vernonwiley/E+ via Getty Images

As investors, we also always have to be aware of our innate and very human tendency to be fighting the last war. We forget that Mr. Market is an ingenious sadist, and that he delights in torturing us in different ways. – Barton Biggs

There’s one universal thing that all human beings have in common: We are not good at predicting the future. No matter anyone’s pedigree, you can only use the information presently at hand to make an informed prediction.

Just think back to what so many thought last year at this time:

- SPACs were going to democratize access to capital markets usually reserved for the elite and empowered companies against oppressive Wall Street fees.

- Inflation would likely be “transitory” and not require extensive action from the Fed as supply chains would be ungummed, and things would return to normal.

- There was a stable international structure, and military confrontation between great powers seemed a remote possibility.

Unsplash.com

These three instances show how predictions are always just a snapshot in time, and often when they’re correct, it can be for the wrong reasons. Or, even when predictions turn out entirely correct, they might be helpful.

Take the sell-side’s startlingly accurate earnings prediction of $221 for 2022, but the general failure to anticipate the severity and length of the current bear market. Sometimes you can predict something right, but the market might laugh in your face and do the exact opposite of what you thought it would do on the news or data you correctly anticipated.

Other times, massive changes occur that might be difficult to price or even comprehend, like the international system being shaken to its core. Many year-end targets last year, for instance, experienced a kind of obsolescence as soon as it became clear that Russia’s invasion of Ukraine would turn into a sustained, high-intensity conflict between two nations central to the trade of many vital commodities.

It’s prediction season again – a flurry comes right between Christmas parties and New Year’s Eve. It is within this holiday spirit I now embark on making some predictions for the new year, but draped in humility and acute knowledge of the futility of my task. Mostly, I want this article to be a thought-provoking and worthwhile read as we turn the calendar. In short, this year’s great debate will shift from the scourge of inflation to the fear of recession.

Initial joy at what I suspect will be a rapid rolling out of the inflationary tide will be short lived, as the next thing in the market’s sight is a potential recession. Most fear a recession, and some think the economy is more robust than most would suspect. And the Great Game goes on…

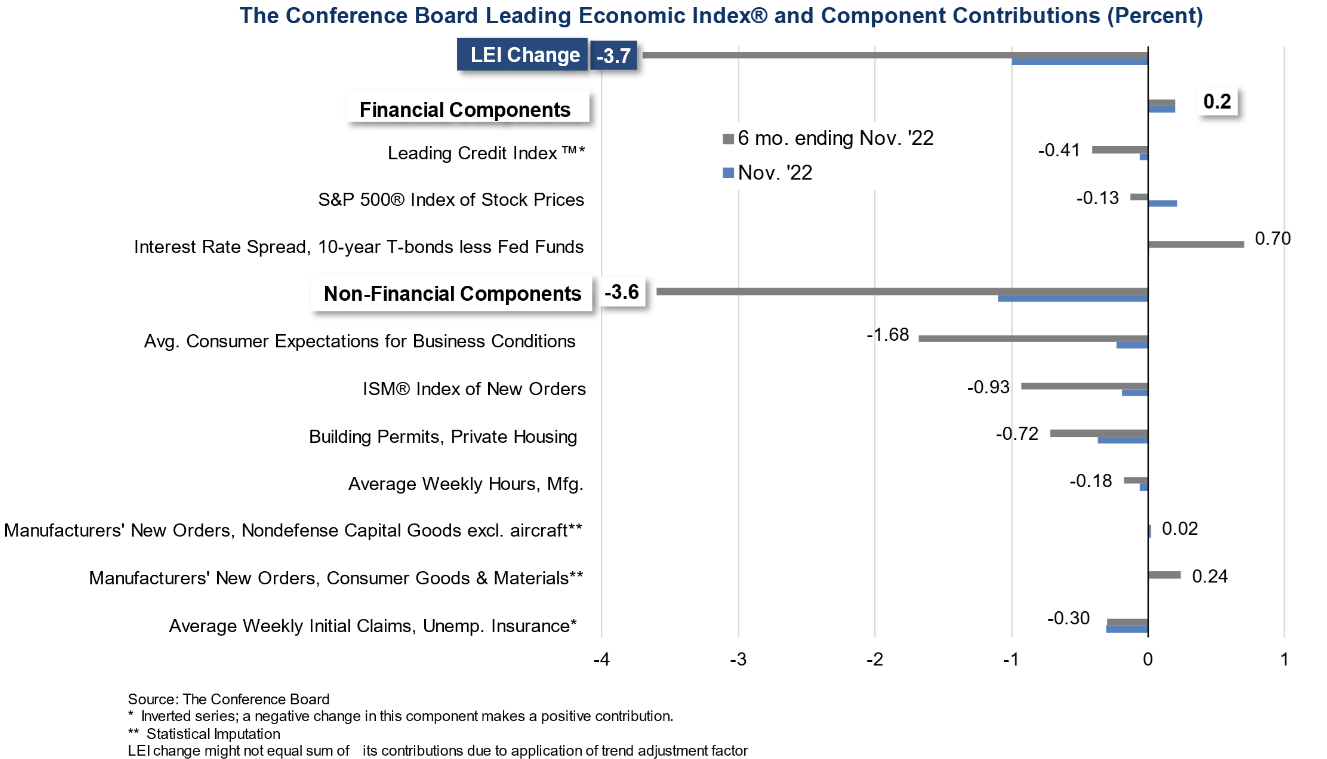

The Conference Board

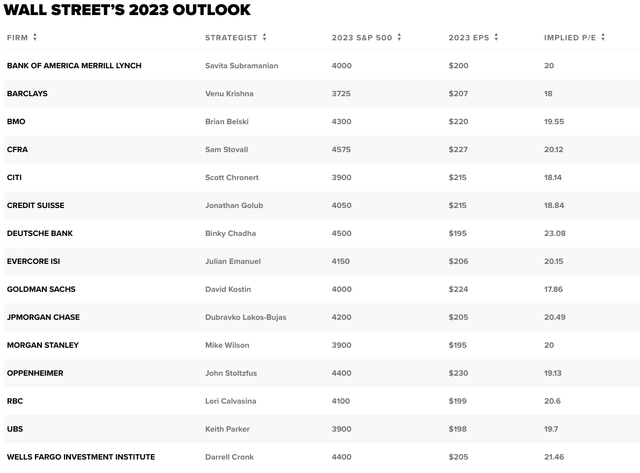

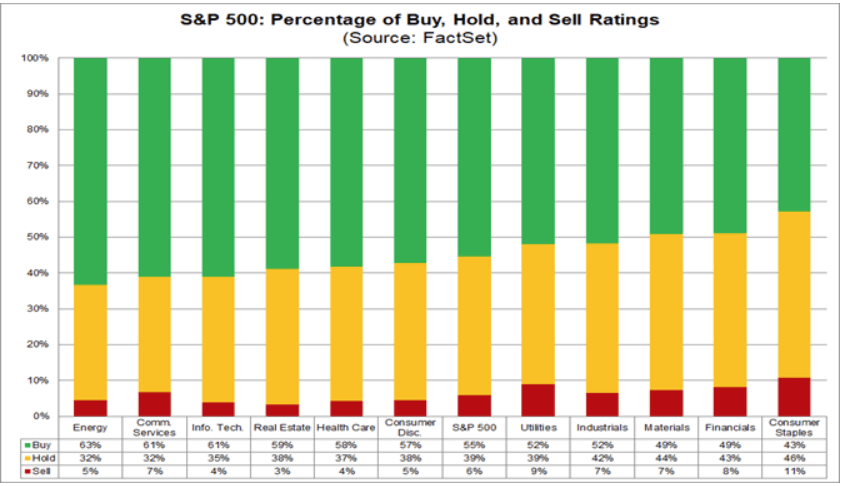

The outlooks shown below had an average price target of 4,140. The average estimate for earnings is about $209, which is less than last year’s average of $223 by about 6.3%. The average P/E target for the sell-side shops listed below is 19.8 this year, which is pretty high given historical trends. It was an average of 17.84 for 2022.

Markets likely transition from consternation about the Fed’s actions to hopes for accommodation between midway and three-quarters into 2023. When this occurs, I suspect a significant inflow will come from fixed income, where a lot of capital will be hiding out in the first half after bonds had their worst year on record and the risk/reward looks favorable.

The relative appeal of equities compared to debt will be higher if the Fed cuts sometime in 2023, in contradiction to the current dot plot.

CNBC Research

Generally, most shops believe the first half will be challenging, and I fully agree. There’s a discrepancy between those willing to play their hands thinking the Fed is bluffing and those who are taking the Fed at face value. There’s also a reasonably wide discrepancy on the sell side as to whether there will be a recession or not.

Market Fixation on Inflation/the Fed Will Move to Assessing if a Recession Is Imminent/Ongoing

Many people were not alive during the last go-round with the Fed’s campaign to end inflation under the good Mr. Volcker, or at least not conscious of markets on a day-to-day basis. The Fed of Volcker’s day was a different animal, though. For example, the Regulation Q interest rate ceilings gave the Fed an effective way to instantly cause a financial crisis by raising the Fed Funds rate higher than the rate on bank deposits.

This would cause money to flood out of the banking system into money market mutual funds, constraining the extension of credit. This made monetary policy more precise. Now, the jawbone is the strongest bone the Fed has in its body, so it cannot afford to lose credibility or risk losing control of financial conditions, inhibiting its mandate. Right now, the consensus on the street is that a recession will likely occur in 2023. Many indicators suggest this, as you can see below.

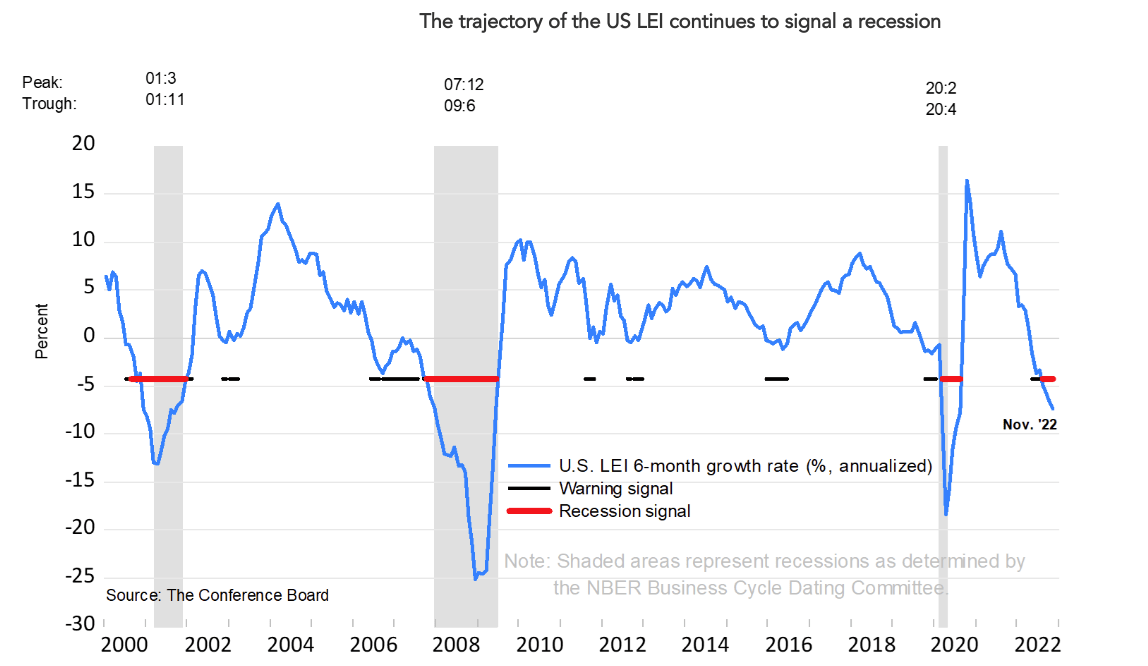

The Conference Board

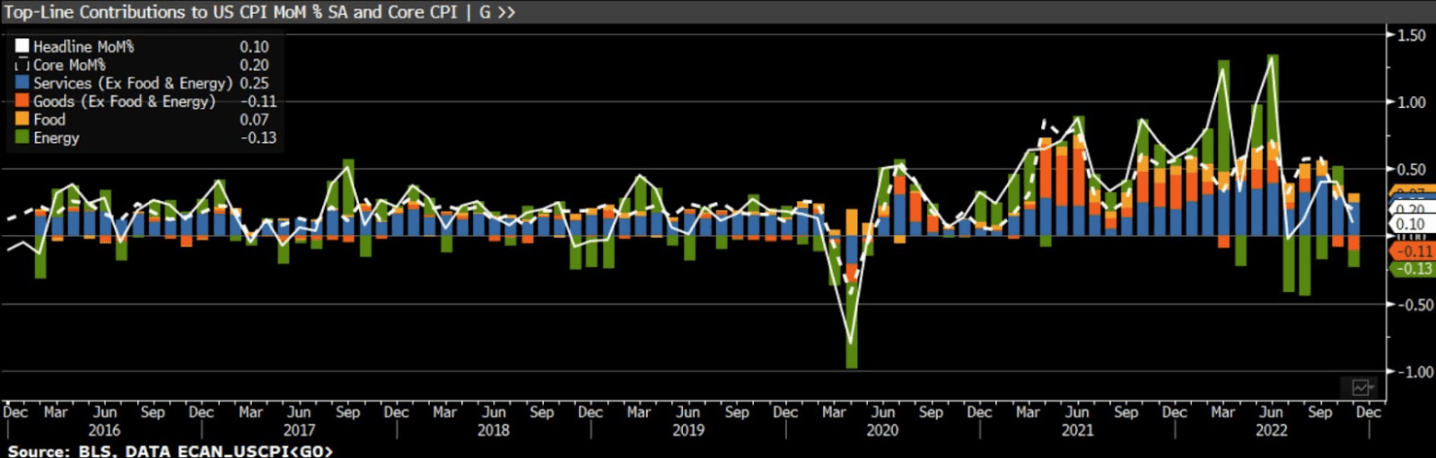

But, inflation is coming down, and the leading data and particulars with how things like CPI are measured cause the backward-looking headline numbers to be higher than the reality on the ground in the economy. There is clear evidence that the Fed has made the lion’s share of progress on inflation, and thus light at the end of the tunnel can be seen. However, there will be some more mirages (bear market rallies) along the way until a buy-the-dip regime can be restored when markets might see through the risks that have been vexing them throughout 2022.

Inflation still could crop up again on an energy price spike or another idiosyncratic driver, but the inflation expectations appear well anchored, and the tightening is making its way throughout the economy. A significant minority also believes that the recession could be narrowly avoided (soft-landing scenario) or will be of a minor variety.

So, although the Fed has been wrong, and although it might be wrong again, the one thing that can unify the hawks and doves on the FOMC is maintaining the upper hand in tightening financial conditions when they’d prefer them to be tighter. That’s why Powell has kept coming out with the belt month after month following the summer rally. But the tightening is clearly working, and with QT, the effective fed funds rate is even higher than the nominal rate.

BLS, Bloomberg

Inflation shows signs of significant alleviation, but Powell keeps talking tough. Whether the bond market is right and the Fed begins tightening in the back half of 2023 or whether the “dots of doom” (the Summary of Economic Projections) is right will have a significant bearing on where the market ultimately settles. Of course, the multiple will be dependent on this outcome.

The Atlanta Fed Market Probability Tracker now sees a wide potential differential for our year-end target period. In a bullish scenario where the Fed is forced to turn dovish in the middle of 2023, the rate could be around 3.5 at the end of the year. If the Fed sticks to “high for longer,” the rate will be around 5.1%.

If it’s at the upper bound, then debt remains competitive with equities, if not the safer alternative. Equities will be more attractive if it comes in at the lower bound, and future earnings will be discounted less (higher valuations). This is why it’s still the Fed’s show in 2023, and all we can do right now is guess what they’ll do with the limited information we have.

Atlanta Fed

For my part, I see evidence that the commentators who believe the dot plot is overly hawkish compared to how reality will play out are likely correct. My reasoning here is that if the Fed tightens and the economy proves resilient, the market will likely be able to rally in the face of this after some appropriate consternation in the first half of 2023. And, by the end of 2023, we will be looking to a brighter future with more accommodative financial conditions.

If the Fed causes something to break or some other exogenous risk causes forced liquidation on a meaningful scale, the Fed is better equipped to rectify the situation in that case and likely will by the end of the year in 2023. Jay Powell has stated this is his opinion unequivocally. He’d prefer to overtighten and correct his mistake, which likely makes more sense from his seat than from ours. Heavy is the head…

Putnam Investments, Bloomberg

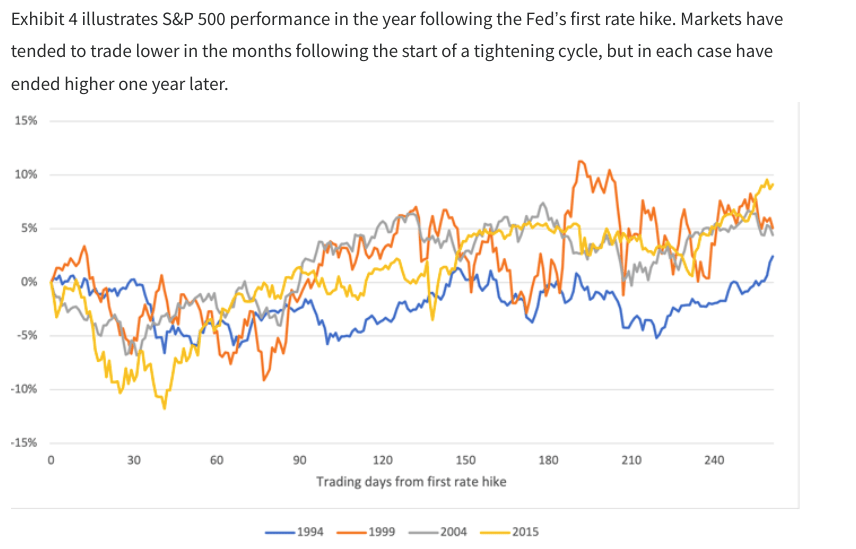

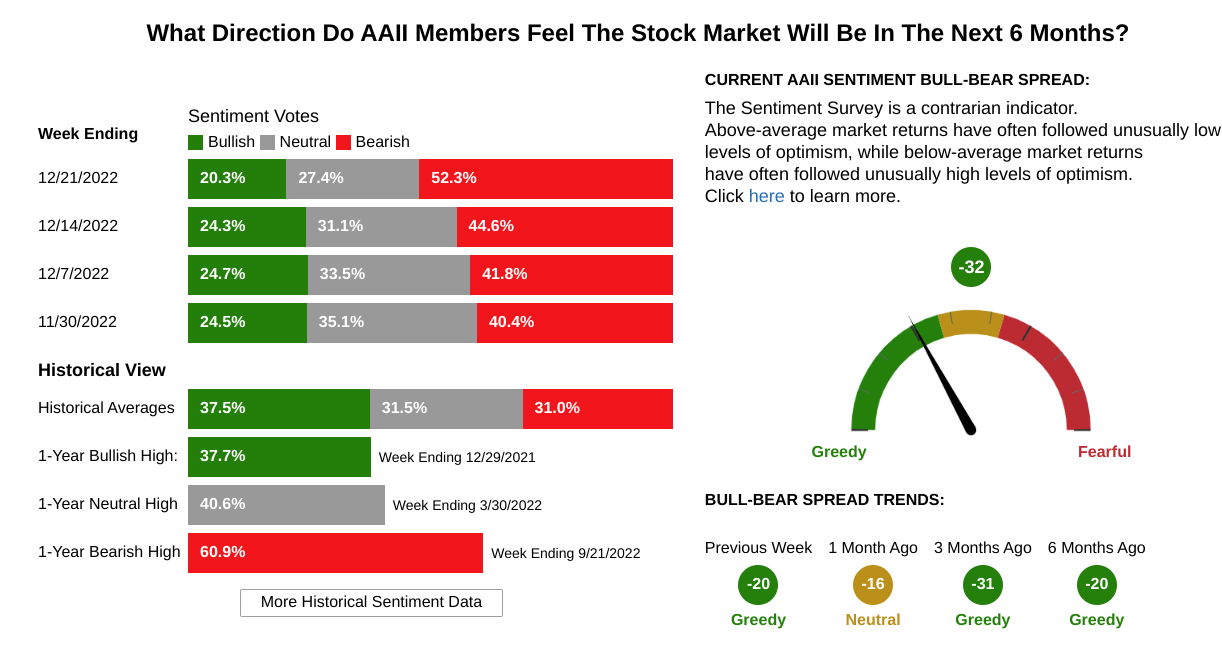

Nonetheless, the data from previous hiking cycles (meek as they might have been in relation to this one) indicates that if you’re more than midway through the hiking cycle, the market can start seeing through and rallying. By April or May, more should be revealed about the Fed’s intentions, and we’ll have some new dots to go off of. This precedent makes me more biased toward the upside, particularly when considering historically bad sentiment. People are offside during upside moves and better positioned for downside ones.

AAII

To be clear, I think a lower low is likely in the first half. However, I also think once a capitulatory flush-out occurs with a significant VIX inversion and the spot above the 52-week high, markets will recover very quickly and multiple expansions will again become possible, particularly if a Fed u-turn is required to steady the boat. The Fed and regulatory authorities are a lot better prepared to handle contagion than in the past. Their ability to quickly resolve failing entities, higher capital standards, and statutory authority to prevent contagion is significantly augmented compared to the past. Remember the accompanying financial crisis in March 2020 in the depths of COVID-19? Yes, neither do I.

Sentiment and Regulatory Changes Should Help Mitigate Potential Financial Crisis

In an unlikely, severely adverse downside scenario, a policy error could cause prolonged periods of volatility or uncertainty as the Fed struggles to regain credibility; none of these price targets or P/E estimates will be handy anyway. One thing Wall Street is often biased about is considering the government incompetent. This can undoubtedly be true, but the Fed and its prudential friends seem to have done their jobs well. Despite a vicious bear market this year, the elevated VIX levels of 2020 were not revisited.

Boston Consulting Group

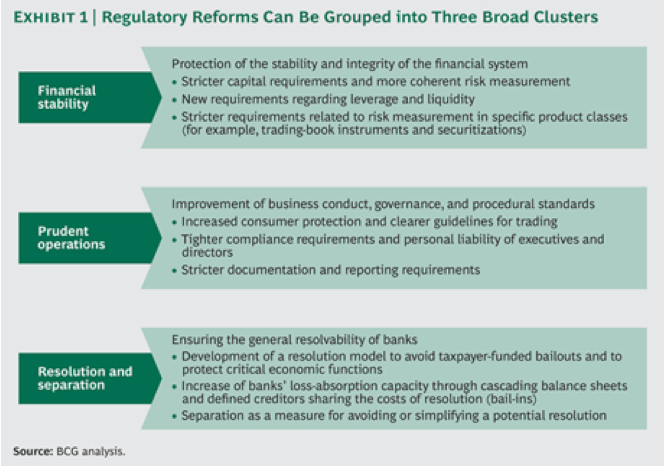

However, the regulation in the housing market has shown that the efforts around a decade ago to improve regulation have likely improved financial stability and made mass forced liquidations, the most significant risk to markets, much less likely. This also limits potential downside.

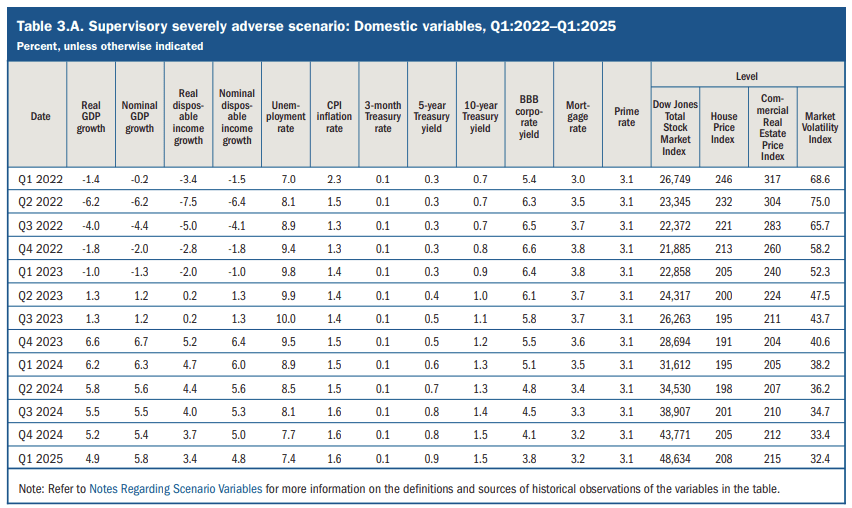

What I mean by the “greatest risk” is that the stock market got cut in half in the Great Financial Crisis when the real economy was seemingly fine. When there was a massive threat to the real economy from COVID-19, but capital levels were more conducive to financial stability, the market fell only 33% before rallying sharply. For what it’s worth, the Fed’s own idea of a severely adverse economic scenario from their 2022 Dodd-Frank Stress Test is below to give you an idea of what they think a worst-case scenario would be like.

Federal Reserve

2022 was an extraordinary year in the markets. Markets bled down, and the VIX stayed relatively subdued. After the turkey shoot of 2021 and a global pandemic, it’s harder to predict earnings at the company level, given the wayward and unpredictable nature of trends and their effect on historically more predictable economic cycles and industry dynamics. The earnings growth in 2021 off of 2020 comps made analysts’ jobs considerably harder in predicting forward earnings.

Seeking Alpha

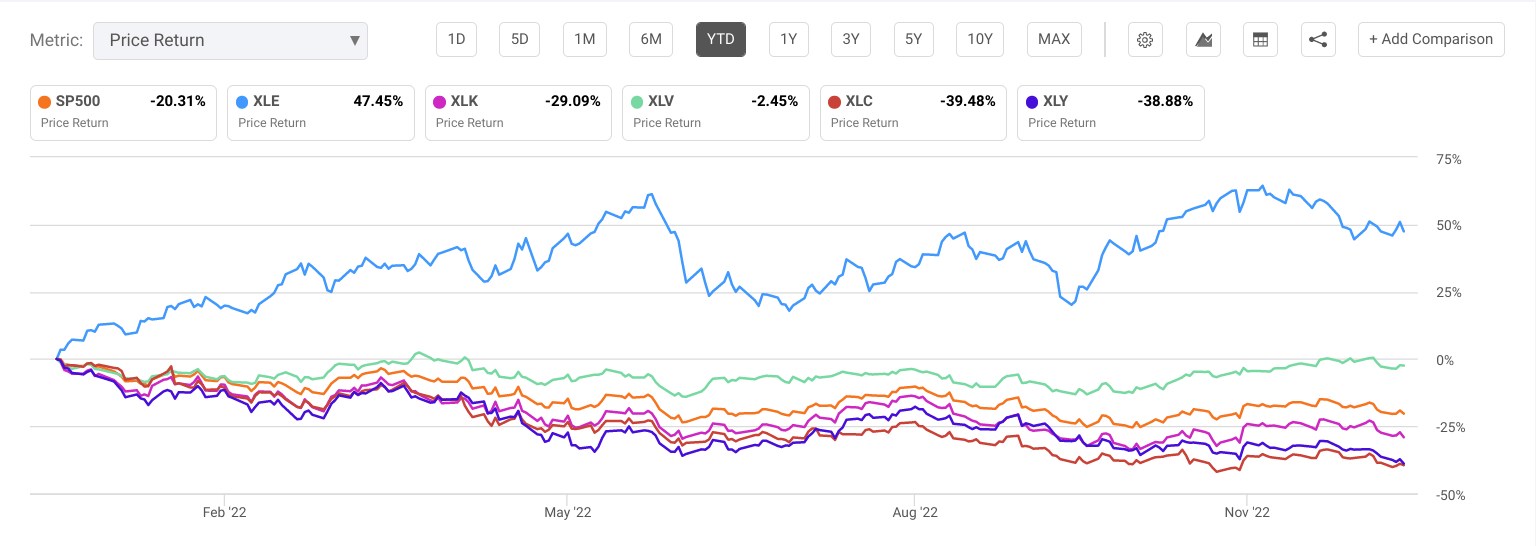

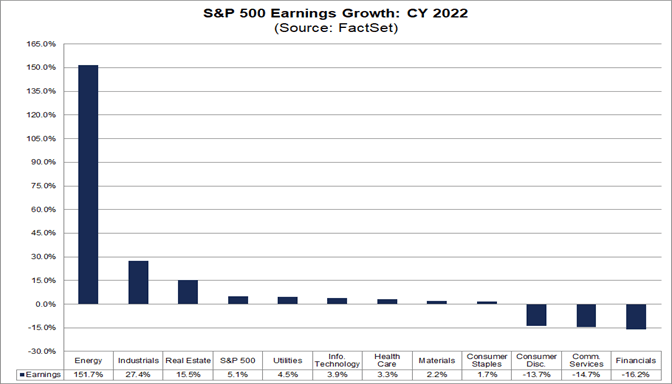

Energy outperformed by a long shot while Comm Services Consumer led to the downside. Next year, there’s likely not a lot of relief for discretionary, but the American consumer has held up very well, probably partially because the credit cycle has been knocked out of sync with the business cycle by the generous pandemic assistance. While some indicators point to recession, others, like consumer confidence and low credit utilization, suggest that U.S. consumers aren’t entirely down for the count yet.

Earnings Will Likely Contract Limits Upside; Energy Will Be Key

Factset

I like to look at the relationship between stock valuations and interest rates, like the relationship between rain and crops. I am a native Californian and have, unfortunately, lived through several droughts now. At the height of the drought, almond farmers get particular flack from political factions in the state because their crop is so water intensive.

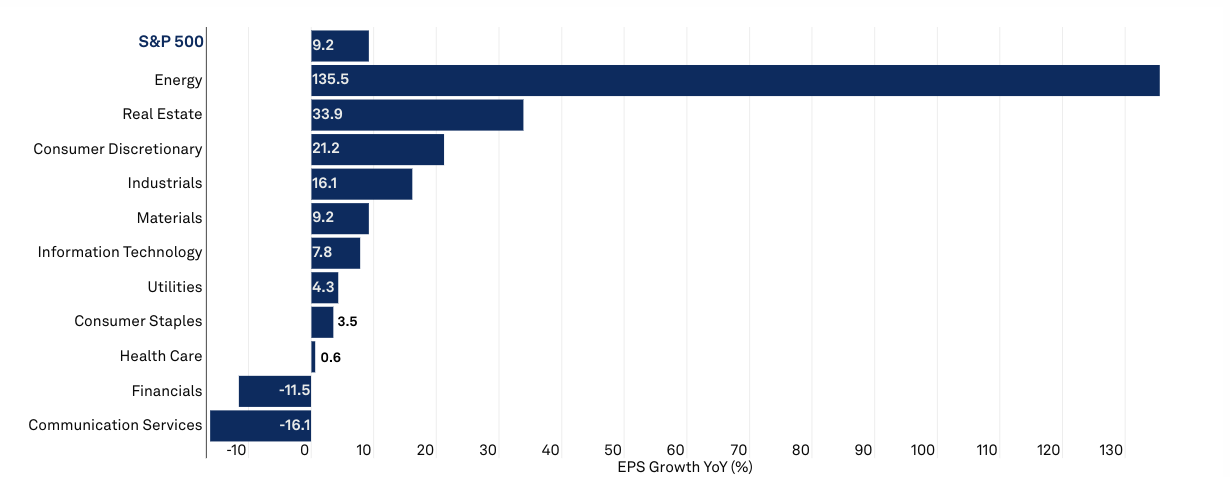

Growth stocks with high P/E ratios are like water-intensive crops. When the liquidity shuts off during Fed tightening (less rain), then it’s hard for these “crops” to perform well, no matter how good the “seeds” (fundamentals) might be. Energy has had its best year, but its market cap share is still far below its share of earnings last year.

With supportive secular factors on the supply side and management more focused than ever on returning capital to shareholders, I think this sector continues to be strong, at least through the first half when there’s more clarity on Fed action and the potential for recession. Once the end of tightening is firmly in sight, valuations should expand. Thus, one of the primary “upside risks” is a collapse in inflation that exceeds consensus expectations.

S&P Global

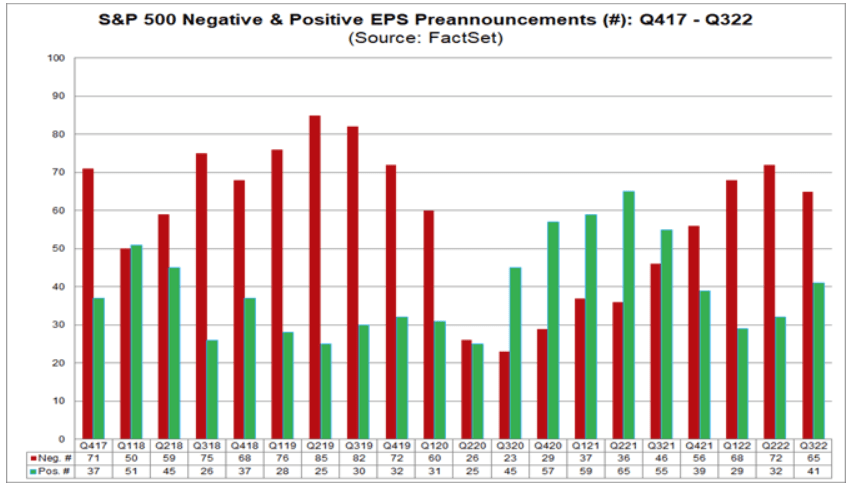

Guidance continues to be primarily negative, but positive guidance has been building in the last few quarters. Macro factors were driving the market in October around the British “mini-budget” of Liz Truss, but idiosyncratic factors have steadily been becoming more important.

For example, last quarter, the companies that beat expectations were handsomely rewarded relative to the last few years. Idiosyncratic factors should continue driving markets, and index-driven strategies should take a back seat to good old-fashioned stock picking as long as it successfully identifies outperformed. 2023 will be a good year for stock picking, and idiosyncratic factors should continue driving performance.

There will be a premium on quality management teams as plenty of obstacles will need to be circumvented. Preannouncments have been moving in the right direction.

Factset

I believe earnings will be supported by energy again, which should mitigate the headline effect of the upcoming earnings recession. Companies have recently been through a crisis and made difficult changes that have increased operating leverage in many cases.

This can be an albatross if economic activity significantly declines, but if it declines less than consensus anticipates, companies can outperform increasingly negative earnings expectations. If we continue getting a reversal of the very strong dollar in 2022, it should also alleviate some of the downward pressure on earnings. I suspect earnings expectations will initially overly discount a lousy outcome before showing some unanticipated strength.

Factset

My Year-End Scenarios and Respective Targets

I am going to use the rough average of estimates for earnings in 2023 of $215 on a P/E ratio of 20 to arrive at a projected 2023 year-end price of 4,300. This represents approximately a 12% upside from the close on Dec. 23rd, 2022. This is my base case scenario.

In a less probable bullish scenario where a soft-landing and pause of hikes is definitively achieved sooner than midyear, earnings surprise significantly to the upside, or there is an unexpected resolution of the war in Ukraine, then I would put earnings of $220 on a 21 multiple since tech will once again be able to buoy the market. This would result in a year-end target of 4,620.

In a less probable bearish scenario caused by “something breaking” or an adverse geopolitical development like an escalation of the war in Ukraine or a blockade of Taiwan, the resulting contraction in global trade and demand will likely hit earnings. If inflation proves persistent and the following dot plot contains an even higher terminal rate, this would also be in the adverse camp. In this event, I think $200 on a multiple of 17.5 is appropriate, bringing the bearish scenario year-end target to 3,500.

Main Risks to My Target

Inflation proves more persistent than current progress would indicate

This would mean the Fed has to do more, and the potential for stress and obstacles to economic expansion will take a more tremendous toll on earnings and keep sentiment depressed. A Fed policy error where the FOMC loses credibility could cause a sustained period of adversity for risk assets and the U.S. economy.

Geopolitical risks involving the Russia-Ukraine War and the world’s second-largest economy, China

The war in Ukraine does not appear close to ending, but it has achieved a temporary stasis. If Russia conducts a large-scale offensive in the spring that increases intensity or a serious escalation/WMD (weapon of mass destruction) use occurs, this will be a significant headwind on markets and the global economy in general. How China handles the current COVID-19 outbreak and recently boiling political tension (and how their economy is affected by both) will be another significant wildcard in 2023.

The course of the U.S. dollar will have significant consequences for earnings

Mega-cap weakness has been holding indices down recently. If they are able to get some relief from declining U.S. dollar headwinds, then they might be able to ride the storm better. But if dollar strength persists on the back turmoil across the global economy, it will likely make the earnings recession significantly worse and will also likely mean there’s a lot more downside for high P/E stocks and businesses with a large share of international sales.

A flock of potential black swans is stalking the market; the most acute risk would be a significant clearinghouse failure

The notional size of burgeoning global derivatives markets dwarfs the size of the real global economy. Unlike many sections of the financial system, the risk was actually augmented by the Dodd-Frank reforms by forcing all bilaterally cleared derivatives onto centralized exchanges. Any more acute version of what happened to the London Metal Exchange nickel debacle after the Ukraine war began could cause global financial contagion similar to – or worse than – the mortgage meltdown a decade and a half ago.

Worse-than-expected recession in the global or U.S. economy could lead to low energy prices, significantly lower energy earnings in 2023

If this happens, it will stop masking the declines across other sectors in the S&P 500, and an earnings recession will be more apparent. A recession would also make the prodigious buybacks that have been propping up markets over the last years less frequent and remove what’s been a serious contributor to the superior returns of the last decade.

Sometimes the early bird gets the worm, but sometimes the early bird gets frozen to death. – Myron Scholes

Editor’s Note: This article was submitted as part of Seeking Alpha’s 2023 Market Prediction contest. Do you have a conviction view for the S&P 500 next year? If so, click here to find out more and submit your article today!

Be the first to comment