Sundry Photography

While many software companies like Microsoft (MSFT) has posted rather weak results, ServiceNow (NYSE:NOW) has demonstrated strength in its earnings in the recent fourth quarter results.

There was only one rather small miss for ServiceNow’s fourth quarter earnings which, in my view, is rather insignificant, which I will explain further below.

This article goes deeper into ServiceNow’s fourth quarter earnings and highlights the key takeaways from the quarter. I have written previous articles on ServiceNow that can be found here.

Earnings results largely in-line except for one

In the fourth quarter of 2022, ServiceNow reported results that were ahead on all key metrics except one.

Subscription revenue grew 27.5% on a constant currency basis to $1.86 billion, one percentage point ahead of the guidance.

Operating margins came in at 28% in the fourth quarter, two percentage points ahead of guidance. This was driven by lower FX headwinds than expected and discipline in expenses.

ServiceNow also generated $1 billion of free cash flow. Free cash flows for the quarter also came in 8% higher than consensus.

Miss on cRPO

The only miss in the fourth quarter results was cRPO.

This was a rather small miss of 50 basis points, with cRPO growth on a constant currency basis coming in at 25.5%.

So, what was the reason for this miss in cRPO?

The reason for the narrow miss was due to lower-than-expected early renewals in the quarter. As the normal rate of early renewals were baked into the guidance, there were slightly fewer early renewals in the quarter than normal.

Other key metrics showed strength

Net new ACV exceeded the company’s own target, growing more than 30% in the quarter. This includes the ACV from new logos and expansion and contributes to incremental revenue growth. Net new ACV is important for ServiceNow as this is what drives the business going forward, bringing more incremental growth than the customers who are renewing contracts.

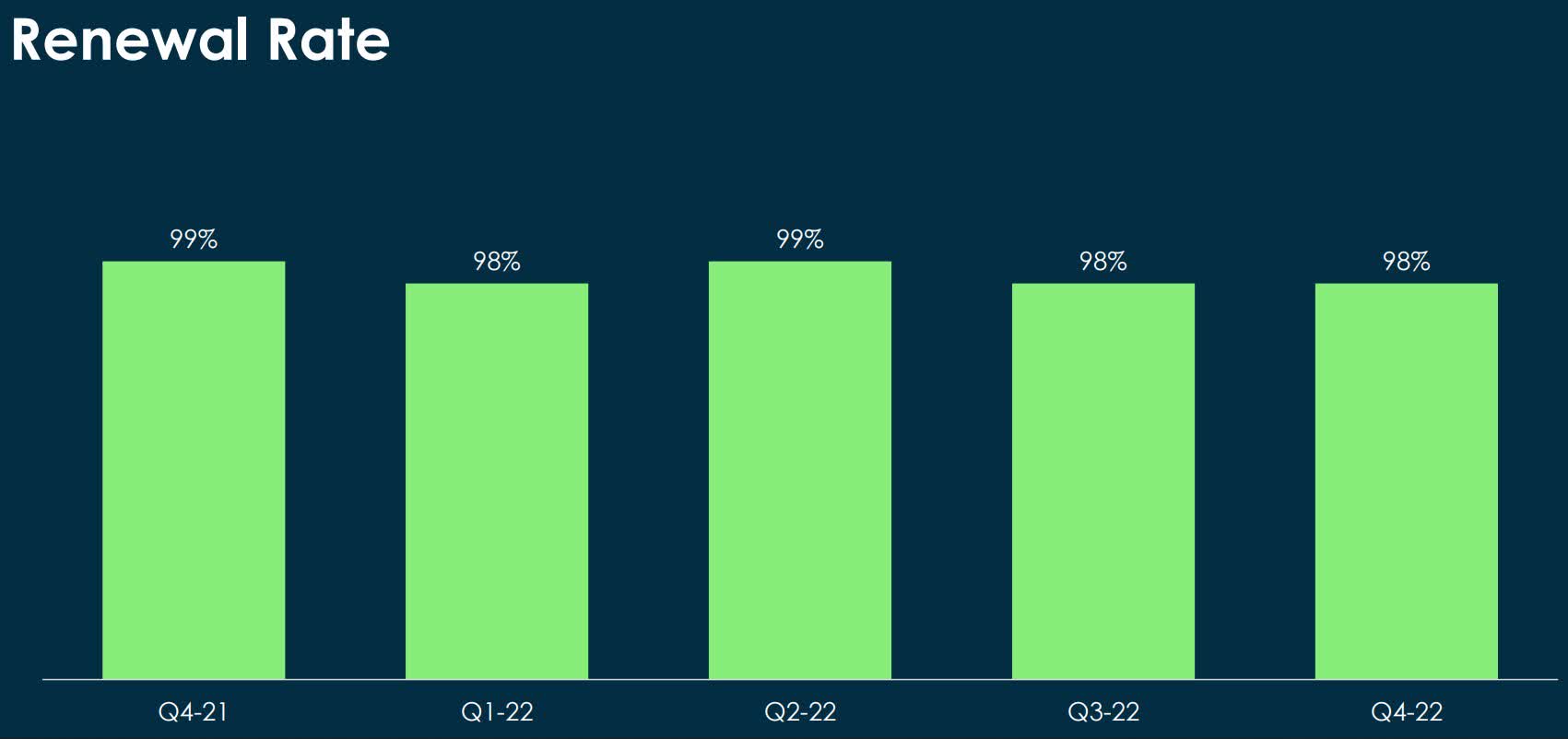

ServiceNow also highlighted that its 4Q22 on-time renewals remained “best-in-class” at 98%, providing ServiceNow confidence that customers will renew at historical levels.

ServiceNow renewal rates (ServiceNow IR)

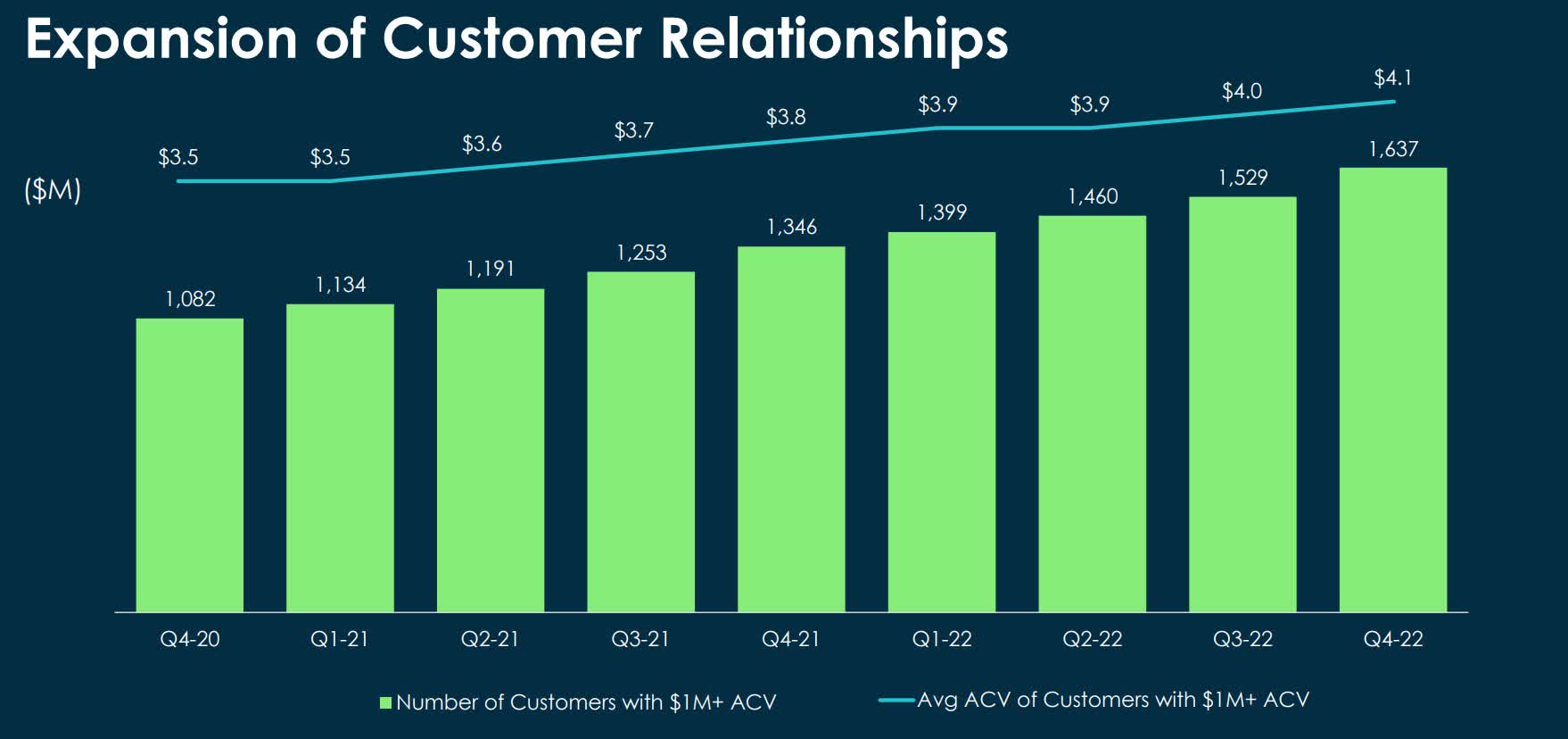

The company demonstrated strong ability to land large deals as it has its largest net add of customer deals with more than $1 million in ACV to 126. In the quarter, ServiceNow also had two of its top five largest deals ever. This expansion of large deals in an uncertain time is testament to ServiceNow’s quality platform that adds value to its customers.

ServiceNow’s number of customers with more than $1 million ACV (ServiceNow IR)

In addition, ServiceNow saw broad-based strength in non-IT workflows. Non-IT workflows like customer, employee and creator workflows are the other workflows that are critical for the investment thesis for the company. With its large customer base in its IT workflow, my investment thesis for ServiceNow is that it is then able to cross sell and upsell its other products and offerings to this customer base.

Lastly, management commented that its pipeline coverage ratio is higher than it was a year ago.

Guidance

In terms of guidance, ServiceNow is guiding for subscription revenues to be between the range of $8.44 billion to $8.50 billion. This guidance implies 22.5% to 23.5% subscription revenue growth. In addition, the guidance for revenues comes a little higher than what market consensus was expecting.

As for guidance for ServiceNow’s operating margin and free cash flow margin, management guided that this will come in at around 26% and 30% respectively. Both operating margin and free cash flow margin guidance met consensus expectations.

I think that ServiceNow’s guidance provided in this fourth quarter results differentiated itself from the rest of the software industry.

This is because its forward guidance shows resilience and strength in the business as the guidance management put forward either met or exceeded market expectations. I think that this demonstrates how solid the fundamentals of the ServiceNow platform are today despite the noise in the macro backdrop. Relative to peers like Microsoft that reported recently, despite both companies operating in what I would describe as a tough macro backdrop, ServiceNow continues to exceed expectations compared to competitors.

As elaborated in the earlier earnings analysis for Microsoft, the company initially came up with a 10% revenue growth target, which it has lowered in the current earnings report. This is due to the weak macro backdrop, uncertain PC demand and weakness in Azure, resulting in Microsoft having difficulty in meeting its prior target. On top of that, Microsoft also disappointed in its cloud segment when it guided a worse than expected deceleration in Azure, expecting and guiding for a deceleration of Azure by 4 to 5 percentage points for the next quarter after Azure missed in the recent quarter.

Valuation

ServiceNow is currently trading at around 42x P/E.

Based on this relative valuation, I think that ServiceNow seems fairly valued at the current stock price.

I am neutral on ServiceNow stock at current levels.

While it remains to be a solid software company with great execution and growth profile, the current valuation does not offer me decent margin of safety. As a result of its risk reward perspective being relatively fair, I am staying on the sidelines for now.

Risks

Competition

ServiceNow operates in the software industry that is rather competitive and continuously seeing innovation. While ServiceNow is a leader in the ITSM space, it risks having new threats from other new entrants and established players in the industry.

In addition, as ServiceNow looks to drive growth in its newer businesses and other workflows, the company needs to be able to differentiate itself and its offerings to be able to penetrate these markets and drive market share growth in these segments.

Weakening and uncertain macro backdrop

I think that ServiceNow has demonstrated its ability to execute well in a difficult macro backdrop. That said, there are risks that come with this. The main risk is that with the high expectations that ServiceNow’s business is relatively resilient, if there are signs of weakening or slowing down of its business, there could be a material impact to its stock price given what has already been priced in.

Key takeaways from ServiceNow’s quarter

- The first thing I would note is that while competitors in the industry like Microsoft cited a tough operating environment, ServiceNow managed to beat on multiple fronts, delivering a solid quarter.

- Not only that, guidance for ServiceNow’s platform continues to hold up well as management continued to maintain guidance even in a more challenging operating environment.

- Miss in cRPO was due to the lower-than-expected early renewals for the quarter, which when removed, lead to one to two percentage points beat in cRPO.

- ServiceNow continues to have best-in-class renewal rates despite a weakening macro environment, which is encouraging in my view.

- Lastly, ServiceNow continued to show strength in net adds of customer deals with more than $1 million ACV, continued momentum in non-IT workflows and pipeline coverage ratio remains solid.

Be the first to comment