Smederevac

A Quick Take On Duos Technologies

Duos Technologies (NASDAQ:DUOT) reported its Q3 2022 financial results on November 14, 2022, missing revenue and EPS estimates.

The firm provides a range of ‘intelligent’ software development for enterprises, primarily in the rail industry.

With a confident and upbeat-sounding management update on DUOT for 2023, continued steady revenue growth and higher gross margins, my outlook for the stock is a Buy at around $4.90 per share.

Duos Technologies Overview

Jacksonville, Florida-based Duos was founded to develop software solutions for a variety of industry verticals, including transportation, retail, law enforcement, oil & gas, and utilities.

Management is headed by Chief Executive Officer Chuck Ferry, who was previously President and CEO of APR Energy and General Manager at ARMA Global Corporation.

Chief Financial Officer is Adrian Goldfarb, 62 years old, who has been with the firm since 2010 and has extensive experience in the information technology industry.

The company’s primary offerings include:

-

vue – rail undercarriage examiner

-

t-vue – thermal undercarriage examine

-

apis – pantograph inspection systems

-

centraco – command and control interface

-

alis – automated logistics information systems

-

praesidium – analytics suite

-

truevue360 AI systems software capabilities

Duos Technologies’ Market & Competition

According to a 2018 report by Mordor Intelligence, the North American rail industry grew by 5% in 2017 and ‘is expected to grow at a steady pace’ through 2023.

Notably, Mexico has approved six new railway projects and Canada’s oil & gas industry remains a strong driver of rail demand in the years ahead.

Major potential rail customers include:

-

Union Pacific (UNP)

-

VNSF

-

CSX (CSX)

-

Norfolk Southern Railway (NSC)

-

Canadian National Railway (CNI)

-

Canadian Pacific Railway

-

Ferromex

-

Kansas City Southern Railway (KSU)

Duos Technologies’ Recent Financial Performance

-

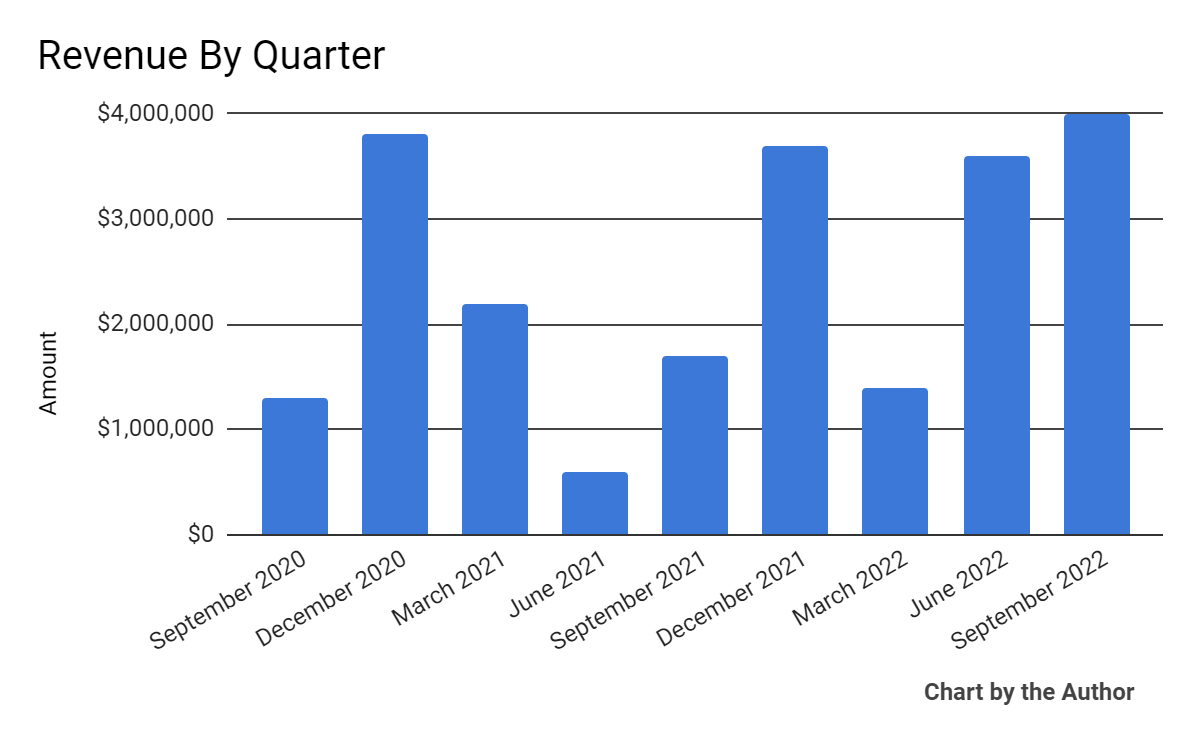

Total revenue by quarter has followed the trajectory shown in the chart below:

Total Revenue (Seeking Alpha)

-

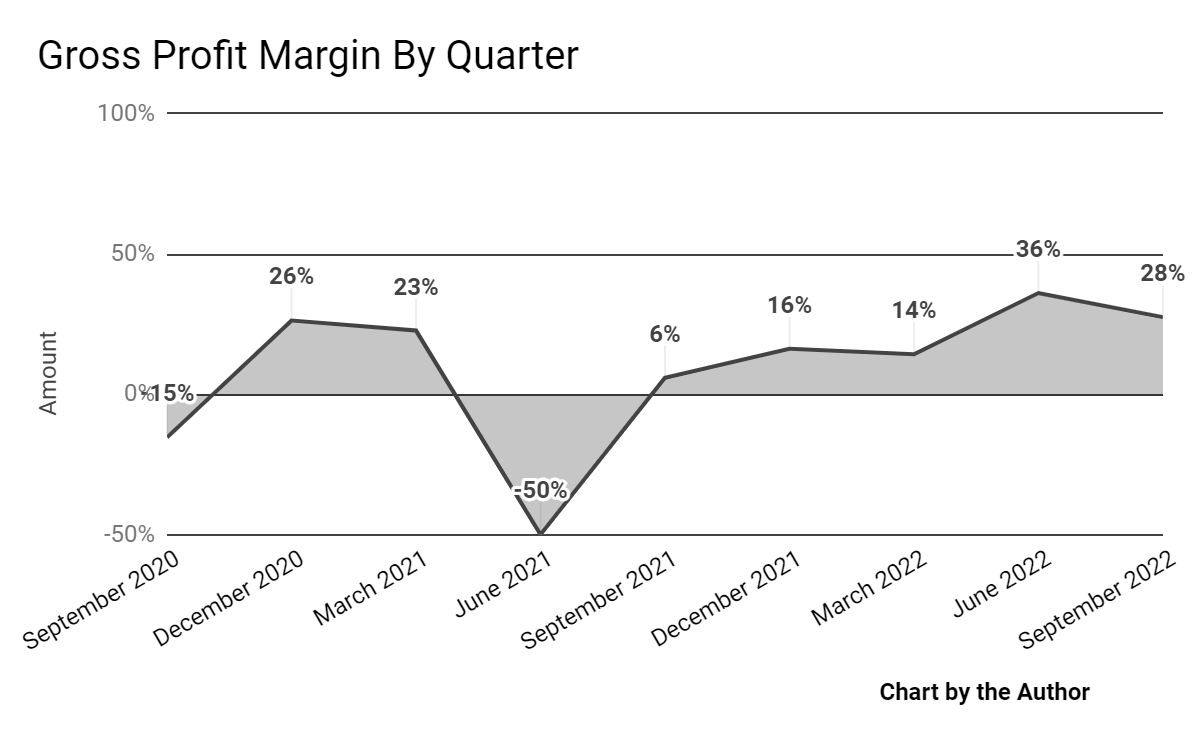

Gross profit margin by quarter has varied substantially, as shown here:

Gross Profit Margin (Seeking Alpha)

-

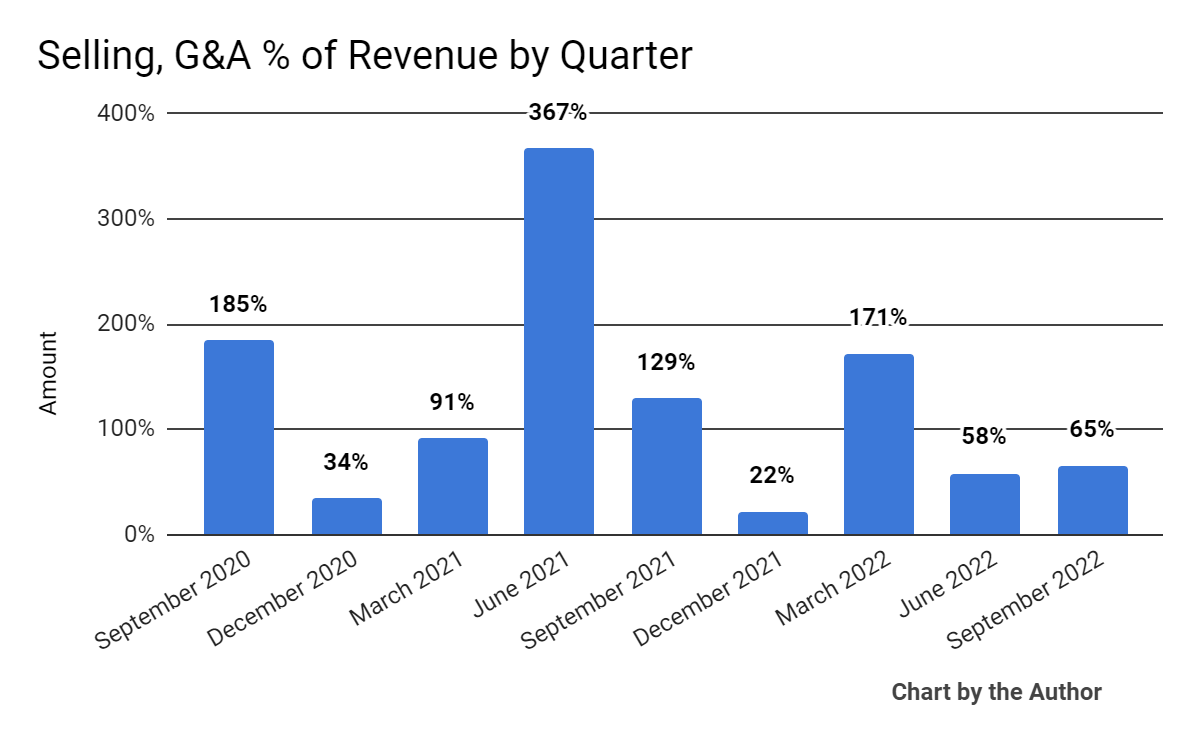

Selling, G&A expenses as a percentage of total revenue by quarter have fluctuated materially in recent quarters:

Selling, G&A % Of Revenue (Seeking Alpha)

-

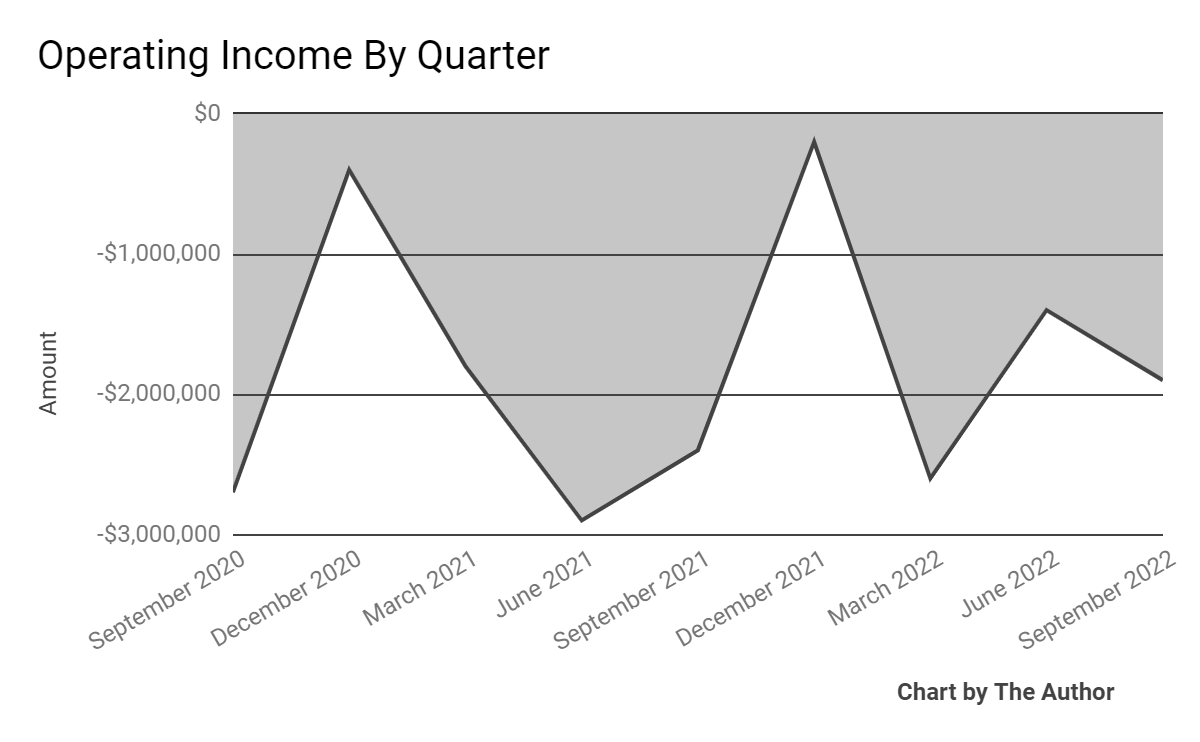

Operating income by quarter has remained negative in the past 2 years:

Operating Income (Seeking Alpha)

-

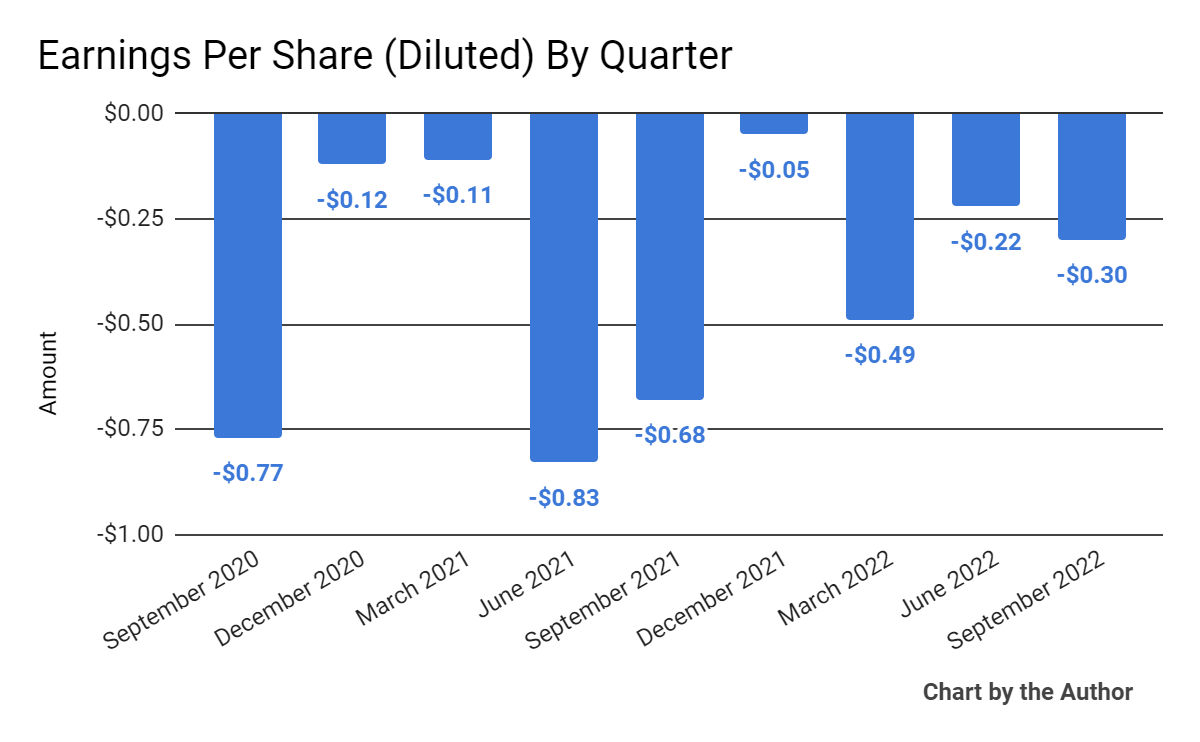

Earnings per share (Diluted) have also fluctuated widely, as the chart below indicates:

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP)

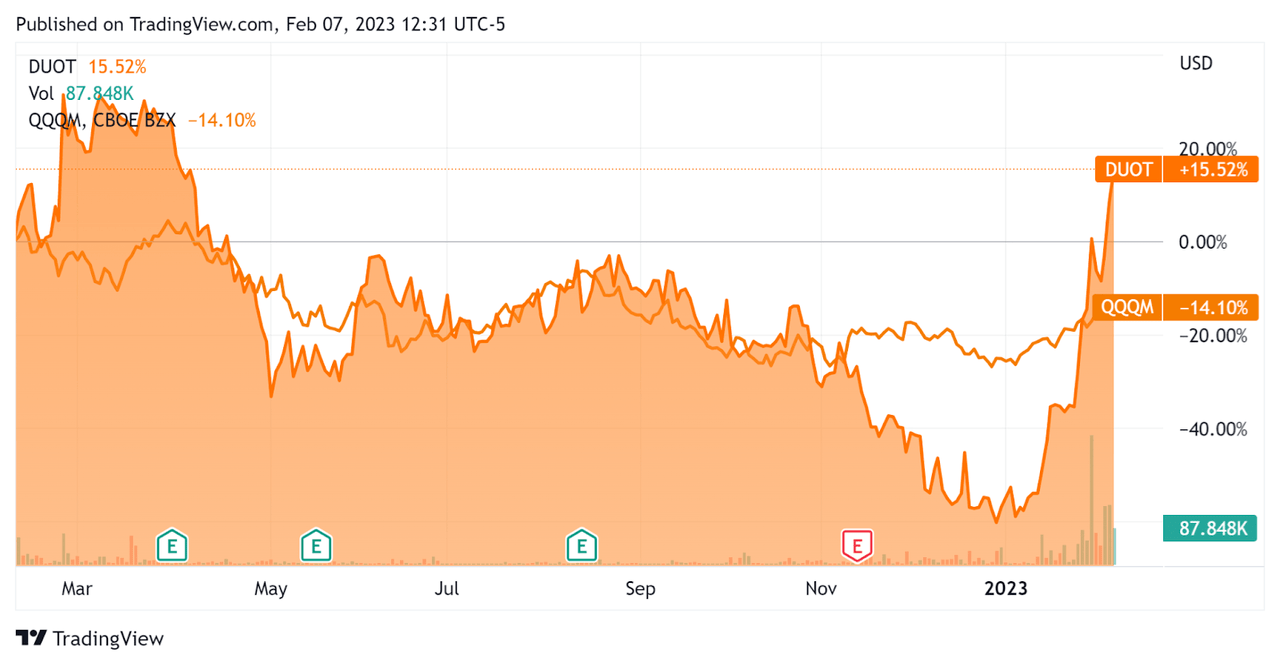

In the past 12 months, DUOT’s stock price has risen 15.5% vs. that of QQQM ETF’s drop of 14.1%, as the chart below indicates:

52-Week Stock Price Comparison (Seeking Alpha)

Valuation And Other Metrics For Duos Technologies

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

2.8 |

|

Price / Sales |

2.1 |

|

Revenue Growth Rate |

53.6% |

|

Net Income Margin |

-47.8% |

|

GAAP EBITDA % |

-46.3% |

|

Market Capitalization |

$32,132,434 |

|

Enterprise Value |

$32,418,836 |

|

Operating Cash Flow |

-$4,907,165 |

|

Earnings Per Share (Fully Diluted) |

-$1.06 |

(Source – Seeking Alpha)

Commentary On Duos Technologies

In its last earnings call (Source – Seeking Alpha), covering Q3 2022’s results, management highlighted the firm’s continued efforts to transition to a recurring revenue and software focus.

The firm expects that it will finish 2023 with a total of 20 RIPs [Railcar Inspection Portals] in operation on the North American rail network.

Notably, moving to a subscription model will slow its revenue ramp but enable the company to ‘drive a greater lifetime value and higher margins.’

As to its financial results, the firm recently announced its preliminary Q4 2022 revenue expectation of $6.3 million, or 71% year-over-year growth.

Management did not disclose any company retention rate metrics.

Q3 2022 GAAP operating loss and negative earnings remained substantial.

For the balance sheet, the firm finished the quarter with $4.97 million in cash and equivalents.

Over the trailing twelve months, free cash used was $5.5 million, of which capital expenditures accounted for $600,000. The company paid $800,000 in stock-based compensation in the last four quarters.

Looking ahead, 2023’s backlog was estimated at $10.7 million, of which the firm expects to recognize $8.4 million in 2023.

Management guided 2023 revenue to $20.5 million at the midpoint of the range, or 33% growth at the midpoint.

Regarding valuation, the market is valuing DUOT at a trailing EV/Revenue multiple of around 2.8x and the stock has risen sharply in recent days on the strength of its Q4 2022 numbers and expected growth in 2023.

The primary risk to the company’s outlook is its transition to a recurring revenue business model, which can slow its revenue growth rate.

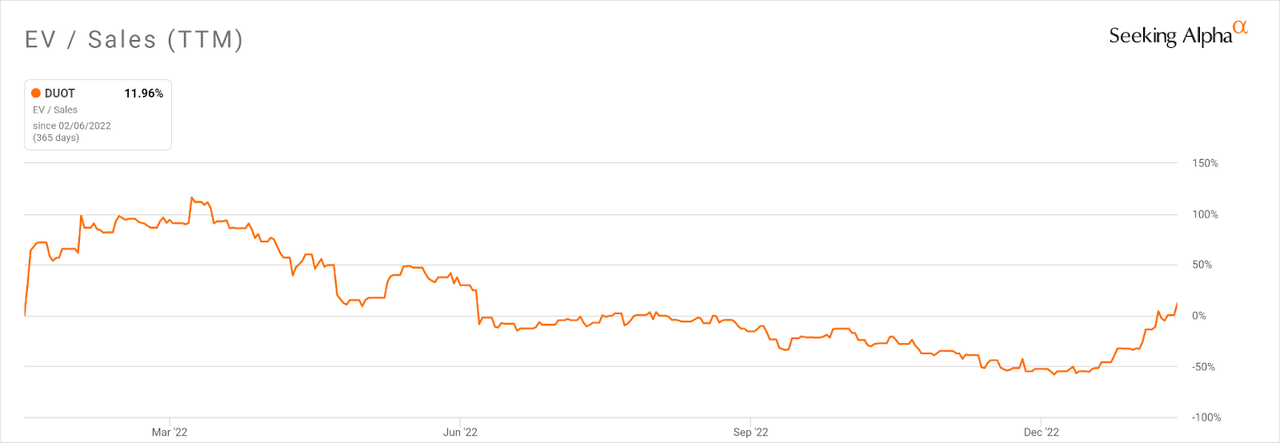

Notably, DUOT’s EV/Sales multiple [TTM] has risen by approximately 12% in the past twelve months, but has been quite volatile over that period, as the chart shows below:

Enterprise Value / Sales Multiple History (Seeking Alpha)

With a confident and upbeat-sounding management update on DUOT for 2023, continued steady revenue growth and higher gross margins, my outlook for the stock is a Buy at around $4.90 per share.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment