William Thomas Cain/Getty Images News

While the past 12 months have not been kind to the market as a whole, the period has been especially rough for media names as investors worry what a softening economy and lower ad revenues would mean for some of these leveraged names. We feel as though the recent COVID pullback taught us a lot about the durability of these businesses and that management teams in this industry are perfectly capable of cutting back to lower costs in order to maintain positive cash flow status or even profitability. While most of the low hanging fruit has already been harvested, there are a number of management teams we are following as they continue to cut costs and sell assets that are hidden within the balance sheet. This is helping a number of companies drive down their net debt and improve leverage ratios.

Revisiting A Previous Buy

With the latest pullback in some of these media names – which started back in November as key names were reporting earnings – we have been reading through quarterly filings and conference calls to try and find interesting names to deploy capital to. We have recently been buyers of Gray Television (GTN) and some terrestrial radio names, but we think that 2023 is the year to really focus on the television broadcasters as we should see political advertising pick up at the end of 2023 and then carry over into 2024 for what should be another recording breaking year for political spending. This is why we started looking at Sinclair Broadcast Group (NASDAQ:SBGI); a name we previously had some pretty nice gains with.

Ignore Diamond, Focus On Sinclair

There have been some news items out recently about the potential for Sinclair to walk away from, or at least lower their equity stake in, the RSNs (Regional Sports Networks) it controls via deals with teams whose broadcast rights it currently owns or even the leagues themselves. This centers around speculation that certain major sports leagues in the U.S. are interested in launching their own streaming apps and would need to own certain rights (regionally) in order to stream in those geographical areas as well as use the feeds to stream nationally. Some believe that it would be cheaper for the leagues to purchase Diamond Sports (the entity Sinclair formed to hold the RSNs) rather than piecemeal an offering together in the early days and gradually add to it.

While the purchase of the old Fox RSNs, via Disney (DIS) in order to get that merger approved, has turned out to be a major disappointment, from a credit perspective we think that Sinclair has done a great job in minimizing their downside in a worst-case scenario. Now that restructuring is being talked about for Diamond, Sinclair might be able to get the leagues to come in as equity investors or at least stay out of the way to allow Sinclair to clean this up in order to avoid what could be a painful bankruptcy process for Diamond and the individual sports teams. At the end of the day, this is not why we are interested in Sinclair at this time, and think that whatever comes of this situation should be viewed as a bonus and not a potential game changer for one’s investment in Sinclair.

Sinclair’s Recent Quarterly Conference Call

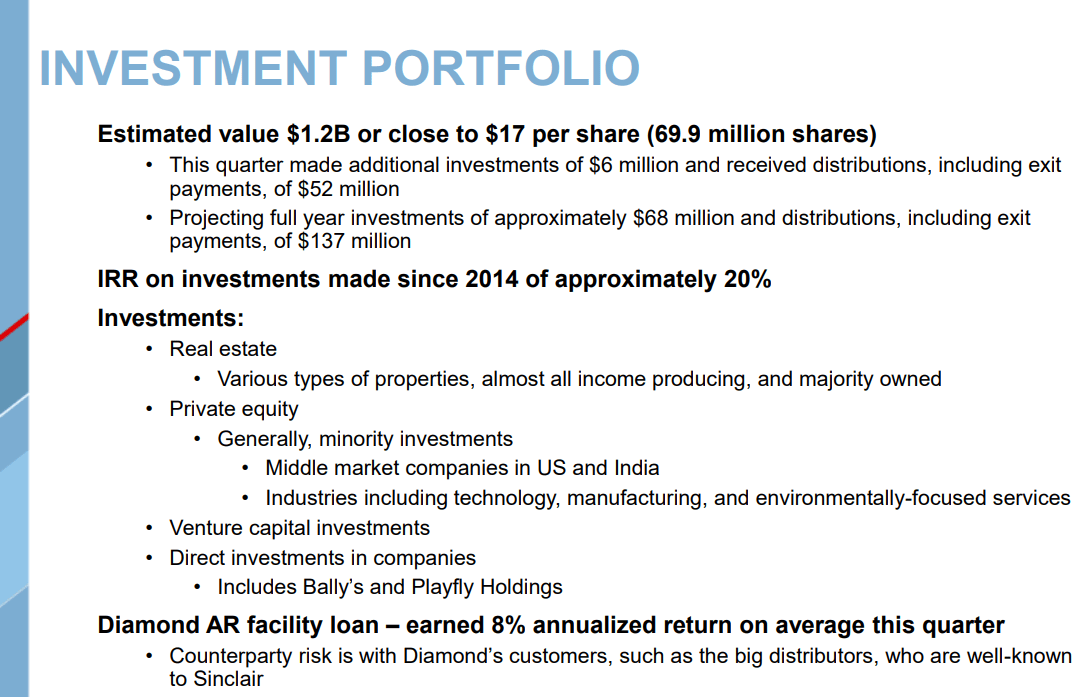

Sinclair last reported results back on November 2nd, issuing this press release and holding a conference call – the transcript of the call can be found here. Our first move was to read the conference call transcript and while viewing the slide deck, which was available via Sinclair’s website, we were stunned by management’s claim that the company has investments which they believe are worth nearly $17/share. For those not familiar with the company or its stock, that is just under the current share price!

Slide 6 of Sinclair’s slide deck for their most recent earnings call discusses their investment portfolio. (Sinclair Investor Presentation)

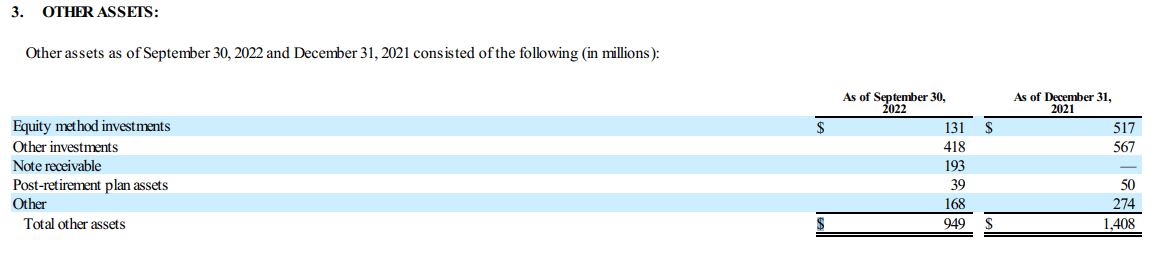

Claiming to have nearly $1.2 billion in investments is one thing, but actually having investments truly valued at $1.2 billion is another. Now to be fair, management does say that the investment portfolio’s value is estimated and when looking through their filings it does appear that they have cleaned up assets that would have been overvalued (RSN assets). From December 31, 2021 to September 30, 2022 we can see that Sinclair had some rather large changes within the category of ‘Other Assets’.

Sinclair carries a book value on its investments of $949 million but says that they believe the assets to be worth an estimated $1.2 billion. (Sinclair’s 10-Q)

Equity method investments were impacted by the deconsolidation of Diamond. Sinclair also entered into an A/R lending agreement with Diamond by buying its current lending facility and becoming the lender itself; that is the $193 million ‘Note Receivable’ line item.

So what could be causing this difference? It appears that the difference is the price at which the assets are being carried on the books at and current values. This is nothing new, it happens all the time and even with real estate having come under pressure in recent months, we are inclined to believe that management might very well be accurate in their estimates (although we cannot say for certain as we are not 100% sure on the investments or the allocations they are currently utilizing for the portfolio).

Add in the $600 million or so of cash and cash equivalents that Sinclair has on the balance sheet and we like what we see.

Potential Issues

While Sinclair’s debt is manageable at current levels, and the company has the cash flow to continue to service the debt, we do think that an overly aggressive Federal Reserve in 2023 could inflict further pain on the broadcaster. Per the conference call, Sinclair has about 60% of its debt structured as floating rate and each 100 basis point increase in rates results in roughly $27 million in additional interest expense (on an annual basis). While this is partially offset by Sinclair’s cash and cash equivalents also earning higher interest rates, the fact of the matter is that Sinclair is going to be paying more for interest expense/debt servicing moving forward (until the Fed cuts rates or Sinclair repurchases a bunch of debt). The good news is that there are no impending maturities that Sinclair has to address, so they still have some flexibility in addressing debt, investments and buybacks.

Share Buybacks And Debt Repurchases

Sinclair has repurchased approximately 5,300,000 shares already this year, which represents about 7% of the total shares outstanding (note: 5,000,000 of the shares were purchased through the end of Q3 with an additional 300,000 shares purchased in Q4 through November 4, 2022). That is pretty impressive, but even more so is the fact that Sinclair has reduced shares outstanding by nearly 40% over the last three years – which Chris Ripley, President and CEO, was quick to point out during the Q&A session of the conference call. As of quarter end, Sinclair had $704 million remaining in their share repurchase program – so yes, we do believe that management will continue to focus on returning capital to shareholders via share repurchases.

These share repurchases will enable management to redeploy the roughly $5.3 million in annual dividends to offset additional interest expense from the variable rate debt, help increase dividends moving forward or use it to buy back more shares or debt. It is not a lot of money in the grand scheme of things, but it can be deployed in an efficient manner.

Not only is management repurchasing shares, but they are also paying down debt. Sinclair refinanced and rolled some debt during the quarter, but then shifted focus to the STG 5.125% senior notes due 2027 and repurchased $118 million aggregate principal amount for $104 million, which created a gain on the extinguishment of debt. This move will save nearly $6.05 million annually in interest expense.

Our Take

Over the years this is a story that we have liked; although we have owned it for very different reasons, we are now bullish once again on the long-term outlook for Sinclair. We are well aware of the big brokerages having lowered their outlooks and price targets since Sinclair reported earnings back in November, and while we agree that there might be some revisions to the downside, it is our opinion that the story here is not fully understood by the market and that the company is well suited to work its way through a possible economic pullback. Sinclair might look boring from the outside, but if you look under the hood it is apparent that the company continues to generate ample adjusted free cash flow and has many levers to utilize in order to increase shareholder returns, including selling some of its investments to simplify the balance sheet.

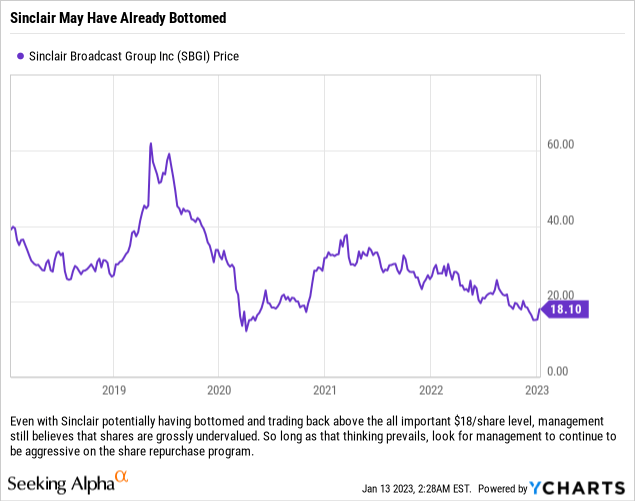

We purchased shares at $17.94/share in a handful of accounts yesterday to hold for 12-24 months with our eye on the 2024 election cycle and the political money which should pour in. These accounts vary in their mandates, but Sinclair pays a healthy dividend (meaning it can be considered a dividend play) and has capital gain potential which allows it to fall within the scope of many mandates. The good news, in our opinion, is that we can sit back, collect a dividend yielding over 5.50% and trade covered calls if we really want to generate additional income over the next year as we wait for the 2024 political ad dollars to show up and potentially push shares into the $25/share area.

Be the first to comment