Will “o the Wisp RollingEarth/iStock via Getty Images

This company was reviewed on the 13th of July in the Daily Drilling Report.

Introduction

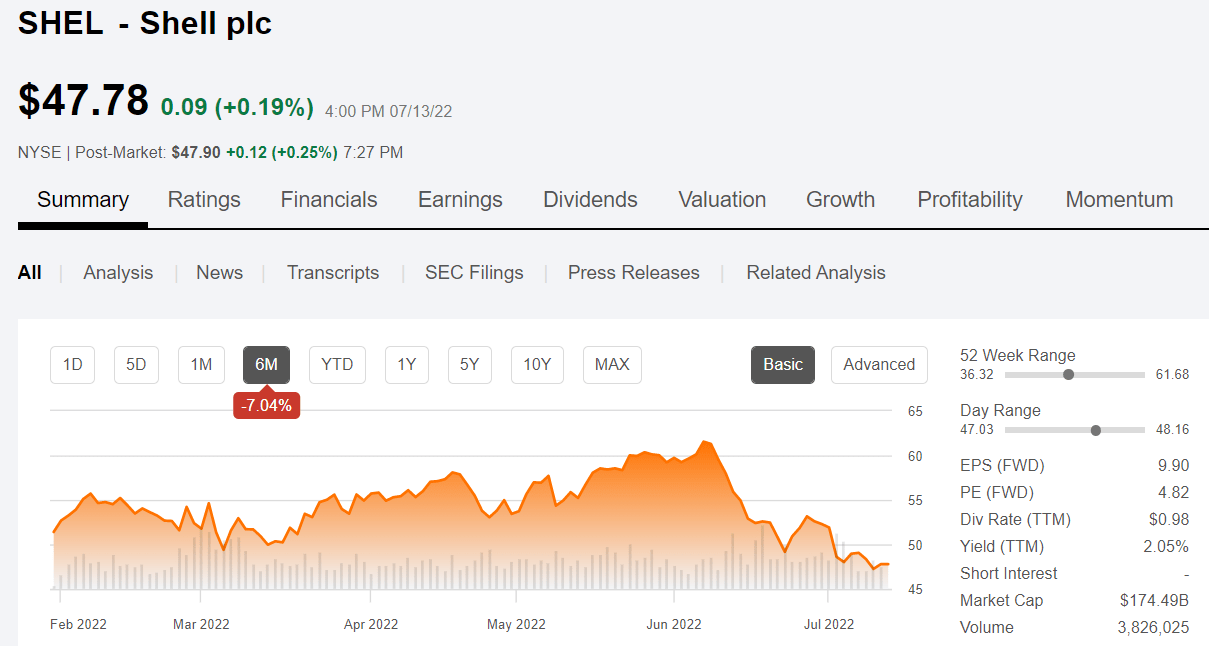

Shell plc (NYSE:SHEL, RYDAF) has been getting a lot of BUY ratings in Seeking Alpha articles recently. Enough that I was moved to take a peek under the hood to see if there was anything I was missing out on. I quit following Shell closely a couple of years ago, in favor of shale drillers that had a much stronger investment thesis. It’s been a rewarding decision. Then came the energy sell-off of late June.

The share price of Shell has dropped from the low $60’s to the upper $40’s, improving the usual multiples of OCF and P/FB. For that matter, the price of everything in the energy sector is down and, in many cases, substantially more than Shell, making me wonder at the Euro-giant’s resiliency.

Shell price chart (Seeking Alpha)

Does this swoon make Shell’s current price a bargain? Let’s face it, when we put new capital work in this sector, we want to be sure we are getting as much bang for our buck as we possibly can.

I wanted to see if I could find an investment thesis for this stalwart, British-domiciled, transitioning to clean energy, oil and gas company, that would enable me to hold my nose and pick up a few shares.

I won’t be coy, Shell will never be my favorite in the upstream energy space, as the title of this article reveals. They are far too invested in ESG nonsense, and throwing billions in capital at energy phantasms that may never bear fruit. I called this search “will o’ the wisp” (an elusive light in the forest that you can never reach) for a reason that should become clear as we look at Shell’s quest for H2.

That doesn’t mean they are uninvestable. At some point the risk/reward proposition becomes irresistible. Are we there yet?

I believe so. I think there is a strong case for investment at current prices and rate the company as a buy.

Please note, this article appeared in the Daily Drilling Report, last week on the 13th, in approximately its current form.

Rebelling against the clean energy “Will o’ The Wisp”

In some recent articles, I’ve made some fairly aggressive commentary regarding the “lemming-like” passion for the unproven “clean energy” – the kindest thing I can say, narrative that’s dominated the headlines for the last couple of decades. More truthfully in my view, this “The sky is falling” narrative has begun a rapid “decomposition” that’s left a bad taste in investors portfolios. Here are a couple of links if you missed them, as it would help you understand my deep skepticism of all things green. (Except for Kermit The Frog, that is.)

“Energy: Turn Out The Lights…”

“Jeff Currie On The Pillars Of Modern Life…”

The evidence mounts daily in support of the contentions I’ve put forward in the above articles. The International Energy Agency (“IEA”) laid out just yesterday a slate of actions Europe must take if it is to avoid a “major gas crunch” this winter. People continue to be shocked that the winds blow irregularly in the marine environment. People are shocked that onshore winds are just as fickle. People are shocked that solar farms don’t produce as much energy when its cloudy or at all at night, and will require vast tracts of land to deploy.

People are tired of being shocked by electricity brownouts. They are tired of pursuing the green energy “Will o’ the wisp,” with the endless and relentless government mandates. Indeed, President Biden may declare a “Climate Emergency” later this week. At the end of the day, people just want one thing: cheap, reliable power. It has been postulated that, when electricity service is lost for any length of time, people will burn a-n-y-t-h-i-n-g to get it back. This is known as the Iron Law of Electricity. Feel free to offer an exception to this law in comments.

In this context we now begin our examination of Shell’s determination to build out a hydrogen network, beginning in the EU – The Netherlands – and perhaps coming soon to a wind farm near you.

Shell and Clean Energy

Shell got a rude shock a year or so ago, with an edict from a Dutch court to do more in reducing its carbon footprint at a rate much faster than they had planned. Ouch. The good Shell upper management folks, who up to that time had been nearly breaking their arms patting themselves on the back with how green they were becoming, were nonplussed. It wasn’t long afterward they picked up their “toys” and removed themselves to a new sandbox in London and contested the court ruling.

I will avoid discussion of the intellectual consistency of going from one hotbed of carbon shaming, to another. Let’s just say, sometimes you just need a change of scenery, and they’d been in the Hague for what seemed a hundred years. I wrote this up in a fair amount of detail in an article last December. We have new ground to cover, so please give it a read for color on that topic.

We covered the lunacy of Shell’s commitment to wind power in the last article. This time around, we are going to focus on hydrogen. Of all the green initiatives that are gaining traction as we transition away from fossil fuels, hydrogen probably wins the prize for being the least practical and most poorly thought through in most cases. We are going to take a quick detour and put up a few bullets for you to keep in mind as we discuss Shell’s plan to develop hydrogen as a fuel.

The Problems with Hydrogen

This is a financial article, so we can’t go into too much detail on this complex topic. That said, there a couple of key points no one seems to discuss. Hydrogen is virtually useless as a motor fuel. A LinkedIn contact of mine who is an expert in hydrogen has an article for those who would like a longer discussion than I will provide here. I know there are pilot projects that have found funding – in the billions of dollars – that have no apparent likelihood of ever turning a profit. The linked WSJ article notes the wishful thinking that runs rampant in these projects. Most of these are the result of a very cozy government and private entity partnership that is underwritten by tax incentives. This is how government puts their preferences at the front of the line for capital. Government has a nearly perfect track record of wasting money, and this will prove to be no exception. Ultimately tears will be shed. Moving on.

I said hydrogen is virtually useless as a motor fuel, and only marginally useful in most other applications. What do I mean? It’s simple, really. In relation to the fuels it is displacing, hydrogen is the least dense. Hydrogen is the lightest element in the universe. By comparison, as the linked article notes, compression is the deal killer on H2.

Natural gas is about 8.5 times as dense as hydrogen, and dense gases are easier (more energy efficient) to move than less dense ones.

So, storage and transportation is a key issue for H2. And, on the shelf, solutions are few. Here’s an IEA paper detailing some of the problems impacting large scale adoption of H2 as a fuel. What this means, is it very mobile in nearly every substance. It can’t be used in existing pipelines as hydrogen embrittlement could cause them to fail. It is, after all, the elemental building block from which (thanks to nuclear fusion in stars) everything is made. Including us.

Ok, it’s hard to ship it. It’s hard to store it. Are there any other problems with H2?

Well how about this one. Paul Martin ties a bow on it neatly in his article (emphasis supplied):

it takes about three times as much energy to compress a MJ’s (megajoule)worth of heat energy if you supply it as hydrogen than if you supply it as natural gas.

This is related to the density of H2 and Newton’s Law of Energy Conservation kicks in. Compression is the deal killer.

In summary for this section. You can’t store it, ship it, or condense it economically. So other than ESG initiatives…why do it? Exactly. My friend, Paul calls much of what is being planned for H2, “Hopium.” A word you don’t run across everyday that implies irrational, or unwarranted optimism about an outcome. Great to have a word for it, ain’t it?

Back to Shell.

Shell and Hopium

Shell reached FID on the Holland Hydrogen project. Financial details were undisclosed. How often do we hear that? This is tied into the massive NortH2 project that we discussed in quite a bit detail last time around. In this phase, Shell is building out the electrolyzers that will take seawater (Surely. It isn’t explicitly stated but surely they wouldn’t destroy freshwater…would they? Of course not. Seawater it will be.), and produce the green hydrogen that will power the now being built, Shell Energy and Chemicals Park in Rotterdam. As noted in the Shell press release linked, this facility will produce biofuels, principally biodiesel:

The Rotterdam biofuels facility is expected to start production in 2024. It will produce low-carbon fuels such as renewable diesel from waste in the form of used cooking oil, waste animal fat and other industrial and agricultural residual products, using advanced technology developed by Shell.

There is quite a bit of hopium built into all of this hydrogen-happy talk. The first being the wind will blow consistently. The North Sea winds have been pretty fickle of late. One wonders if there is a backup power source? Next this project at 60K kilos of H2 is 10X the scale of the next largest plant of its type. Not surprisingly this mini-H2 plant is at the Shell Energy and Chemicals plant Rheinland, in Germany, and is being prepped for a massive scaleup. Whoohoo!

Closing out this section it should be noted that it is just going to rain Green H2 on Europe if all the projects I turned up in a search come to fruition.

- HyNetherlands A project just up the coast in Holland in Groningen, targeted to reach FID in 2023, with a similar design basis to the Shell project. First gas slated for 2025.

- Puertollano in Spain and led by Spanish utility Iberdrola. A mini-plant was just commissioned in May and is awaiting EU certification as an Important Project of Common European Interest. This will qualify it for funding from an EU green energy slush fund, and enable it to operate. Plans were immediately announced for it scale up to 100 MW following another 3 bn Euro investment. A Financial Times article wonders if the project will ever be economic at the estimated 6-7 Euro per kilo of H2 delivered.

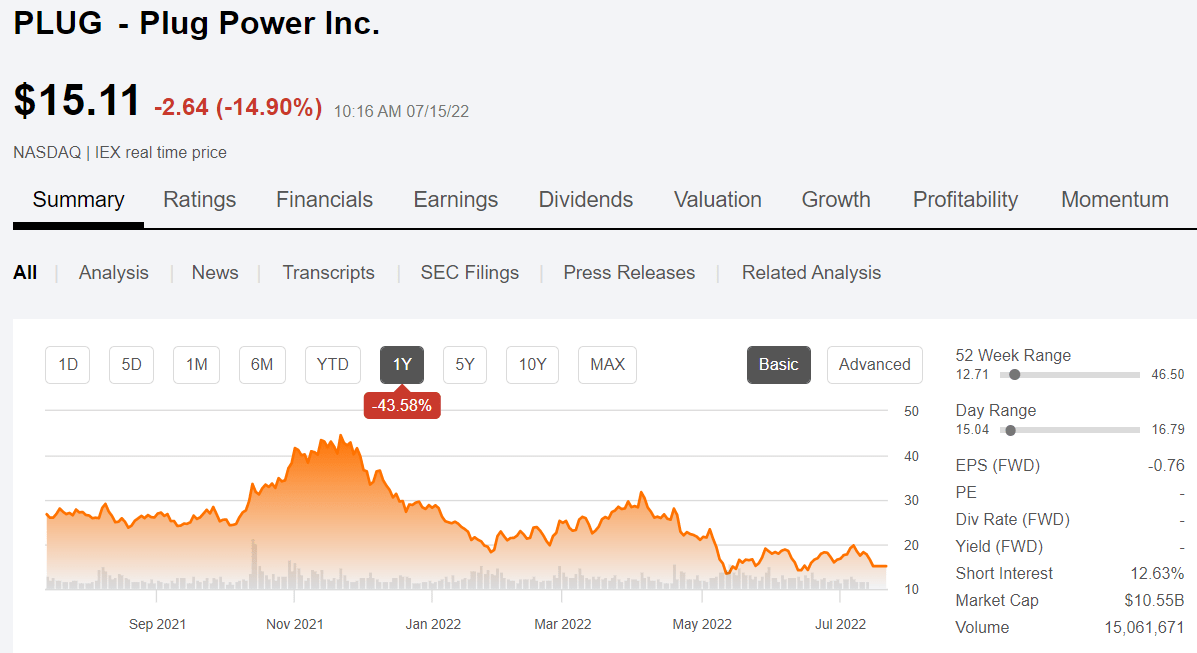

- Plug Power, (PLUG) a U.S. electrolyzer manufacturer plans 100 MW installation in the coastal Belgium city of Antwerp. A quick scan of this company doesn’t suggest any confidence their being able to pull off a multi-billion dollar project of this type. Entrants like PLUG suggest to me a “tulip-craze” mania descending upon H2.

Plugpower price chart (Seeking Alpha)

Assuming that all these projects and others get FID’d and come to fruition, there will be a lot of competition in this space. As with any nascent industry there will be implosions along the way. I see no reason for Shell to be a survivor. They have no moat, no technological, logistical or commercial advantage and will be price takers in this market. If it turns out they are unprofitable, shareholders will feel the pain.

While Shell has nothing else on the scale of the NortH2 project on the drawing board, there are about 20+ projects underway globally, including a future hydrogen hub in Australia. Partnering with Aussie company Bluescope, a steel manufacturer Shell has signed an MOU to develop hydrogen projects in eastern Australia.

I will close this section out by saying that with the exceptions I’ve pointed out, much of the technology applied here exists and is functioning in various applications. What’s new is this obsession to produce H2 for the sake of producing H2. It is the very definition of hopium. Hoping that interlacing technologies will mesh, that markets will be robust enough to deliver profits is new territory without demonstrable analogs in operation. Billions are being spent in the hope of an eventual return. If you’re an investor in Shell, it’s your money and you have no clue when a return will be generated on the investments. The truth is they don’t either. Now we’ll lighten up a bit.

LNG: The core thesis for Shell other than clean energy

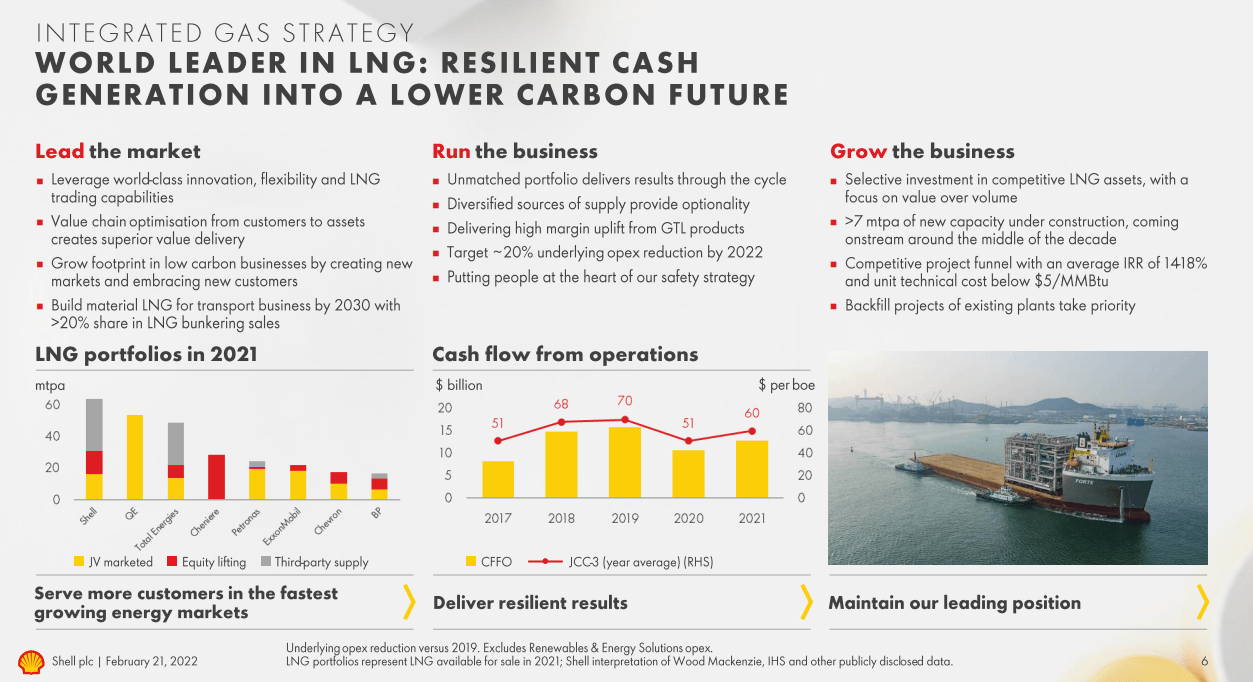

The Shell we knew and loved was one of the premiere oil exploration and producing, refining, and chemical derivatives companies globally. Those legacy investments still form the basis for investing in the company, and for the present are thriving. Particularly LNG.

Shell is a world leader in natural gas and LNG. This thanks to its purchase of British gas a few years back. Recent moves in Qatar, buying into the $29 bn North Field East project, and in Norway with the approval of the Ormen Lange gas field, enhance this leadership position in this increasingly import resource. Its Australian Prelude FLNG, capable of shipping 5.3 MT of LNG and condensate, is shipping cargoes again.

Shell LNG portfolio (Shell)

Shell has a robust outlook for LNG in 2022 and beyond. Energy analyst firm Rystad, concurs with this outlook with a grim forecast for winter of 2022, and a shortfall of 150 mmpta through 2030. The upshot is recent growth should be maintained for years to come, providing a key source of revenues and profits for the company.

Other businesses

It’s putting a new project into the GoM. Vito will be commissioned later this year and deliver up to 100k BOPD starting in 2023. Powernap, a satellite subsea tie-back, is delivering 20K BOPD to the Olympus hub. Shell is the leading GoM operator with 8-producing platforms/hubs and 476K BOPD barrels a day of production. Earlier this year, it acquired Equinor’s (EQNR) interest in the Sparta deepwater project, which is progressing toward sanction.

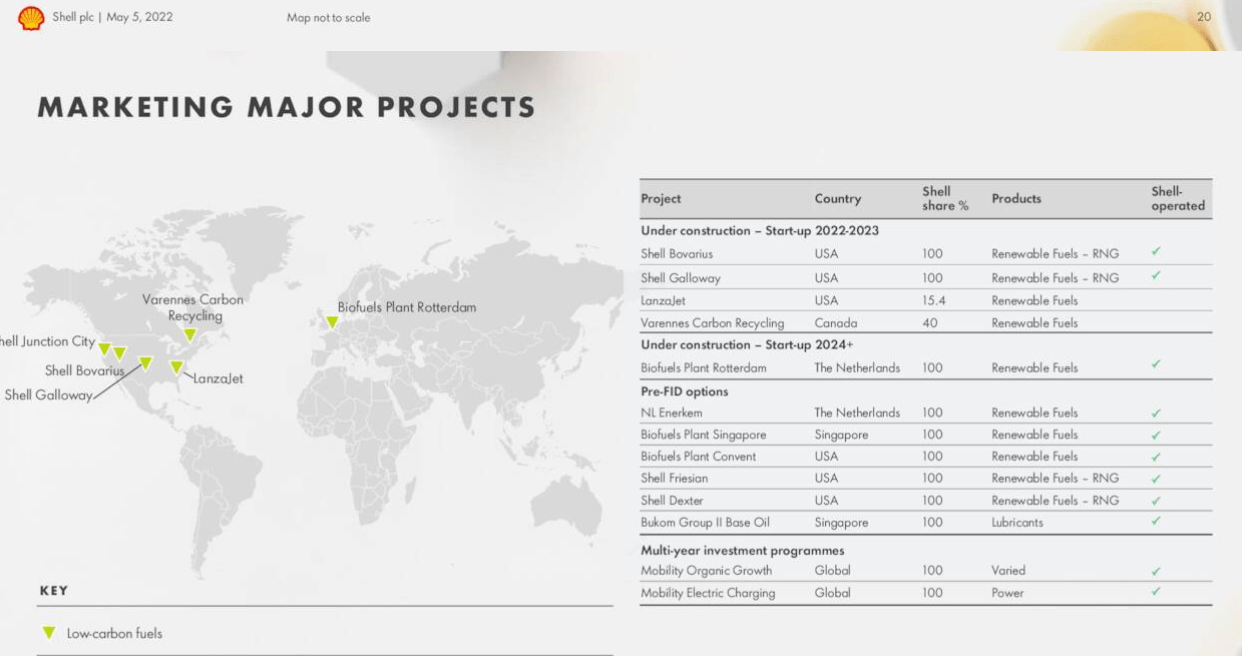

Shell has largely exiting petroleum refining globally, but has expansion plans for its emerging biodiesel business. I am on record as saying this is a business that makes sense, as the feedstock can be manipulated from vegetable oils to animal fats, and the output is tax favored. It’s also a viable product for reducing the carbon footprint of aviation fuels, delivering a hi-BTU product similar to kerosene in functionality. This will be a winner for Shell.

Shell Global projects (Shell)

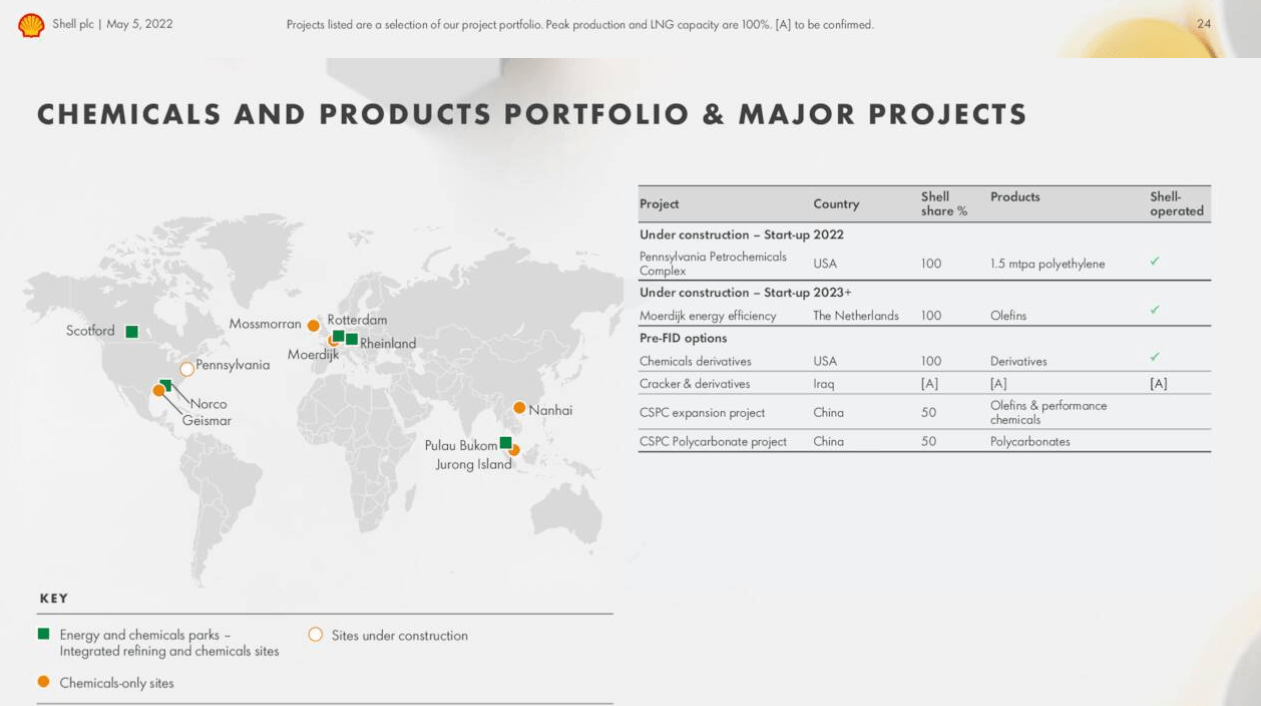

Shell is also a key player globally in the petrochemicals space with ethylenes, olefins, resins, and lubricants being advantaged by its position in gas and condensates. Shell Norco and Deer Park are huge installations delivering millions of pounds of these materials annually.

Shell Chemicals Portfolio (Shell)

Shell continues to have robust daily output of oil and gas at 3,367 BOEPD for 2021. This has been on the decline the last several years along with its proved reserves, some of which is due to key asset sales. In 2021 Shell divested its Permian properties to ConocoPhillips (COP) taking about 200K BOEPD off the books. This is by design to help meet the climate imperatives laid down by the Dutch court, and targeting a 45% reduction in carbon emission by 2030. Much of this will occur in the growth of their LNG and biofuels business.

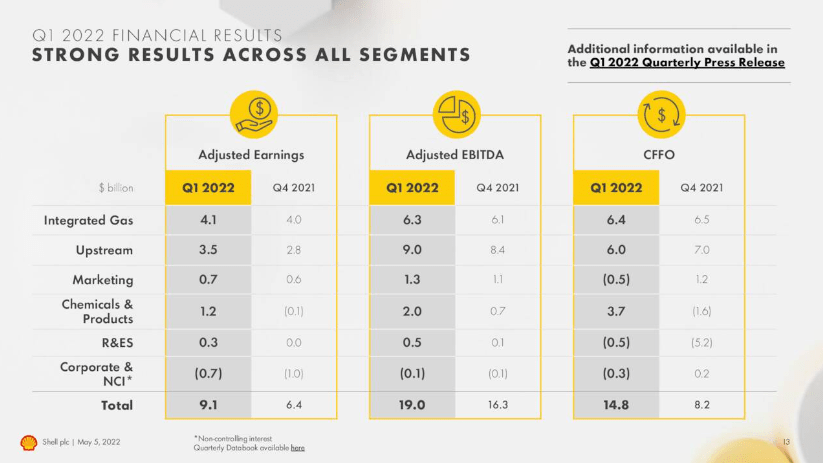

Q-1, 2022

Shell took in $14.8 bn in OCF for Q-1, or $58 bn on a one year run rate basis. Capex ran to $4.2 bn, dividends cost another $1.9 bn, and ~$2.5 bn in debt was repaid. This left them with $6.2 bn to throw a share buyback party, and that’s just what they did to the tune of $4.5. They expect another $4.0 bn of buybacks for the 2nd Qtr. Cash on hand rose by roughly the balance to ~$38 bn. Over the last year and a half the company has strengthened the balance sheet knocking $14 bn off the total, which now stands at $52 bn. A non-cash charge of $3.9 bn was taken for Russian asset divestitures.

Shell results chart (Shell)

Risks

Other than the obvious oil price risk, Shell is one of the companies that has a target painted on it from governmental agencies and environmental groups around the world.

There is also the risk the capital they are expending in pursuit of the H2 “willow the wisp” will never see a return leading to billions in eventual write downs. That is just risk a present investor needs to keep in mind, and we will discuss how best to mitigate that risk in the next section.

Your takeaway

At its current June Swoon downdraft induced price of $47ish Shell is trading at an absurdly low cash flow multiple. I peg it at ~2.9X. Exxon Mobil, (XOM) is trading at 6.3X OCF and Chevron, (CVX) is at 8.9X.

The P/FB is $47,000 per barrel, which is at significant discount to Brent. CVX trades at $98,000 per barrel and XOM logs in at $100K per barrel. As a final check, French energy giant TotalEnergies (TTE) trades at 5.6X OCF, and at $60K per flowing barrel.

Analysts are high on Shell with 25 of the 30 covering the company rating it a BUY. Price targets range from $60 on the low side to $88 on the high side. I think we can agree that Shell doesn’t deserve a OCF multiple at its current level. If we give TTE’s OCF multiple to Shell, the stock price would hit the mid $80’s, right in line with the upper analyst estimates.

Because of the comparisons to competitors, and the strength of their LNG position, I have to give Shell a buy rating at its current price. It’s a no-brainer really. The concerns I have about the hydrogen boondoggle will take a decade to play out, if I am right. If I am wrong then the cash flow and revenue from these investments will begin to fill in the gaps from declining oil and gas sales.

Recently the company has reduced the share count by ~150 mm shares. That’s not a lot when you consider their float of ~7.7 bn shares, but it is significant nonetheless. It has also made comments about improving shareholder returns to make the stock more attractive to investors. Shell CEO, Ben van Beurden, made the following commentary in this regard:

We have to look after our shareholders because I think our shares are very significantly underpriced, and therefore giving back more to shareholders to help that part of the equation is going to be very important” van Beurden told Reuters

A refreshing outlook from that voiced a couple of years ago. Shell has a history of paying a very attractive dividend in the 3.5-4% range. At current prices it’s only 2%, so I would think investors could expect a sizeable bump soon.

If investors accept my thesis, supported by many analysts, that oil prices will stay in the $100 range for the foreseeable future thanks to tightness of supply, then Shell is bargain-basement priced and should be bought for growth and modest income.

This is not to say I would park cash – as I once did – in Shell and forget about it. Those days are over. If the shares were to revert to a higher level as I suspect they soon will, I would probably cash out and look for other opportunities.

Be the first to comment