SimonSkafar

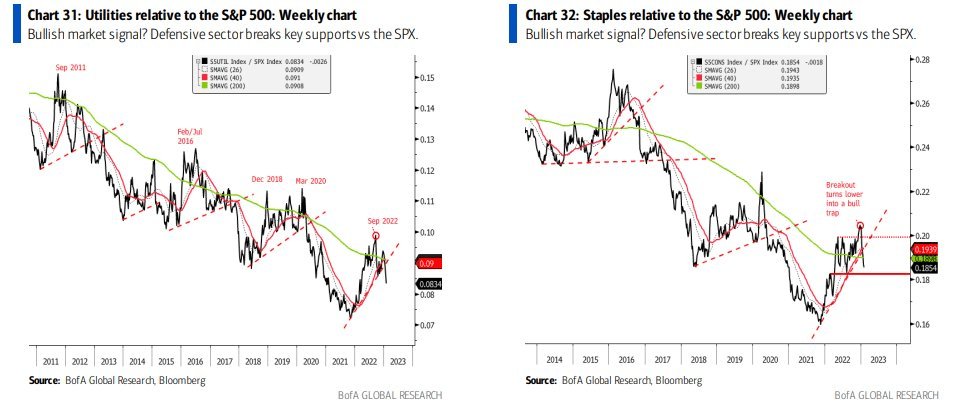

It has been a defensive trainwreck to start the year. The technical relative charts of Utilities and Staples have deteriorated in the last several weeks after the two niches were seen as safety trades last year. One utilities sector name features a trendless chart, but is it a decent value ahead of earnings? Let’s figure it out.

Utes & Staples Struggle In 2023

BofA Global Research

According to Bank of America Global Research, Sempra (NYSE:SRE) is a natural gas and electric transmission and distribution company. Operations are divided among three segments: the California Utilities, Texas Utilities, and Sempra Infrastructure Partners (Gas, Power, and Renewables). The California Utilities (South California Gas Company and San Diego Gas and Electric) distribute gas and electricity to approximately 25mn customers in Southern California.

The San Diego-based $49 billion market cap Multi-Utilities industry company within the utilities sector trades at a high 22.1 trailing 12-month GAAP price-to-earnings ratio and pays a solid 2.9% dividend yield, according to The Wall Street Journal.

SRE has some upside potential through its new LNG projects, namely the Port Arthur LNG Phase 1 deal. A volatile domestic energy market has perhaps pressured the stock since last September, along with rising interest rates – another key risk. Shares have sharply underperformed the broad XLU sector ETF since early December. California wildfire risk could be less now following the atmospheric river that struck the state several weeks ago.

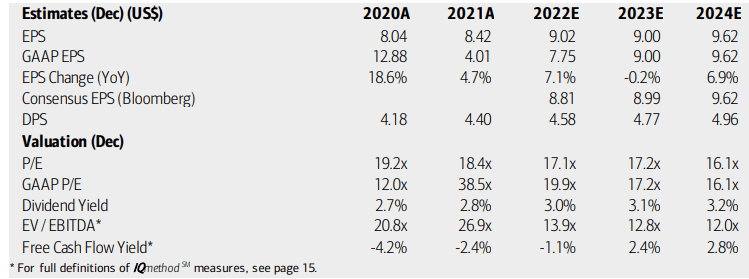

On valuation, analysts at BofA see earnings falling slightly this year. That’s a bearish change from modest per-share profit growth that had been expected when I previously covered the name. A nearly 7% bounce back is expected next year, though. The Bloomberg consensus outlook is about on par with what BofA sees. Dividends, meanwhile, are expected to rise even with a near-term dip in EPS.

Shares continue to trade near the sector-median P/E in the mid to high teens while SRE’s EV/EBITDA ratio is a bit high. Overall, the valuation continues to look unimpressive, but not overly expensive either given decent longer-term earnings prospects. I will be watching how Sempra executes on its LNG project developments this year.

Sempra: Earnings, Valuation, Dividend Forecasts

BofA Global Research

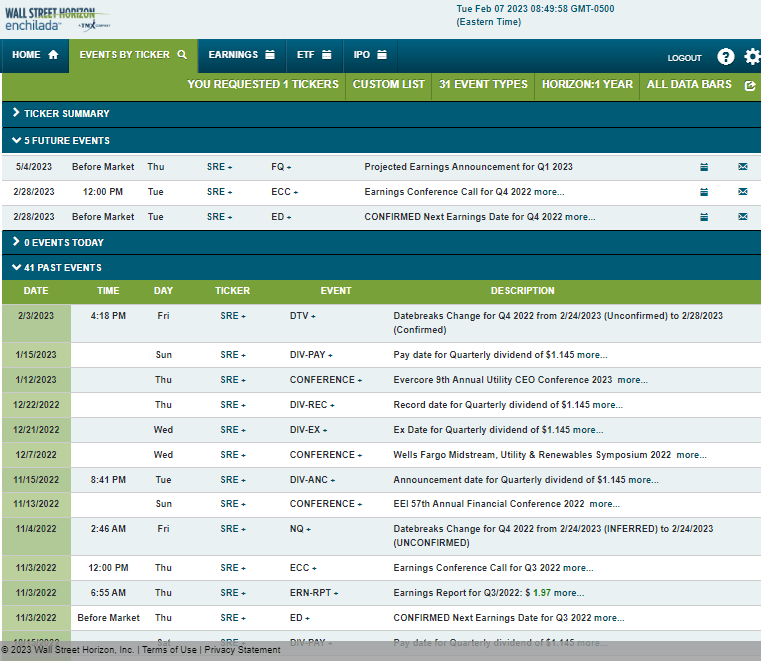

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q4 2022 earnings date of Tuesday, February 28, before the open with a conference call in the afternoon. You can listen live here. The event calendar is light on volatility catalysts aside from the reporting date.

Corporate Event Risk Calendar

Wall Street Horizon

The Options Angle

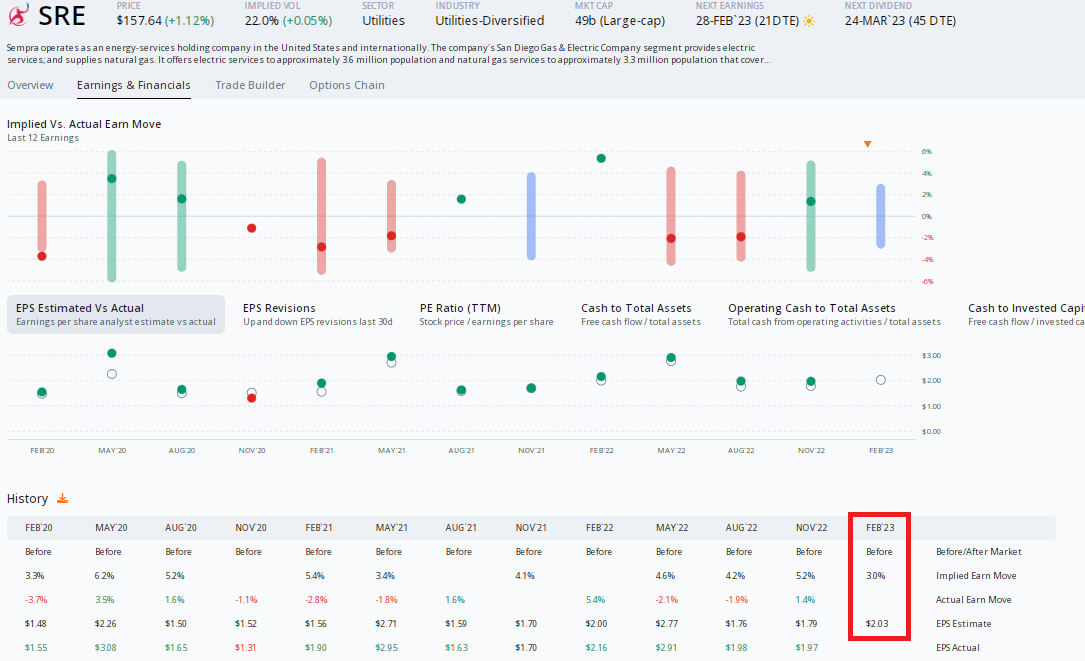

Digging into the upcoming earnings report, data from Option Research & Technology Services (ORATS) show a consensus EPS forecast of $2.03 which would be a 6% drop from $2.16 of per-share profits earned in the same quarter a year ago. The bulls can point to a 5:1 ratio of analyst EPS upward to downward revisions since the last quarterly release. Sempra has exceeded expectations in each of the last eight reports, but shares have a mixed performance history post-earnings.

The options market has priced in a small 3.0% earnings-related stock price swing using the at-the-money straddle expiring soonest after the earnings report. That’s a small premium to pay, so I would be long options heading into the Q4 report.

SRE: A Small Earnings Move Priced In

ORATS

The Technical Take

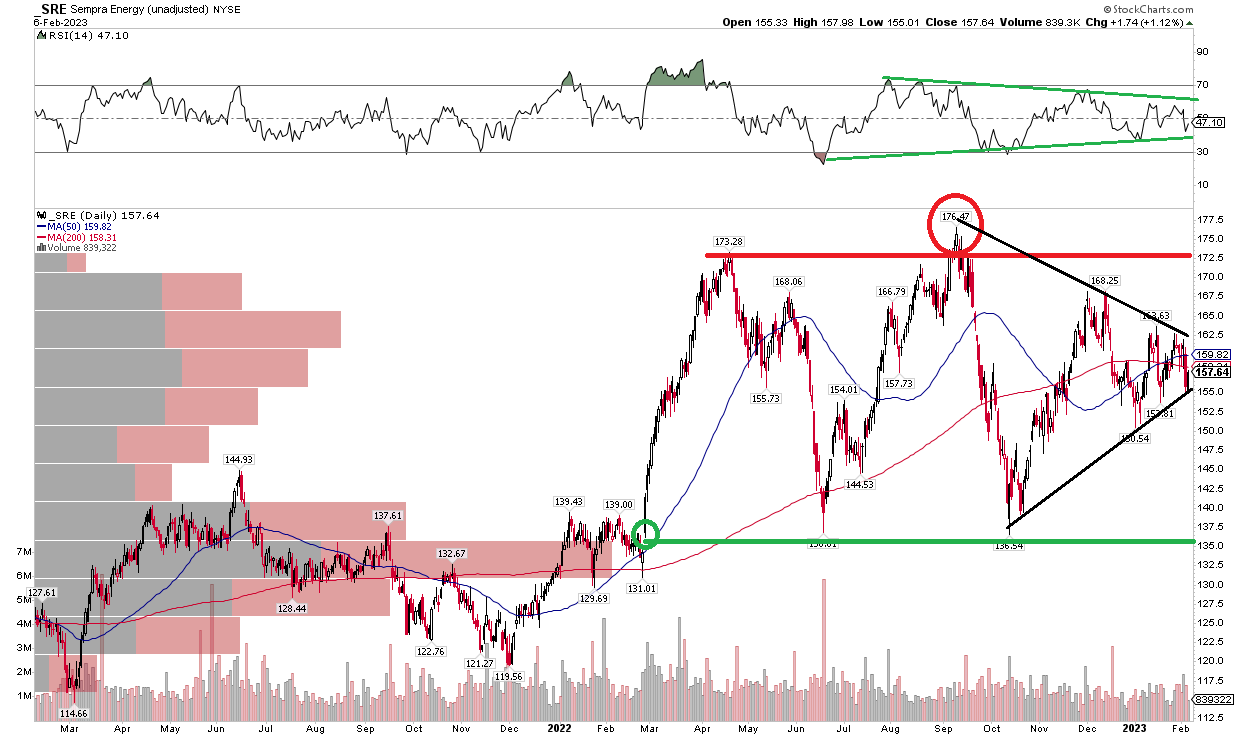

With a fair fundamental value and inexpensive options, how does the chart look? Notice in the graph below that shares had a bearish false breakout in September. That is precisely when I had a ‘buy on technicals’ call which was clearly wrong. From false moves come fast moves, and SRE indeed fell hard right to support near $136 – the June low.

The stock is now in a consolidation pattern. Without an established trend, we really need to wait for a breakout or breakdown from this triangle. $173 is resistance while $136 is support. For now, flat moving averages and a consolidating RSI are evidence of no trend, so I am a hold technically.

SRE: In Consolidation Mode

Stockcharts.com

The Bottom Line

Ahead of an expected YoY EPS drop and with mixed technicals, I’m a hold overall on SRE, but keep your eye on how its LNG projects go and how the chart unfolds from here.

Be the first to comment