sestovic/E+ via Getty Images

This is a Z4 Energy Research quarterly summary note. It’s written before the conference.

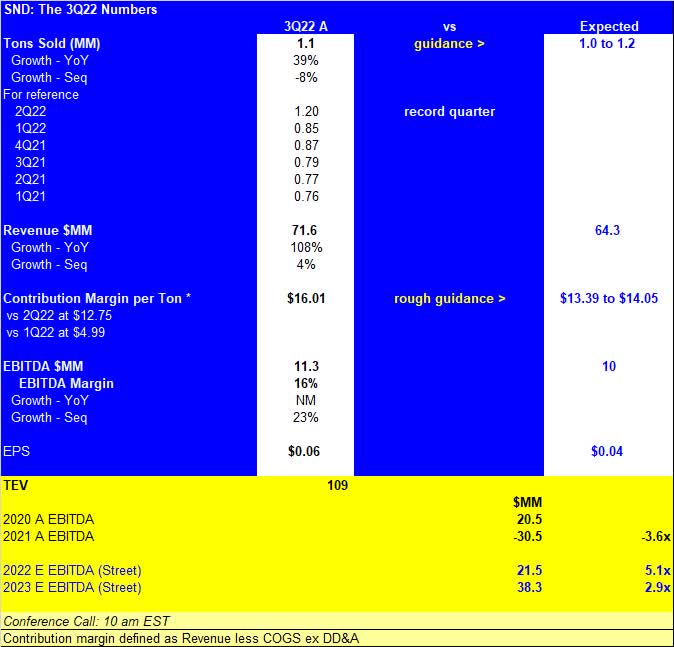

Smart Sand (NASDAQ:SND) record beats across the spectrum of headline numbers as follows.

Z4 Energy Research

Other notable financial times

Third quarter revenues were up sequentially despite the slight pullback in total sand volumes sold in the quarter on higher pricing and better equipment utilization. The sand market was tight in the quarter and remains so but as noted on the second quarter call, management guided volumes down for 3Q due to customer timing issues and volumes ended up in the middle of that guidance range. Note they returned to recording short fall revenue of $2.7 mm in the quarter (4% of total) vs $0 in 2Q22 and $2.7 mm in 3Q21. These payments reflect customer take or pay contract obligations.

Also this quarter, higher revenues and better margins helped yield a return to positive free cash flow of $6.4 mm vs -$3.7 mm in the prior quarter. One of the complaints we heard from investors after the 2Q call “if not now, when?” with regard to FCF generation. This is good to see and we’d like to see more of it in 2023.

Favorite Quotes Watch:

Smart Sand delivered solid operating and financial results in the third quarter. Activity levels continued to be strong at our Oakdale and Utica facilities and we increased the utilization of our SmartSystems last mile fleets during the quarter. Additionally, Smart Sand generated positive Free Cash Flow in the quarter as we continue to execute our plan to increase margins while efficiently managing our costs and capital expenditures. The outlook for completions activity in North America continues to be positive and we expect demand for our products and services to continue to be strong. ~ Charles Young, Smart Sand Chief Executive Officer.

Guidance: Smart Sand has not of late been big on providing spoon fed guidance in print but they generally guide to volumes for the next quarter during the conference call. They have not, again of late, provided revenue or EBITDA ranges with their volume color. We think it’s time. Our view has been that ranges for lightly covered names are helpful in dampening quarterly volatility as consensus gravitates to the middle of said range in most cases anyway, helping to control outlier analysts from creating misses. Moving on, in the 10Q published overnight we did note reaffirmation of prior 2022 capex guidance as of range $20 to $25 mm (including the purchase of the Blair, WI mine and facilities for $6.5 mm earlier this year). We’d like to get a sense from management of inflation for 2023 as well as a rough breakout of growth vs maintenance.

Highlights:

- Two Mines Active. Smart Sand has two operating mines with a combined capacity of 7.1 MM tons per year which could produce nearly 1.8 MM tons in a perfect quarter. The second quarter’s 1.2 mm tons was a record with 3Q22 just shy of that level and we understand the mines often produce more in the middle quarters each year as operating costs are lower in the non winter months. We’d like to hear more about how they can push utilization higher for these two mines and what gating factors such as transportation (especially trains), labor, and energy costs might be currently barring them from getting close to nameplate.

- One Mine Shuttered. The 7.1 MM TPY capacity figure excludes SND’s Blair, WI mine. Blair has a capacity of 2.9 MM TPY of 40/70 northern white sand. 40/70 is in high demand but the mine has remained shuttered since they bought it last March. We would like additional color as to what conditions would prompt a Blair restart and what factors might prevent such a restart. Are short term contract prices high enough relative to costs to re-open the mine and processing facility now? What kind of incremental capital cost would this entail and are there any long lead time parts that would need to be ordered? Could the company staff it given a quarter or two of notice? Alternatively, our sense has been that some of the equipment there could be reallocated to their other mines to expand those mines’ capacity. In short, we’d like to better understand the current options for Blair.

- Lastly, while on the topic of better understanding we note that some of their sand peers often speak in terms of physical last mile infrastructure. For our own edification and modeling, we’d like a better window into any plans to grow the fleet of SmartSystems (SmartDepot (well site storage) and SmartPath (transloader systems)) as it pertains to winning customer orders.

- Balance Sheet: Cash increased by $8.1 mm in the quarter to $10.4 mm and on a net debt to annualized 3Q22 basis they’re at just 0.1x.

Nutshell: The quarter was strong across the board. Likewise, our checks with other players and with the myriad upstream segment calls we’ve been on this year and this quarter in particular point to continuing tight frac and tight sand conditions. Customers want to know they can get sand. One larger sand player has noted the US sand market could grow by 10 MM TPY next year and this would be readily absorbed by the small frac segment expansion expected for 2023. So that seems like there’s maybe an opportunity for Blair or at least for upping utilization at their two currently active mines.

So, with the results strong and the outlook for sand being strong, the tone of the guidance on the call is fairly key for this small cap player. We note there are only 2 sell-side analysts in print here (there’s a third quality name involved as well but they don’t submit numbers to our knowledge). The first, Stifel, has a Hold on the shares and I used to work at the same firm at the same time as the analyst and people saw him as smart so that’s a positive. He was the only guy on the call last quarter. Perhaps more interesting now is that Piper initiated coverage as a Hold in October which means they worked up their initiation piece on the name and wanted to be in print in front of this quarterly report. These results and any incrementally positive guidance on the call could prompt them to upgrade. Given the lack of broader coverage, the reaction to today’s report and conference call color could be delayed, this is not as high priority a name as bigger Oil Service names and may not be squawk box worthy pre call this morning at either shop. We would however expect some volatility around their prepared remarks on 4Q volumes and contribution margins, and any plans they disclose to potential de-shutter capacity. Lastly, we note SND trades at just 2.9x 2023 Estimate Street EBITDA which we see as low given the solid balance sheet, the rising net pricing environment for sand, and concurrently improving margins. In this kind of strong macro backdrop market, that low ball multiple speaks to a name that needs more exposure. We’ve owned a Trading Only position in SND for the last few quarters.

Be the first to comment