Daria Nipot/iStock Editorial via Getty Images

If a year ago, you had predicted that Amazon (NASDAQ:AMZN) would drop by a third in twelve months, and that it would still be outperforming two of the other three FANGs, you would have been labeled fifty-one-fifty.

Yes, the long time darlings of the stock market are now pariahs. The best performing of the four FANGs has dropped further year-to-date than the S&P 500.

Pundits commonly claim Amazon’s slide was prompted by dismal first-quarter results. That is not surprising considering the company reported a net loss of $3.8 billion in Q1 2022, its first quarterly loss in seven years.

However, the stock had dropped 15% in the month leading up to that earnings call. More importantly, the last quarter has a lot of moving parts, so to speak, and it behooves investors to dissect the earnings call to gain insights into the company’s future.

Furthermore, there is a Jekyll and Hyde quality to Amazon’s growth trajectory that should be examined.

Why AMZN Shares Plummeted

Internet, technology, and growth stocks, particularly those that experienced a surge in revenues due to pandemic trends, have been cast aside by investors. Amazon checks each of those boxes.

Next consider that Amazon is the second largest retailer in the world, and rising interest rates and inflation present manifest threats to consumer spending. Combine that with the aforementioned poor quarterly results, and you have a perfect storm for AMZN shares, down over 33% in 2022.

Moreover, while threatening future sales, inflation is also driving up costs. Amazon’s pandemic related expenses totaled $10 billion plus in 2021. Supply chain costs also continue as a headwind for the company. Management has stated the shipping containers cost more than double that of the pre-COVID period.

Inflation was in the transportation costs, especially in wage inflation last year. It remains there. It’s been amplified a bit by the fuel costs following the Ukraine conflict, which has happened since we last spoke. So, it’s more a factor — those costs will now, we believe, will persist a little longer than we were hoping at the beginning of the year. And I mentioned some of the per unit rates for transportation, cargo shipments and also fuel costs. Those are real, and we have to find ways to offset those or use less of high-cost things, like transportation and fuel.

Brian Olsavsky, CFO

The tremendous surge in ecommerce sales is a double-edged sword. AMZN nearly doubled its operations capacity in the past two years, and this led to a commensurate increase in the firm’s workforce.

Capacity decisions are made years in advance, and we made conscious decisions in 2020 and early 2021 to not let space be a constraint on our business. During the pandemic, we were facing not only unprecedented demand, but also extended lead times on new capacity. And we built towards the high end of a very volatile demand outlook. …We estimate that this overcapacity, coupled with the extraordinary leverage we saw in Q1 of last year, resulted in $2 billion of additional costs year-over-year in Q1.

The fact is, AMZN was caught in a “damned if you do, damned if you don’t” moment. During the Q2 2021 earnings, management stated, “our focus is really squarely on adding capacity to meet the current high customer demand.” Later in the call, Brian Olsavsky added, “… again, we’re handling volumes that were somewhat unheard of year-over-year. And that’s why we’re building out our networks so quickly in our minds.”

Despite ramping up capex devoted to fulfillment, the company noted in the accompanying 10-Q that sales growth was “partially offset by fulfillment network capacity and supply chain constraints.”

However, warehouses need workers. During the Q3 earnings call, the CEO remarked, “…labor became our primary capacity constraint, not storage space or fulfillment capacity. As a result, inventory placement was frequently redirected to fulfillment centers to have the labor to receive the products.”

Now flash forward to the last quarterly report:

We hired more people and then found ourselves overstaffed when the Omicron variant subsided rather quickly, at least from our standpoint in warehouses. So, the issue is switched from disruption to productivity losses to overcapacity on labor. And we believe that that will dissipate. It will take time in Q2, but — so it’s not the full — we don’t get the full $2 billion back in Q2, but we will make great strides on that.

Brian Olsavsky

Amazon estimates that inflationary pressures and excess fulfillment capacity each added $2 billion in incremental costs during the most recent quarter.

That is how you get to the dismal Q1 results that sent investors scurrying to dump shares. Amazon reported the first quarterly loss in seven years, shocking analysts and investors with a net loss of $3.8 billion, well below its net income of $8.1 billion in the comparable quarter.

Operating income fell year-over-year from $8.9 billion to $3.7 billion, and Amazon’s operating margin dropped by 5% to 3.2%. Perhaps worst of all, free cash flow decreased to a negative $18.6 billion for the trailing twelve months versus the prior positive FCF of $26.4 billion.

Where Growth Won’t Move The Needle

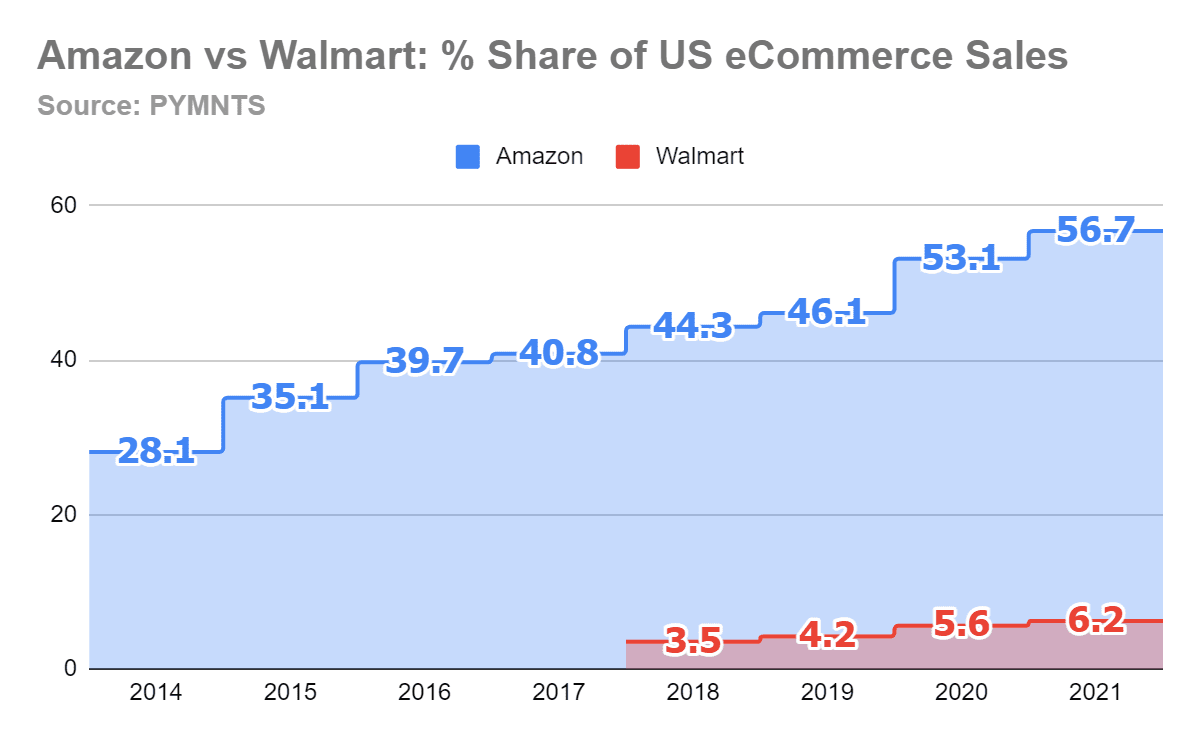

Many investors think of Amazon as an ecommerce company. Despite strong showings by the likes of Walmart (WMT) and Target (TGT), AMZN continues to increase its share of a rapidly growing market.

PYMNTS.com

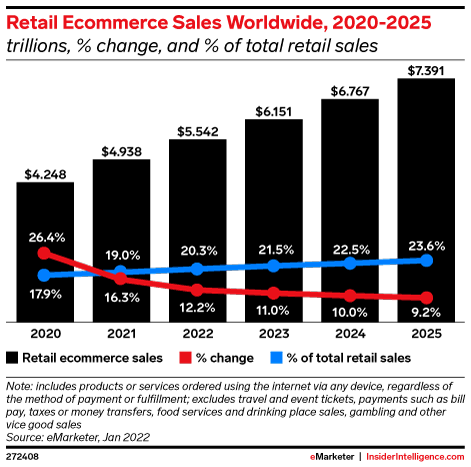

While the surge in ecommerce sales is subsiding, continued strong growth is projected for years to come. Amazon also has potential for outsized ecommerce expansion overseas. This provides AMZN with ample opportunity for growth going forward.

eMarketer

Even though Amazon’s continued dominance in ecommerce is practically assured, growth in that arena will not spur the share price. The low single digit retail margins the company generally reports cannot support the high P/E ratio that marks Amazon’s stock.

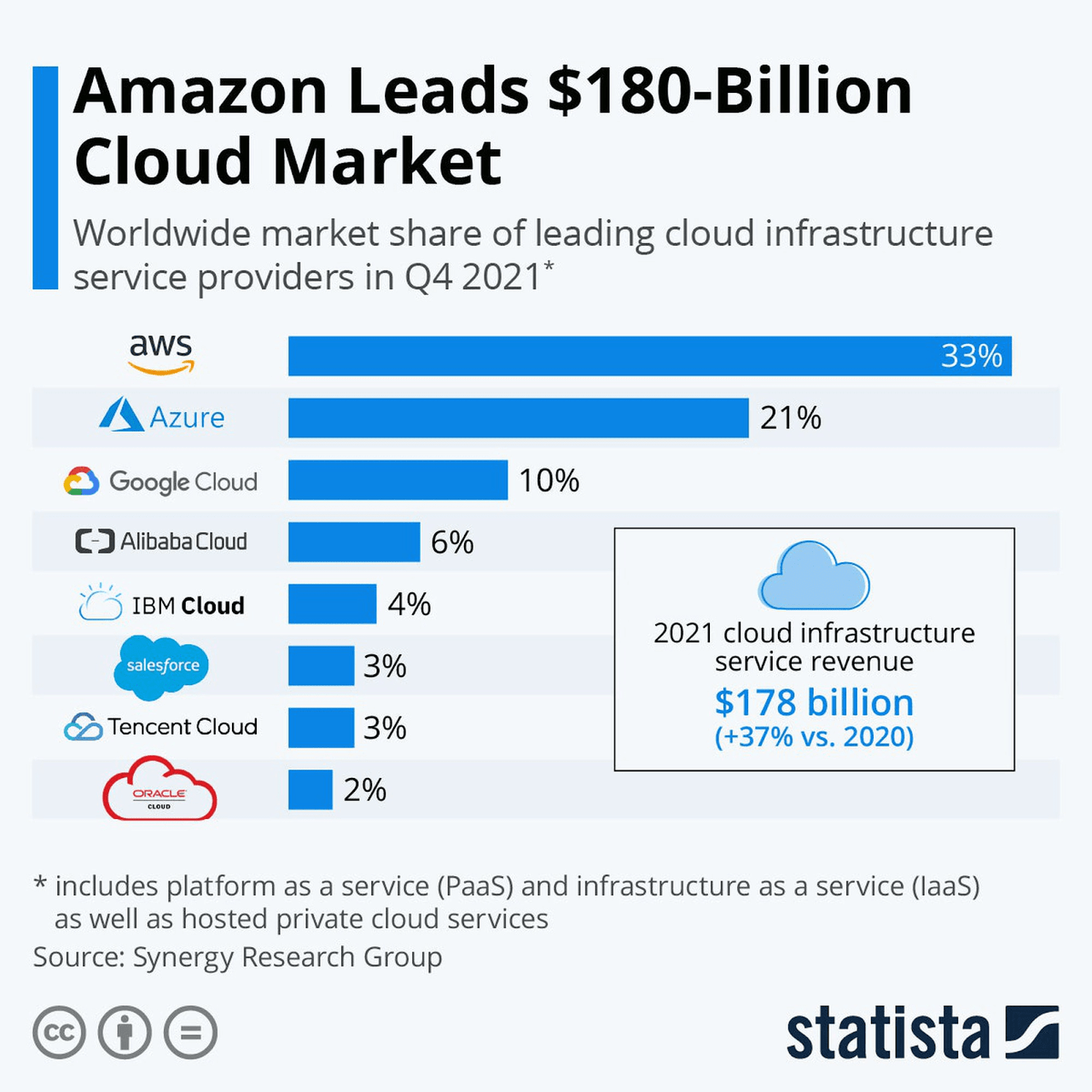

AWS Is A Horse Of A Different Color

Like the company’s ecommerce offerings, Amazon’s cloud business is expected to record strong growth for the foreseeable future. However, unlike ecommerce, AWS provides robust and growing margins. Therefore, strong growth in the cloud business should lead to real growth in free cash flow, supporting the sort of P/E ratio that characterized FANG stocks over the last few years.

AWS generated 13% of Amazon’s total revenues last year, but accounted for more than 74% of the company’s total operating income. In Q122, revenue growth for AWS stood at 37%, jumping from $13.5 billion to $18.44 billion year-over-year. That also pushed the segment’s share of overall revenue to 16%, up from 13% year over year.

Operating margins for AWS went from 30.8% in Q121 to 35.3% in Q122. Due to greater economies of scale, it is likely that AWS margins will continue to climb. All of these metrics highlight how AWS can bolster Amazon’s revenues in years to come.

Additionally, launching a cloud infrastructure service requires massive initial investments. Amazon, Microsoft (MSFT) and Google (GOOG) (GOOGL) generate enormous free cash flow, and this enabled each of the firm’s to devote the capex needed to establish the cloud businesses.

In fact, look no further than Google Cloud for proof that size matters in this arena. Google Cloud lost $17.6 billion over the last four years, despite its position as the number three player in the cloud market. This is proof that Amazon’s enormous investment in cloud infrastructure also provides a wide moat to stave off rivals.

Statista

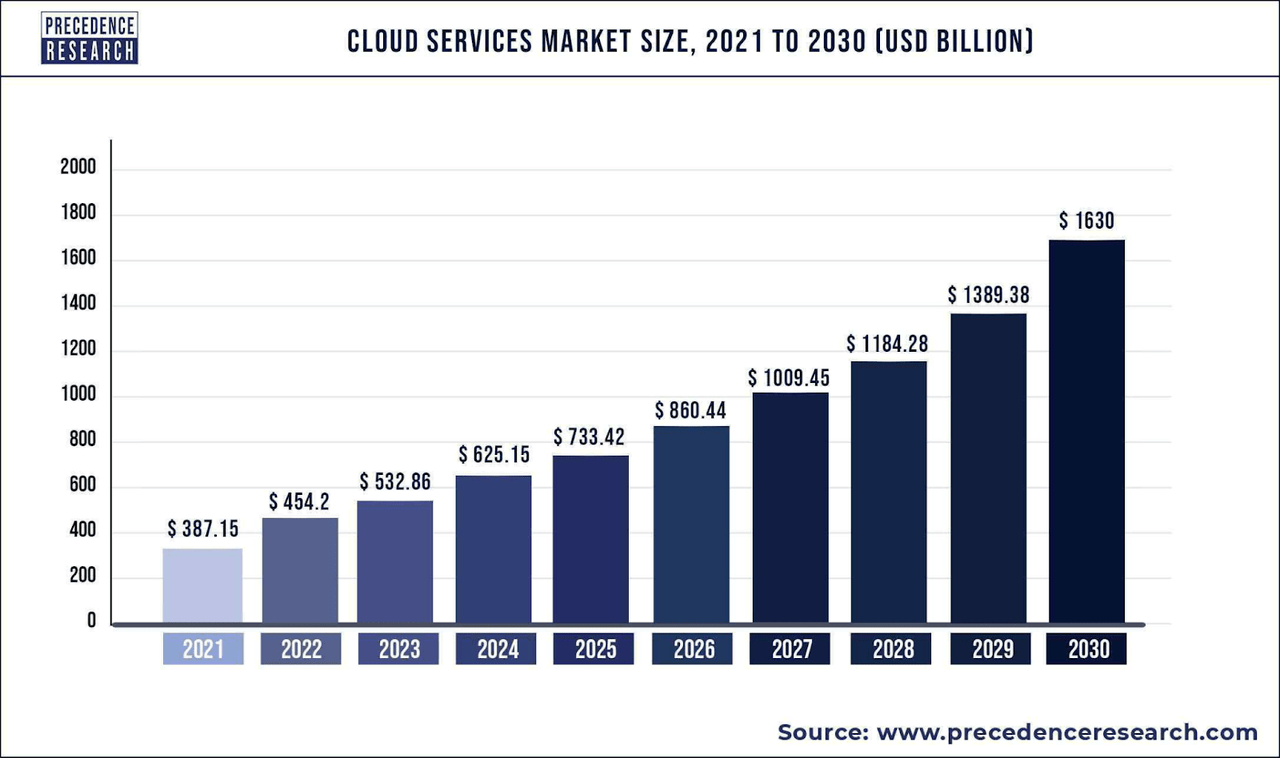

Now consider that Grandview Research forecasts a CAGR of 15.7% for the global cloud market from 2022 to 2030. This would increase the market by 272% over that time frame. This is backed up by a report by Precedence Research that projects the global cloud services market will surpass $1.6 trillion billion by 2030, growing at a CAGR of 17.32%.

Precedence Research

A Second Source Of Sure Growth

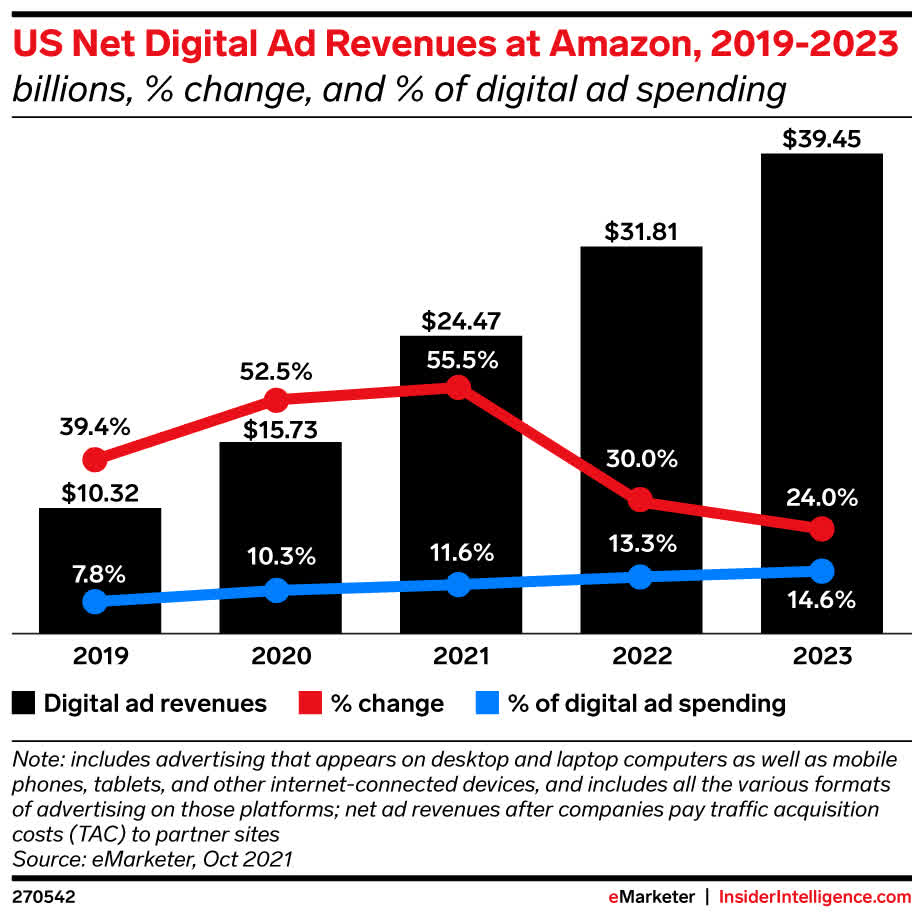

In FY21, the company reported r $31.2 billion in ad revenue. That marked a 58% increase over 2020, and a 146% increase over 2019. Last quarter, AMZN recorded $7.9 billion in advertising revenue. That represented 25% year-over-year growth. Amazon’s advertising business ranks as the third-largest US online advertising service, behind only Alphabet (GOOG) (GOOGL) Google and Meta (META).

There is good reason to believe Amazon’s advertising arm can capture a larger market share. According to a study by Feedvisor, advertising on AMZN gives businesses a seven times return rate, and Businesswire reports 58% of brands see “great value” in Amazon Advertising.

eMarketer

eMarketer projects Amazon advertising will increase its US market share from 11.6% in 2021 to 14.6% in 2023. Like AWS, advertising is a high margin business. In fact, when you compare Meta and Google’s operating margins to that of AWS, it is reasonable to assume that Amazon’s advertising business will generate higher operating margins than the cloud division.

A Few More Considerations

Amazon raised annual Prime subscription prices by 17% in February, and management reported the company “added millions more new Prime members during the quarter.”

Prime Day concluded last week with the company reporting that Prime members made purchases at the rate of 100,000 items per minute. In total, over 300 million items were sold, and AMZN set a new record for Prime Day, with $11.9 billion in sales.

There is also a retail related initiative AMZN is pursuing that could provide additional growth. The company has opened a number of stores using Just Walk Out technology. Just Walk Out provides a cashierless buying experience. A customer simply enters the store using a QR code, selects his or her purchases, and walks out of the store without waiting in line for checkout. A smart app charges the purchases to the shopper’s account.

engadget

The technology is gaining a bit of a foot hold. The Houston Astros will provide Just Walk Out in two stores at Minute Maid Park, late last year, Starbucks (SBUX) teamed with AMZN to open a cashierless store in New York City, and AMZN licensed the technology for use to the UK supermarket chain Sainsbury’s.

Verified Market Research estimates the retail automation market will be worth nearly $32 billion by 2028. Loop Ventures sets the mark a bit higher, forecasting a potential market of $50 billion.

Where Many Are Missing The Mark

Perusing the Q1 2022 earnings call provides a number of clues as to why last quarter’s results were so disappointing and where the company will go from here.

But putting all that aside, you asked the question about transportation shipping rates. Our shipping rates are very competitive, and we are seeing savings versus what we would get from external carriers. And it’s beyond that. We would not even necessarily have had the capacity to — from external third-party providers to handle the transportation loads that we’ve seen in the last couple of years.

Brian Olsavsky

So, we’re really glad that we have our — as we built our AMZL network, we would not be able to have a one-day program, same day and one-day shipments, if we try to deliver it with third-party shippers. It just would not be cost effective. So, what you’re seeing there in the growth in shipping costs versus the unit growth, a little bit on the unit side, but essentially a factor of inflation and productivity that I’ve mentioned to you on the component that hits in the transportation area.

Brian Olsavsky

We have lowered our operations, capital expenditures for 2022 and are evaluating other ways to increase our fixed cost leverage. We estimate that this overcapacity, coupled with the extraordinary leverage we saw in Q1 of last year, resulted in $2 billion of additional costs year-over-year in Q1.

Brian Olsavsky

We have worked to protect and enhance the customer experience despite a sharp increase in costs, particularly over the past three quarters. We’ve seen a large cost to keep up with demand these past two years. During this period, we doubled the size of our operations and nearly doubled our workforce to 1.6 million employees.

Brian Olsavsky

Capital investments were $61 billion on the trailing 12-month period ended March 31. About 40% of that went to infrastructure, primarily supporting AWS, but also supporting our sizable consumer business. About 30% is fulfillment capacity, primarily fulfillment center warehouses. A little less than 25% is for transportation.

Brian Olsavsky

We reported an overall net loss of $3.8 billion in the first quarter. While we primarily focus our comments on operating income, I’d point out that this net loss includes a pretax valuation loss of $7.6 billion, included in nonoperating expense from our common stock investment in Rivian Automotive.

Brian Olsavsky

The next excerpt is Dave Fildes responding to an analyst’s question regarding AWS backlog.

It’s the increase of AWS customers making long-term commitments for AWS. At the March period ended, we had $88.9 billion balance for that. So, that’s up about 68% year-over-year.

My take is that the company has “paid it forward” albeit in a strictly financial sense. AMZN took a big hit to its bottom line by devoting capex to projects that should spur margin growth and provide a competitive edge. While management overspent on the company’s logistics network, that will even out over the long term.

AMZN Stock Key Metrics

AMZN has a solid balance sheet, with cash & marketable securities of $66.4 billion at the end of 1Q22 versus total debt of $47.6 billion. S&P rates Amazon’s credit as AA- (stable) while Moody’s provides a rating of Baa1 (stable). Both ratings are investment grade.

Seeking Alpha provides a forward P/E of 154.53x, and a 5 year PEG of 4.91x. Both are well above the company’s average ratios over the last five years.

Yahoo Finance calculates the forward P/E as 68.49X, and the 5 year PEG at 4.28x.

AMZN currently trades for $113.55 per share. The average one year price target of the 41 analysts covering the company is $183.06. The average price target of the 31 analysts rating the company following the last earnings report is $180.93.

Every analyst that provided a rating has AMZN at Buy, Overweight or Outperform.

Is AMZN Stock A Buy, Sell, or Hold?

I fully understand why Amazon’s last quarterly results shocked analysts and investors alike. I also agree that in some respects, the valuation metrics for the stock are unappealing.

However, I think the multiples represent a temporary aberration, and that we will see the P/E and PEG ratios return to more attractive levels once Amazon’s enormous investments in logistics and AWS have time to play out.

Furthermore, investors need to allow that Q1 included a $7.6 billion after-tax write-off in Rivian (RIVN). Then consider that the company reported a backlog for AWS of $88.9 billion.

There is also ample reason to believe the company will resume its former growth trajectory. Amazon’s advertising division is large, is growing at a marked pace, and should provide hefty margins. I base this on my observation that Meta had margins greater than 30% when it was a similarly sized business.

As previously noted, AWS also commands high margins. Furthermore, those margins have increased over time.

To demonstrate Amazon’s potential for growth, let’s create a scenario in which AWS revenue increases at a 24% rate over the next three years, noting that would represent a markedly lower growth rate than witnessed for over a decade.

The division would double in size over that time frame. Using the 2021 fiscal year’s $62 billion in AWS revenue, that would put AWS revenue at $124 billion by the end of 2025. Assuming margins stayed the same (margins are likely to expand) Amazon’s operating profits would increase from $25 billion to $37 billion, and that is assuming the remainder of the company’s divisions reported stagnant growth.

Weighing these factors, I rate AMZN as a BUY.

Why I’m Waiting To Add To My Position

Before I launch into this explanation, I must admit that I am climbing out onto a limb. Nonetheless, it represents my strategy for the next few months.

Once again, I will resort to quotes from the last quarterly report to highlight the rationale for my position.

We do expect the effects of these fixed cost leverage to persist for the next several quarters as we grow into this capacity.

Brian Olsavsky

Our guidance includes an expectation that we will incur approximately $4 billion of these incremental costs in Q2.

Brian Olsavsky

The other thing — again, Brian mentioned it towards the end there of this opening — to see that seasonal step-up in stock-based compensation expense. So, recall that our employees received those RSU grants in the second quarter. This year, we expect to see the expense of approximately $6 billion. And so, that’s up from about $3.3 billion in the first quarter.

Dave Fildes

…note that this year’s Prime Day sales event will occur in the third quarter, in July to be specific. Last year, in 2021, Prime Day occurred in the second quarter. Prime Day contributed about 400 basis points to our Q2 2021 year-over-year revenue growth rate.

Brian Olsavsky

Management guided for revenue of $116 to $121 billion, and a loss of $1.0 billion to a profit of $3.0 billion in Q2. I doubt that the lower end of that guidance will inspire renewed confidence in the stock.

Of course, investors will contrast this Q2 to Q2 2021. As noted in management’s statements above, there are a number of factors that could make for a poor comparison.

I believe that anything short of a blowout quarter will not result in a big positive move for the share price.

On the other hand, Q2 results on the lower end of guidance, the economy officially entering a recession, and/or continued downward pressure on the market, all of which I view as likely, will work against the share price.

My decision largely boils down to market sentiment and macroeconomic factors. I think the odds are in my favor if I wait until sometime near the third quarter, or later, to add to my position. Of course, developments could alter my perspective.

Be the first to comment