the current price, I believe a lot of optimism and catalysts have already been priced in. Yet, a slight miss in revenue or a small bump in manufacturing will trigger a huge downgrade in valuation. This is why I do not think the risk-to-reward ratio now is attractive and investors should wait for a more compelling price point. I rate the company as a hold.

Be the first to comment