Alpha potential of SCHD after 2 years of outperformance bondarillia/iStock via Getty Images

Introduction

If you think the Schwab U.S. Dividend Equity ETF (NYSEARCA:SCHD) is a defensive dividend ETF, you may change your mind after reading this article. My analysis of the ETF shows a higher indexation to the market than what would be considered a typical defensive play.

Furthermore, the top industries in SCHD have a future mixed with caution for the time being. Technicals also indicate relative underperformance vs the S&P500 (SPY) (SPX). Hence, I adopt a ‘hold’ stance on SCHD.

SCHD Industry Exposure Mix

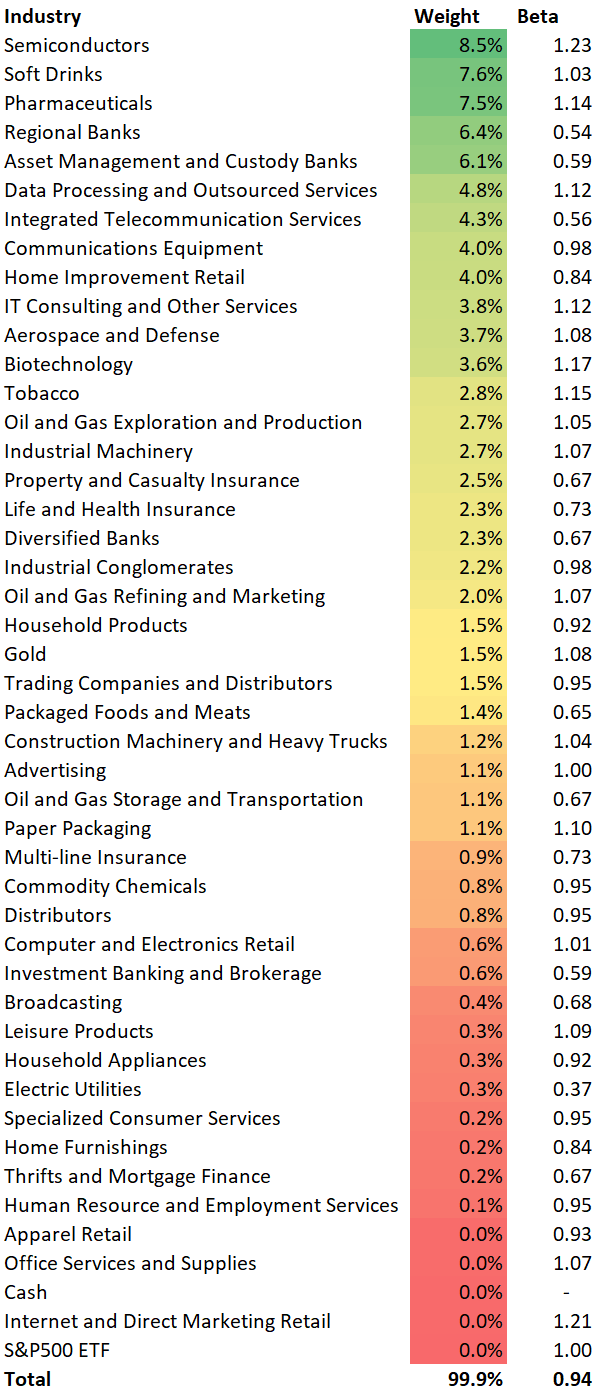

Other Seeking Alpha analysts have done a good job of giving a broad sector exposure and holdings exposure overview of SCHD. To offer new points of discussion to the conversation, I have looked a bit deeper into the underlying industry exposures and their betas to reveal some interesting insights:

SCHD Industry Exposure Mix (SCHD ETF Website, Author’s Analysis)

To my surprise, I found the cyclical semiconductors industry and the volatile pharmaceuticals industry right at the top in terms of sector weights. These industries have a beta much higher than 1, which some may argue is a bit uncharacteristic of high-dividend yielding companies in traditional sectors.

Another interesting observation is that the weighted average beta exposure for SCHD is 0.94; representing only 6% lower volatility vs the broader market. I believe this should raise some questions about certain assumptions about the defensive characteristics of this ETF.

The top industry exposures along with their weights are banks (12.5%), semiconductors (8.5%), soft drinks (7.6%) and pharmaceuticals (7.5%). Let’s explore the key fundamental drivers for these pieces:

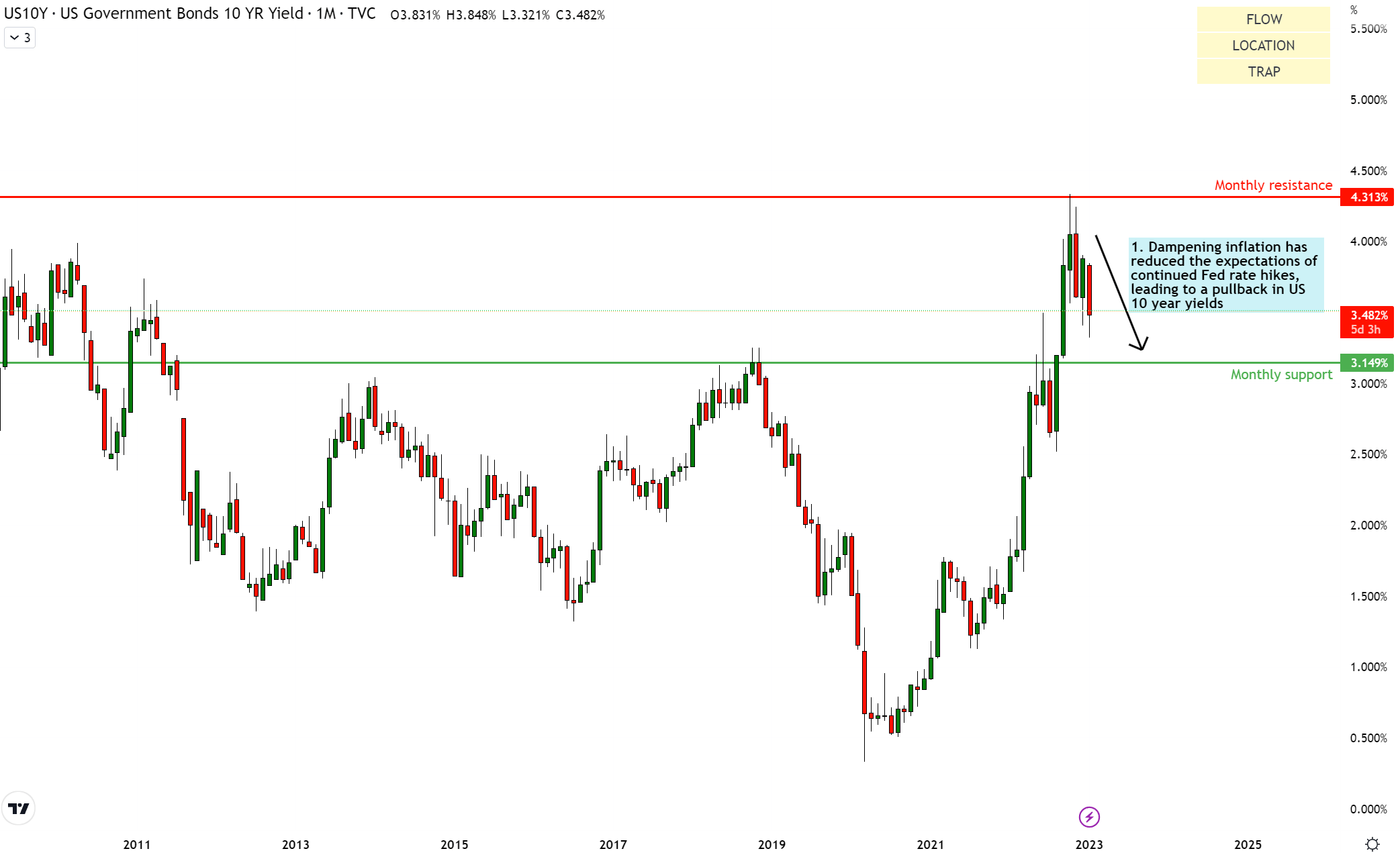

Banks

Banks tend to have higher net interest margins (NIMs) when interest rates are higher. The US 10-yr yields tend to be a good proxy for longer term interest rate expectations. Currently, the US 10-yr yields are undergoing a pullback after a broadly consistent move up since early 2021:

US 10-yr yields (TradingView, Author’s Analysis)

This would result in some incremental moderation for banks’ profitability levels in upcoming quarters.

Semiconductors

Latest earnings call commentary from the world’s largest foundry TSMC (TSM) suggests continued weakness in the sector driven by end-client slowness in demand. Management suggested that the semiconductor industry is likely to recover in H2 of 2023. H1 of 2023 is expected to see a sales decline of 5-9%, with most of the decline coming in the March 2023 quarter.

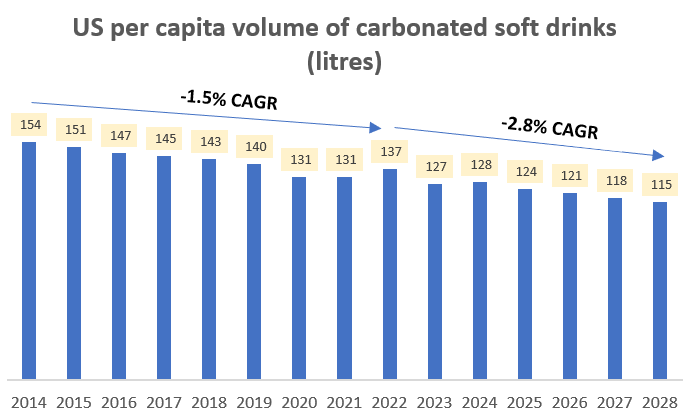

Soft drinks

A shift towards healthier eating habits coupled with the government’s fight against soda are long term inhibitors of soft drink market growth in the US. Data from Statista Consumer Market Insights shows that after a -1.5% CAGR from 2014 to 2022, there is expectations of an accelerated decline with -2.8% CAGR over 2022 to 2028 in the US per capita soft drink consumption:

US per capita soft drink consumption (Statista, Author’s Analysis)

Pharmaceuticals

As mentioned in my previous analysis of Vanguard Health Care ETF (VHT), the US pharmaceutical industry is facing a loss of $200 billion in revenues. This is due to governmental pressures to reduce the cost of prescription drugs as part of an all-round effort to curb inflation.

Takeaway

All in all, I believe the aforementioned headwinds in SCHD’s key industries will hinder the dividend ETF’s performance in the quarters ahead.

Technical Analysis

If this is your first time reading a Hunting Alpha article using Technical Analysis, you may want to read this post, which explains how and why I read the charts the way I do, utilizing principles of Flow, Location and Trap.

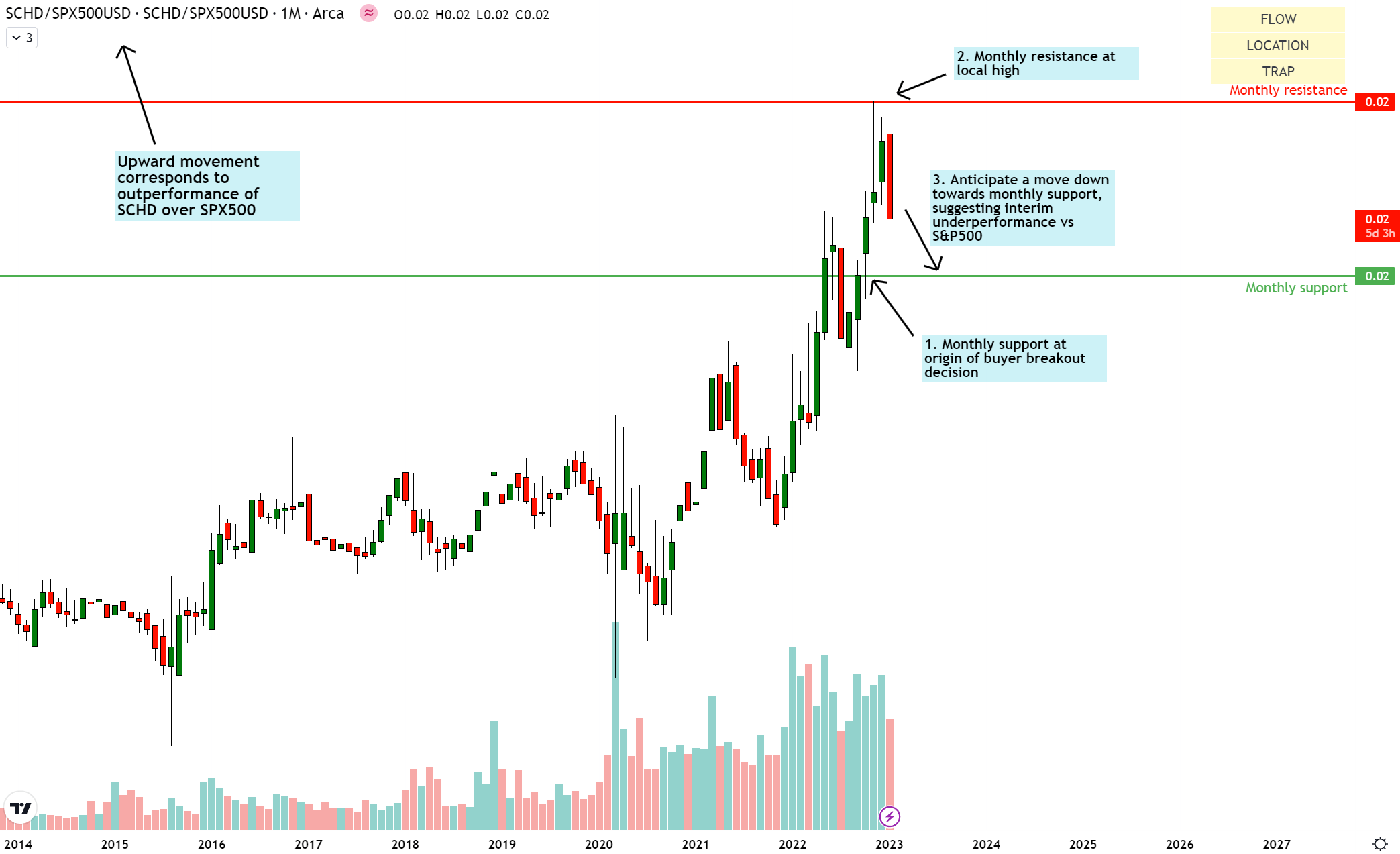

Relative Read of SCHD vs SPX500

SCHD vs SPX500 Technical Analysis (TradingView, Author’s Analysis)

After broadly consistent outperformance over the S&P500 (SPY) (SPX), SCHD is printing a bearish engulfing and looking like it is due to go down toward the monthly support. Such a move would result in more underperformance over the S&P500 ahead for SCHD.

Standalone Read of SCHD

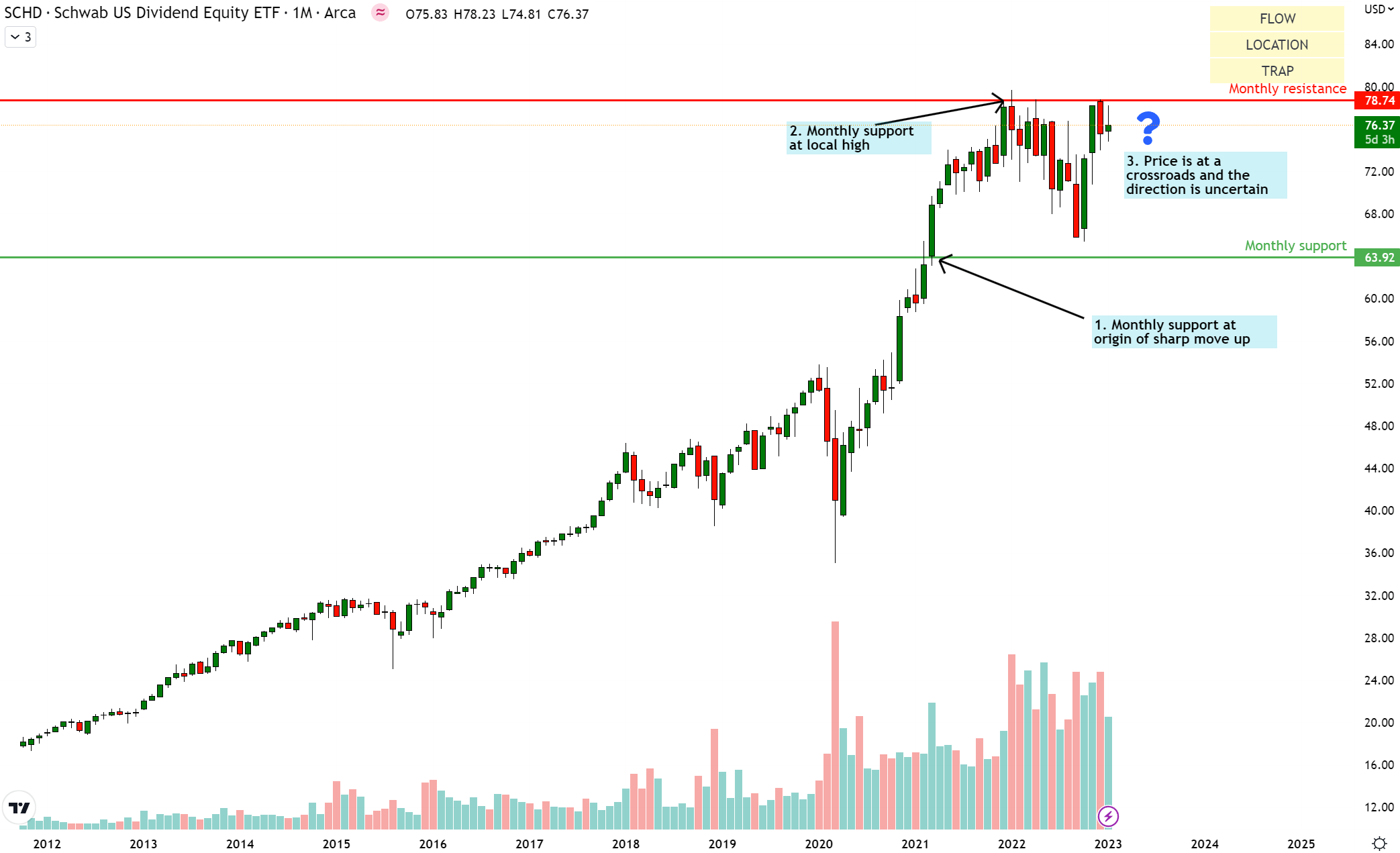

SCHD Technical Analysis (TradingView, Author’s Analysis)

On the standalone chart of SCHD, price is currently at a crossroads in between the $63.92 monthly support and the $78.74 monthly resistance. I do not have a clear anticipation on its direction. However, its location towards the top end of the range makes me doubly cautious of buys.

Conclusion

Overall, a closer look at the industry exposures reveal that SCHD is not as defensive as it seems. There are also various headwinds affecting the dividend ETF’s top industries, which I think will hold back SCHD’s performance over the next few months and quarters. Technical analysis of SCHD relative to the S&P500 also agrees with this notion, suggesting a period of continued underperformance vs the broader market. For these reasons, I am not a buyer of SCHD here.

Be the first to comment