BeyondImages/iStock via Getty Images

SolarEdge (NASDAQ:SEDG) continues to ride the generational shift to green energy with the company reporting dual beats for its fiscal 2022 fourth quarter earnings. Revenue grew by 61.74% year-over-year on the back of growing demand for solar inverters for the fast-growing rollout of solar photovoltaic across the US and the world. The company also has a smaller and growing business selling EV chargers, battery energy storage, and energy generation monitoring software to households and commercial customers. I’m bullish on the great forward march of solar PV as green energy more broadly moves to occupy a vanguard position in the energy story.

Critically, the shift away from fossil fuels has become pertinent and near visceral. It’s one of the core central investment themes set to play out over the next decade as an energy crisis, Russia’s war in Ukraine, and recent aggressive subsidies by national governments pull forward the timeline for the adoption of green energy. This will embed elevated levels of growth for relevant green energy companies as the world looks to redevelop an energy architecture that allows for greater energy security whilst driving forward a reduction in carbon emissions.

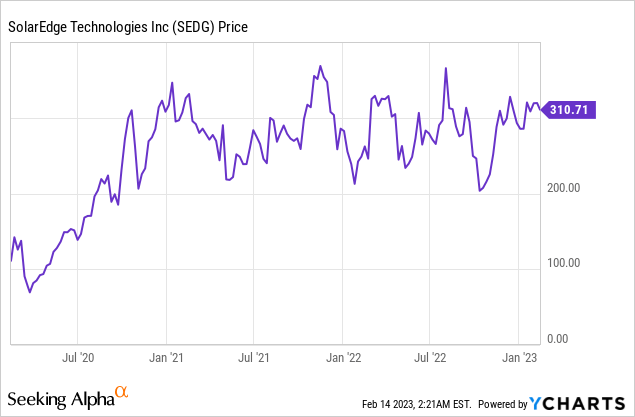

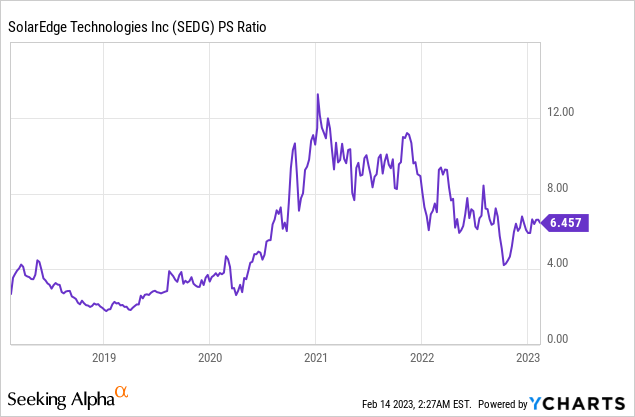

The fourth quarter results come as SolarEdge’s stock has essentially traded rangebound for the last two years as the stock market continues to adjust to dire macroeconomic news that has kept the valuation of high-growth firms muted even against a ramp-up of revenue and overall operating momentum. Bulls are somewhat still ahead here though as flat performance against the broader decimation of growth stocks has at least preserved shareholder value. It has also potentially opened up an opportunity with SolarEdge trading at its lowest revenue multiple since 2020.

Fiscal 2022 Fourth Quarter Revenue Outperforms Expectations

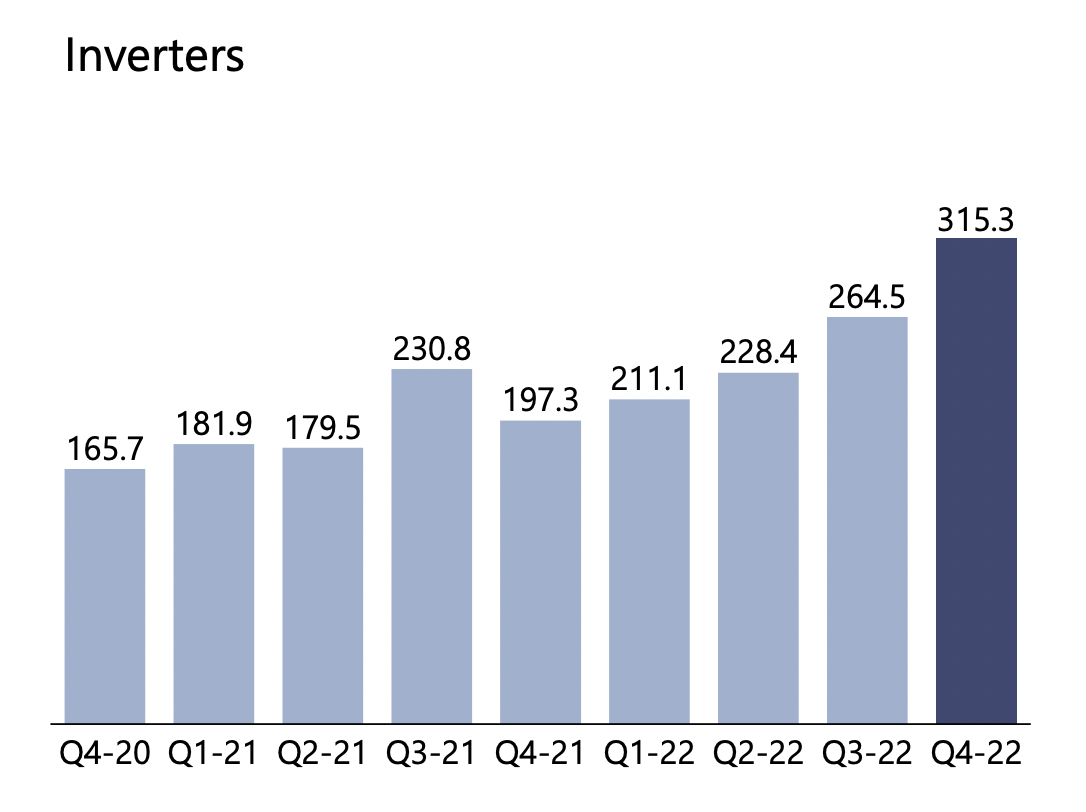

SolarEdge reported revenue of $890.7 million, up 61.4% from the year-ago period and a beat by $11.64 million on consensus estimates. The solar PV business brought in record revenue of $837.0 million with 315,300 inverters and 6.7 million power optimizers shipped during the quarter. Overall, 3.14 Gigawatts of inverters were sent to customers during the period, up from 1.9 Gigawatts in the year-ago comp. Battery energy storage saw 217.6 MWh of batteries shipped as customers continue to look to build resiliency into energy generation with onsite storage.

SolarEdge

The growth of inverters has been dramatic and sustained with SolarEdge now gearing up to grow its non-solar business as demand for decarbonization ramps up. Inverters, which change direct current electricity captured by the panels into alternating current to connect to the electricity grid and power household appliances, have been SolarEdge’s primary focus since its founding in 2006.

SolarEdge

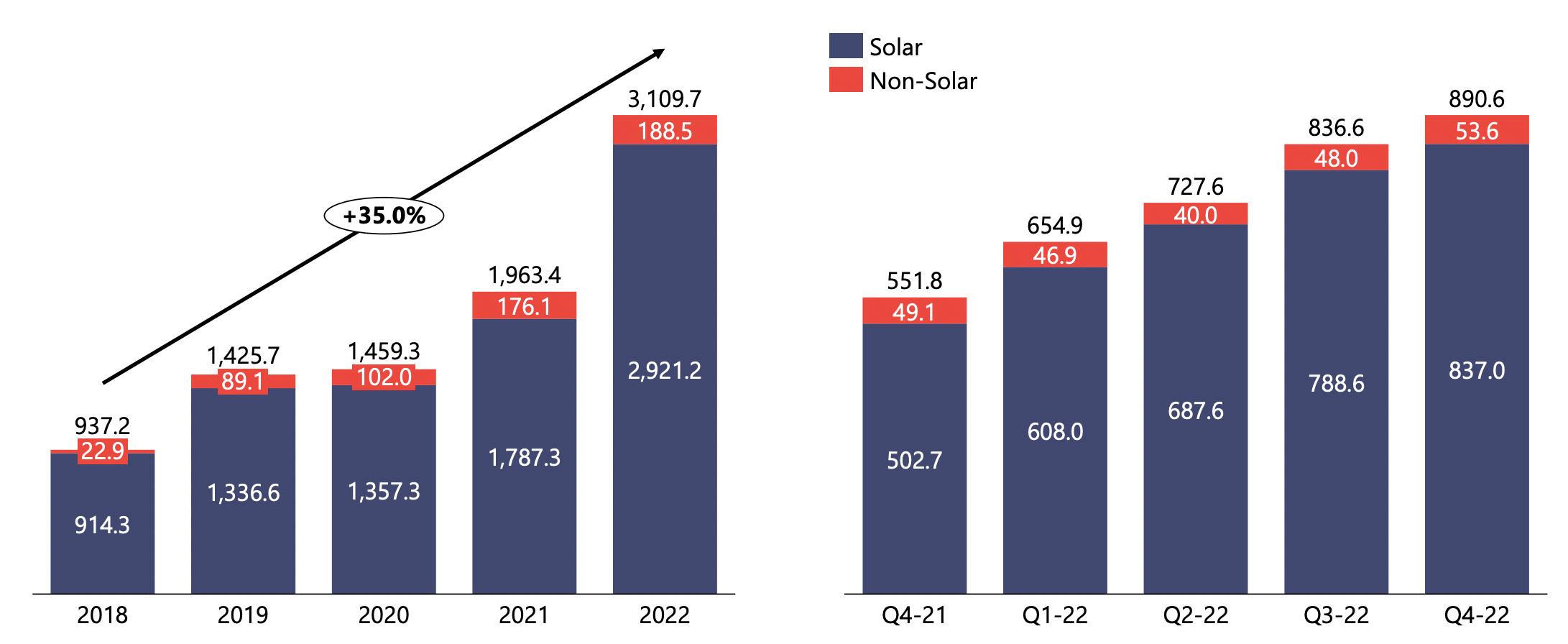

And whilst this segment will continue to grow, SolarEdge should see non-solar revenue increasingly form a larger percentage of total revenues. Management was upbeat on this during the earnings call noting a trend of increased battery attachment rates to new PV installations with their inverter systems. During the fourth quarter, 52% of the batteries attached to these installations were from SolarEdge. Hence, the company is seeing growth as more solar PV installs use its batteries and as more installs include batteries with their build-out.

The Profitable And Expanding Renewable Opportunity

Herzliya, Israel-based SolarEdge reported GAAP gross margin of 29.3%, up 20 basis points from 29.1% in the year-ago comp. This saw gross profit come in at $261 million, up from $160.49 million in the year-ago period. This drove Non-GAAP EPS of $2.86, a beat by $1.27 on consensus estimates.

Core profitability, which I define as cash flow from operations was $111.3 million, up from $89.6 million in the year-ago quarter. This boosted SolarEdge’s cash and equivalents to $783 million, up from $530 million in the year-ago period. This liquidity position now accounts for 4.6% of the company’s $16.81 billion market cap.

Strong growth is expected to continue with SolarEdge guiding for fiscal 2023 first quarter revenue to be in the range of $915 million to $945 million. This would beat consensus estimates of $914.7 million even at the low end and would mean year-over-year growth of 44.27% at the top end of the range. The company is confident that this growth will continue as electrification, decarbonization, and decentralization move to form pillars of the post-pandemic economic zeitgeist of nations now also responding to an energy crisis whilst trying to meet ambitious net-zero targets. Fundamentally, Russia’s war and US subsidies have turbocharged the green transition, likely knocking as much as ten years off its timeline.

Hence, with SolarEdge’s price-to-sales multiple at its lowest level since 2020, we could see this eventually begin to move back up once broader macroeconomic concerns around inflation and rising Fed funds rates are in the rear-view mirror. However, and the key risk to a long position, the company’s valuation is still far above its peer group average with its PS multiple 105.62% higher than its peers. This strong valuation presents a reason for some pause especially if the macroeconomic conditions remain dire. I’m currently neutral on starting a position on the back of this.

Be the first to comment