Dilok Klaisataporn

Scotts Miracle-Gro (NYSE:SMG) has been one of my best picks over the past few months, giving a 57% total return since my last bullish take on the stock in October, far surpassing the 11% return of the S&P 500 (SPY) over the same timeframe. In this article, I revisit the stock and recent developments, and highlight why it remains a buy for risk tolerant investors, so let’s get started.

Why SMG?

Scott Miracle-Gro is one of the largest global marketers of branded lawn and garden care products for consumers. Its market-leading brands include Scotts, Miracle-Gro, Ortho, and through its subsidiary, Hawthorne Gardening Company, provides nutrients lighting and other materials used for indoor and hydroponic growing.

It’s no secret that SMG has seen challenges over the past year, as a broad opening of the economy has dampened sales on home gardening products. In addition, the cannabis industry is contending with oversupply issues, to which SMG has exposure through its Hawthorne hydroponics segment. These difficulties are reflected by sales declining by 33% YoY during the fiscal fourth quarter, driven by decreases in all four of SMG’s business segments.

Fiscal 2022 was clearly a year that SMG looks forward to putting behind it, and management sees potential for a rebound in the current fiscal year, guiding for low-single digit growth in adjusted operating income, and mid-single digit percentage growth in adjusted EBITDA.

Importantly, management expects to see free cash flow of $1 billion over the next two years. This would go a long way in covering SMG’s dividend commitment, which amounts to just $166 million per year. Management reiterated its commitment to paying the dividend and sees little to no benefit to leverage by cutting it, as expressed during the last conference call:

Regarding the dividend, we have no plans to touch it based on what we see today. The truth is that cutting the dividend entirely or even by a percentage does not move leverage that much. We’ve heard feedback from investors around this topic. Most of our largest shareholders have told us in clear terms, that we should not cut the dividend unless absolutely necessary. And here’s what I think about issuing more equity. Based on our current view, I do not believe it will be necessary. As always, we will evaluate our options and do what is required.

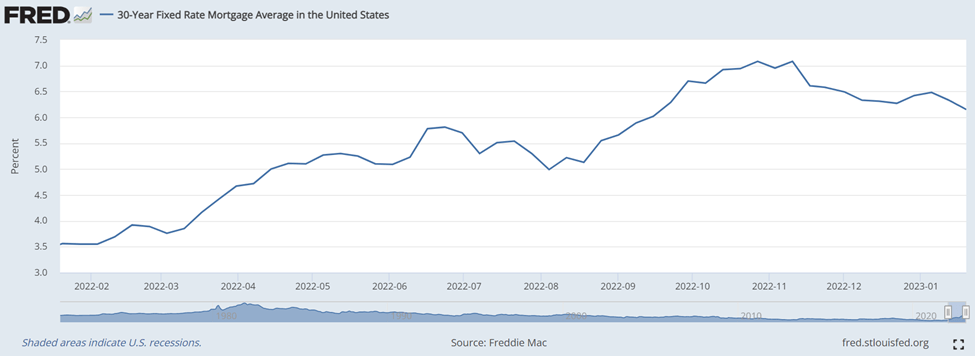

Looking forward, SMG may benefit from improving mortgage rates, as that drives transaction activity in the housing market, resulting in increased home gardening. Morningstar sees potential for a housing rebound next year, driven by lower mortgage rates, as noted during its recent analyst report:

We now project housing starts to decrease 18% year over year in 2023 to 1.275 million-down from our prior projection of 1.420 million units-which is about in line with the level of residential construction activity in 2018-19. However, we expect starts will begin to rebound in 2024 as lower mortgage rates and home prices improve affordability and entice buyers back into the market. Specifically, we project the average 30-year fixed mortgage rate will decline from 6.25% in 2023 to 4.5% in 2024, and we see new and existing home prices decreasing 15% and 5% between 2022-24, respectively.

Plus, as shown below, the 30-year mortgage rate has continued to dip since peaking in November of last year, and currently sits just above the 6% mark.

30-year Mortgage Rate (St. Louis Federal Reserve)

Those investing in SMG should be comfortable with its risk profile, as SMG racked up debt due to recent acquisitions. It carries a net debt to EBITDA ratio of 6x, and I would expect focus over the next couple of years to be around deleveraging the balance sheet.

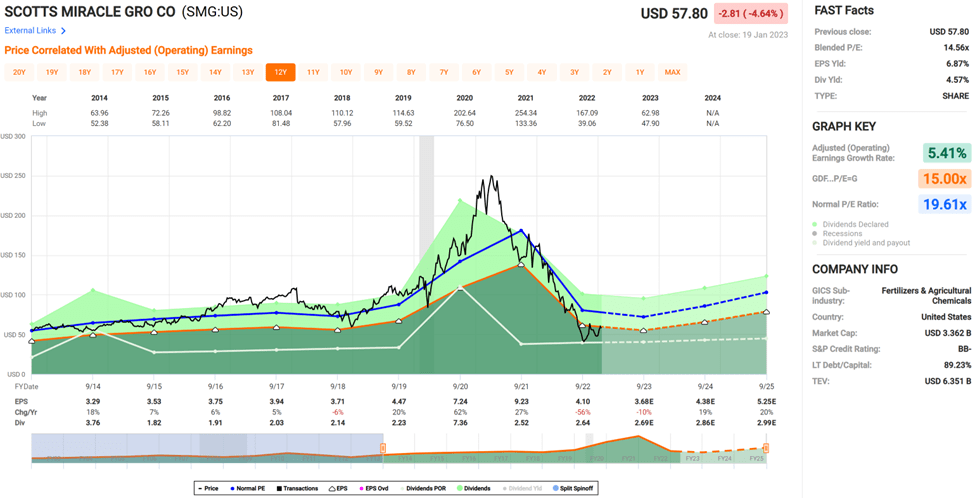

Nonetheless, I see value in the stock at the current price of $62, as many of the risks appear to be baked into the share price. SMG has a forward PE of 16.6 sitting below its normal PE of 19.6, and analysts expect to see robust 18 to 20% annual EPS growth in the following two years. This could be the case should the housing market rebound and the cannabis industry work through near term difficulties and stabilize.

SMG Valuation (FAST Graphs)

Investor Takeaway

Scotts Miracle-Gro is a major player in the lawn care, home gardening and hydroponics markets. It’s facing a number of challenges at the time, driven in large part due to a slow housing market. However, those headwinds seem to already be baked into the share price, as the stock is trading far below its 52-week high of $156. Meanwhile, management has reiterated its commitment to the dividend and the stock may be good choice for long-term risk tolerant investors.

Be the first to comment