SweetBunFactory

Sifting through the markets for opportunities in the micro-cap space is an arduous task filled with false promise, little information and red herrings. While this process is certainly frustrating, it can also be quite rewarding when you finally find an interesting prospect to dig into.

Today, I will be exploring a small company in the Ultrasonic Coatings market out of Milton, New York named Sono-Tek (NASDAQ:SOTK). I would like to discuss why I believe this company deserves a deeper dive.

Company Overview

Sono-Tek can trace its roots back 48 years to the energy crisis of the 1970’s and was built out of the desire by founder Dr. Harvey L. Berger to develop a technique to conserve oil by way of a more efficient spraying process. While the energy markets eventually stabilized, during the development of his solution, the ultrasonic spray nozzle, Dr. Berger noted dramatic benefits for this new technology in the coating of medical devices and printed circuit boards of the era; and with that, Sono-Tek was born.

Sono-Tek

This is a company that for most of its existence has been far ahead of its time. While the advantages of ultrasonic coatings have been known for decades, industries in years past had been reluctant to re-tool their manufacturing process given that standard practices had served them well.

In my opinion, the tide has finally begun to shift firmly in the company’s direction. The major markets in which Sono-Tek operates, semiconductors, medical devices and alternative energy, each are attempting to build more complex and compact products which rely on exact specifications that become more and more difficult to achieve using legacy pressure nozzle coating solutions.

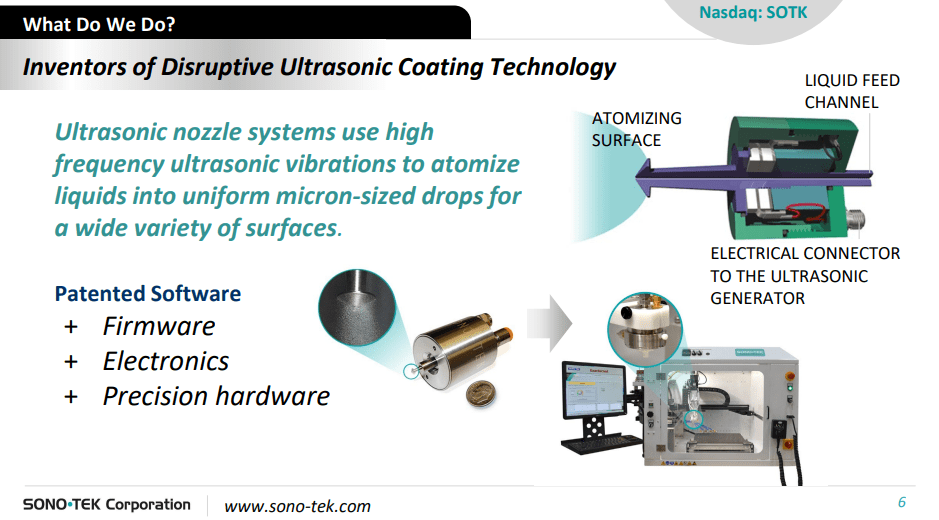

Sono-Tek’s ultrasonic coating method can be used to create a conformal coating on a material that is only 10 to 20 microns thick, or about 1/100th the width of a human hair. Legacy technologies and standard practices in the semiconductor field use between 1 to 5 mils (25 to 127 microns).

Sono-Tek

In addition to the obvious benefit of a more uniform and accurate coating, Sono-Tek’s system is dramatically more efficient and reduces material consumption by 80%. The nozzle itself, by way of its design, is also inherently non-clogging, thus dramatically reducing maintenance and machine down time. The system also allows for minute changes in droplet size, which is ideal for medical device manufacturers.

In the alternative energy market, precision and efficiency are highly prized both in the solar cell manufacturing market and even more so in the fuel cell and the emerging green hydrogen market. Below is a customer testimonial on Sono-Tek by a manufacturer of hydrogen fuel cells:

The purchase of the SonoTek ExactaCoat and AccuMist Ultrasonic Nozzle has had a very important impact on membrane electrode assembly (MEA) fabrication procedures at PaxiTech. The ExactaCoat and AccuMist Ultrasonic Nozzle allowed us to increase our production capacity considerably and will also assist us in our technical preparation for a completely industrial automated MEA fabrication process… The change to SonoTek has improved MEA fabrication efficiency, productivity, precision and reliability without any loss in fuel cell performances. PaxiTech SAS – Grenoble, France

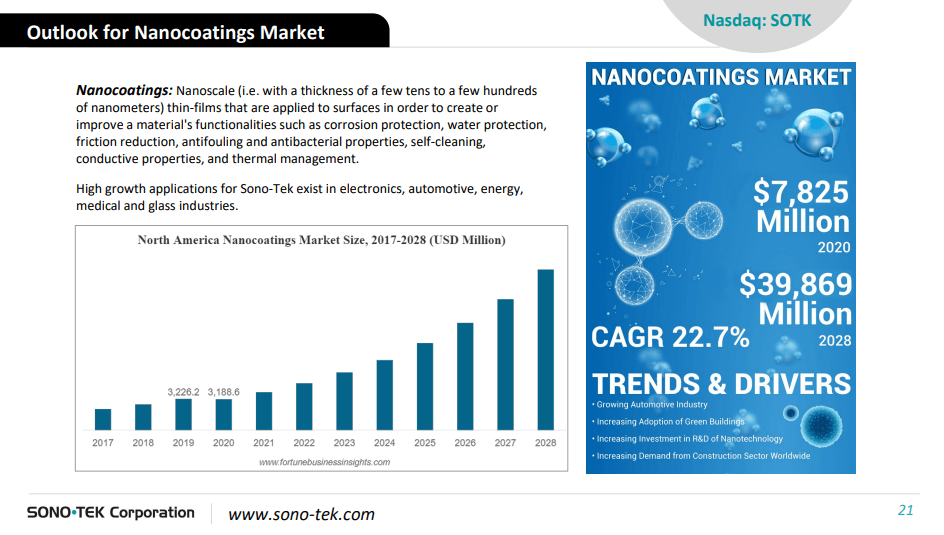

The overall market in which Sono-Tek operates is the nanocoating market. This market is primed to explode over the next decade given the rapid rise in applications and technologies that stand to benefit from, or in some cases, require this technology.

The hundreds of billions flowing into the semiconductor and alternative energy space from governments around the globe is likely to provide a gale-force tailwind to the sector given the blistering pace that new manufacturing facilities are to be built.

Sono-Tek

To be clear, Sono-Tek’s addressable portion of this market is certainly nowhere close to 100%, in fact, I believe it may be closer to only 5%, however, the markets in which they specialize such as medical devices, semiconductors and alternative energy appear to be headed directly up and to the right for the foreseeable future.

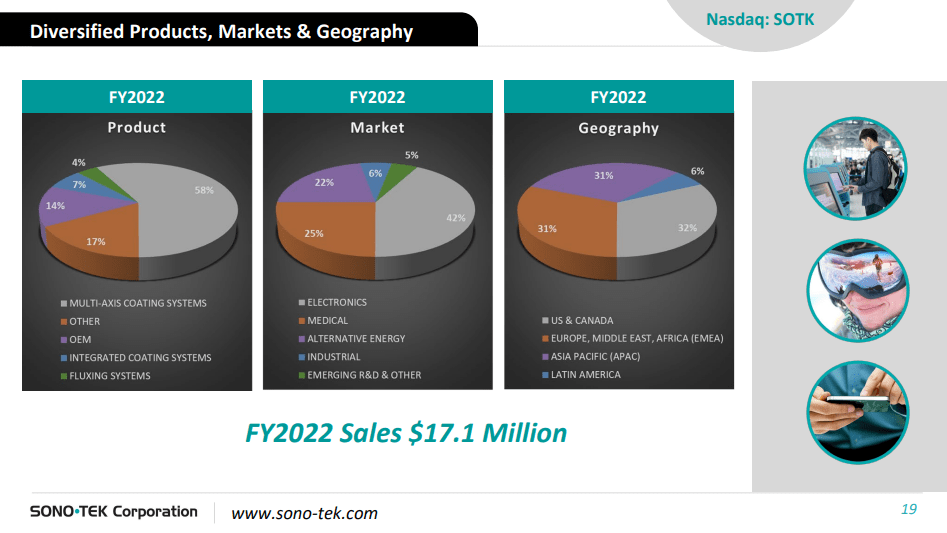

The company itself is surprisingly diversified for such a small operation, both in product areas and in geographical distribution.

Sono-Tek

I would like to point out that unlike many other smaller tech focused company’s, Sono-Tek does not appear to be overly reliant on China for sales or growth as only 31% of sales come from the APAC region which includes Japan and South Korea. The company clearly has the attention of customers around the globe.

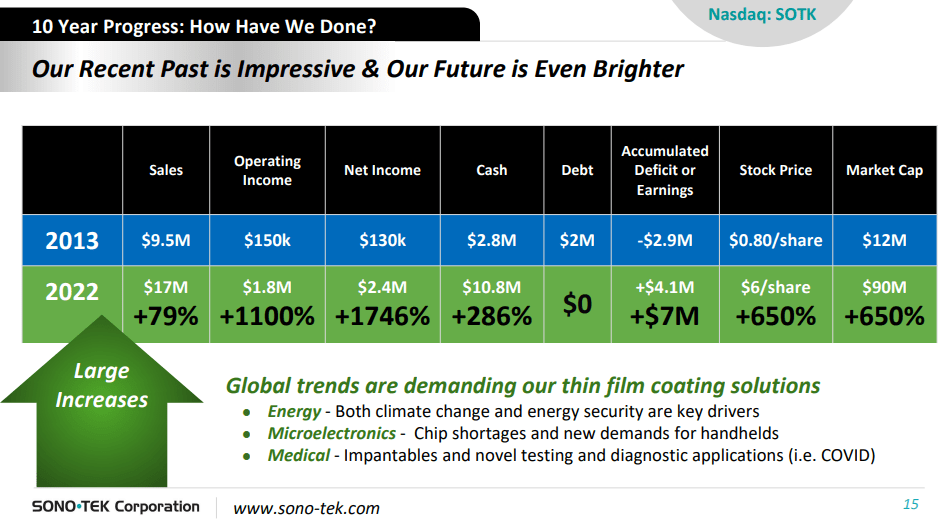

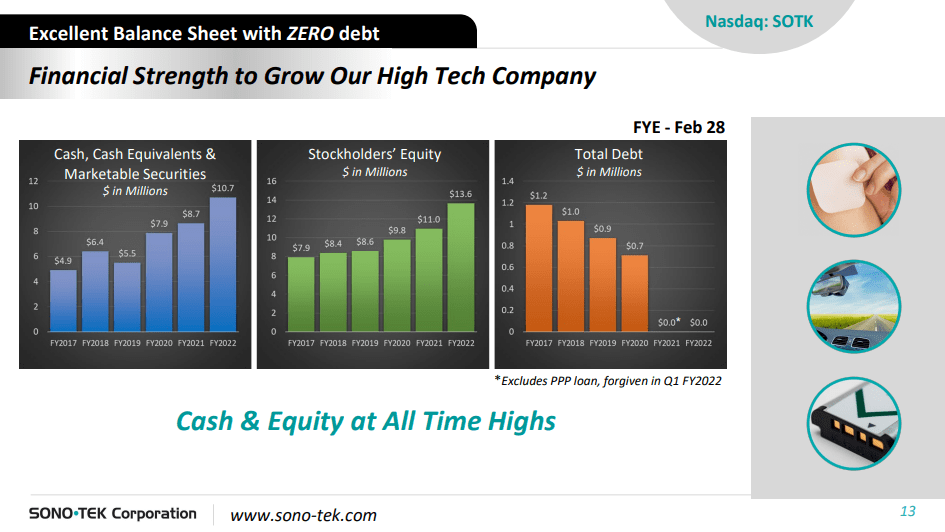

What I appreciate most about the company is that it has proven throughout its existence to be a responsible and fiscally conservative company. Over the last decade, the company has grown consistently, all while staying cash flow positive and reducing and eventually paying off its debts.

Sono-Tek

To me, this is the hallmark of a disciplined management team dedicated to building long-term shareholder value. This is not a trait that is frequently associated with smaller company’s which tend to have more of a undisciplined “family run” business environment.

In addition, Sono-Tek does not appear to be highly promotional regarding its stock price. Certainly, management is proud of their achievements, but I see a pragmatism regarding targets they set and expectations that they hope to achieve.

Sono-Tek

The company is clearly in an advantageous position regarding its balance sheet as they have $11 million in cash and zero debt. This pristine position will allow the company to look at potential bolt on acquisitions to improve its position in the market even further.

Hedge funds do play a large part in Sono-Tek’s ownership structure with Emancipation Management, run by Charles Frumberg, currently owning over 42% of the common shares outstanding. Company management is also highly invested as well and owns 7% of the company between them.

Valuation

This is the part of the article where things get a bit tough for the company. Sono-Tek, for all of its positive traits, is certainly not a cheap stock. The company, in fiscal 2022, reported revenues of only $17.13 million and earned a total of $0.16 per share giving the company a PE ratio of roughly 37 based on the most recent closing price of $5.88, quite a rich valuation in the current market.

In addition, the company has been facing extreme supply chain difficulties so far in fiscal 2023, leading orders to be pushed out, potentially into next year. It is clear that valuation metrics at the company will likely get worse, before they get better as in fiscal 2023, the company is highly likely to see a reduction in both sales and earnings per share.

Analyst estimates for a company such as Sono-Tek are pretty close to meaningless, given the drastic changes in business that can occur from single orders off of such a small base of revenues. In addition, it appears that only a single analyst covers the stock from Wall Street firms.

The company, during recent earnings calls, has pointed to 2024 as a potential record year for revenues as it anticipates shipping production level equipment to alternative energy customers and is in receipt of multiple million-dollar-plus orders, with the prospect of more to come. It is a fool’s errand to predict future valuations for this company, however, I think it is clear that results during fiscal year 2023 will be difficult.

Risks

This is a micro-cap stock and as such, to even consider investing in the company, appropriate risk tolerance is needed. Considering the industry in which they operate and the growth prospects foreseen, it is highly likely that competing technologies will be offered in time, perhaps by much larger and better capitalized companies.

In depth information on a company of this size is quite limited, leading to a reliance on company provided disclosures and SEC filings, this makes independent verification quite difficult. In addition, given the small size and limited financial resources at the company, any financial misstep or failed acquisition could severely hamper the company and its prospects going forward.

It is also clear that the supply chain of specialized chips and technical parts for the manufacturing of the company’s products is complex and is vulnerable to disruption, creating risks of continued supply chain pressure leading to delayed or cancelled sales.

While it appears that the market for ultrasonic coatings is broadening and that product specifications may require more efficient methods of conformal coating, customers may decide to continue using legacy technology to avoid disruptions caused by re-tooling in place manufacturing techniques. Also, newer applications such as green hydrogen, fuel cells and green natural gas may never develop.

Liquidity in shares of Sono-Tek is miniscule, with share volumes averaging an anemic 4,032 shares traded per day over the past 3 months. This can lead to rapid share price movements, both up and down, from extremely small trades. In addition, building, or disposing of a position of any substance in the company may take extreme patience as the bid / ask spread varies wildly.

If you choose to invest in Sono-Tek, please perform your own thorough due diligence and seek the advice of your licensed financial advisor.

Bottom Line

Sono-Tek is a fascinating company with a plethora of growth opportunities that appear to be coming into focus. With hundreds of billions of dollars set to be poured into both semiconductors and alternative energy around the globe, it is hard to imagine that the company will not be a significant beneficiary.

I am drawn to the company due to its conservative financial profile, manufacturing facilities located in the USA, the lack of notable dilution at the company and a demonstrated history of profitable and responsible operations, tempered by the potential for a tough 2023 due to supply chain issues along with the high current valuation metrics.

I can clearly see a significant growth trajectory for this company into the future and the world looks to be finally catching up to the technology the company offers and as such, I have decided to take a small, speculative position at current levels and will look to expand this initial position meaningfully upon news of the supply chain issues abating along with further developing my comfort with the company.

Let me know your thoughts in the comment section below and I highly welcome comments from those with further knowledge or experience directly with the company. Thank you for reading and good luck to all!

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment