Marko Geber

I listened to the live Silvergate Capital (NYSE:SI) call, and in summary, they didn’t say anything earth shattering, but in general, it wasn’t great. The CEO and CFO were on the tight-lipped side, which added to the impression out there that they may not entirely be upfront with investors. This article is an updated version of yesterday’s note to subscribers.

One of the new developments is that Silvergate is offloading what they refer to as a few non-core customers. They’re letting some of their crypto customers go. According to the CEO, this isn’t due to any regulatory pressure but it’s a business decision. This appears to be the same thing Signature Bank (SBNY), a competitor with similar crypto-related banking services, is doing and announced back in December. Some customers simply aren’t bringing any volume or generating any revenue, and with the crypto market downturn, that’s unlikely to change anytime soon.

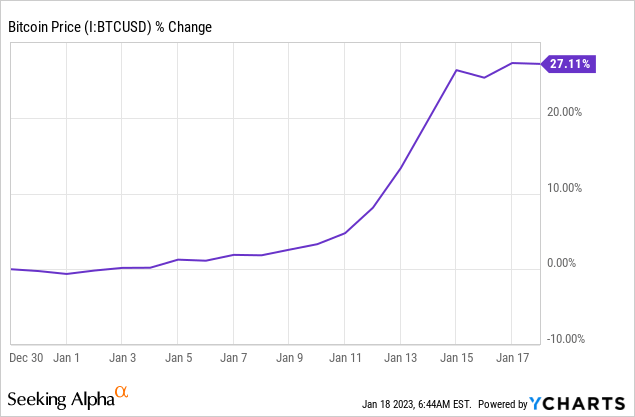

They’re also cutting service products specifically aimed at their digital asset customers. Management also is calling this another business decision. They’re gearing the company up to maintain profitability even if the crypto downturn continues for an extended period of time. I’ve been pleased to notice year-to date Bitcoin (a bellwether for the industry) has started to recover:

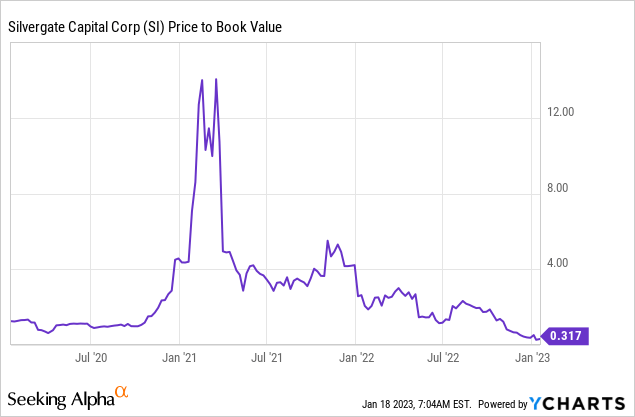

Book value at Silvergate is now $12.93 and there was one caller who specifically asked if we could expect further impairments next quarter. This is one of the questions where the CFO didn’t make a great impression. He talked around the question and said that (depending on how conditions evolve) there could be further impairment driven by tax assets going down in value.

The worst part of the call was when management was asked about the Signature Bank call. Specifically about the part of the Signature call when an analyst inquired about the AML/KYC/BSA problems around FTX and he got a very forthright answer. Here’s the question from the Signature call (emphasis mine):

Analyst

Got it. OK. And then my last one is just you know, I love your thoughts on the crypto regulatory front and implications to you, particularly on the back of the interagency guidance earlier this month. I’m curious in the wake of FTX [ph] if there’s been any reassessment on the institutional client book or the BSA, AML, KYC process front to make sure that there aren’t other instances of fraudulent activity. What changes actions have you taken? And what kind of comfort can you give us on the quality of the remaining client book?

Joseph DePaolo

Well, I’ll say this with FTX, it wasn’t a matter of BSA AML. Everyone thought that he was [indiscernible] and he ended up being very made offline. So I don’t think anyone could say that they knew that, and we catch it. What we’re talking about regulation is we just want to know which way you go because we had Signet and we try to make enhancements on it, and some were okay by the regulators and some were not. It puts us in a difficult position as to what we do – what do we do next? And not knowing regulation-wise what’s going to happen puts us really at behind everyone else that is in the crypto world.

I will tell you this. We’ve had – we’ve had a number of discussions with the regulators, and they seem to be waiting for other regulators. So I don’t know if the Fed is waiting for the FDIC. The FDIC was waiting for the OCC. But I think they have to get together, meet with Congress because Congress was going to put some before the end of the year. Congress is going to put some of those across to get some loss put on the books for regulation. And they were not things that we thought were good for us or good for the industry.

So we need to get them to get on the same level of field and give us some guidance. There’s no – I think what happens is when the regulations come out, that will eliminate a number of players. I don’t know if [indiscernible], but I would say a number of players couldn’t want to look to the regulation, whether it’s capital integrate or just doing AML DSA. But again, FTX was not a BMA AML. It was a Bernie [ph] made of like a situation that no one really thought that Sam [ph] was a bad asset.

He’s implying there was nothing wrong with the processes and FTX was a Bernie Madoff-type situation, and no one thought Sam was a bad asset.

On the Silvergate call, they discussed the issue and didn’t want to comment on FTX and AML processes. The way it was handled on the Signature call was much more relaxed. To an extent, I can understand. The pressure on Silvergate is much higher due to a short-selling campaign and their deposit base isn’t as diversified as Signatures. They’ve also got more attention from lawmakers like Elizabeth Warren.

The last weak moment came when the CEO responded to a question about rebuilding the balance sheet, tier-1 capital, and raising capital, and he said the following:

Yes. Jared, I appreciate the question. I’m going to ask Tony to comment in just a minute. But the one thing that I would point out is – and again, of course, we’re not going to provide guidance on if and when we might quote unquote, raise capital. But, I think Tony will touch on this. It’s important to recognize that, number one, our risk based capital ratios continue to be extremely robust, which is reflective of the very low credit risk on our balance sheet. But importantly that Tier 1 ratio is based on average asset. And so, it’s really important to think about that as we move into the first quarter here. And without stealing anymore Tony’s thunder. Tony, do you want to address that in a little bit more detail?

The CFO did give a solid walkthrough of why the tier 1 capital ratio looks low but it’s actually in much better shape. But they left the door open for a capital raise, and I wouldn’t be surprised if they raised capital to the tune of $50 – $100 million. That would be quite dilutive for shareholders. At the same time, it could be valuable if done with a strategic or someone who also brings a seal of approval. Think along the lines of the deal Goldman Sachs (GS) did with Warren Buffett’s Berkshire (BRK.A) (BRK.B) in the depths of the GFR.

Summary

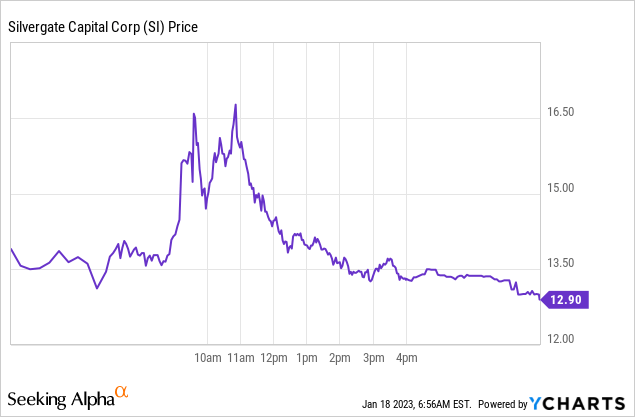

It either wasn’t a great performance by the management OR there are still some shoes to drop. I think the market isn’t wrong to give back some of the gains before the call. It’s a shame, though, because the company was up toward $16.50 at one point and declined back down to $12.90.

At the same time, crypto markets appear to be recovering, and the call wasn’t downright terrible. The numbers could have been worse. They’re doing the right thing in demonstrating resilience and safety to customers, and they’re rightsizing the ship to get back to profitability in 2024 and onwards. I recently added to my already large position when the stock dropped ~45% in a day. At the time, I added between $12.25 and $13.90. Yesterday, I reduced my position back to the size it was before the Jan. 5 crash. Some because the stock was quite strong pre-call and some when I didn’t love things, as discussed above on the call.

Silvergate is now a 2% position for me. It started quite a bit larger because I entered most of it much higher. Given the volatility in this name, I don’t mind it’s now a lot smaller. However, I do think with the stock below book value, it’s too cheap. If it trades down from book value, I’ll be tempted to top up again. Right now, investors are looking at book value as an anchor. All the excitement about earnings power due to servicing the crypto industry is gone. However, the excitement around crypto ebbs and flows. It’s currently at a low point because of the FTX fallout and the sustained crypto bear market. Longer term, I do think the crypto industry won’t go away and could very well be a net benefit to society. Returning to that viewpoint, the stock can start trading above book value again as it has in the past. In addition, there are ways some book value could be recovered through reversing the write-off of the Diem asset, for example.

Be the first to comment