jamesteohart

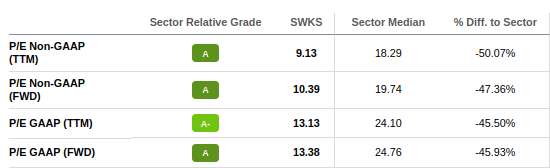

There are many reasons to like Skyworks (NASDAQ:SWKS), from the exposure it gives to 5G and IoT, to the excellent profit margins and growth it delivers. One reason that is particularly relevant right now is its valuation, which has become very attractive, especially when compared to the market in general, and its sector in particular. Trading at roughly half of its sector median, it is no surprise that Seeking Alpha gives it an excellent valuation grade.

Seeking Alpha

There are some explanations for the low valuation, one is that many investors are concerned by the significant dependence on its largest customer Apple (AAPL), worrying that one day it might switch to a different supplier, or that it might try to develop replacements itself. This is a real threat. Bloomberg, for example, reported some time ago that Apple was hiring RF engineers to develop wireless chips that could eventually replace components from companies like Skyworks and Broadcom (AVGO). While this is a real risk that should be taken seriously, we believe it would be harder than many seem to think for Apple, or other customers, to do this. For starters, they might infringe on one or more of Skyworks’ ~4,600 patents, triggering expensive litigation. They would then need to find someone to manufacture these devices for them, which isn’t as easy as it is with digital chips where they just have to call TSMC (TSM). Skyworks operates its own specialized fabs, and there are few companies with the necessary expertise to manufacture cutting-edge RF devices. As a result, it may be more cost-effective for Apple to continue to rely on established suppliers like Skyworks.

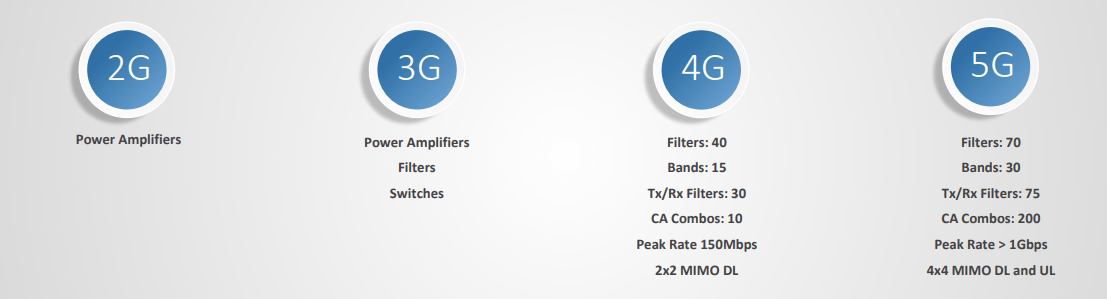

Another reason shares have been under pressure recently is that the smartphone market has been very weak. Some in the industry are saying that recovery is not likely until late 2023. While this may be true, and the smartphone market could remain weak for some time, we believe it will eventually recover and that it is less of an issue for Skyworks as it has the 5G tailwind. As smartphones transition to 5G, Skyworks has a bigger content opportunity per device, as 5G smartphones require far more RF components.

Financials

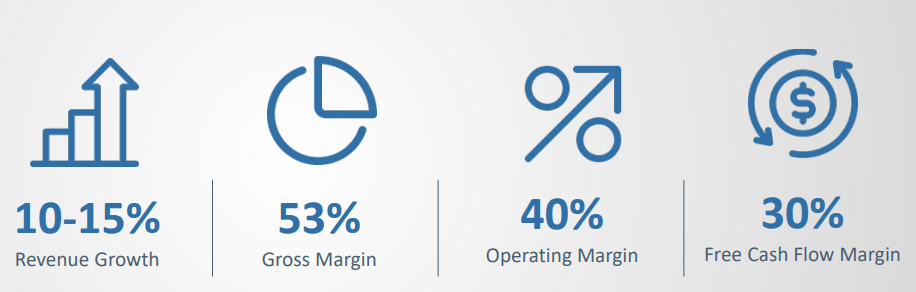

The company has terrific financials. Few companies in the world have profit margins this high. One small detail we would like to point out is that the numbers below are non-GAAP.

Skyworks Investor Presentation

GAAP gross profit margin is closer to 47% and GAAP operating margin is closer to 29%, in large part due to stock-based compensation. Still these are excellent profit margins, and show that Skyworks is a great business.

Growth from 5G

Skyworks has benefited from the growth resulting from the 5G transition. There have been increasing levels of RF complexity with each new generation, resulting in increasing content opportunities for Skyworks. The company therefore benefits from these trends every upgrade cycle, as it sells more RF components per phone.

Skyworks Investor Presentation

Diversifying Revenue

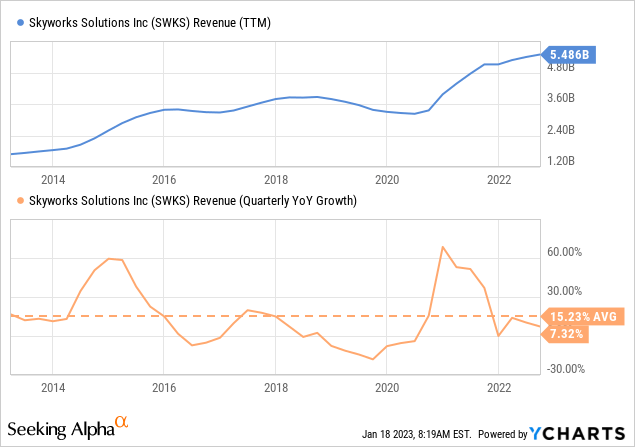

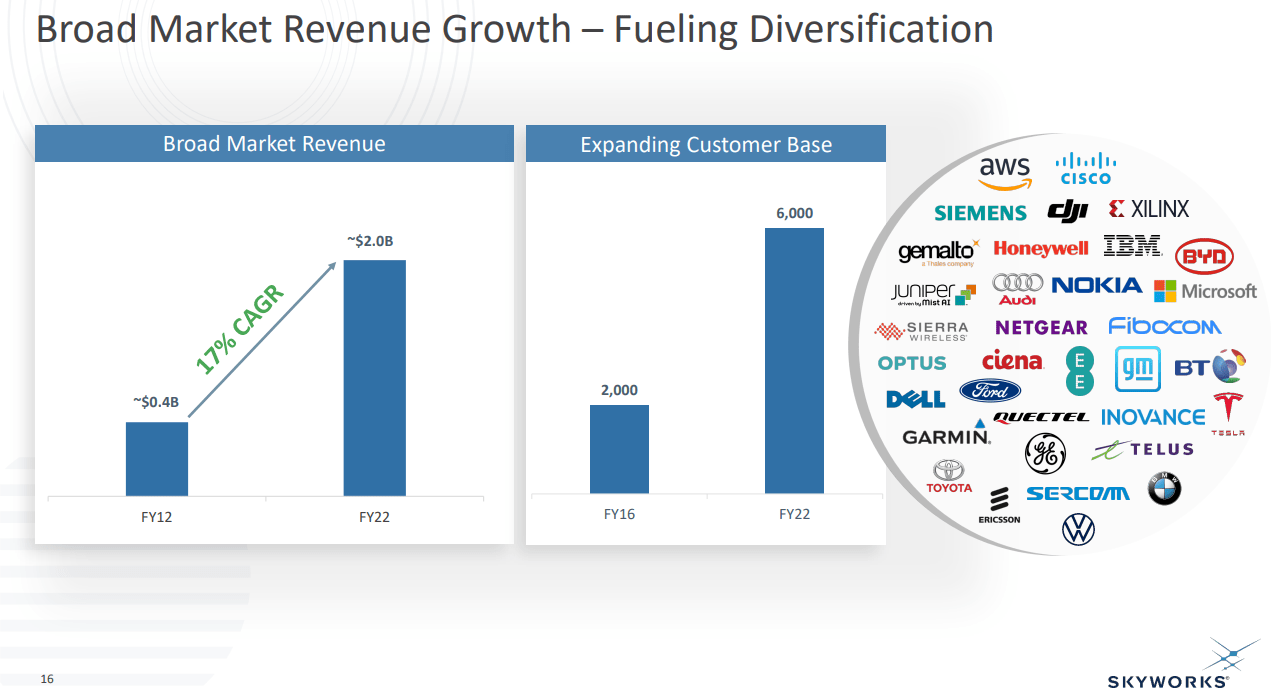

Skyworks has also been working very hard to diversify its revenue from Apple, and from smartphones in general. It has products targeting the Internet of Things, automotive and industrial applications, etc. Another area where Skyworks shines is in infrastructure. The company recently showcased their AccuTime and NetSync clock and timing portfolio. As the industry transitions to 5G core infrastructure, these solutions will become increasingly important. The need for tighter clocking solutions that are synchronized at the base station, and all the way back to the network is a greenfield opportunity for Skyworks. All these examples are part of what the company calls ‘Broad Market’ revenue, and it is now more than a third of the total, and has been growing at an impressive CAGR of ~17%.

Skyworks Investor Presentation

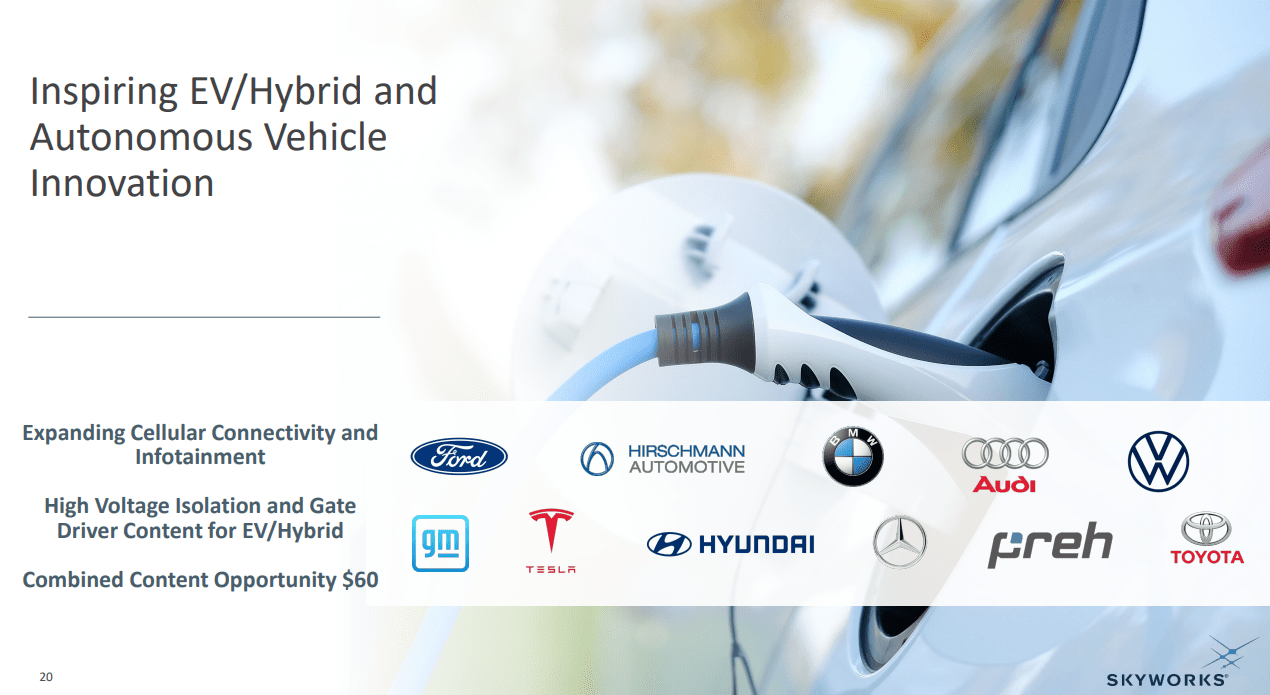

One of the most impressive new offerings from Skyworks is their automotive-grade complete RF front-end system. This system includes all the low, mid, and high bands, as well as ultrahigh bands for 5G, all supplied by vertically integrated Skyworks technology. The company also has power isolation and timing devices targeting the automotive market. With all of these combined, the company is looking at a content opportunity per vehicle of ~$60, and it already has some of the biggest car manufacturers as customers. At a recent investor conference the company said they are seeing enormous growth from what they consider the number one EV maker in the world. It sounded like they were talking about Tesla (TSLA), and importantly they mentioned that content per car is also going up:

So it’s a little bit daunting to consider how fast that business is growing really. And we’re strapped on to that number one — who I consider as the number one EV maker in the world. We’ve partnered with them early, and we’re hanging on because they’re growing quickly, not just in units but also in content. – Carlos Bori, Senior Vice President of Sales and Marketing

Skyworks Investor Presentation

Skyworks is also focused on the transition to the more advanced WiFi 6E and WiFi 7, which requires new BAW filter technology, more amplification, and low-noise amplifiers. They have a strong partnership with Broadcom and have recently announced a collaboration with them on a new product line called Sky ICE that has incredibly low power consumption.

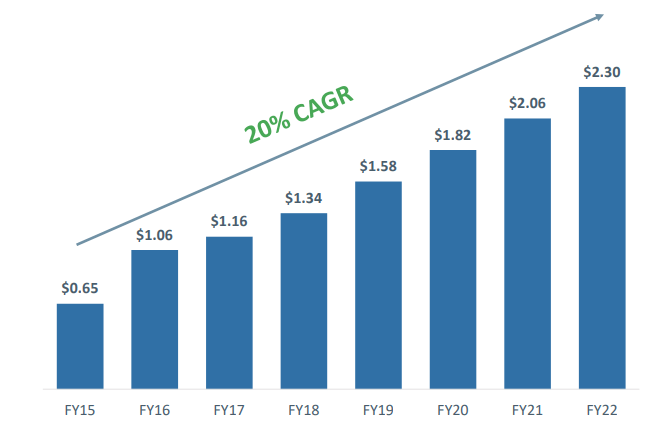

Dividend Growth

Skyworks is an excellent dividend growth investment, with 8 years of dividend increases at a ~20% CAGR. Given that the payout ratio remains modest, and the company continues growing at a good pace, we believe it is likely that the dividend will continue growing at a very good rate for several more years.

Skyworks Investor Presentation

Valuation

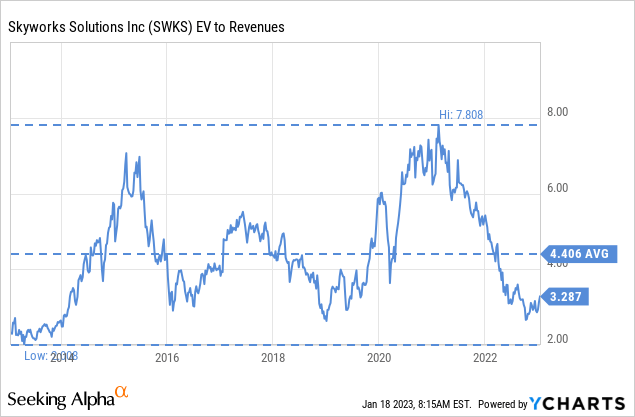

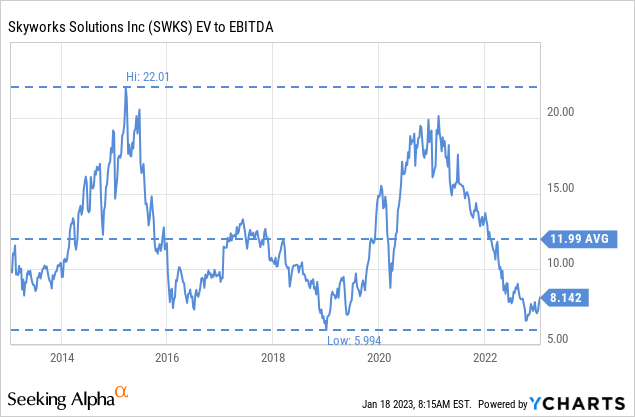

As we said at the start of the article, we like buying straw hats in the winter when they are very cheap. We believe the headwinds currently affecting the smartphone market will eventually dissipate, and Skyworks shares are likely to be re-rated higher then. In the meantime shares can be bought at close to some of the lowest valuation multiples in the past ten years. As can be seen in the graphs below, shares can currently be bought at multiples below the ten year averages of EV/Revenues and EV/EBITDA.

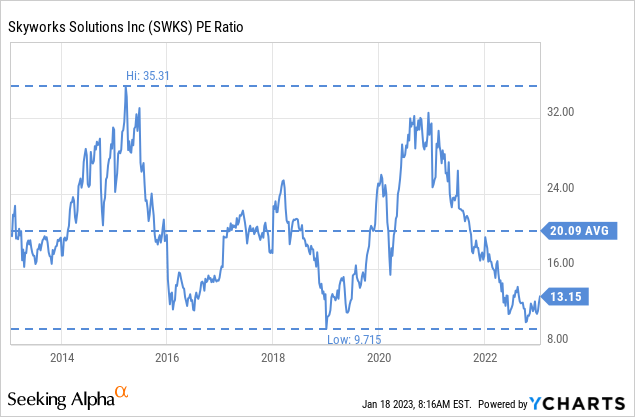

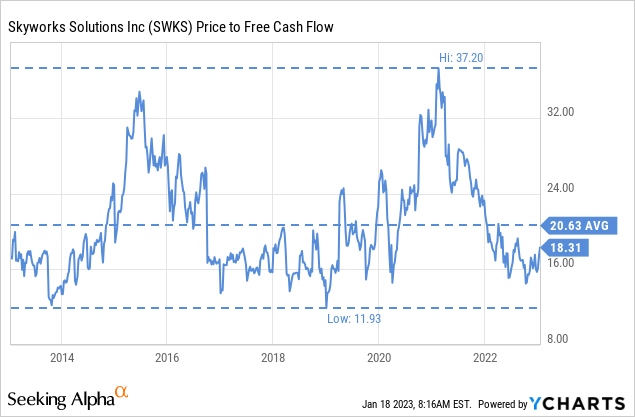

Taking P/E ratio and Price/Free Cash Flow into consideration shows the same level of undervaluation.

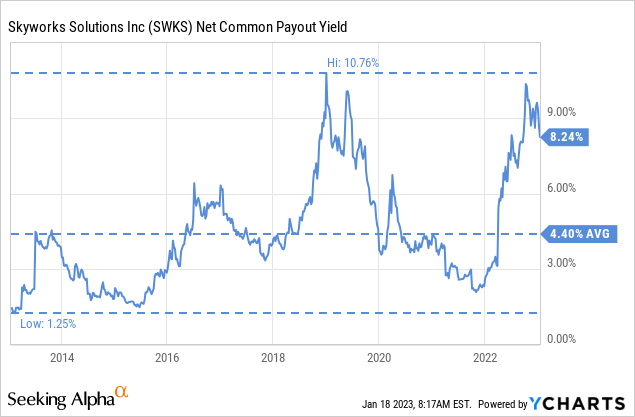

Meanwhile, shares are close to their highest net common payout yield of the last ten years. As a reminder, the net common payout yield combines the dividend yield and the buyback yield.

Risks

As we have previously mentioned, there is customer concentration risk with the company, and is probably one of the main reasons investors are not willing to pay a higher multiple. Risk is especially important as there have been rumors of its biggest customer, widely considered to be Apple, looking to develop its own RF devices.

Another thing to consider is that the majority of their revenue still comes from the mobile segment, which is expected to decline sequentially. This risk is partly mitigated by strong growth in broad market revenue, which is now more than a third of the total revenue.

Conclusion

We believe the headwinds Skyworks is currently experiencing will be temporary and will eventually dissipate. While there are some important risks to consider, shares have rarely been this cheap. As such, we believe right now is a great time to buy the shares. The company is also experiencing excellent growth in its broad market segment, with many interesting and high-growth applications. The company’s devices are now not only found in smartphones, but even in Tesla cars, wireless accessories, etc. The company has terrific financials, and a very strong IP portfolio, and has delivered good growth for many years, even if growth can be cyclical. We believe shares are currently a ‘Strong Buy’.

Be the first to comment