Maxxa_Satori

SITE Centers Corp. (NYSE:SITC) is an owner and manager of open-air shopping centers located in high income communities within suburban neighborhoods.

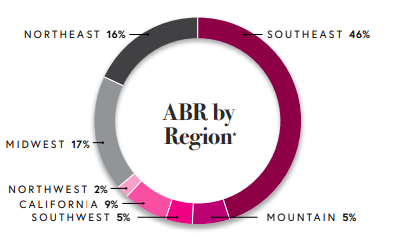

Currently, they operate 101 wholly-owned properties that are geographically diversified across the U.S., with a significantly greater concentration in the Sunbelt region of the country.

Q4FY22 Investor Supplement – Graph Of Current Geographic Operating Presence

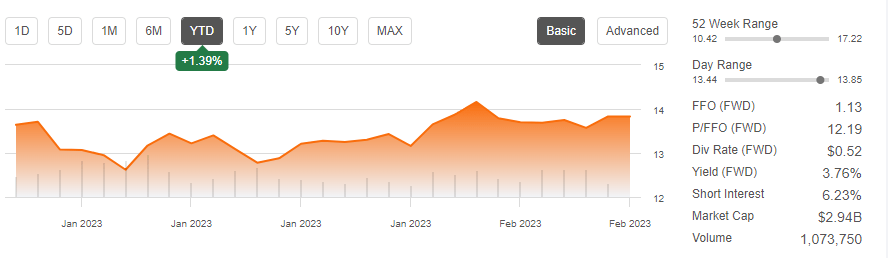

Since a prior update on the stock, shares have gained over 14.5%. This compares favorably to the S&P 500’s 7.5% gain over the same period.

YTD, however, shares are underperforming broader markets, up just over 1%. Additionally, they are down about 8% over the past year and are currently trading at about the midpoint of their 52-week range.

Seeking Alpha – Basic Trading Data Of SITC

For investors, SITC offers a safe dividend payout. While the current yield may not be attractive to most, the payout has attractive upside potential. In addition, the company maintains strong portfolio metrics, including leased occupancy rates of 95.4% and a commencement pipeline representing 5% of annualized base rents (“ABR”).

Exposure to high income households also buffets the portfolio from recession risks. The company is exposed, however, to several weaker tenants. And though they are likely to recapture space from the non-performing ones, the lag in commencements could weigh on results in the near-medium term. At current trading levels, shares appear fairly priced, given these uncertainties.

Recent Performance and Current Portfolio Metrics

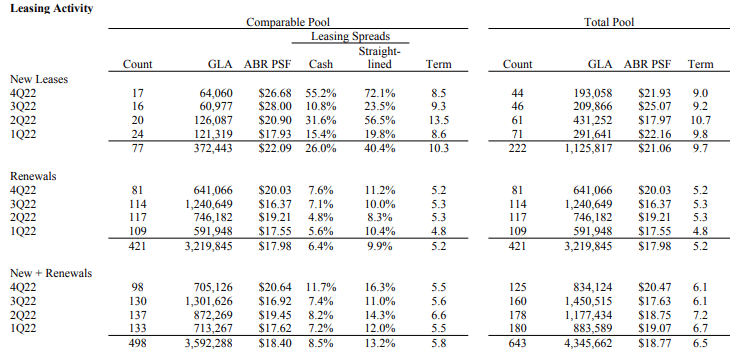

SITC turned in quarterly results in Q4 that came in ahead of internal expectations. This was driven by high leasing levels despite limited availably of space. In total, the company leased over 800K SF of space during the quarter. This includes approximately 200K SF of new signings.

While the total volume is down from prior quarters, this is mainly due to the availability of space, as the portfolio is up to a leased rate of 95.4%. That is up 380 basis points (“bps”) over the last two years.

Q4FY22 Investor Supplement – Summary Of Leasing Activity By Quarter

On a sequential basis, the leased rate is up 40bps from last quarter. More specifically, their shop lease rate was up 120bps sequentially and a whopping 530bps from the fourth quarter of last year. This stemmed in part by signings within their redevelopment pipeline.

The signings have also been completed at healthy spreads. On a trailing 12-month basis, for example, spreads on new and renewed signings were about 9%. And looking ahead, SITC has 250K SF of space in negotiation with blended spreads above their trailing 12-month average.

Within the signed but not yet commenced pipeline (“SNO”), 290K SF of new leases, representing +$6.4M of ABR, commenced in the fourth quarter. Yet, the pipeline was down just +$3M on a sequential basis due to the offsetting impact of new signings. As such, the total pipeline still represents about 5% of total ABR.

Despite the positive developments on the leasing front, management did note the return of post-holiday bankruptcy filings. Some of the more notable tenants on watch include Party City, Bed Bath & Beyond (BBBY), and Cineworld.

For Party City, SITC’s exposure include 12 wholly-owned locations, representing about 90bps of rent. On this, the company is moving aggressively to recapture the space so that they can capitalize on the robust demand environment.

With regards to BBBY, SITC’s total exposure, including JV units, is 18 stores. Through the date of their earnings release, they had already taken back one space location through natural expiration and re-leased it to Planet Fitness (PLNT) with a 2023 commencement date. Of the remaining stores, which represent 1.9% of ABR, the company expects to backfill 17 of them.

All considered, SITC expects to execute leases at most of the properties taken back, with rent commencements by year-end 2023.

Liquidity and Debt Profile

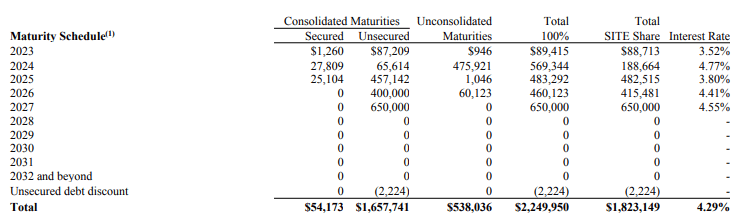

At year end, total debt levels remained within the desired targeted range. As a multiple of EBITDA, net debt stood at 5.1x. This is down from the 5.4x at the end of 2021.

And in 2023, if results came in on the low end of guidance, leverage levels would still remain below 6x. The company, therefore, has ample cushion for additional debt capacity, should they require it.

Their lower degree of debt is complemented by over +$950M of available liquidity, comprised of +$20M of cash on hand and availability on their revolving credit facility. Additionally, SITC has just +$87M in debt maturing through 2023. That is just a fraction of their total available liquidity.

Q4FY22 Investor Supplement – Debt Maturity Schedule

Furthermore, the company has only +$23M of redevelopment commitments during the upcoming year. Negligible exposure to variable rate debt also insulates them from interest rate uncertainty.

The balance sheet strength paired with a modest level of capital commitments has enabled SITC to opportunistically repurchase shares at favorable implied cap rates in relation to recent dispositions. It has also enabled them to enact gradual hikes to their recurring dividend payout.

Dividend Safety

SITC currently provides a quarterly payout of $0.13/share. At current pricing, this represents an annualized yield of about 3.75%. Compared to prior period payout levels, 2022’s payout was 8% greater than 2021 but still over 50% below what shares offered prior to the COVID-19 pandemic.

Seeking Alpha – Recent Dividend Payout History

At a quarterly rate of $0.20/share, the annualized yield would be approximately 5.8%. This would certainly provide more incentive to income-focused investors.

And the company does appear to have the capacity for increases. At year end, the payout was less than 50% of their operating funds from operations (“FFO”). This is well below the sector average of 64%. In addition, on an adjusted basis, the payout was about 70%, which also compares favorably to the sector.

Furthermore, looking ahead, even if 2023’s results came in on the low end of their guidance range, the payout would still be below 75%. Moreover, they would still generate +$35M in retained cash flow.

For dividend growth investors, SITC offers a promising outlook for future increases. A return to their former payout levels is also within the realm of possibilities.

Main Takeaways

Despite limited availability of space, SITC is still posting robust leasing figures. This is reflective of the continued expansion into high-income suburban communities by well-capitalized retailers. This ferocious demand can clearly be seen in the numbers over the past two years.

In 2021 and 2022, for example, SITC has signed over 2M SF of new leases at spreads of over 20%. These signings include 73 anchor placements, which is notable since anchors typically require higher capital commitments in space preparation. This in turn creates a headwind on spreads. Despite this, however, the company has remained in the driver’s seat on rents due in part to the limited availability of space.

Their portfolio leased rate, for example, is up almost 400bps over the past two years and currently stands at above 95%.

The eventual recapturing of space from weaker tenants, such as BBBY, Party City, and Cineworld, will end up being a net-benefit to the company, as it will allow for more expedited mark-to-markets with better quality tenants.

The time lag, however, of when the new leases commence could create headwinds in future earnings growth in the near-medium term. And at current trading levels, with shares commanding a multiple of about 12x forward FFO, the stock appears fairly valued, given current uncertainties. Investors could see further dividend increases in 2023, but the yield still may not be enticing enough for most. Though the stock remains a quality long-term holding, a neutral position may remain most practical.

Be the first to comment