zorazhuang

Investment Thesis

Southwestern Energy (NYSE:SWN) is primarily a natural gas company. That means that when natural gas prices go up, this company’s operating leverage works wonders.

And when natural gas prices go down, Southwestern Energy’s free cash flow rapidly dwindles.

What’s more, with natural gas prices rapidly moving lower, there are plenty of reasons to throw in the towel on this stock.

But here I explain that despite the near-term looking uncertain, the medium-term looks very compelling.

Ultimately, why paying 6x free cash flow for SWN is an attractive investment.

Crunch Time For Natural Gas

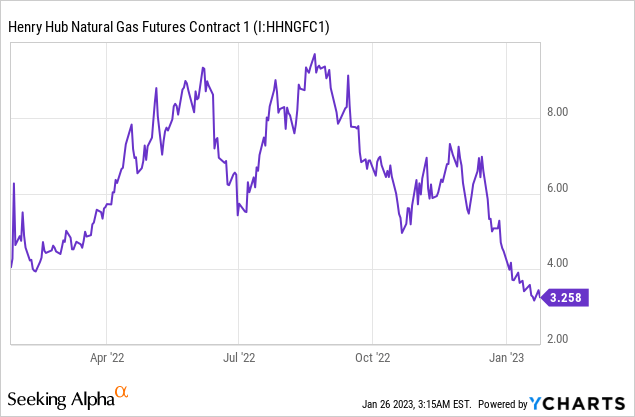

If you are reading this article, I presume you know that natural gas prices have imploded recently.

Prices are down about 50% in a month. The message from the spot market is clear. We won’t need any more natural gas in the foreseeable future.

We just got over this winter, when everyone was talking about there being a potential energy crisis. And now the dynamics rapidly went from a crisis-type shortage, and spikes in natural gas prices, to overabundance.

Time to Call it a Day Here?

The problem is made worse by two aspects. In the first case, the unseasonably warm winter impacted the amount of supply the US used.

Secondly, the Freeport LNG facility, that’s responsible for approximately 17% of LNG exports out of the US has seen its reopening delayed countless times since August. More specifically, Freeport LNG exports about 2.2 bcf.

This led investors to believe that despite Freeport LNG asserting that in January it would reopen, this may not be the case, at least not immediately. And that even if it does resume soon, it will be in small batches.

Altogether both characteristics have made natural gas supplies turn from scarce to oversupply.

What’s more, even after the Freeport LNG facility reopens and temperatures revert to seasonal averages, there will be a natural gas stockpile glut that will take a long time to go through.

Altogether, it now appears $5 MMBtu is a mirage for 2023.

Got It, So This Trade Is Now Done?

I don’t believe this trade is done. In the first instance, there’s reason to believe that a partial restart of the Freeport LNG is imminent.

In the second instance, the major tailwind for US LNG hasn’t gone away because of a few weeks of low natural gas prices.

Presently, the difference between natural gas prices in the US and in Europe is more than 6x. Essentially, there’s no reason for prices in the US to be so much lower than this much-coveted energy commodity in Europe.

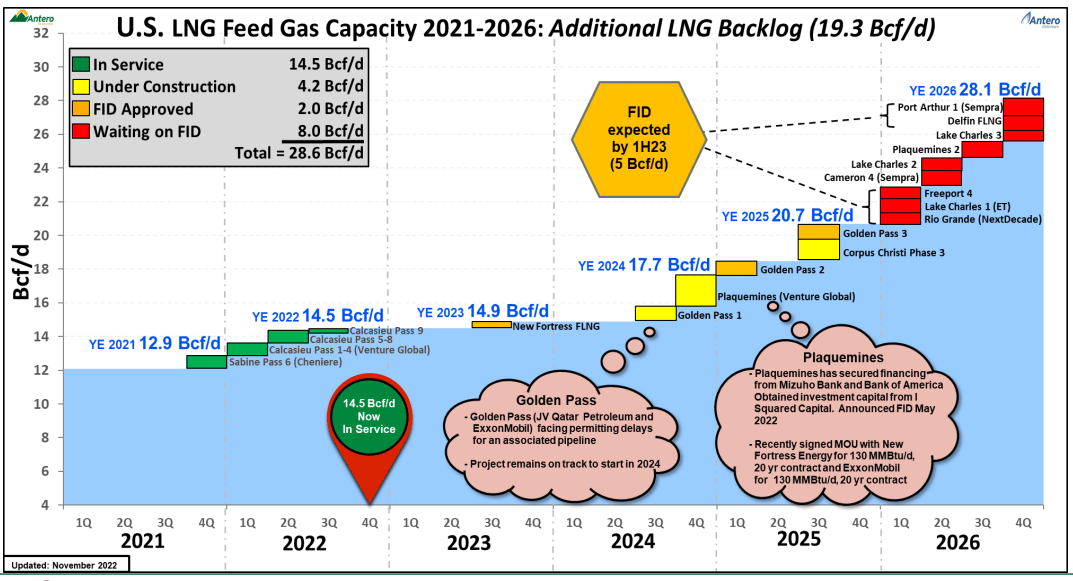

Antero Resources presentation

Thirdly, and perhaps the most important consideration, next year we’ll see LNG exports go from 14.9 bcf/d to 17.7 bcf/d. That’s approximately a 17% increase. Note, this is on top of the 17% that will come back online from Freeport LNG in 2023.

Consequently, my argument is that this is not the time to sell SWN.

SWN Stock Valuation — 6x 2023 FCF

SWN is 60% hedged in 2023. That means that only 40% of its production is exposed to natural gas prices. What in late 2022 seemed like a blemish in the bull case, has ironically turned out to be now a huge cash driver for SWN.

The hedges are priced at about $3 MMBtu. That means that by rough estimates, SWN will make about $1.2 billion of free cash flow this year.

In sum, paying six years’ worth of cash flows for one of the most coveted energy sources doesn’t strike me as expensive.

The Bottom Line

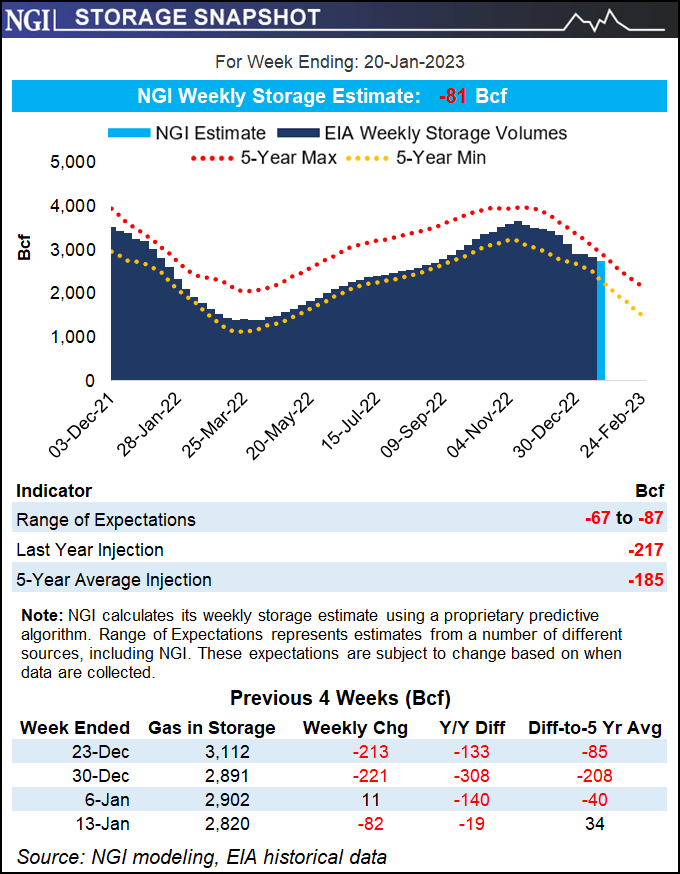

Natural Gas Intel website

There’s a lot of fear that natural gas prices are going to continue trending lower. However, I simply don’t buy this argument. Natural gas is a key energy source. Natural gas is far superior in terms of cost to many other energy sources. Natural gas is flexible, with a range of uses, including chemicals and feedstock, such as ammonia input. Natural gas is reliable.

In sum, paying 6x free cash flow for SWN is a compelling risk-reward, irrespective of what the spot price may lead one to believe. Stay long SWN.

Be the first to comment