Marko Geber

scPharmaceuticals is a de-risked small-cap biotech targeting a lucrative USD>500 peak sales opportunity

scPharmaceuticals Inc (NASDAQ:SCPH) is a ~200M market cap commercial biotech with an exciting cardiology drug that is about to launch in the US market during Q1 2023. We are buyer of SCPH due to three reasons a) market opportunity of decompensated heart failure is lucrative, >500M peak sales, b) drug is already approved with clear differentiation (convenience, comparable efficacy, safety, and cost saving) coming from SC dosage form, c) the current valuation seems modest enough for us to risk buying into the launch.

Heart failure has a high unmet need.

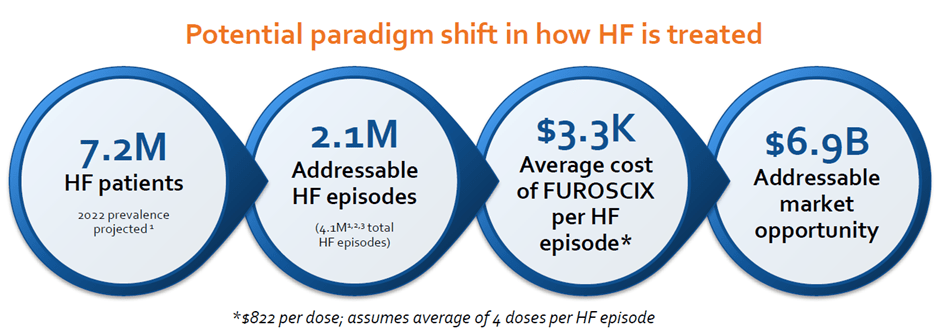

The prevalence of heart failure is around 7.2 M in the US and 15.8M in the G7 countries; in the US, around 4M HF events occur annually, and congestion is the key driver of hospitalization for patients above 65 years old. Heart failure is defined as a situation when the heart is incapable of maintaining a cardiac output adequate to accommodate metabolic requirements and the venous return, which means that the heart is not producing enough output to sustain the system. Cardiac output is defined as the volume of blood pumped out per unit of time, and it is a function of heart rate and stroke volume. Therefore, the definition of reduced ejection fraction heart failure (HfrEF) is defined as left-ventricular ejection fraction (LVEF) under 40%, meaning that the heart is not pumping out enough blood to meet our system’s requirement. The most common symptom of heart failure is dyspnea (shortness of breath), fatigue, weakness, and fluid retention (peripheral edema). Fluid retention is caused because our heart (right side of the heart) cannot pump enough blood out of the right atrium and to the kidney, leading to fluid retention in the periphery organs like the legs. If the left side of the heart is not functioning, it leads to edema in the lungs (pulmonary edema) as blood comes into the left side of the heart from the lungs. Coronary heart disease is the cause of 70% of the cases, and hypertension is the main leading cause of heart failure; if we can control hypertension, we can prevent 50% directly or indirectly by preventing the coronary heart disease manifestation; this is why heart failure is considered as largely a preventable disease. Other causes of heart failure are value disease, infections, drug/alcohol, congenital abnormalities, diabetes, pregnancy, and obesity. Diagnosis is based on i) clinical history, ii) physical examinations (rates, heart murmur, jugular venous dilation, bilateral ankle edema), iii) ECG/Echocardiography, and iv) biomarkers – natriuretic peptide (NT-proBNP).

FUROSCIX delivers loop diuretics through an on-body device

FUROSCIX (Furosemide SC) is an on-body device delivering SC furosemide, which has IV-like efficacy for diuresis, but with an increase in convenience through SC administration. We highlight that the device that SCPH selected is the same device that Repatha (PCSK9 inhibitor on-body infuser), meaning that the device is tried and tested, de-risking potential hiccups around device failure.

Furosemide is a loop diuretic, and the key rationale for using diuretics in HF is that HF is caused by fluid overload and decompensation of the heart. Using diuretics, we can expect symptomatic benefits that may perpetuate neurohormonal activation in HF, stimulating renin release and angiotensin 2 and aldosterone. Of note, no beneficial effect on mortality was shown using diuretics. FUROSCIX is indicated for the treatment of congestion due to fluid overload in adult patients with New York Heart Association (NYHA) Class II and Class III chronic heart failure. New York Heart Association (NYSE) classification system has four classes, patients with NYHA class 1 have no limitations, class 2 patients have slight limitations, class 3 patients have marked limitations, and patients in class 4 have severe to complete limitations of activity (symptoms appearing even at rest). However, FUROSCIX is not indicated for use in emergency situations or patients with acute pulmonary edema. When we analyzed the product label, we liked the fact that i) the label was broad and the label did not require patients to exhaust oral diuretics (by showing inadequate response), which can add more flexibility to prescribing FUROSCIX, and ii) there is no limit on the duration of use was mentioned, allowing prescriber to prescribe it multiple times a year. The key value proposition for FUROSCIX is that it can reduce in-hospital stays needed for IV diuretics while having superior efficacy compared to oral diuretics, and we believe FUROSCIX to be used readily as a bridge between oral and IV diuretics.

Many patients on stable oral diuretics experience worsening HF and fluid overload due to potential diuretic resistance. There are several theories around it, but we believe it could be because decompensation leads to a decrease in the oral bioavailability of diuretics or the effect of thiazide lost with eGFR falling under 30ml/min, decreasing the ability to reach the distal convoluted tubule of the nephron. The resistance could be overcome by increasing the dosage of loop diuretics, administering IV loop diuretics, or combining loop and thiazide diuretics together. Now with the approval of FUROSCIX, there is an additional option for patients and prescribers.

We highlight that worsening symptoms are the most common reason patients get hospitalized. When patients get hospitalized, they turn to IV diuretic; however, hospitalizing patients are expensive (>USD11.8k per patient (Milliman et al., 2017)), and many patients end up getting readmitted to the hospital after discharge within 30 days. Considering that Furoscix’s cost is around 3k (4 doses with USD825 per dose) are going to be used, this could offer almost USD 8k of saving vs. hospitalization. According to recent research, more frequent hospitalization for heart failure has been associated with disease progression, and the median survival drops significantly with multiple hospitalizations (1st hospitalization median survival 2-2.5 yrs, and 4th hospitalization 0.5-1 yr of median survival).

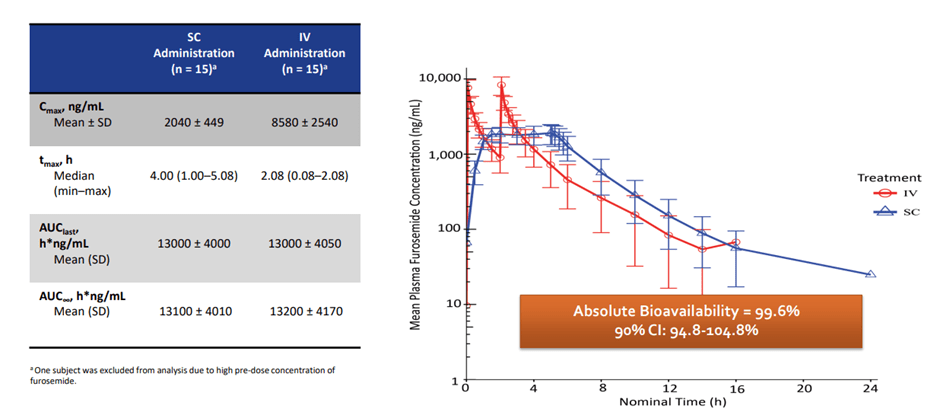

Pivotal PK/PD studies suggest IV vs. SC Furosemide concentration time was comparable between the two dosage forms.

PK/PD trial data of FUROSCIX (Sica DA, et al. JACC: Basic to Translational Science. 2018.)

We highlight that Furoscix was approved through the 505 b 2 pathway.

The 505 (b)(2) pathway provides manufacturers who have certain types of drugs with an opportunity to acquire FDA approval without performing all the work that’s required with an NDA. These drugs are not strictly generics, but are often not entirely novel new molecular entities either. Source

SCPH’s pivotal study showed that when 80 mg was administered over 5 hours in a biphasic delivery profile via the On-Body Infusor, 30 mg was delivered in the first hour, and 12.5 mg was delivered per hour over the subsequent four hours, Furoscix showed 99.6% bioavailability compared to IV bolus furosemide, which formed the basis for the FDA approval. Furthermore, we note that AT HOME-HF Pilot study showed FUROSCIX outside of the hospital setting can reduce cost, which will be used as key evidence for the company to secure attractive pricing negotiations with the payers.

The current valuation seems fairly modest; we expect peak sales of >500M

Heart Failure Market Size (Company)

Assuming that Furoscix captures 10% of the market share, we expect around 500-600M peak sales. Using a conservative peak sales multiple of x3, we get around 1.8Bn in enterprise value. Adding 100M of cash to the equation, we believe the valuation should be around 1.9Bn, which is almost x5 from the current valuation. Furthermore, we like the robust patent for FUROSCIX until 2034 (potentially up to 2040 with the recent patent filing) and a strong financial position with cash with ~USD100M (cash burn of ~USD60-70M) with the recent Oaktree debt agreement. We believe the company won’t need additional capital and have a cash runway for another 2 years, further de-risking potential risk around dilution.

We own a patent family directed to the composition of matter of our subcutaneous formulation for furosemide and methods of treating edema, hypertension and heart failure using the formulation of furosemide. This patent family includes one pending U.S. patent application, one pending patent application in each of Canada, China, Europe and Japan, and nine pending patent applications in other countries outside of the United States. Patents that issue from this patent family are generally expected to expire in 2034, excluding any additional term for patent term adjustment.

In addition, we own a patent family directed to methods of treating infections and other diseases using a tri-phasic or a bi-phasic dosing regimen of a time-dependent antibiotic, which methods can include subcutaneous delivery via a micropump or patch pump device. This patent family includes one pending U.S. patent application, one pending patent application in Europe, and one pending patent application in another country outside of the United States. Patents that issue from this patent family are generally expected to expire in 2035, excluding any additional term for patent term adjustment. Source

Risks

SCPH is marketing the product in-house; considering that cardiovascular disease is dominated by generic players and big pharma, it is possible that the sales ramp could be underwhelming (especially with a lean sales force of 40 that the company plans to deploy). Another risk could be market access, securing attractive pricing from payers. The drug seems to have secured an average wholesale price (AWP) of USD986.40 per box (4 units per course), which we believe is a better-than-expected price, and we are positive on the company’s ability to persuade the payer as the rationale around cost saving (from FREEDOM HF STUDY) is robust.

Conclusion

We are initiating SCPH with a buy rating even though we usually try to avoid first-time launchers because of three reasons a) the market opportunity of decompensated heart failure is lucrative, with>500M peak sales; b) FUROSCIX is already approved and has a clear differentiation (convenience, comparable efficacy, safety, and cost-saving) coming from SC dosage form, and c) the current valuation seems modest enough for us to risk buying into the launch.

Be the first to comment