Brett_Hondow

It is the first time that we write about Schneider Electric (OTCPK:SBGSF; OTCPK:SBGSY), but it is a company that we successfully held in the past which now is back to a compelling valuation. Despite being a market leader, it is not very well covered in Seeking Alpha, so today our internal team will provide the company’s deep-dive and a full analysis thanks to our initiation of coverage.

Schneider Electric is a French multinational corporation that engages its activities in two business units: industrial automation and energy management.

- Energy management is split into three specific areas:

- Low voltage engages its activities in finding solutions from data center needs to higher energy efficiency in private residential and non-residential end-market such as hotels, hospitals, etc.;

- Medium voltage provides services for companies with a more difficult and complex energy structure. End-markets are transportation, oil & gas corporation, and utilities;

- Secure power is a division that manages what in jargon is called “critical power and cooling“. This division offers its services to IT companies, financial service entities such as banks and insurers, and telco operators.

- Industrial automation engages in process automation with the most diversified clientele.

Schneider Electric was founded in 1836 and is headquartered in France. Despite being an European entity, the company has a global footprint. In 2021, revenue per geographical area was split into the following:

- APAC region accounting for 31%,

- North America region accounting for 29%,

- Western Europe region accounting for 26%,

- Rest of the World at 15%

Looking at the financials, in the 2021 account industrial automation represented 23% of the group revenue. Top line sales were at more than €6.7 billion with an EBITA margin of 18.5%. Whereas the energy management division accounted for 77% of the group sales with revenue of €22 billion and an EBITA margin of more than 20%.

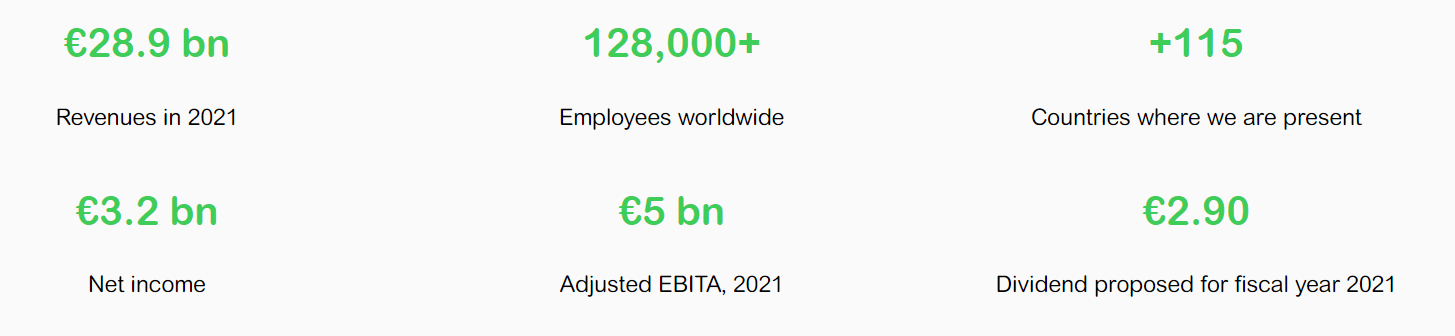

Schneider Electric at a Glance

Source: Schneider Electric Corporate Website

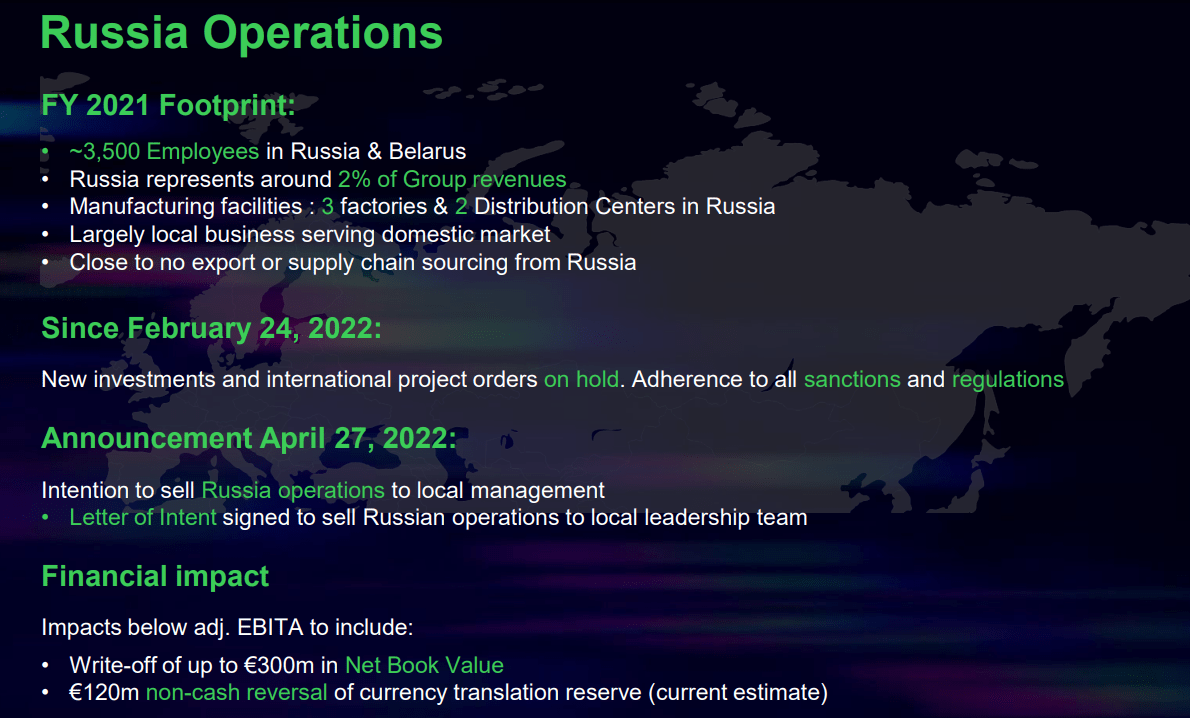

Before going deeper into the company’s long-term opportunity, the latest company announcement was on the sale of its Russian activity to local management. The snap below presents the main highlights.

Schneider Electric Russia activity

Aside from the financial consideration, we should say that no critical sources came from the Russian region.

Looking ahead

Ahead of the Q2 presentation that the company plans to report on the 28th of July, our internal team believes that Schneider offers the following MACRO to MICRO upside:

- First of all, manufacturing onshoring. This is an important topic that is becoming consistently stronger in the latest conversations. This is due to the higher logistic costs and continuous challenges in the supply chain;

- EV and residential building efficiency are driving demand in the energy management division (in particular in the low and medium voltage sector). This is amplified by the macroeconomics context that European countries are facing. RePower Act and energy independence will drive Schneider Electric’s future performance;

- Digitalization and IoT adoption will be supported by the company’s EcoStruxure platform, Schneider is targeting to build a hybrid digital company;

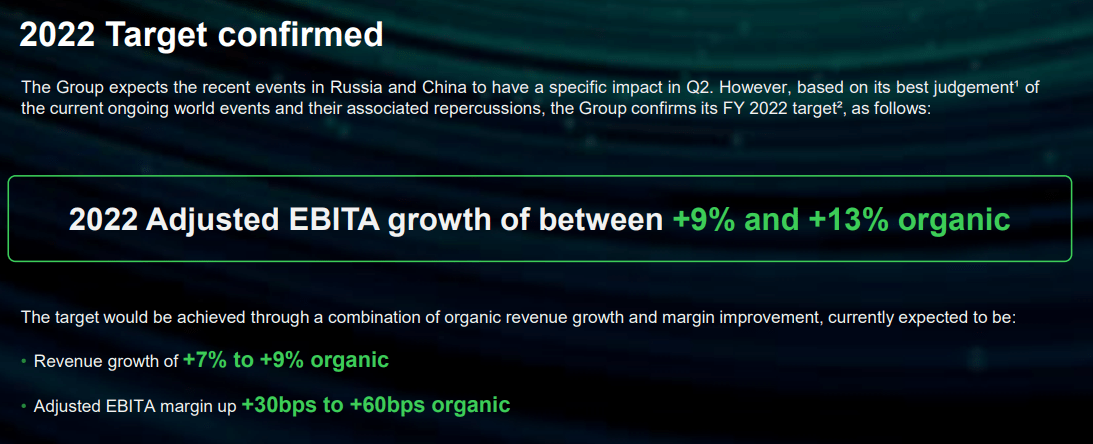

- Despite the Russian implication and the continuous and prolonged lockdown in China, the company maintained its 2022 guidance.

Schneider Electric 2022 guidance

On the company’s specific, we should also mention that Schneider is continuously reviewing its JV portfolio for strategic fit and better optimization. Last November, during the capital market day, they also targeted €1 billion in savings thanks to an operational efficiency plan to be carried out during 2022.

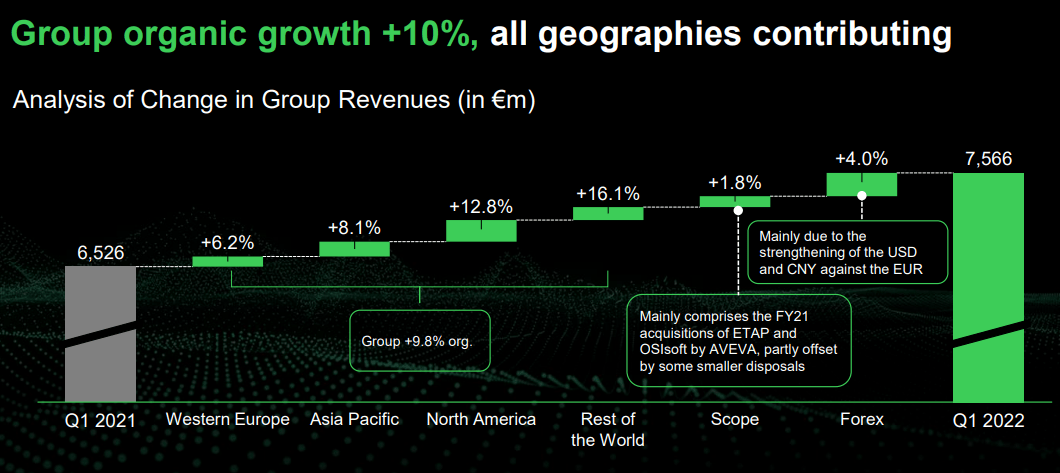

Adjusting our internal estimates in line with the management guidance (+0.6%), we raise the company’s EBITA 2022. This is supported by pricing power as achieved in Q1 (+6%) and also supported by further price action planned in Q2, favorable FX, and no more restrictions in China.

Schneider Electric Revenue Growth

Looking at a few more years ahead and given the strong track record, there is a real possibility to increase the adj. EBITA margin (higher than 21%) and FCF generation (higher than €4 billion beyond 2024) thanks to operational leverage and business mix evolution.

Conclusion and Valuation

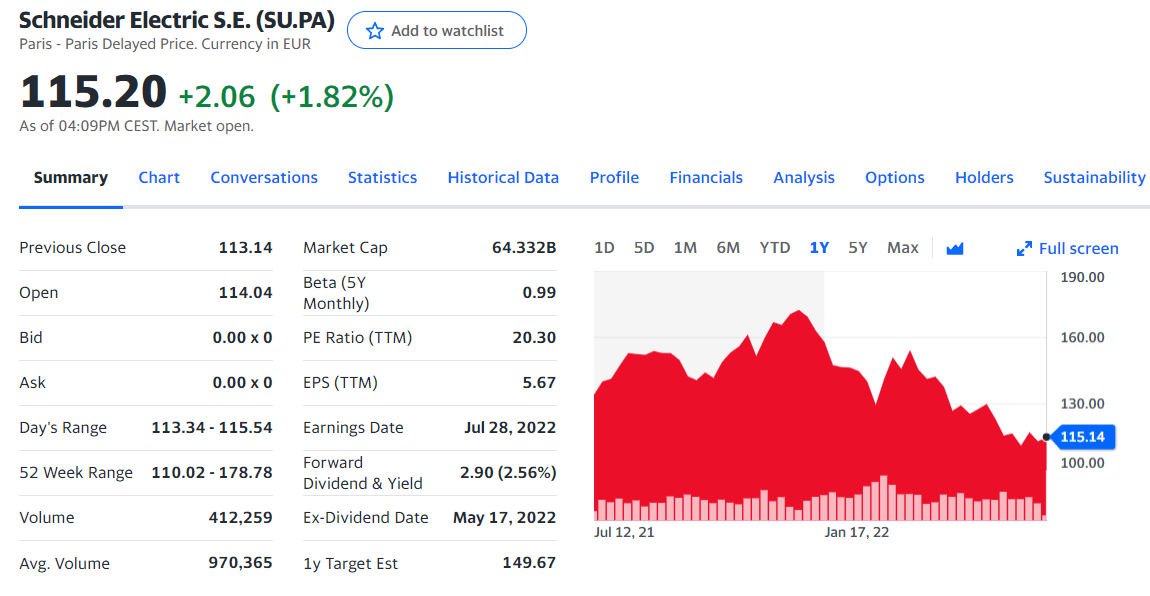

Despite what is going to be a weaker Q2 2022 from Schneider in China, fundamentals and strong execution continue to support the group’s operating performance. The company is currently trading on a 2023 Price Earning ratio of 16x and at an EV/EBITA level of 13.1x, which we find very compelling given the quality growth that Schneider offers. Eaton Corporation and Rockwell automation are trading on average at 22x PE and 15.8x on EV/EBITDA. This represents a significant discount that cannot be justified. We value Schneider Electric in line with its peers and we derive a target price of €165 per share.

Schneider Electric stock price evolution

Be the first to comment