StockByM

SL Green (NYSE:SLG) has been criticized for raising the monthly distribution and then coming out with fiscal year 2023 guidance that then cut the monthly distribution. The new rate amounts to $3.25 annually for the next fiscal year. Back in December 2021, management had increased the monthly distribution to an annual rate of $3.75.

There had been a hope that the base dividend rate would be something that the company could maintain. But rising interest rates have put a stop to those hopes. This has unsettled some investors who have felt that management should have foreseen the situation before they raised the base dividend in the first place. But then again hindsight is always 20/20.

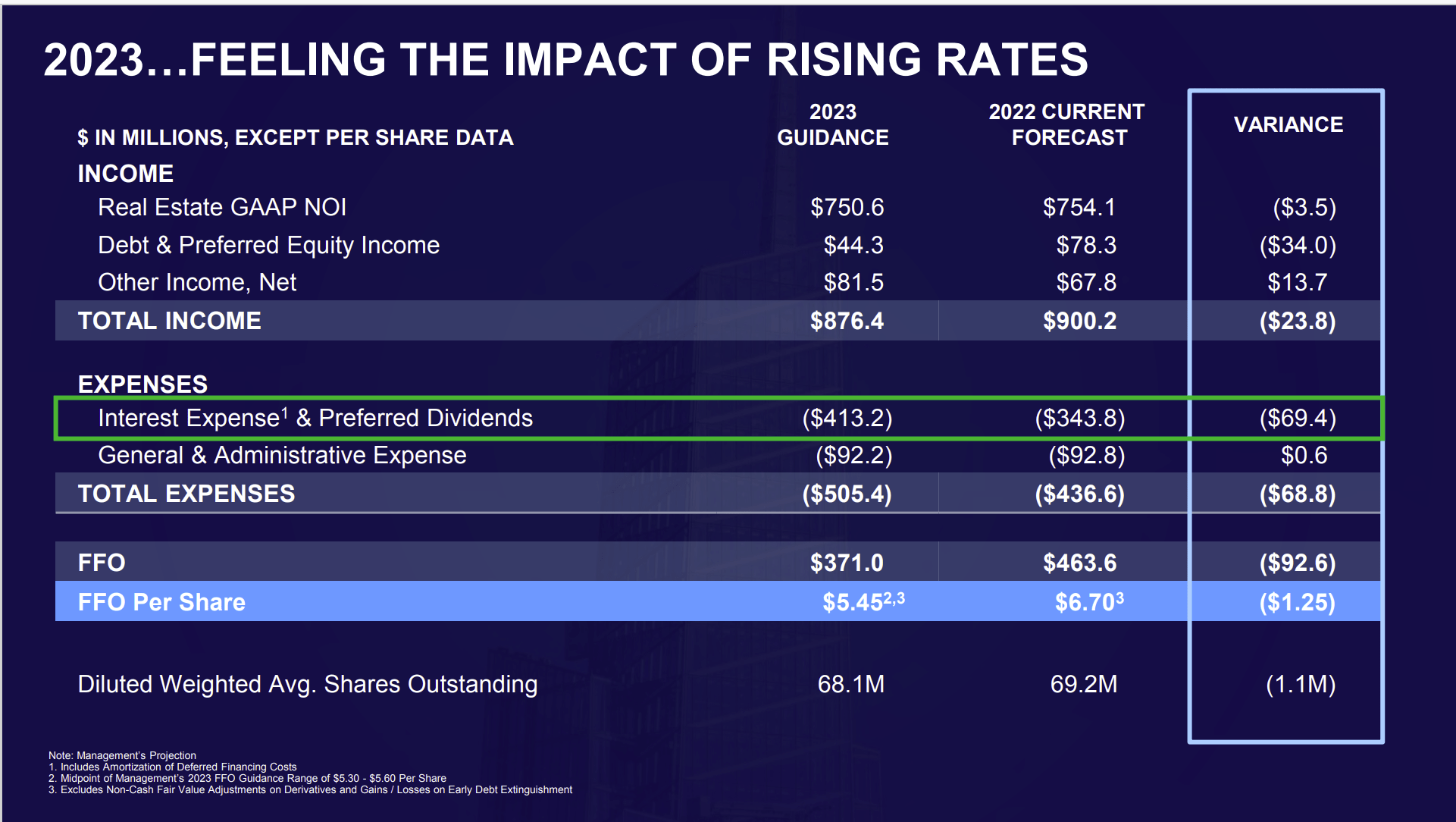

SL Green 2023 FFO Guidance Presentation To Investors (SL Green December 2022, Institutional Investor Presentation)

What has changed since that original distribution raise has been the outlook for interest rates. Management notes in the same presentation that they have hedges to protect the floating rate debt. However, it took some time for the outlook to change for that strategy of hedging to become apparent.

The result is shown above. Income declines a little bit, but interest expense “goes through the roof”. Management was recovering from the effects of fiscal year 2020. Increasing occupancy appears to be still a reasonable goal. However, right now interest rates are increasing the fastest and will have the most impact on FFO shown above. Therefore, management is doing the prudent thing and adjusting returns to shareholders.

Note that this management had found a way in the REIT structure to declare a stock dividend and then a reverse split right after to hang onto some cash flow. That already gives this REIT some stability that other REITs do not have.

REITs by nature are a variable distribution entity. They distribute profits and those profits will vary according to the economic situation. SL Green had a decent fiscal year 2020 because interest rates remained low while the value of real estate climbed. Since the company has essentially two major sources of cash (rent and sales at a profit), fiscal year 2020 turned out to be rather reasonable.

But rising interest rates are another matter entirely. The effect is shown above in the form of a material decline in FFO. As a side note, there is considerable confusion over FFO and FCF. Management has a lot of options to decide FCF. Management can decide to do the minimum to generate more FCF or the company can decide to grow which reduces the FCF. This necessitates the investors looking at cash generated from all sources and deciding whether or not they agree with management about the expenditures of cash flow (from all sources including sales).

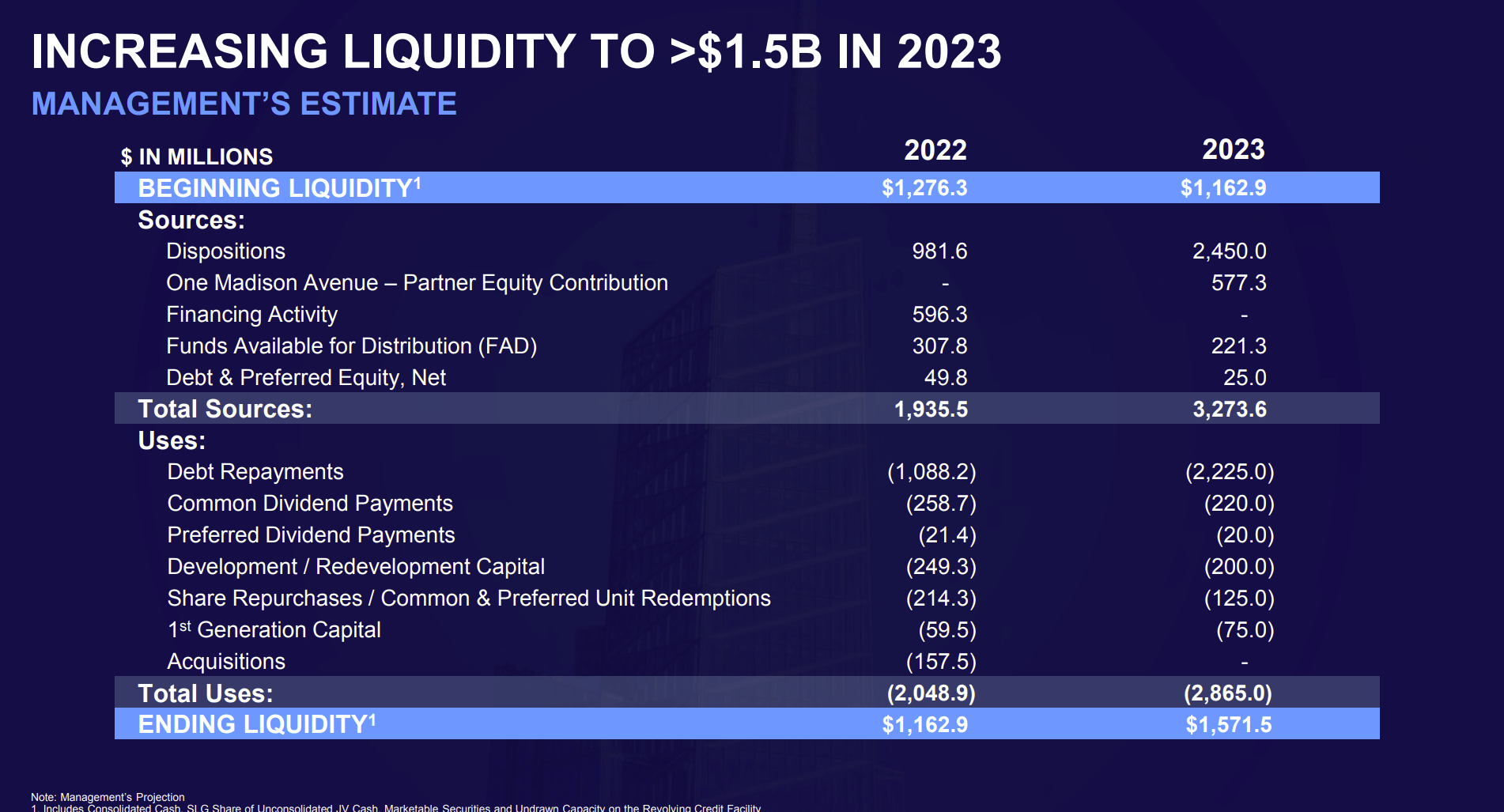

Sources And Uses Of Liquidity

Management actually has a greater source of liquidity than FFO. Even though FFO is a key measure for many investors, a lot of REITs do buying and selling that actually offers far more cash flow potential than is the case with FFO.

SL Green Sources And Uses Of Liquidity Fiscal Year 2023 (SL Green December 2022, Institutional Investor Presentation Fiscal Year 2023)

Probably the biggest risk for the coming fiscal year is the ambitious disposal of roughly $2.5 billion of real estate that is expected to generate much of the increasing liquidity above. Rising interest rates often pressure sales prices. So, if there is a shortfall or even a crunch, it is likely to come from sales that are less than expected (one way or another).

Such a shortfall could result in higher-than-expected debt payments and pressure on the monthly distribution. Management noted that common unit repurchases have been paused as the economic situation deteriorates. Up until now, management had repurchased nearly half of the outstanding shares since the program began. But downturns often put an end to such programs and this downturn appears to be no exception.

Buy Low And Sell High

One of the hardest things in the investment world to learn as an investor is to buy low when all the negatives make the headlines and sell high when all the news proclaims that higher is just around the corner.

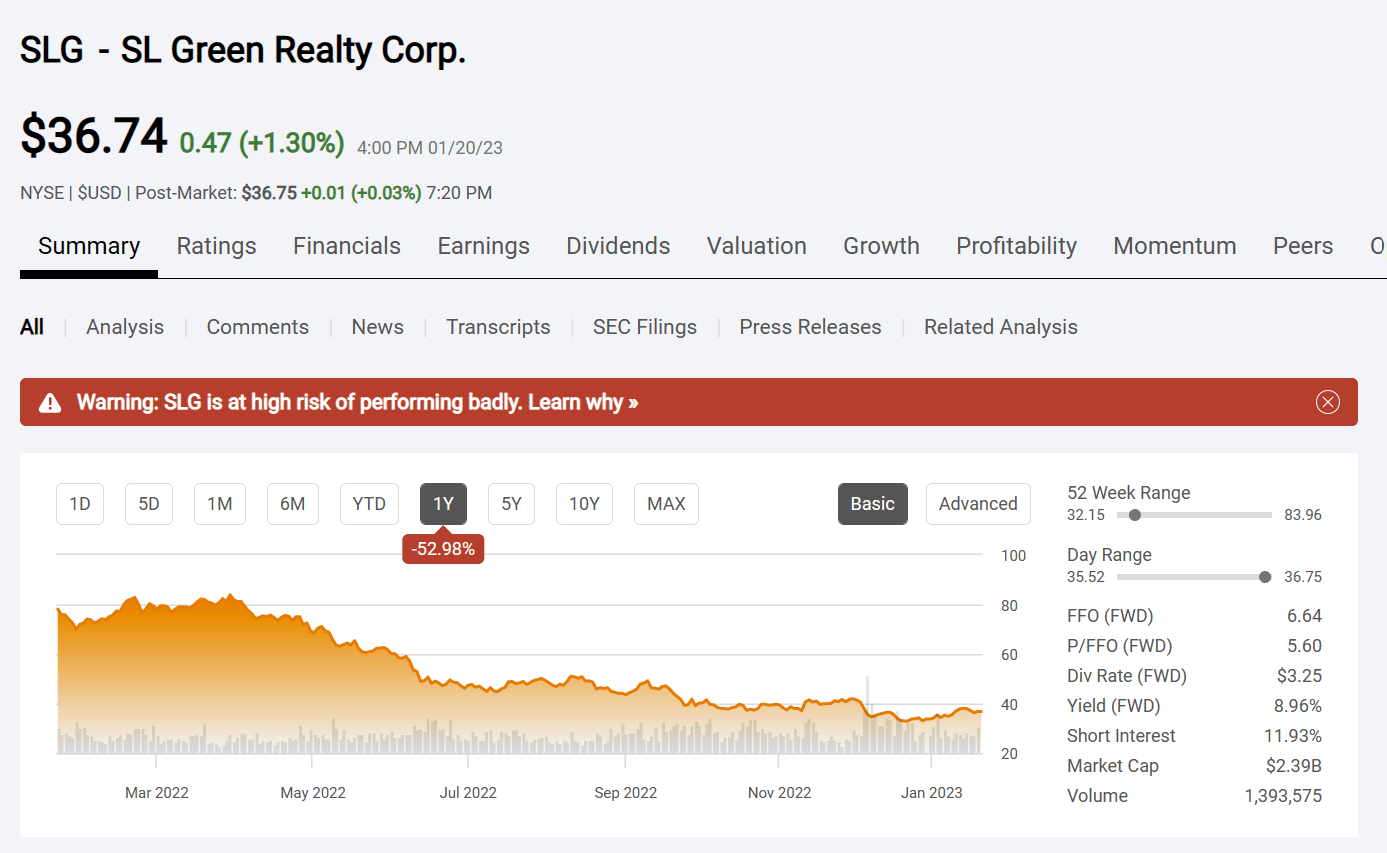

SL Green Realty Corp Common Stock Price History And Key Valuation Measures (Seeking Alpha Website January 20, 2023)

The stock has clearly responded to rising interest rates. There is a fear that interest rates will remain high for the foreseeable future. Yet much of the country’s history is that of low interest rates. The 1970s turned out to be an anomaly in our country’s history. Yet the fear of a repeat of the 1970s clearly pervades market thinking at the current time.

Even so, it appears that a lot of interest rate sensitive stocks like this one have “hit bottom”. The stock is already as low as it was in 2020. It also appears that the price is not responding to the interest rate increases (and threats of more increases) as it had back when the interest rate hikes started. Often times these stocks will bottom and begin to rally before anyone pays attention to the progress. That process could be underway as I write this.

In just about every economics textbook (Samuelson “Economics Eleventh Edition”) a tax cut paid for by debt followed by increasing deficits combined with an easy money policy is a prescription for inflation. Generally, it takes a few years for inflation to appear. Now however, the general budget deficit declined for the second year in a row and rising interest rates both combat inflation.

This is far more conservative management of the economy than was the case since really the 2016 fiscal year. That trend bodes very well for lower interest rates in the future. If that is the case, then the stock price shown above has a lot of recovery potential with very little long-term downside risk.

More importantly, the biggest part of the core CPI is housing. But the calculation for housing is a lagging calculation. Since housing costs and rent costs have been declining for more than a year, investors already know that a big chunk of the CPI will be reported as going down in the current year. That leaves the volatile energy and food groups left. The Federal Reserve will likely make sure that energy and food do not spawn add-on inflation while making sure that inflation expectations do not take permanent hold.

But those kinds of issues are generally short-term. So, the idea of long-term higher interest rates does not hold a lot of “water”. Now this is dependent upon the federal budget deficit continuing to remain low and hopefully get lower. But that does appear to be the case with the current atmosphere in Washington. The former “big spenders of 2017-2020” appear to be “on the wagon” for the time being. Meanwhile covid stimulus spending has also faded as a necessity. Therefore, the six year or so big spending period appears to be at an end.

That is very good news for a company like this one as it solidifies the contrarian case. The stock price is likely to reach its old highs and then some as management continues to embark on new profit opportunities.

Be the first to comment