Michael M. Santiago

Investment Thesis

Chipotle Mexican Grill (NYSE:CMG) is a great company. It is a unique play in the fast-food industry that emphasizes the use of real ingredients to make quality food to attract customers to its restaurants. It operates all the restaurants in its portfolio and does not have a franchising model, which ensures a more consistent level of service. This superior product quality has created a loyal customer base that sees significant value in its menu offering. This has allowed the company to grow sales at a very high rate, both in terms of new store additions and increases in same-store sales. Moreover, the company has demonstrated its pricing power ability without sacrificing top-line growth. On top of that, it has a very strong balance sheet that is debt free. However, it can be argued that the share price has factored in a lot of these strong attributes and thus the valuation is somewhat stretched. Assuming a 3-year net income CAGR of 26%, the stock trades at a forward 2025 P/E ratio of 26.5x. I find that valuation to be on the high side and accordingly my recommendation for the stock is “Hold.”

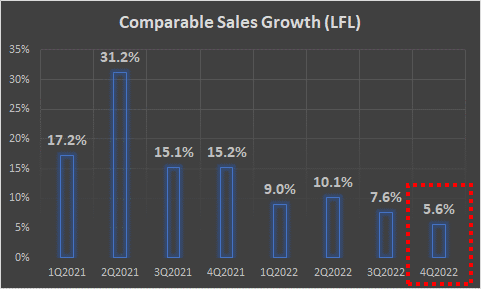

4Q2022 Comparable Restaurant Sales Growth Disappoints

CMG reported comparable sales growth of 5.6% YoY in 4Q2022. This comes at the lower end of management’s guidance of mid to high-single digits growth in comparable sales. Moreover, management indicated in the 3Q2022 earnings call that 4Q2022 will be up against easy YoY comps. Their logic was that they ran out of stock for the brisket limited time offering (LTO) in mid-November 2021, while they anticipated the latest LTO (the Garlic Guajillo Steak) will run for the entire 4Q2022. However, it seems that the performance of the Garlic Guajillo Steak in 4Q2022 was underwhelming—most likely due to its high price point in weak economic conditions. Also, the YoY comps in 4Q2022 saw an 80-basis points headwind from the loyalty program.

Figure 1 Comparable Sales Growth Slows Down

Calculated by Author using data from the company

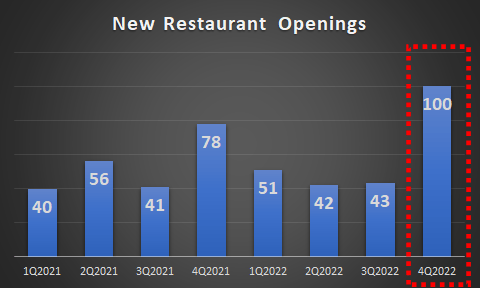

New Restaurant Openings – Firing on All Cylinders

CMG set a quarterly record for new restaurant openings in 4Q2022. The company managed to open 100 new restaurants during the quarter and raise its tally for FY2022 to 236 new restaurants. Again, this was towards the bottom end of guidance, which pointed to 235 to 250 new restaurants. I believe that achieving 100 new restaurants in a single quarter should be viewed positively. On the other hand, management stated that most of the new restaurants were backloaded in the quarter—as the majority opened in December. Thus, these new openings had very little contribution to the top line in the quarter.

Figure 2 New Restaurant Openings

Calculated by Author using data from the company

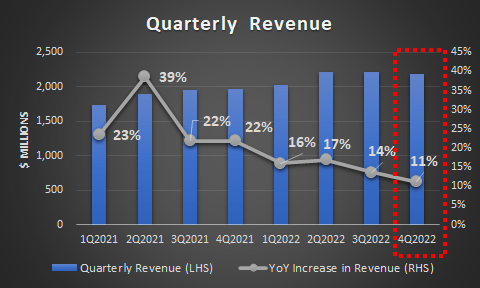

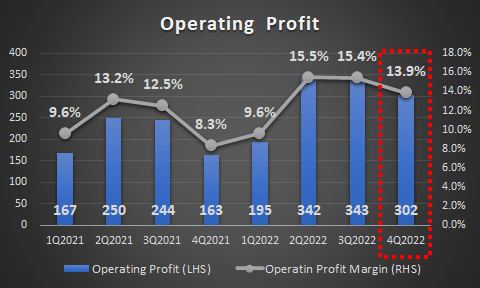

A Look at the Operating Results

CMG posted an 11% YoY top-line growth in 4Q2022, which is the slowest pace of growth in the last 8 quarters. Given that the store openings were largely on track, I find this slower pace of growth to be a bit alarming relative to the stock’s high valuation. On the other hand, the operating profit margin continued to benefit from the positive implication of the menu price increases that were made in FY2022.

Figure 3 Quarterly Revenue

Calculated by Author using data from the company

Figure 4 Operating Profit

Calculated by Author using data from the company

Outlook for FY2023 Looks to be on the Softer Side

CMG’s stock price is heavily reliant on growth expectations for sales. For FY2023, the company plans to open 255 to 285 new restaurants. This represents an 8-9% YoY increase in the store count, a pace that is very similar to FY2022. The second driver of sales growth is the increase in comparable sales. Management only guided for comparable restaurant sales growth in the low-double-digits for 1Q2023. During the 4Q2022 earnings call, management said that this is the last quarter to benefit from the increase in menu prices and that they expect comps to moderate in the second and third quarters of FY2023. The lack of planned price increases for FY2023 would mean that sales comps improvement needs to be driven by an increase in transactions. However, in 4Q2022, transactions were down by 4% YoY. Thus, unless there is a meaningful pickup in transactions, sales comps would likely be challenged to post growth in the second half of 2023.

Key Risks

The key risks for the stock revolve around situations that could negatively impact the pace of sales growth. This could stem from increased competitive pressure (a new entrant with a superior value proposition or an enhanced service offering from existing players) or damages to the reputation of the chain (like the E. coli outbreak in 2015). CMG has an aggressive expansion plan and aims to add more than 255 new restaurants in 2023. There is always a risk that the new locations could be less successful than the average store in the portfolio or cannibalize the customer base of other nearby stores. Other risks are on the cost side, namely ingredient costs and labor costs. Ingredient costs are on the rise to rising food prices, but CMG has shown its ability to pass on the increase to customers. Another threat would be the company’s ability to continue to hire new labor at competitive rates and be able to cope with a potential rise in unionization.

Valuation

For valuation, I try to look at the 3-year forward P/E ratio (FY2025). I assume that sales will grow at a 3-year CAGR of 15% and that the net profit margin will expand by 220 basis points, using FY2022 as my base. This implies a 3-year CAGR growth of 26% for net income. Accordingly, the 3-year forward P/E ratio is 26.5x, which is a hefty multiple given the above assumptions. Thus, I see Chipotle as a great company that trades at a rich valuation.

Final Thoughts

It will be interesting to see how the market will react to CMG’s result over the next two weeks. The stock was down 5% in the after-hours post the announcement. The short-term outlook for CMG could be a little murky and this could lead to some divergent views among investors. However, I believe that the medium-term growth story remains very strong.

Be the first to comment