relif

Earnings of ServisFirst Bancshares, Inc. (NYSE:SFBS) will benefit from double-digit loan growth through the end of 2023. Further, the margin will slightly expand amid the rising rate environment, which will further support the bottom line. Overall, I’m expecting ServisFirst Bancshares to report earnings of $4.52 per share for 2022, up 19% year-over-year. For 2023, I’m expecting earnings to grow by a further 14% to $5.16 per share. Next year’s target price suggests a small upside from the current market price. Based on the total expected return, I’m maintaining a hold rating on ServisFirst Bancshares.

Margin Expansion to Continue, Albeit at a Lower Rate

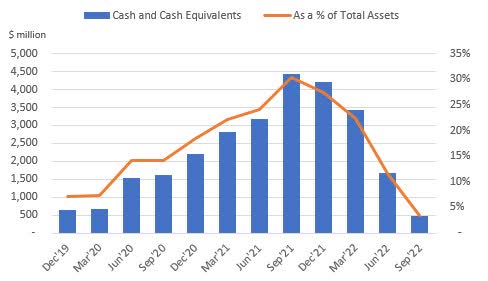

ServisFirst Bancshares’ margin expanded by 38 basis points in the third quarter, following the 37 basis points hike in the second quarter of 2022. This expansion was attributable to both the rising rate environment and the deployment of excess cash into higher-yielding assets. The cash level is almost back to normal (see below); therefore, this factor will not provide further benefit to the margin going forward.

SEC Filings

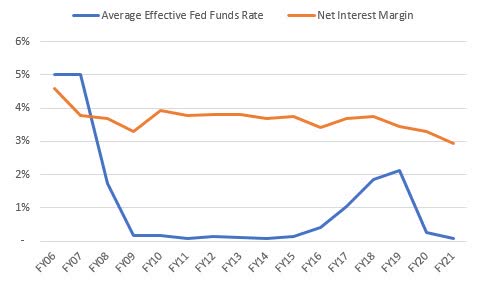

However, the ongoing up-rate cycle will continue to boost the margin through 2023. As fixed-rate residential mortgage loans make up a majority of total loans, the average earning-asset yield is only moderately rate-sensitive. The margin’s historical trend also shows that it has been only loosely correlated to interest rate changes in the past.

SEC Filings, The Federal Reserve Bank of St. Louis

Considering these factors, I’m expecting the margin to grow by 10 basis points in the last quarter of 2022 and a further 10 basis points in the full-year 2023.

Loan Growth to Decelerate but Remain in Double-Digit Range

ServisFirst Bancshares’ loan portfolio grew by a remarkable 6.2% in the third quarter (25% annualized) which was above my expectations. The management expects loan growth to moderate in the coming quarters as the pipelines are lower than before, according to details given in the conference call. Further, the management mentioned that it will be more selective about accepting loan applications going forward.

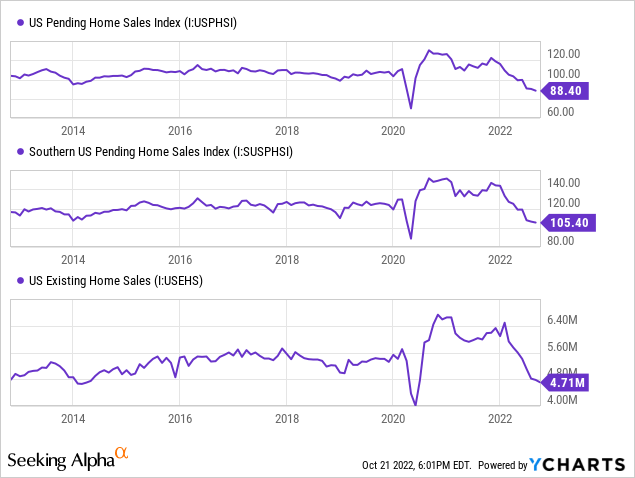

Moreover, high borrowing costs will dampen credit demand, especially for residential mortgage loans which make up almost 60% of total loans. Home sales in the country have been on a downtrend for most of this year, as shown below. The up-rate cycle is far from over; therefore, further pressure is expected on loan growth in the coming quarters.

On the other hand, growth in human resources will support loans. ServisFirst Bancshares continued expanding its team during the third quarter of 2022. As mentioned in the conference call, the company added 13 new bankers during the quarter after adding 15 bankers in the second quarter of 2022.

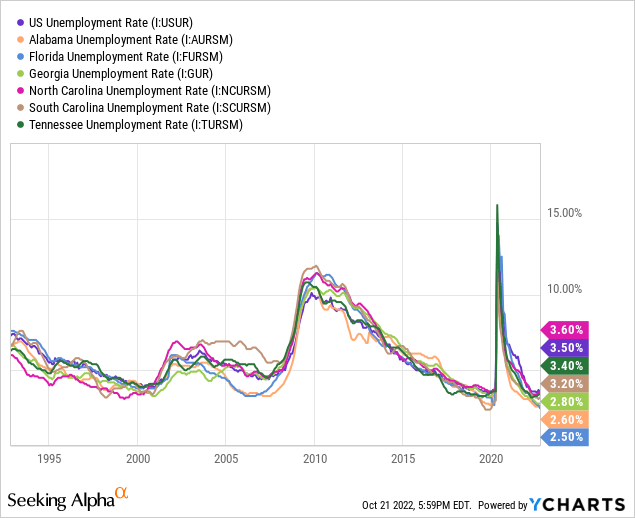

Strong job markets in ServisFirst Bancshares’ operating regions will further support loan growth going forward. The company operates in southern states, namely Alabama, Florida, Georgia, North Carolina, South Carolina, and Tennessee. Except for North Carolina, all of these states currently have better unemployment rates than the national average.

Considering the factors given above, I’m expecting the loan book to grow by 2.75% every quarter till the end of 2023. Meanwhile, I’m expecting other balance sheet items to grow somewhat in line with loans. The following table shows my balance sheet estimates.

| FY18 | FY19 | FY20 | FY21 | FY22E | FY23E | |

| Financial Position | ||||||

| Net Loans | 6,465 | 7,185 | 8,378 | 9,416 | 11,444 | 12,756 |

| Growth of Net Loans | 11.6% | 11.1% | 16.6% | 12.4% | 21.5% | 11.5% |

| Other Earning Assets | 1,176 | 1,217 | 3,017 | 5,479 | 1,919 | 2,077 |

| Deposits | 6,916 | 7,530 | 9,976 | 12,453 | 11,356 | 12,657 |

| Borrowings and Sub-Debt | 353 | 535 | 916 | 1,776 | 1,562 | 1,691 |

| Common equity | 715 | 842 | 992 | 1,152 | 1,292 | 1,517 |

| Book Value Per Share ($) | 13.2 | 15.6 | 18.3 | 21.1 | 23.7 | 27.8 |

| Tangible BVPS ($) | 12.9 | 15.3 | 18.0 | 20.9 | 23.4 | 27.6 |

| Source: SEC Filings, Earnings Releases, Author’s Estimates(In USD millions unless otherwise specified) | ||||||

Excessive Reserves to Keep Provisioning at a Normal Level

ServisFirst Bancshares’ reserves for loan losses appear excessive considering the portfolio’s credit risk. The allowances-to-nonaccrual-loan ratio stood at 1209.5% at the end of September 2022 compared to 1191.36% at the end of September 2021, as mentioned in the earnings release. As ServisFirst normally prefers a high reserve level, I’m not expecting any out-of-the-ordinary reserve releases in the coming quarters. Meanwhile, high borrowing costs and inflation will worsen asset quality, but as the reserve level is excessive, it will easily cover the quality deterioration.

Overall, I’m expecting the net provision expense to make up around 0.38% of average loans every quarter (annualized) till the end of 2023, which is the same as the average for the last five years.

Expecting Earnings to Grow by 19%

Future earnings will benefit from double-digit loan growth and slight margin expansion. On the other hand, strong growth in salary expenses due to high inflation will restrict earnings growth. Meanwhile, the provisioning for expected loan losses will likely remain at a normal level.

Overall, I’m expecting ServisFirst Bancshares to report earnings of $4.52 per share for 2022, up 19% year-over-year. For 2023, I’m expecting earnings to grow by 14% to $5.16 per share. The following table shows my income statement estimates.

| FY18 | FY19 | FY20 | FY21 | FY22E | FY23E | |

| Income Statement | ||||||

| Net interest income | 263 | 288 | 338 | 385 | 479 | 565 |

| Provision for loan losses | 21 | 23 | 42 | 32 | 42 | 48 |

| Non-interest income | 19 | 24 | 30 | 33 | 35 | 36 |

| Non-interest expense | 92 | 102 | 112 | 133 | 164 | 201 |

| Net income – Common Sh. | 137 | 149 | 170 | 208 | 247 | 282 |

| EPS – Diluted ($) | 2.53 | 2.76 | 3.13 | 3.82 | 4.52 | 5.16 |

| Source: SEC Filings, Earnings Releases, Author’s Estimates (In USD millions unless otherwise specified) | ||||||

In my last report as well, I estimated earnings of $4.52 per share for 2022. I have tweaked all my income statement line item estimates following the third quarter’s results. As the immaterial changes cancel each other out, my updated earnings estimate is almost the same as the earnings estimate given in my last report on the company.

Actual earnings may differ materially from estimates because of the risks and uncertainties related to inflation, and consequently the timing and magnitude of interest rate hikes. Further, a stronger or longer-than-anticipated recession can increase the provisioning for expected loan losses beyond my estimates.

Maintaining a Hold Rating

ServisFirst Bancshares has a long-standing tradition of increasing its dividend in the last quarter of the year. Given the earnings outlook, I’m expecting the company to increase its dividend by $0.02 per share to $0.25 per share in the fourth quarter of 2022, and then by another $0.02 per share in the fourth quarter of 2023. The earnings and dividend estimates suggest a payout ratio of 20% for 2023, which is in line with the five-year average. Based on my dividend estimate, ServisFirst Bancshares is offering a forward dividend yield of 1.4%.

I’m using the historical price-to-tangible book (“P/TB”) and price-to-earnings (“P/E”) multiples to value ServisFirst. The stock has traded at an average P/TB ratio of 2.74 in the past, as shown below.

| FY18 | FY19 | FY20 | FY21 | Average | ||

| T. Book Value per Share ($) | 12.9 | 15.3 | 18.0 | 18.7 | ||

| Average Market Price ($) | 40.8 | 33.9 | 35.7 | 67.4 | ||

| Historical P/TB | 3.16x | 2.21x | 1.98x | 3.61x | 2.74x | |

| Source: Company Financials, Yahoo Finance, Author’s Estimates | ||||||

Multiplying the average P/TB multiple with the forecast tangible book value per share of $27.6 gives a target price of $75.5 for the end of 2022. This price target implies a 7.4% upside from the October 21 closing price. The following table shows the sensitivity of the target price to the P/TB ratio.

| P/TB Multiple | 2.54x | 2.64x | 2.74x | 2.84x | 2.94x |

| TBVPS – Dec 2023 ($) | 27.6 | 27.6 | 27.6 | 27.6 | 27.6 |

| Target Price ($) | 70.0 | 72.7 | 75.5 | 78.2 | 81.0 |

| Market Price ($) | 70.3 | 70.3 | 70.3 | 70.3 | 70.3 |

| Upside/(Downside) | (0.4)% | 3.5% | 7.4% | 11.3% | 15.3% |

| Source: Author’s Estimates |

The stock has traded at an average P/E ratio of around 14.4x in the past, as shown below.

| FY18 | FY19 | FY20 | FY21 | Average | ||

| Earnings per Share ($) | 2.53 | 2.76 | 3.13 | 3.82 | ||

| Average Market Price ($) | 40.8 | 33.9 | 35.7 | 67.4 | ||

| Historical P/E | 16.1x | 12.3x | 11.4x | 17.7x | 14.4x | |

| Source: Company Financials, Yahoo Finance, Author’s Estimates | ||||||

Multiplying the average P/E multiple with the forecast earnings per share of $5.16 gives a target price of $74.2 for the end of 2022. This price target implies a 5.6% upside from the October 21 closing price. The following table shows the sensitivity of the target price to the P/E ratio.

| P/E Multiple | 12.4x | 13.4x | 14.4x | 15.4x | 16.4x |

| EPS – 2023 ($) | 5.16 | 5.16 | 5.16 | 5.16 | 5.16 |

| Target Price ($) | 63.9 | 69.0 | 74.2 | 79.4 | 84.5 |

| Market Price ($) | 70.3 | 70.3 | 70.3 | 70.3 | 70.3 |

| Upside/(Downside) | (9.1)% | (1.8)% | 5.6% | 12.9% | 20.3% |

| Source: Author’s Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $74.8, which implies a 6.5% upside from the current market price. Adding the forward dividend yield gives a total expected return of 7.8%. Hence, I’m maintaining a hold rating on ServisFirst Bancshares.

Be the first to comment