tomos3/iStock Unreleased via Getty Images

Thesis

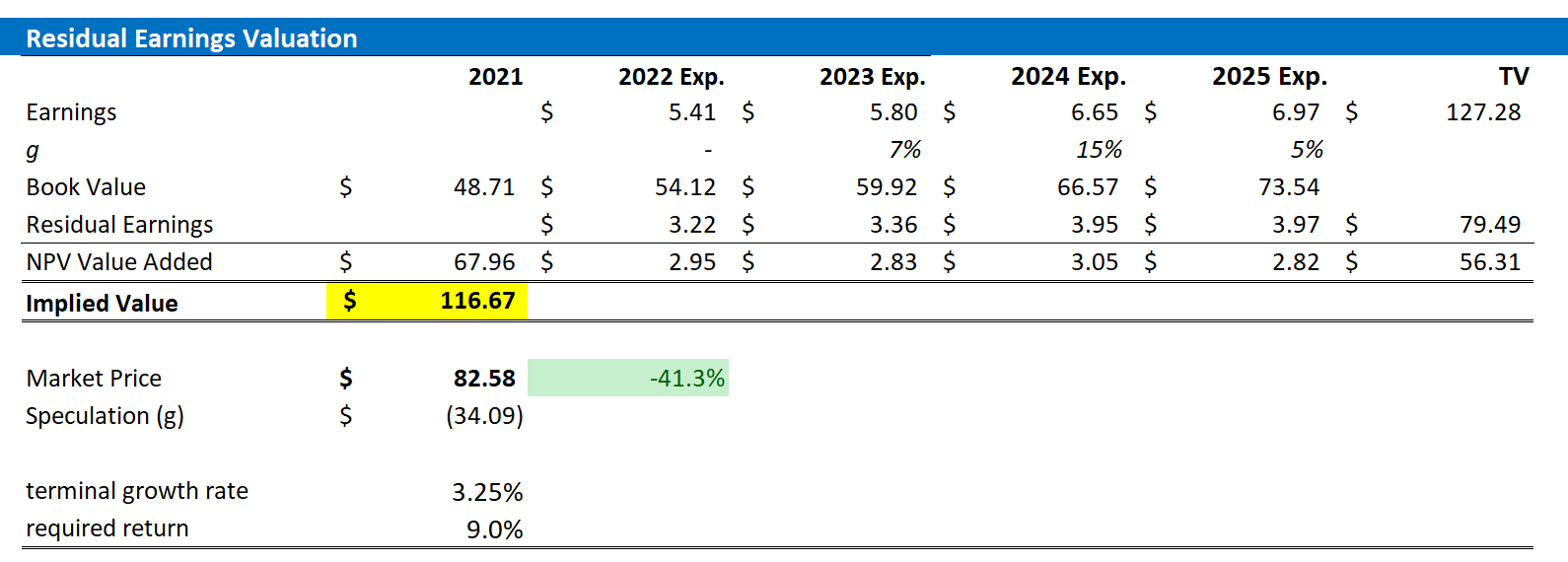

At a one year forward P/E of < x15 and EV/EBITDA < x8, Sony (NYSE:SONY) stock looks too attractive to ignore. The stock is down about 40% YTD, double the drawdown of most international equities, and long-term investors might want to appreciate the share price weakness as a buying opportunity, I believe. Personally, I see approximately 40% upside as I calculate a $116.67 share-price target. I anchor my recommendation on a residual earnings framework based on analyst consensus EPS estimates.

A Quick Company Overview

Sony is one of the world’s largest electronics companies with a strong portfolio for consumer, professional and industrial markets. The company develops, manufactures, and distributes devices such as game hardware and software, televisions, media recorders and players, video cameras, mobile phones, and image sensors. In addition, Sony also produces music and video entertainment as well as game applications. That said, Sony operates 7 major segments: Game & Network Services (G&NS) is the most important segment with approximately 30% of sales, followed by Electronics Products & Services (EP&S) with about 20% of sales, followed by Financial Services, accounting for nearly 20%. The rest is distributed music segment, pictures segment, imaging & sensing solutions and other—each accounting for about or less than 10% of sales. Geographically, Japan is Sony’s largest single market accounting for more than 30% of sales, followed by the US and Europe with approximately 25% each.

Sony Investor Presentation

Sony’s Opportunity

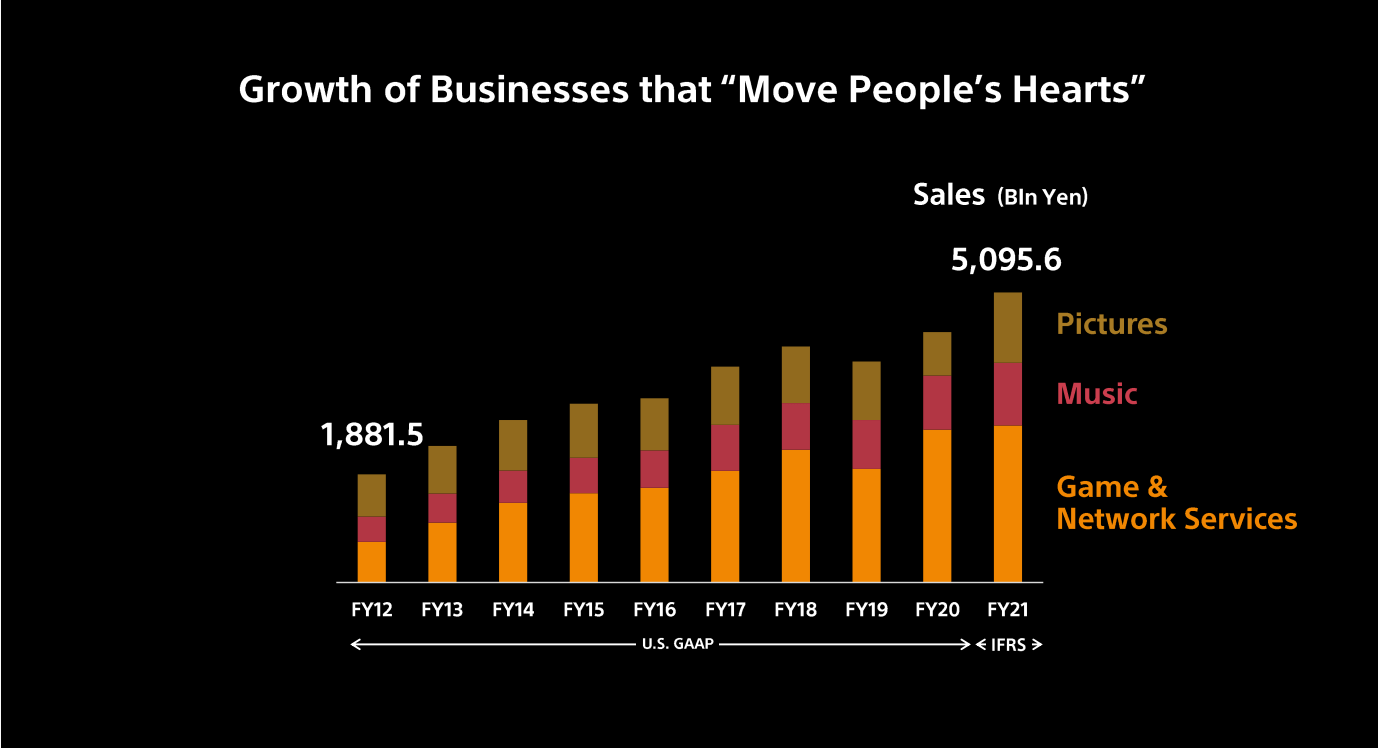

I am bullish on Sony as I believe the company is well positioned to capture some of the most exciting secular growth trends. If for example, we consider the metaverse as an evolution of the digital communication system, then Sony has multiple business opportunities in this space: OLED micro-displays, SPAD sensors, gaming, content, VR headset, virtual production tools. That said, while Sony’s metaverse exposure as a leading electronics hardware manufacturer is undisputed, I am also highly positive on the company’s content potential—based on music, motion picture and especially gaming. The combination of Sony’s Play Station platform, 47.4 million game-network subscribers and the capability to develop popular entertainment content should boost long term sales growth, in my opinion. To support growth, from 2022 through 2024, Sony plans to invest approximately $18.39 billion in the areas of IP/DTC.

Strong Financials

But investors should not build Sony’s thesis on any perceived speculation surrounding the metaverse. Sony is already a strong business with attractive business scale and profitability. For the trailing 12 months, Sony generated $88.4 billion of revenues and achieved a net-income of $7.85 billion, or $6.27/share. Cash from operations was $10.99 billion. The company’s balance sheet is strong and should provide both M&A optionality as well as shareholder distributions. As of Q1 2022, Sony recorded cash and short-term investments of $19.83 billion and total debt of $27.57 billion. Going forward, Sony is expected to increase both top-line and bottom-line. According to analyst consensus, available on the Bloomberg Terminal as of July 5th, revenues for 2022, 2023 and 2024 are expected at $80.87, $87.44 billion, and $96.08 billion, implying a 2-year CAGR of approximately 10%. Respectively, EPS are estimated at $5.41, $5.80, and $6.65.

Residual Earnings Valuation

So, if analyst consensus is right about Sony’s business forecast, what could be a fair per-share value for the company’s stock? To answer the question, I have constructed a Residual Earnings framework and anchor on the following assumptions:

- To forecast EPS, I anchor on consensus analyst forecast as available on the Bloomberg Terminal ’till 2025. In my opinion, any estimate beyond 2025 is too speculative to include in a valuation framework. But for 2-3 years, analyst consensus is usually quite precise.

- To estimate the cost of capital, I use the WACC framework. I model a three-year regression against the S&P 500 to find the stock’s beta. For the risk-free rate, I used the U.S. 10-year treasury yield as of July 05, 2022. My calculation indicates a fair WACC of 9%.

- To derive Sony’s tax rate, I extrapolate the 3-year average effective tax-rate from 2019, 2020 and 2021.

- For the terminal growth rate, I apply expected nominal GDP growth plus one percentage point to a favorable growth outlook.

- I do not model any share-buyback-further supporting a conservative valuation.

Based on the above assumptions, my calculation returns a base-case target price for Sony of $116.67/share, implying material upside of about 40%.

Analyst Consensus EPS; Author’s Calculations

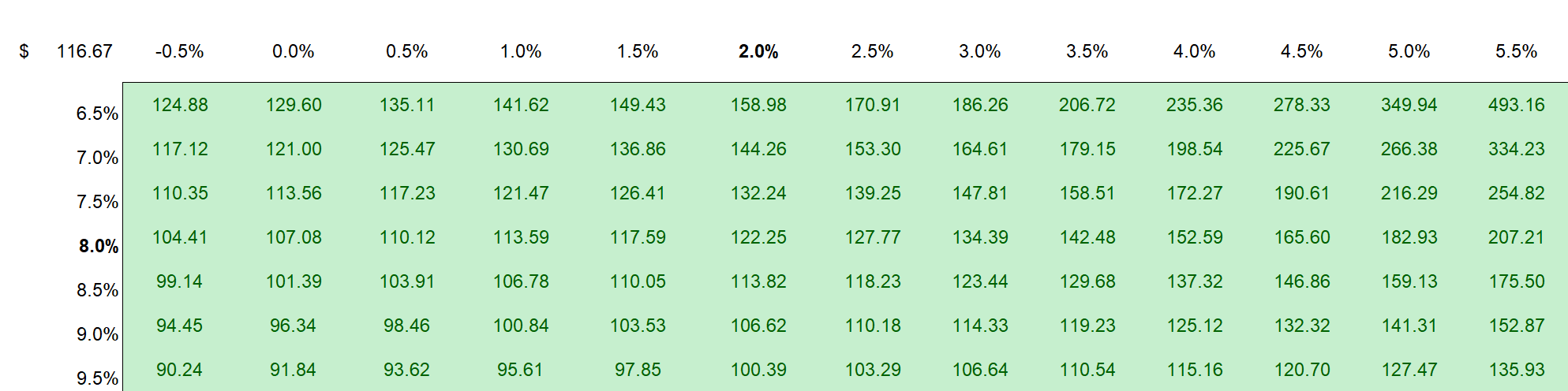

I understand that investors might have different assumptions with regard to Sony’s required return and terminal business growth. Thus, I also enclose a sensitivity table to test varying assumptions. For reference, red-cells imply an overvaluation as compared to the current market price, and green-cells imply an undervaluation. The risk/reward looks highly favorable to me. In fact, all tested combinations imply upside!

Analyst Consensus EPS; Author’s Calculations

Risks

I think Sony is relatively low-risk at current valuation levels. However, investors should monitor the following headwinds that could cause Sony stock to materially differ from my target price: 1) slowing consumer confidence due to inflation outpacing wage growth and rising interest rates could cause a temporary slowdown in Sony’s sales number of discretionary consumer products; 2) loss of competitive advantage in various business segments such as PC and smartphones given accelerating industry competition; 3) higher than expected R&D investments in order to realize new product initiatives and/or to defend competitive positioning; 4) macroeconomic uncertainty relating to the monetary policy actions; 5) That said, much of Sony’s share price volatility is currently driven by investor sentiment towards risk and growth assets. Thus, investors should expect price volatility even though Sony’s business outlook remains unchanged.

Conclusion

In my opinion, Sony stock offers a buying opportunity. I like the company’s slightly underappreciated exposure to the metaverse revolution. In addition, I see upside potential based on fundamentals. Anchored on a residual earnings framework based on analyst consensus EPS, I calculate a fair implied share-price of $116.67/share – implying approximately 40% upside.

Be the first to comment