Luke Chan

Thesis

I view the insurance vertical as one of the most attractive sub-segments in the software sector, with customer relationships between pure-play software providers and insurance carriers often spanning decades. Sapiens International Corporation N.V. (NASDAQ:SPNS) has a broader market focus, as it offers additional IT services and products within Life & Annuity (L&A) insurance, Workers’ Compensation, reinsurance, and financial markets services. I expect SPNS’s top line growth to slow down owing to gains by Guidewire Software, Inc. (GWRE) and Duck Creek Technologies, Inc. (DCT) and higher FX headwinds due to the high revenue (almost 60%) generated outside North America.

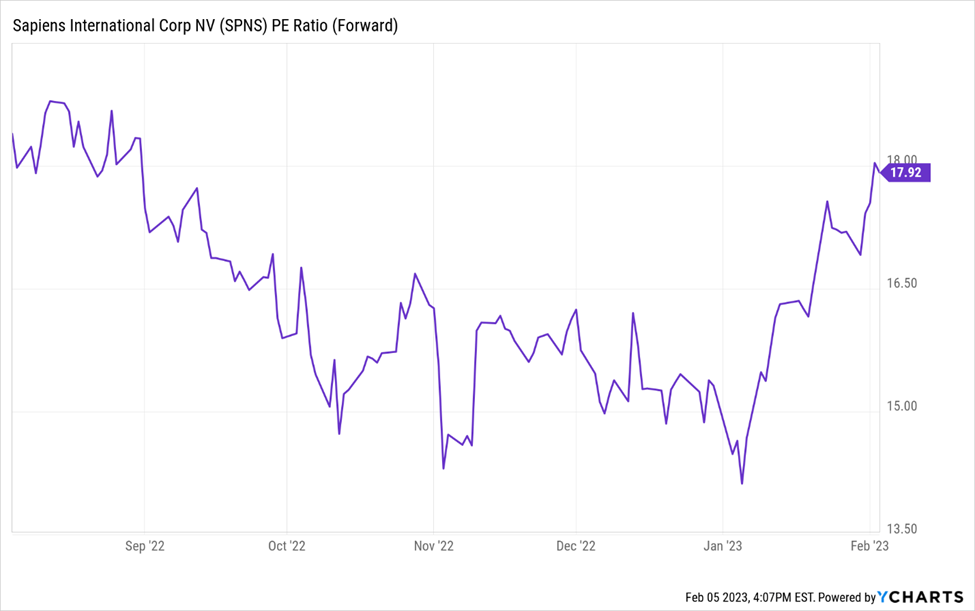

Trading at a forward P/E of 18x, I see Sapiens International Corporation N.V.’s shares trading at fair value and see limited chances of higher multiple re-rating in the medium term. Therefore, I remain Underweight on SPNS with a preference for GWRE and DCT shares.

Company Description

Sapiens International Corporation N.V. is a software provider to the P&C (Property & Casualty) and L&A (Life and Annuity) insurance markets, as well as Workers’ Comp and Medical Malpractice. Sapien’s key products are core policy, billing, and claim solutions. SPNS also has add-on offerings, including Data & Analytics, ML-based use cases, Digital Engagement platform (including customer and agent portals), chatbots, and low-code/no-code digital journey builder—all of these tools targeted at improving customer transition away from outdated legacy systems.

Why I Remain Underweight?

Growth profile

Given its origin, Sapiens International Corporation N.V. has a big focus on European insurance carriers and has been relatively acquisitive in the region, which helped the company deliver a 17% revenue CAGR over the past three years. However, over the coming three years, I expect SPNS growth to slow below its closest peers GWRE and DCT, both of which are benefiting from a more visible large customer transition to the cloud. This is partially reflecting more pronounced FX headwinds for SPNS vs. peers due to the high revenue (almost 60%) generated outside North America.

Competition

GWRE and DCT, in my opinion, pose the biggest threat to the growth potential of SPNS in the U.S. and among Tier 1 as well as Tier 2 players. Additionally, GWRE is already an established market leader in the P&C insurance space and has a strong presence in Europe. DCT is also beginning to roll out more aggressively outside of the U.S., meaning that SPNS is going head-to-head with these competitors (which could hamper revenue growth and profitability).

Sapiens revenue remains dominated by services

The majority of SPNS revenue remains driven by services and implementation: should the company be unsuccessful in driving the shift toward more lucrative software subscriptions and cloud-based solutions, it could cap both topline growth and margin expansion potential.

System conversions slow with growing claims payouts

The combination of global macro weakness and a larger-than-normal volume of tropical storms and wildfires is putting pressure on the P&C carriers, which have been flush with reserves in the last several years. This brings into question the level of motivation of those insurance carriers to continue system modernization projects. Should IT spending slow on insurance digitalization projects, it could potentially dampen revenue growth and hinder performance.

Financial Outlook

Slowing forward revenue CAGR

I do not believe Sapiens International Corporation N.V. can expand its revenue at the same pace as GWRE and DCT. Subscription / SaaS remains a relatively smaller portion of Sapiens business, and expect focus on providing IT services as well as implementation to remain a key component of the revenue mix.

GM and OPM to remain stable

I think SPNS’s GM is weighed on by Services, which represents roughly two-thirds of SPNS’s total revenue. SPNS offers more “in-house-support” versus GWRE and DCT, which equip systems integrators for support functions. Because I do not see Subscription representing a larger mix of SPNS’ business profile over time, I expect the company’s GM to remain stable and not face such pronounced operating leverage as I see with GWRE and DCT. I also do not foresee major changes to SPNS operating expenses as a percentage of revenue. I expect selling, marketing, general, and administrative to collectively continue to be an expense of about mid-teens of consolidated revenue.

Valuation

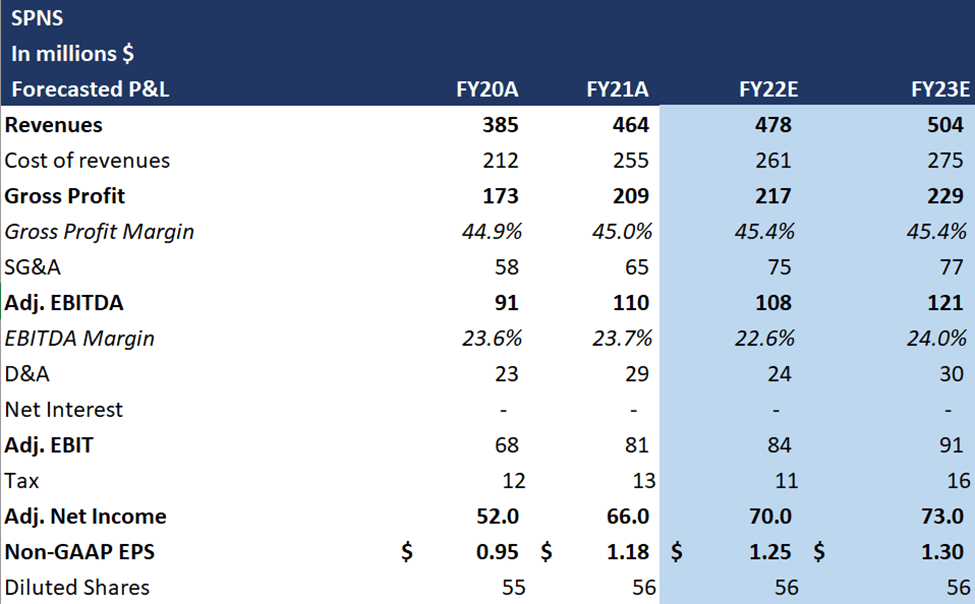

My Dec 2023 price target of $23.4/share is based on an FY23E Forward P/E of 18x (current multiple). I believe that there is a very limited probability of multiple re-rating given the company’s growth profile and SPNS’s revenue mix.

SPNS’s forecasted P&L (my estimates) SPNS forward PE ratio (Ycharts)

Upside Risks

Growing presence and better profitability in the U.S.

Sapiens may be able to accelerate growth of its U.S.-based revenues (which have been lagging other verticals in the past few years) and improve profitability of U.S.-based operations (SPNS P&C North America has so far been roughly breakeven, diluting profitability of the overall operations).

Growth boosted by FX and M&A

SPNS has been showing relatively healthy organic constant currency growth (closer to the bottom of the defined range of 8-11%). While this implies visibly lower reported rates due to the U.S. dollar’s strength against other international currencies, should currency trends reverse, a weaker USD may lead to accelerated SPNS growth trends. Sapiens also has a strong M&A track record and could boost the top line through tuck-in deals as valuations of potential acquisition targets have de-rated, given macro weakness.

Final Thoughts

I expect Sapiens International Corporation N.V.’s top line growth to slow down owing to gains by GWRE and DCT and higher FX headwinds due to the high revenue (almost 60%) generated outside North America. Sapiens International Corporation N.V. stock is currently trading at fair value, in my view, and I see limited upside given SPNS’s growth profile. I remain underweight on the company’s stock and have a preference for GWRE and DCT in the sector.

Be the first to comment