Sundry Photography

Thesis

SentinelOne (NYSE:S) has been doubling their revenue year over year while improving margins. Unfortunately, this rapid pace of revenue growth has come at a cost, and operating losses are still very high. They have a fantastic balance sheet with a lot of cash and no debt and can sustain these losses for now. Despite the positives, we believe that SentinelOne is a show me story and prospective investors can wait until the company cleans up some of their operational metrics before making an investment.

Rapid Revenue Growth

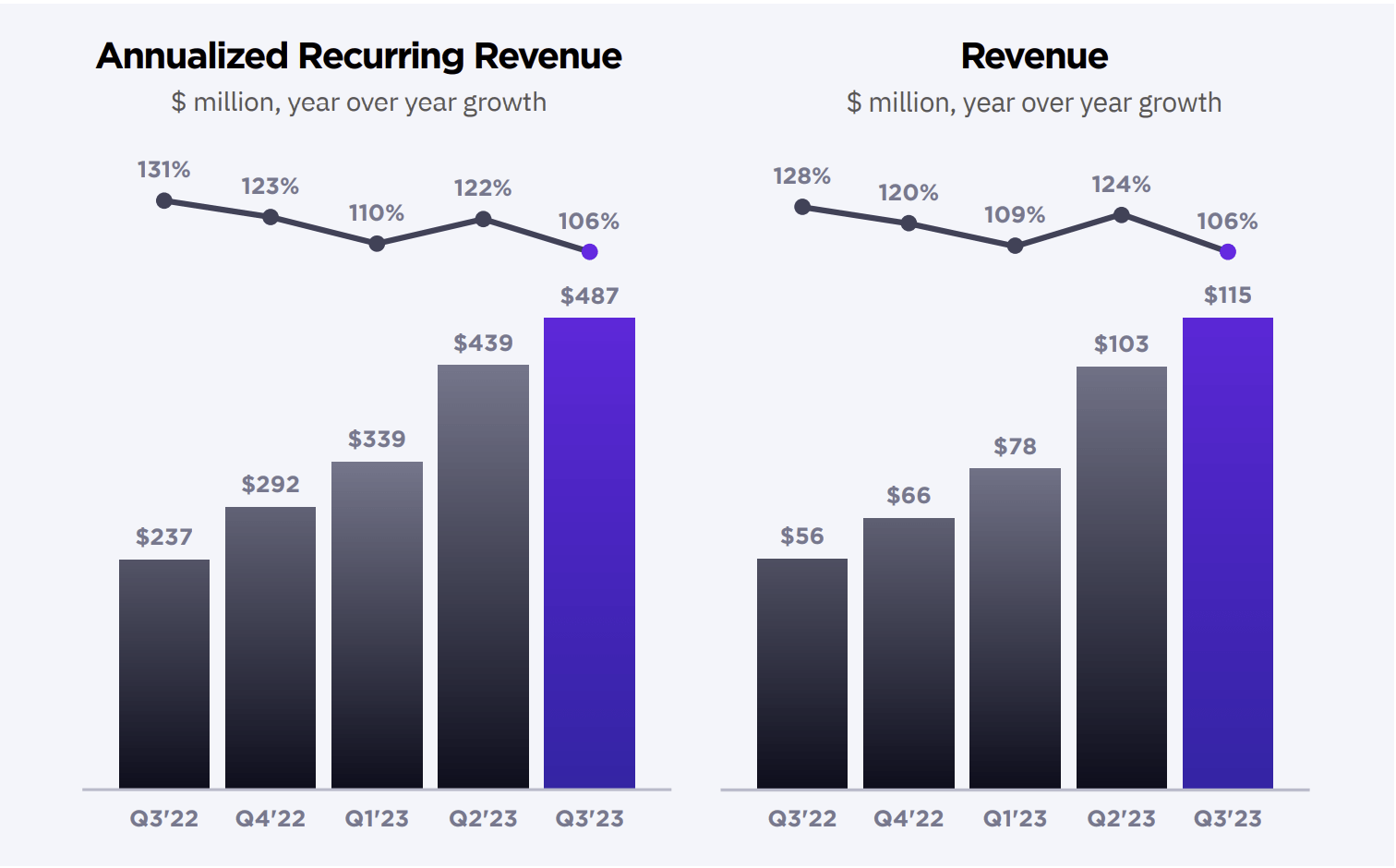

In their third quarter, SentinelOne managed to grow revenues 106% year over year. Another way of looking at it is that their annualized recurring revenue grew to $487 million.

Revenue Visual (SentinelOne Q3 Shareholder Letter)

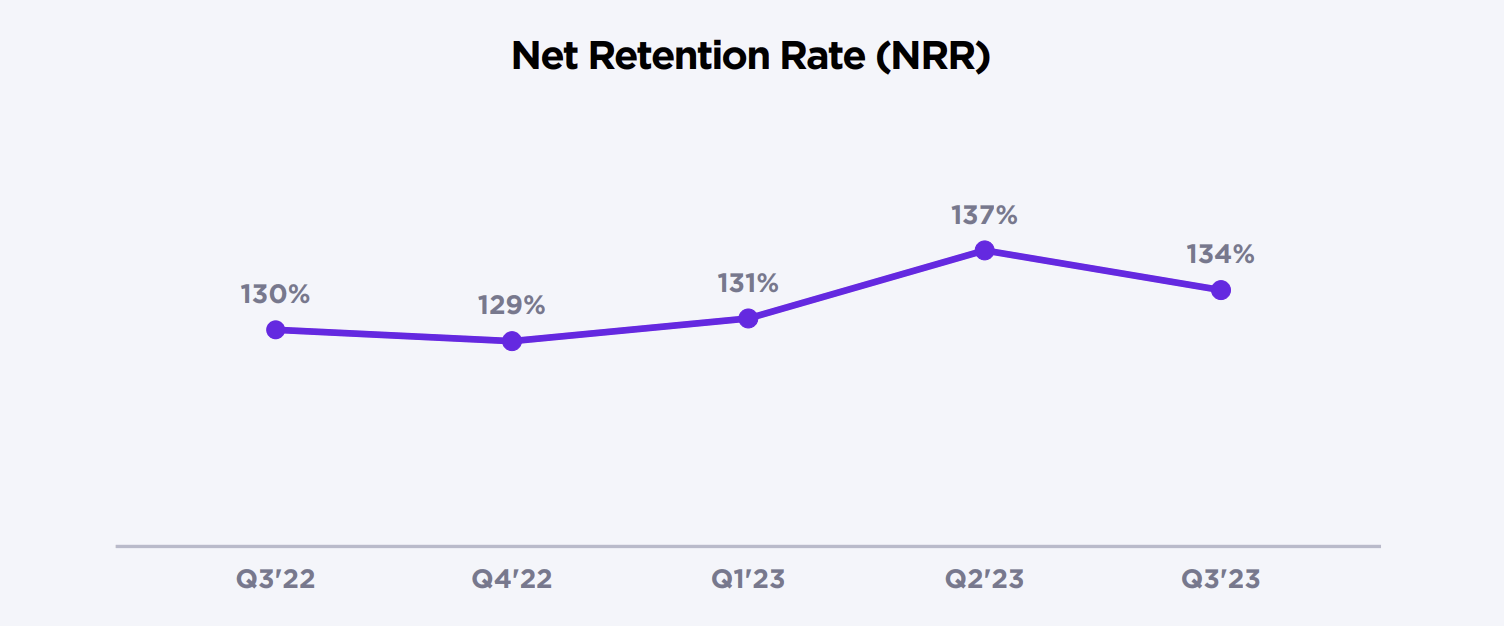

This blistering pace of revenue growth was accompanied by a net retention rate of 134%, which is incredibly high even for a software company.

Net Retention Rate Visual (SentinelOne Q3 Shareholder Letter)

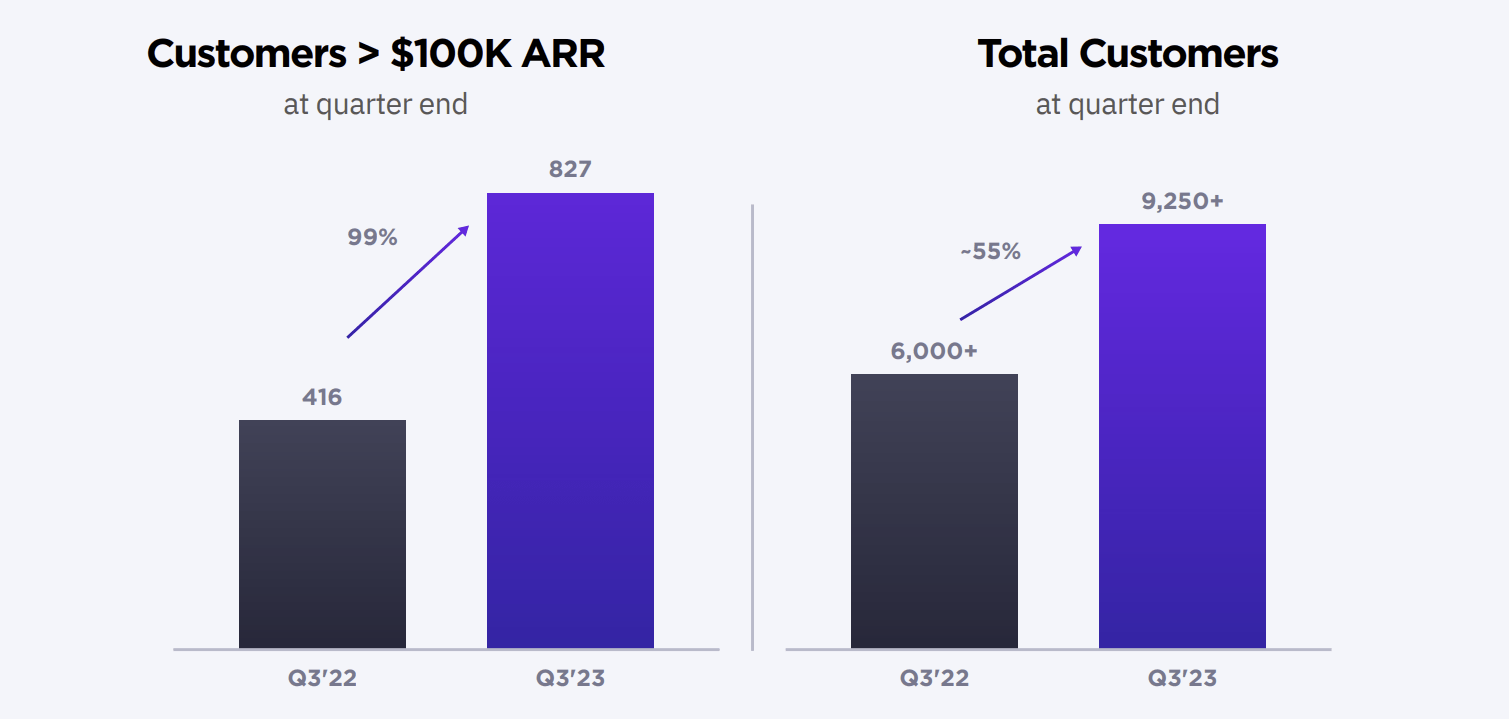

SentinelOne has done a great job at broadening their customer base, increasing their total customer count by 55% year over year. The growth in customers spending more than $100,000 a year is encouraging and shows that SentinelOne is continuing to find ways to provide more value to their existing customers.

Customer Growth Visual (SentinelOne Q3 Shareholder Letter)

All of these positive growth metrics are a welcome sight, and many of them are the best that I’m currently seeing in the cybersecurity sector. That being said, all of this growth is coming at a steep cost. Their revenue growth has been matched by increasing operating losses. Even more concerning is that SentinelOne isn’t just unprofitable on a GAAP basis, they are also operating cash flow negative.

Improved Margins but Still Negative

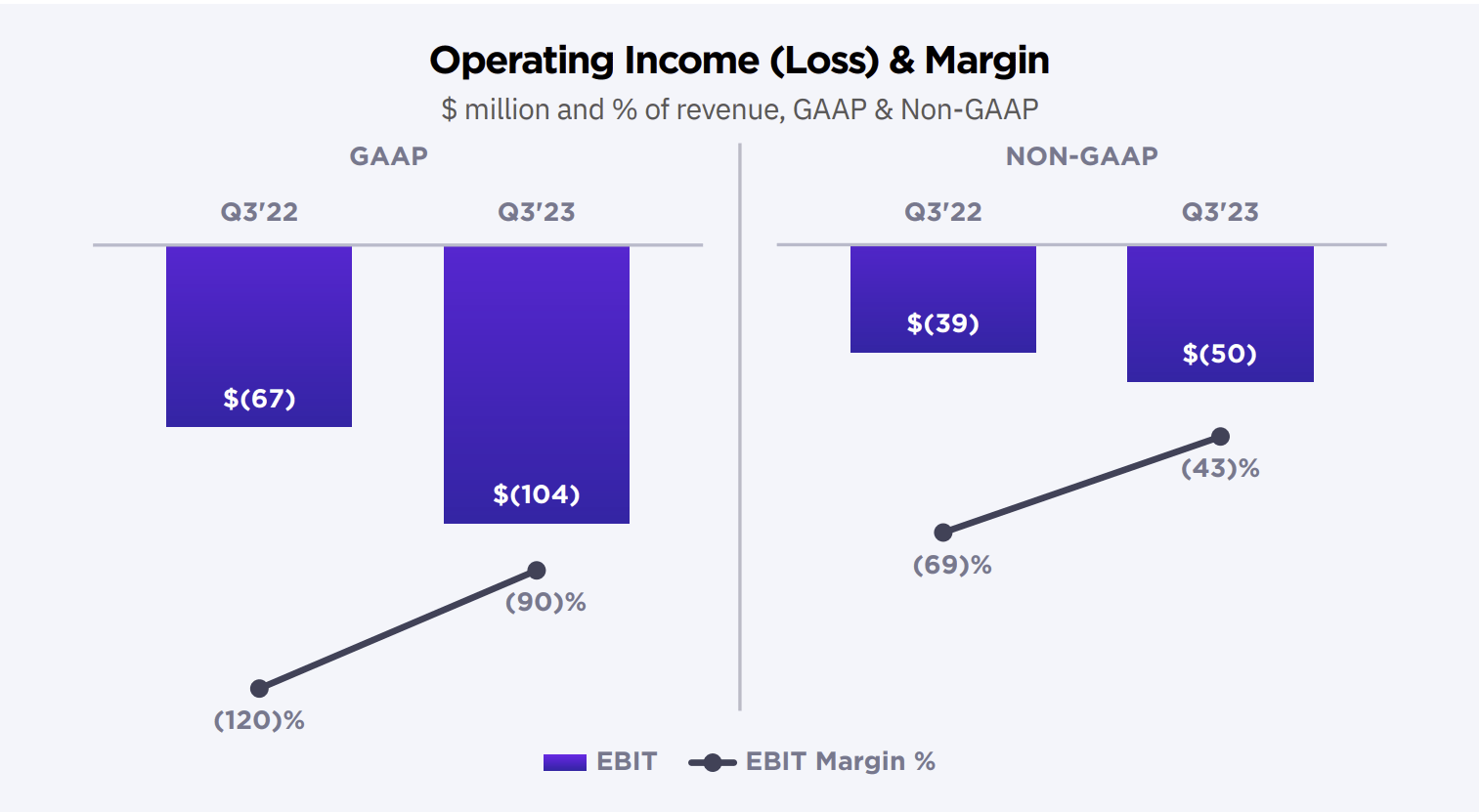

SentinelOne experienced growing operating losses in the quarter, with GAAP losses increasing to $104 million. The good news is that their operating margins improved from -120% to -90%. These margins are still deeply negative, and the company needs to show continued improvement in this area for investors to feel comfortable about management’s financial discipline.

Operating Income Visual (SentinelOne Q3 Shareholder Letter)

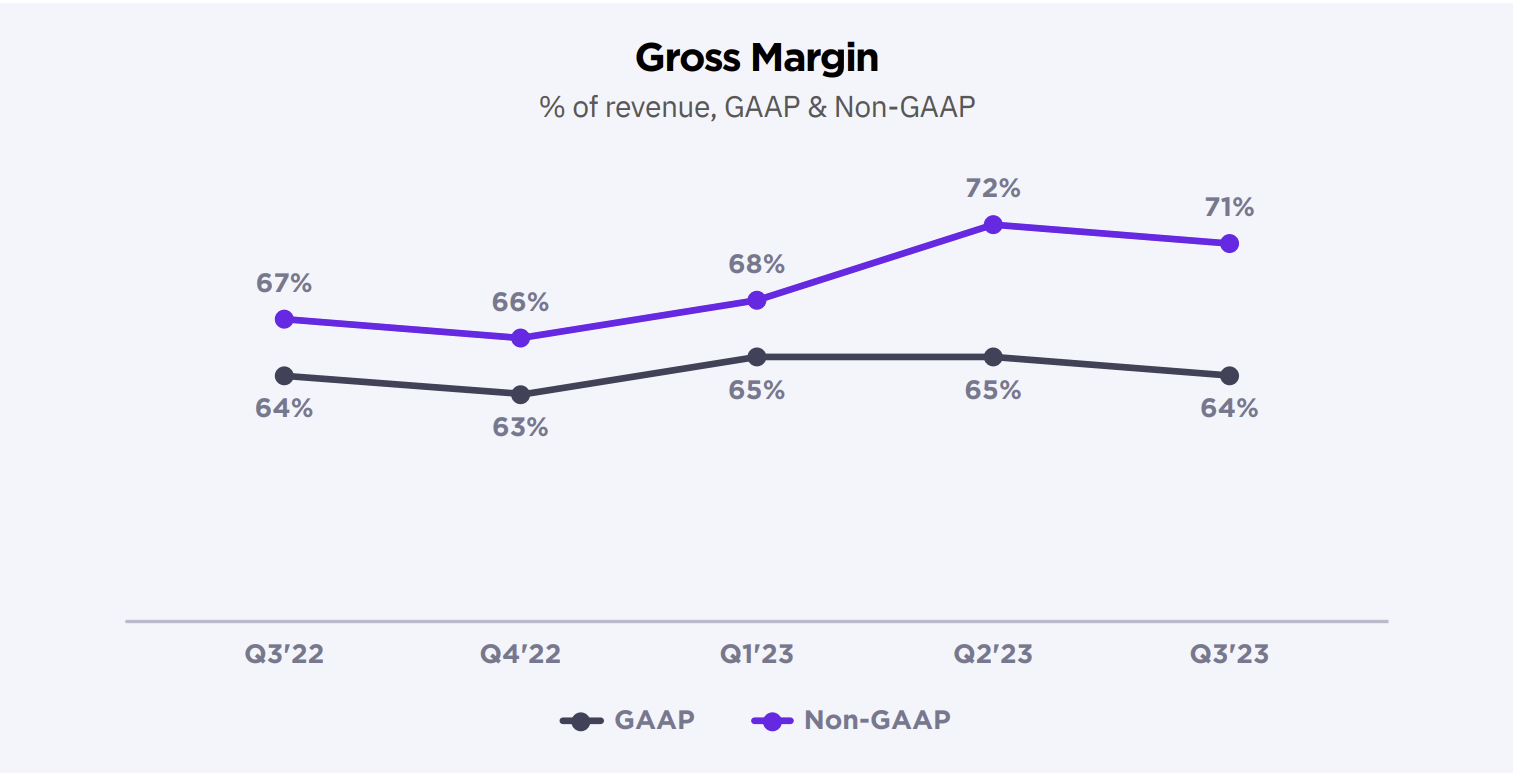

GAAP gross margins declined sequentially, but improved year-over-year. This improvement is to be expected given the nature of their business, but there is likely a ceiling to how good their gross margins can be.

Gross Margin Visual (SentinelOne Q3 Shareholder Letter)

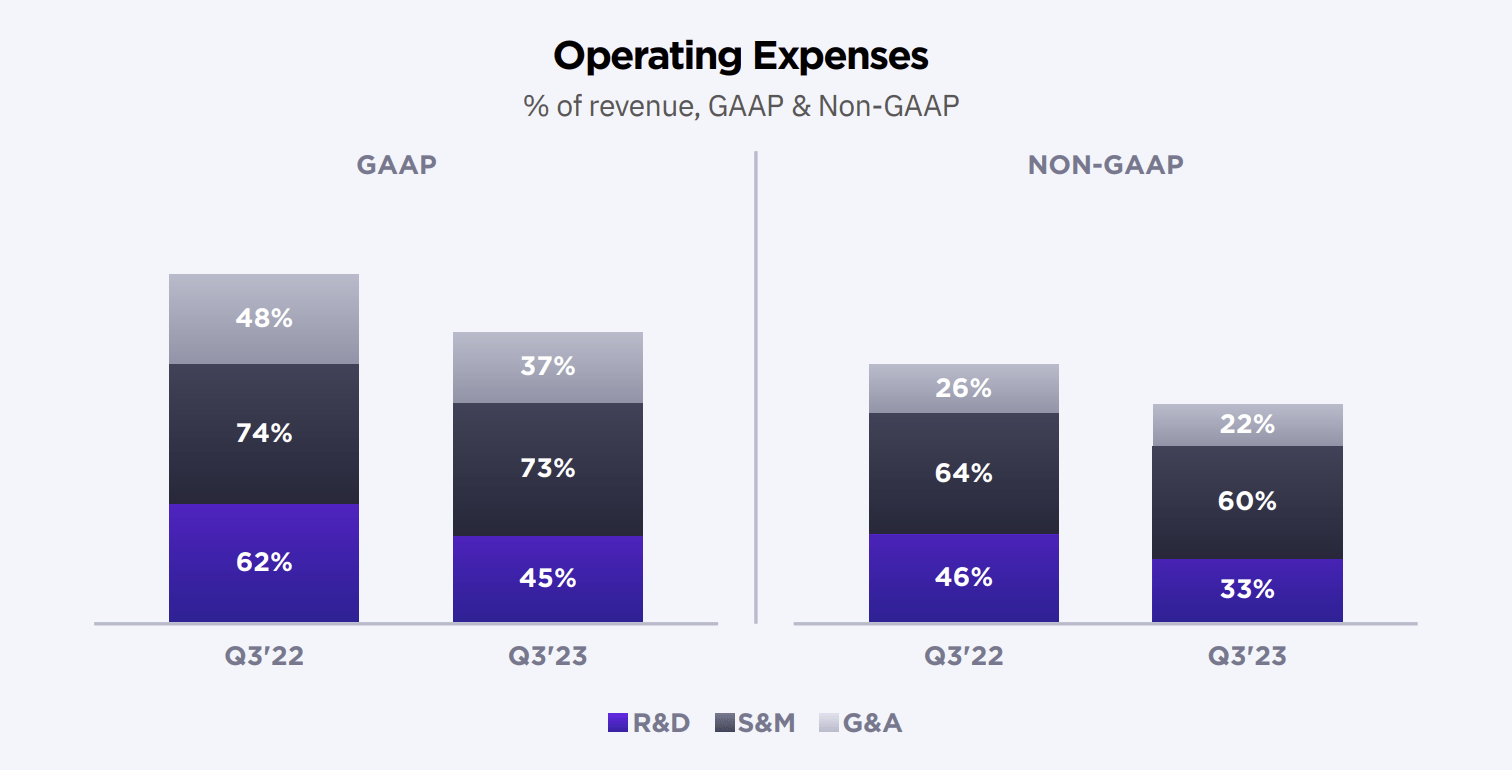

Much of the financial potential in the business model comes from operating expenses decreasing as a percentage of revenue as the company scales up. SentinelOne managed to deliver in this area, with operating expenses decreasing to 155% of revenue from 184% in the year ago period. This is an important trend and shows that they are beginning to realize operating leverage, but these expenses are still way too large of a percentage of revenue, even when considering their revenue growth rate.

Operating Expenses Visual (SentinelOne Q3 Shareholder Letter)

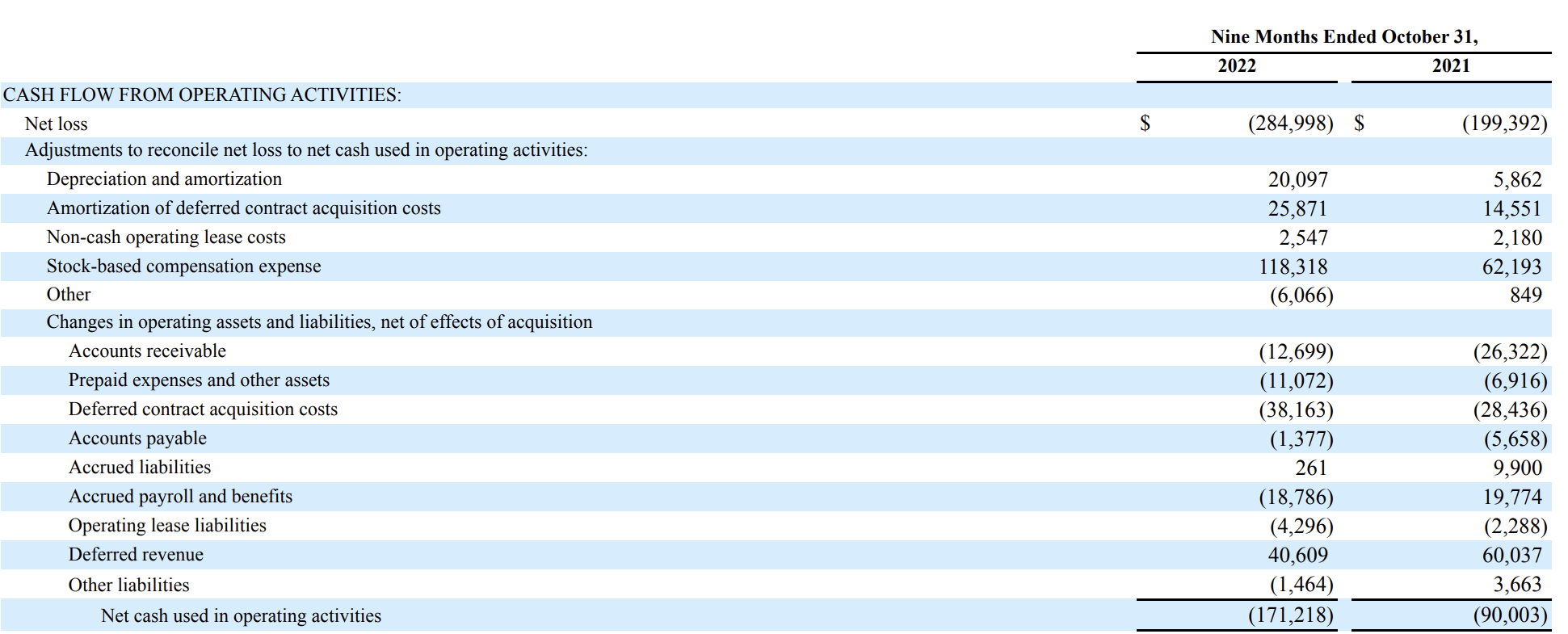

Perhaps more concerning than the operating losses is the fact that SentinelOne is operating cash flow negative, experiencing net cash used in operating activities of $171 million over the past nine months.

Cash Flow from Operations (SentinelOne Q3 Earnings Report)

This cash burn is in relation to their net cash balance of roughly $1.1 billion. Given their large war chest, the company is clearly able to fund existing operations, but the concern is that their cash burn accelerates over the coming years, and they never manage to control it.

Even though the company is showing improvement in many of their profitability metrics, it isn’t enough as of now. We would like to see the company at the very least become cash flow positive before having a positive view of their financial situation, at least from an operating standpoint. From a balance sheet standpoint, the company is in a secure position and has plenty of cash and no debt.

Price Action

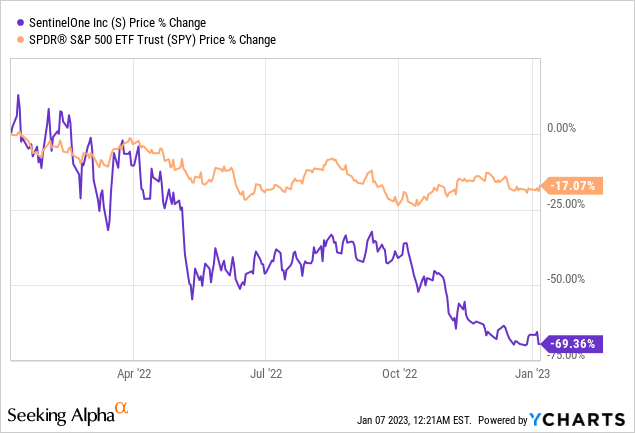

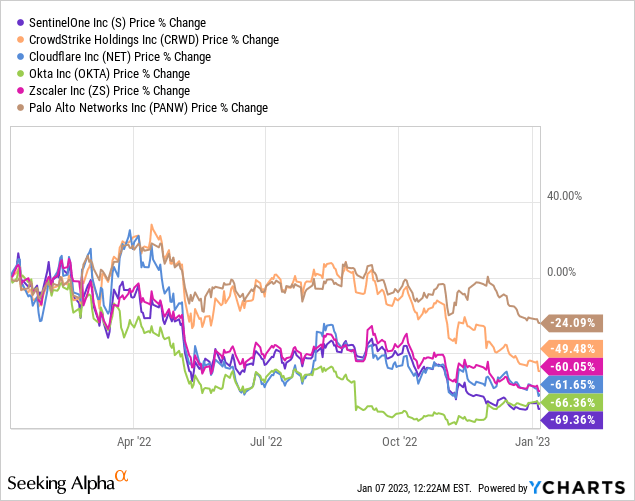

Like most growth stocks, SentinelOne had a rough 2022 and is down 69.36% over the past year, massively underperforming the S&P 500.

This underperformance isn’t isolated to SentinelOne as other cybersecurity stocks haven’t done much better.

It’s worth noting that SentinelOne is the worst performing of the cybersecurity stocks shown in the above chart. This is likely to do with the company being relatively smaller and less established. Investors seem to be unwilling to give them the benefit of the doubt or think the company will have difficulty in a tougher macro environment.

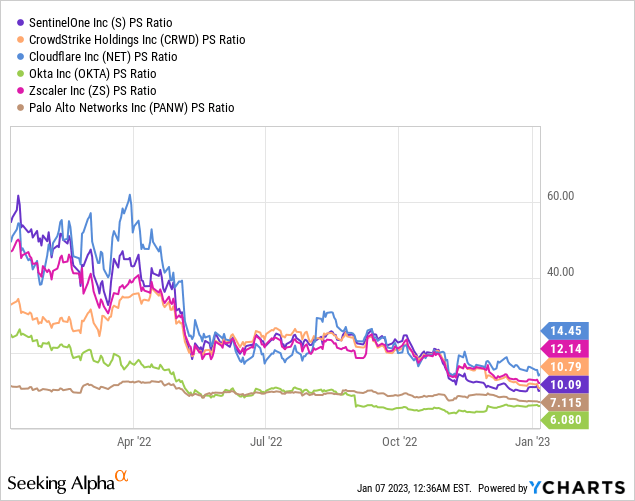

Valuation

SentinelOne is losing a lot of money and remains expensive according to many valuation metrics, but their rapid revenue growth and clean balance sheet somewhat make up for it.

On a price to sales basis, they are trading at around 10x, which is high but not unreasonable for the sector.

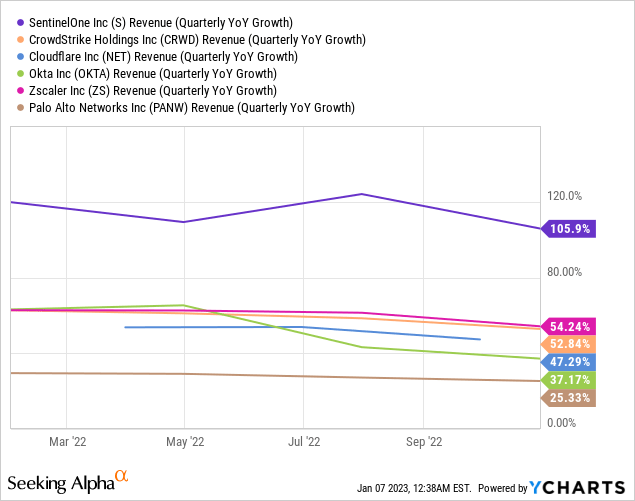

SentinelOne certainly has sales growth going for it, boasting a year-over-year revenue growth rate far above the sector.

As far as the stock is concerned, we think that it’s probably best to ignore valuation metrics and avoid the stock until they stem their steep operating losses and cash burn. Once they do that, it’s worth taking a closer look, but for now we remain on the sidelines.

Potential Acquisition Target

It’s entirely possible that when sentiment improves in capital markets, SentinelOne could be acquired or taken private. There is a high appetite for acquisitive activity in the cybersecurity sector. This is partially because large cybersecurity companies have strong balance sheets and private equity firms have plenty of dry powder and are waiting for conditions to improve. With such high levels of revenue growth and a clean balance sheet, SentinelOne could be an attractive asset for them to buy at these levels. While this probably shouldn’t be a factor in whether or not someone makes an investment, such an event could be a nice bonus for investors buying at these depressed prices. For investors that bought in at much higher prices, not so much.

Risks

We believe that investors should wait for profitability metrics to improve, so the risk to this thesis is that they continue to grow while losing lots of money before eventually flipping the switch on their business and entering profit mode. If the stock price increased despite their operating losses, prospective investors could find themselves wanting to buy at a higher price and miss out on some of the gains. This scenario could certainly happen, and situations like these are a balance of risk and reward. The risk tolerance of every investor is different, and some may like what they see here. In my opinion, it’s fine to wait for SentinelOne to prove profitability before investing, or at the very least stem their massive losses. Even though it may seem unlikely now, it’s possible that SentinelOne is never able to run their business profitably. Even companies with great products and services are sometimes unable to be profitable because management is financially irresponsible. Given how large the losses are and how much they are increasing, I don’t see much downside to waiting before making an investment, given the risks involved.

Key Takeaway

We view SentinelOne as too risky to make an investment here. Investors will not lose anything by waiting for some of the uncertainty to shake out. The worst case scenario is that investors miss out on an increase in the stock price, but there are lots of other companies to invest in that have just as good or better prospects, some of them in the same sector. Despite rapid growth and a solid balance sheet, we believe investors should show patience regarding SentinelOne stock and wait for them to show more improvement in their profitability metrics and stem the massive losses they are currently experiencing.

Be the first to comment