Editor’s note: Seeking Alpha is proud to welcome Bayley Capital as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Magone/iStock via Getty Images

At a current price of ~£1.35, I believe Hotel Chocolat Group (OTCPK:HCHOF) represents an attractive opportunity to enter the beleaguered retail sector of the stock market at historically low valuations. Hotel Chocolat has been one of the most punished names in the UK retail sector, even though the company is debt-free with cash on the balance sheet and is generating record levels of EBITDA. One of the leading premium chocolate brands in the UK, the company has significant growth opportunities ahead and should return to bottom-line profitability by FY24.

Hotel Chocolat came across my radar on July 19, when the share price dropped 45% in response to the company’s announcement that it was expecting to report an IFRS net loss for the year ending June 30, 2022. The loss will come as a result of a strategic review that has led the board to decide to exit the Japanese and U.S. markets, and thus will be recording an impairment charge against the full value of the working capital loan it extended to its Japanese joint venture partner, Hotel Chocolat KK. The share price is down 73% from £5.20 year to date.

Given the dramatic market overreaction, I see an opportunity here to purchase the common stock. I anticipate the market to gain some sense over the next 12-24 months and revalue the common shares to a price 2x greater than currently seen: ~£3, a return of >100% on invested capital, with limited downside exposure.

Investment highlights

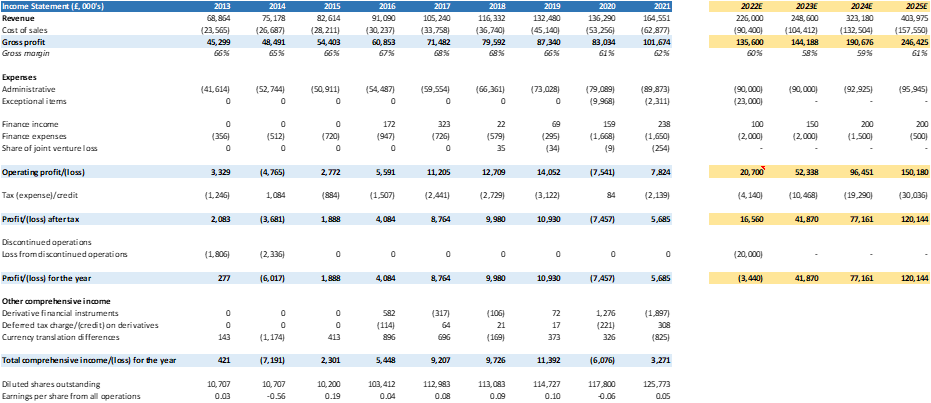

The company is trading at a record low valuation with a LTM EV/EBITDA of ~11x, even though the company is expected to report record revenues of £226mm for the financial year ended June 30, 2022, and record EBITDA of ~£40mm with gross margins of ~60%. The current market valuation implies the company will only achieve £8mm of EBITDA for 2022.

Furthermore, Hotel Chocolat is founder controlled and operated. Angus Thirlwell, the CEO, and Peter Harris, the development director, founded the company together in 1993. They each own 37mm shares each, or 27% of the outstanding shares on issue, for a total of 54%. At a share price of £1.35, their share parcels are valued at £58mm each. With such large financial interests in the company, I believe Thirlwell and Harris will run the company to the benefit of shareholders. The value of their shareholding in November 2021 when the shares reached an all-time high of £5.40 was a whopping £200mm. If anyone is feeling the pinch of the current market rout, it’s them.

Since listing on the AIM market in May 2016, the company has increased manufacturing capacity at its Cambridgeshire factory. Capacity is currently sitting at £250mm, with the option to further double this to £500mm beyond FY23. The latter expansion would be funded via operating cashflows. Furthermore, the company has recently signed a 10-year lease on a second distribution center in Northampton.

Key performance indicators have been trending strongly. Members of the company’s VIP loyalty card program, launched in the first half of 2019, are now sitting at 2.3mm users. These customers now account for 71% of UK direct-to-consumer sales. Loyalty programs encourage brand “stickiness” and enhance customer lifetime value significantly.

Hotel Chocolat is not short on growth opportunities. The directors have expressed their intention to focus on the company’s core UK market and wrap up operations overseas. Overseas operations were hardly ever material, producing only 3% of the company’s total revenue in FY21. Hotel Chocolat operates across three market segments with a total addressable market of between £20 and £30 billion: gifting, chocolate, and out-of-home leisure. The recently launched Velvetiser – a home hot chocolate machine – along with the company’s new range of liqueur and alcohol are opening up further avenues of growth.

Company overview

The company is a vertically integrated premium chocolate producer, manufacturing their range of chocolate products from their factory based in Huntingdon, Cambridge. They also produce a small quantity of their own cocoa on their 140-acre cocoa plantation in St Lucia, where they also happen to run a boutique 14-room hotel. Hotel Chocolat is the only independent premium chocolate company listed on the London stock exchange. They sell their products via a network of 96 stores in the UK, with 70% of their sales coming from their website.

The company has a long-standing operating history, beginning as a branded mint producer, the type a business would go to if they wanted branded pens. However, Thirlwell and Harris decided to focus on mints. Next, they focused on chocolate products under the name “Geneva Chocolates” and pursued the catalogue-based market. Finally, in 2004 they rebranded as Hotel Chocolat and launched their first retail store.

Admitted to the AIM market of the London Stock Exchange on May 10, 2016, the company has grown from revenues of £68mm in FY16 to revenues of £226mm in FY21, a compound annual growth rate of 14%. Over the same period, book equity has grown from £6mm to £72mm, or 31% per annum.

Hotel Chocolat financial forecast (Bayley Capital)

Why is the valuation so low?

There is no doubt the wider stock market has entered bear market territory in 2022. The tech-heavy Nasdaq is down 18%, while the S&P 500 is down 11%. The retail sector is bearing the brunt of the impact as the sector is generally the first that comes to mind when investors think about who will bear the consequences of an economic rout. Inflation prints are the highest on record across the globe in decades as economies wake up from the COVID-19 nightmare to major supply chain congestion, compounded by massive amounts of liquidity floating around from government handouts and stimulus checks during the pandemic.

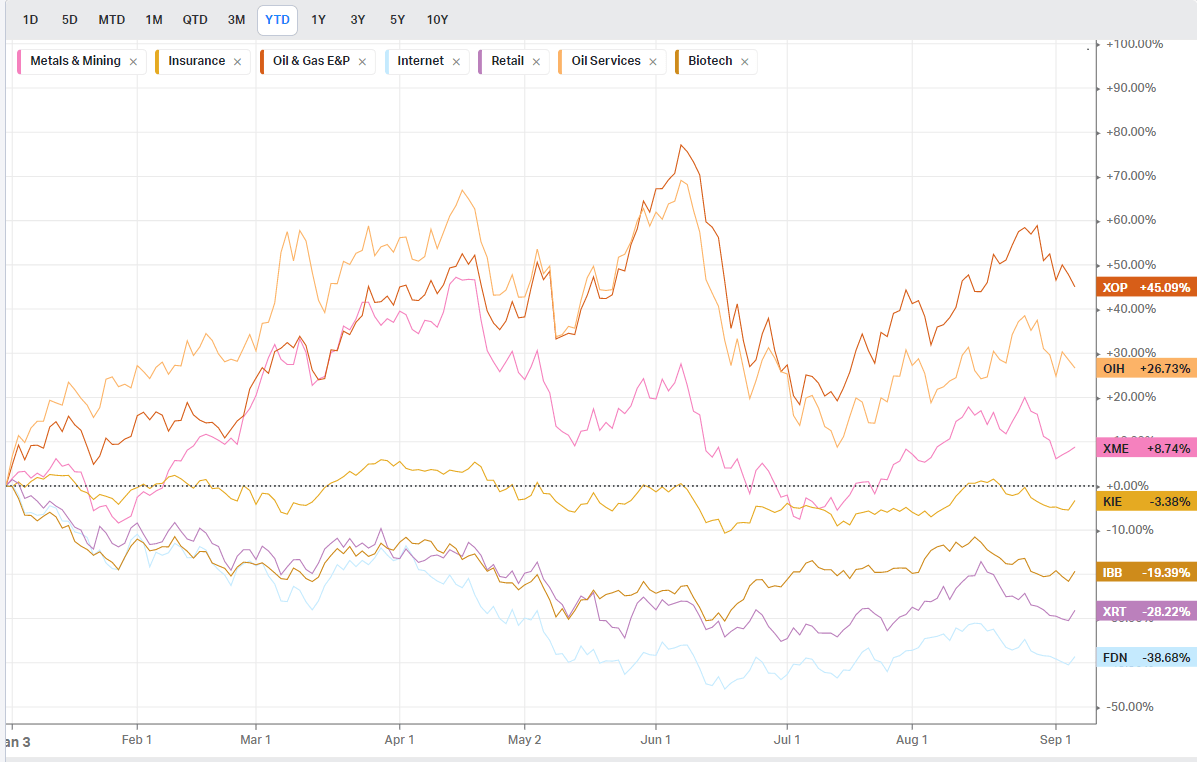

The SPDR S&P Retail ETF (XRT), a good proxy for retail sector stock performance in the U.S., is down 28% year to date – the third-worst performing sector in the market. As is typical when Mr. Market throws the baby out with the bathwater, smaller capitalization – along with higher leveraged stocks – are impacted the most. Case in point: We are presented with the opportunity that is Hotel Chocolat.

XRT etf year-to-date performance (Koyfin.com)

Hotel Chocolat entered the Japanese market during FY18 through a 20% shareholding in the joint venture Hotel Chocolat KK. In the preliminary full year FY22 update announced to the market on July 19, the company stated that it was exiting the Japanese market and thus may record an impairment charge against some or all of the £23mm in working capital loans made to Hotel Chocolat KK over the course of their involvement. Furthermore, on July 28 the company announced that Hotel Chocolat KK gained Japanese court approval to enter into formal restructuring, known as civil rehabilitation in Japan.

The company has been pursuing the Japanese and American markets as an avenue for growth over the past few years. However, they have always adhered to the mantra that entering overseas markets is a strategy that should be pursued slowly and carefully. As such, capital investment in each jurisdiction has been modest, which is further reflected by the small revenue contribution these operations have made to total group revenues – 3% in FY21. Again, a 45% drop on the announcement that these operations were not successful seems like an overreaction.

COVID-19 most certainly prevented these markets from building any momentum. The Japanese operations experienced three consecutive peak Valentine’s Day and White Day trade periods that were severely impacted by COVID-related restrictions. During FY21, the joint venture opened 16 stores, bringing the total to 22. Expanding the brick-and-mortar retail frontage by 370% during a year of COVID-19 restrictions was clearly not the best strategy. Opening physical stores was probably the right long-term strategy for Japan, given the high population density and proliferation of retail malls. However, unfortunately, the timing could not have been worse.

The American operations were always largely focused on online and wholesale, with the company only opening four retail stores. Operating via a fulfillment partnership with The Hut Group, the company was able to maintain a capex-light operating model while retaining control over the brand, customer base, and strategy. However, a meaningful foothold in the market was never really obtained. Once the last physical retail store in America is closed, the company’s focus will be solely on online and wholesale operations.

Company expectations for FY23

The company is expecting operating headwinds to continue through FY23, eventually returning to revenue and profitability growth in FY24. In the July trading update, along with outlining the new strategy of focusing on their core UK market and profitable business segments, the company outlined its expectations regarding the impact of this adjustment and macro headwinds will have on operating performance.

Investment to support the brand will continue

Key to the brand is the further growth of the Gentle Farming program, whereby Hotel Chocolat’s farmers are paid a living wage. Management is also committed to paying a living wage in the UK. Management anticipates these measures will result in a 3% permanent increase to operating costs.

Management aims to increase unit margins by reducing unit costs

With the signing of a 10-year lease on the second distribution center in Northampton, operational in the first half of 2023, the company is aiming to increase unit margins by reducing unit costs. However, this will come with a 3% increase in operating costs in FY23 as the center comes online and “teething troubles” are worked through. The distribution center is complimentary to the company’s option to increase manufacturing capacity to £500mm post-FY23.

Enhanced procurement should reduce external inflation headwinds

Operating costs will increase by 3% as a result of external inflation. However, management believes it can mitigate these cost increases through better procurement and improved production efficiency, driving unit costs down.

The above headwinds total an increase in operating costs for FY23 of 9%, or £10mm based on my estimate of FY22 administrative costs of £90mm (see forecast above). However, management has outlined mitigating steps that they believe will reduce the impact of the above by 3% or £3mm on my FY22 numbers, bringing the net impact of the tailwinds down to £7mm. These include a focus on marketing to current customers – which is lower cost vs. new customer marketing – an increased mix of full-price sales and lower discounting, improved production efficiency and procurement, and scale economies through the increased manufacturing capacity.

FY23 will be a year of adaption, which should lead to a stronger business with lower operating costs and higher margins over the medium to long term. It’s better to clean out the closet during the “bad” times than the good. The market is not ascribing any value to management astuteness in carrying out manufacturing capacity improvements and further optimization of the business model. These changes should be highly value accretive to the long-term value of the business.

At current valuations, the market seems to be implying the company will be in loss-making territory for FY23, which is almost certainly not going to be the case. FY22 will deliver circa £40mm in EBITDA, with FY23 either in line or moderately higher. Depreciation and amortization will largely be in line with FY22, slightly higher than prior years due to the investment in the factory. Interest expense should largely be in line with prior years or even lower as they intermittently draw on their £50mm overdraft facility. Furthermore, I would not anticipate any non-cash impairment charges given that the impairment to the Japan JV will likely be taken in FY22.

Valuation

At a share price of £1.35 with 137mm shares outstanding, Hotel Chocolat has a diluted market capitalization of £185mm. Deducting the cash balance of £17mm as reported to the market on July 19, the enterprise value of the company is sitting at £168mm. In November, when the shares reached an all-time high of £5.40, the market capitalization reached £740mm or an enterprise value of ~£700mm.

Based on the current enterprise value, Hotel Chocolat is trading at an EV/EBITDA multiple of 11x on an LTM (last 12 months) basis. This is compared to a five-year average for the company of 23x. Based on FY22E numbers, if the market was valuing Hotel Chocolat at 23x EBITDA, the enterprise value would be £1 billion, or £7.30 per share, a mere 440% higher than the current price.

Looking at peer analysis on the LSE, although there are no perfect competitors for this exercise, I have taken the next best option – the food products sector peer group. As you can see from my analysis, Hotel Chocolat maintains the highest return on equity of the group yet sits in equal second place, with M.P. Evans with an NTM EV/EBITDA of 4x. Consider that Hotel Chocolat is also only one of two among the group with a net cash position, alongside Anglo Eastern. I don’t recommend valuing a company based on peer or industry valuations entirely, although the practice can help put large market valuation discrepancies into perspective.

Peer analysis (Bayley Capital)

What is interesting to note further is that the company is likely reaching an inflection point with their free cash flow generation. With the expansion of the Cambridgeshire factory during FY21 and FY22, the company will not be investing as heavily into the factory during FY23. They have stated they maintain the option of expanding the factory further post-FY23; however, this will be funded via operating cash flows. My expectations – and clearly management’s expectations as well – are that the operating cash flows generated from the increased manufacturing capability will cover the potential cash required for the expansion to £500mm of capacity. This was not the case with the initial expansion, where the company raised £40mm in fresh equity in July 2021 to carry out the upgrades.

Ultimately, I think one can deduce that the company has been well run so far. Thirlwell and the wider management team have been good stewards in driving 13% annual revenue and EBITDA growth over the past nine years, while also growing equity at 31% per annum and levered free cash flow at 23%. In terms of looking after shareholder capital, the above performance is indicative of careful and accretive capital allocation. The investment in manufacturing capacity has clearly been a successful enabler of growth. An investment of £40mm of shareholder capital to increase capacity from £150mm to £250mm over FY22 has allowed revenue growth of 37% from £164mm in FY21 to £226mm in FY22. More impressive is the growth in EBITDA jumping from £16mm in FY21 to £40mm in FY22. The EBITDA figures represent a 60% return on the £40mm investment and the £40mm will be completely repaid in less than two years.

On this basis, I don’t believe it’s a stretch to conclude that Hotel Chocolat should command a premium valuation multiple. I anticipate my one-year price target of £3 to be conservative with the hope that the market will rerate the stock to a more deserving multiple in the region of 20x EBITDA. For illustrative purposes, if the strategy realignment is worked through and the company can refocus attention toward growth by FY24, a 20x multiple on estimated FY24 EBITDA of £60mm plus net cash of £50mm would result in an enterprise value of £1.20 billion, or a share price of £9.

Risks

The key risks I see, along with mitigants, that might prevent an upward move in the share price or push the price further down are as follows:

Poor cost management during FY23

Given the company has already announced its performance expectations for FY23, if actual results turn out to be worse, the stock will likely be punished heavily. Given the prudent way management has conducted themselves over the course of being a listed company, I doubt they would shock the market with worse-than-expected results. Regardless, if operations are not going as smoothly as expected, I would anticipate management would forewarn the market.

Failure of the Velvetiser

Management has been clear that the Velvetiser is one of the key growth avenues for the company. The market has made it clear that it has high expectations of growth, so any further announcements that growth might not be what they expected or there’s a reduction in the total addressable market would not be good for the share price.

Conclusion

As I have mentioned, at the current implied valuation the market is suggesting that Hotel Chocolat will cease to generate profits and cease to grow. As I have shown, what I believe is more likely to happen is that the company will face some headwinds in FY23 as it transitions its business to be more profitable. The 45% drop in price on the news of the company’s FY23 expectations says to me that any FY23 headwinds have already been priced into the stock. Therefore, performance in line with these expectations or better should result in a higher share price.

Furthermore, although not key to my investment thesis, any improvement in the macroeconomic outlook for the UK will likely have a significant positive impact on the value of Hotel Chocolat. Coupled with strong fundamentals and a basement floor valuation, I believe Hotel Chocolat is primed to appreciate in value in the coming years.

Be the first to comment