The Eye Of Sauron aka The Salesforce Tower, By Day DianeBentleyRaymond/iStock via Getty Images

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Cestrian Capital Research, Inc., its employees, agents or affiliates, including the author of this note, or related persons, may have a position in any stocks, security, or financial instrument referenced in this note. Any opinions, analyses, or probabilities expressed in this note are those of the author as of the note’s date of publication and are subject to change without notice. Companies referenced in this note or their employees or affiliates may be customers of Cestrian Capital Research, Inc. Cestrian Capital Research, Inc. values both its independence and transparency and does not believe that this presents a material potential conflict of interest or impacts the content of its research or publications.

Founder DNA Remains Very Much In The Building

To start a company you have to be a little bit odd. Because it’s scary and difficult. Even if you already have a boatload of money, as did Marc Benioff when he began the 1-800-NO-SOFTWARE journey (Salesforce (NYSE:CRM) original strapline – back when people made phone calls!), you have much at stake. Reputation with peers, superiors, inferiors, family, friends, your pet dogs. Opportunity cost – should you just keep taking the corporate dollar? And the other kind of opportunity cost that comes with never being able to dial it in, on account of, well, it’s your business, so who exactly are you kidding with your WFH game?

To still be running the company you founded, a couple decades later, when you could have declared success, cashed up already and then bought the little of Hawai’i you didn’t already own – you have to be stranger still. Why schlepp to work every day when you don’t need the money, your standing as the Hairy Cloudfather is cemented in Valley history, and frankly the company you run is now likely to be the next roadkill for the pesky kids down the road who keep using the word “legacy” around you, much to your chagrin.

The answer is, the need to control, and to win, and to keep winning, and to keep controlling the win. In many aspects of life this is undesirable. But in business? It’s the most wonderful aspect a CEO can bring to the party. All that stuff about teamwork and blah? That’s just HR acting on behalf of the controlling CEO. They mean, you down there, you grunts, you work as a team. (Because it dilutes the influence of any of you that might look like a challenger.) Me? Despicable me? There’s no Me in Team! Get back to work!

Someone at Salesforce keeps telling Benioff that he should stand aside, step back, do less, surf more. And he keeps pretending to do it. Twice now he has hired a “co-CEO” (like that’s even a thing!) and then thrown them under the tram as it passes by the Eye of Sauron down there on Mission. Probably for yucks and irony these guys get tossed out the window from the Ohana Floor. Yes, that’s a thing.

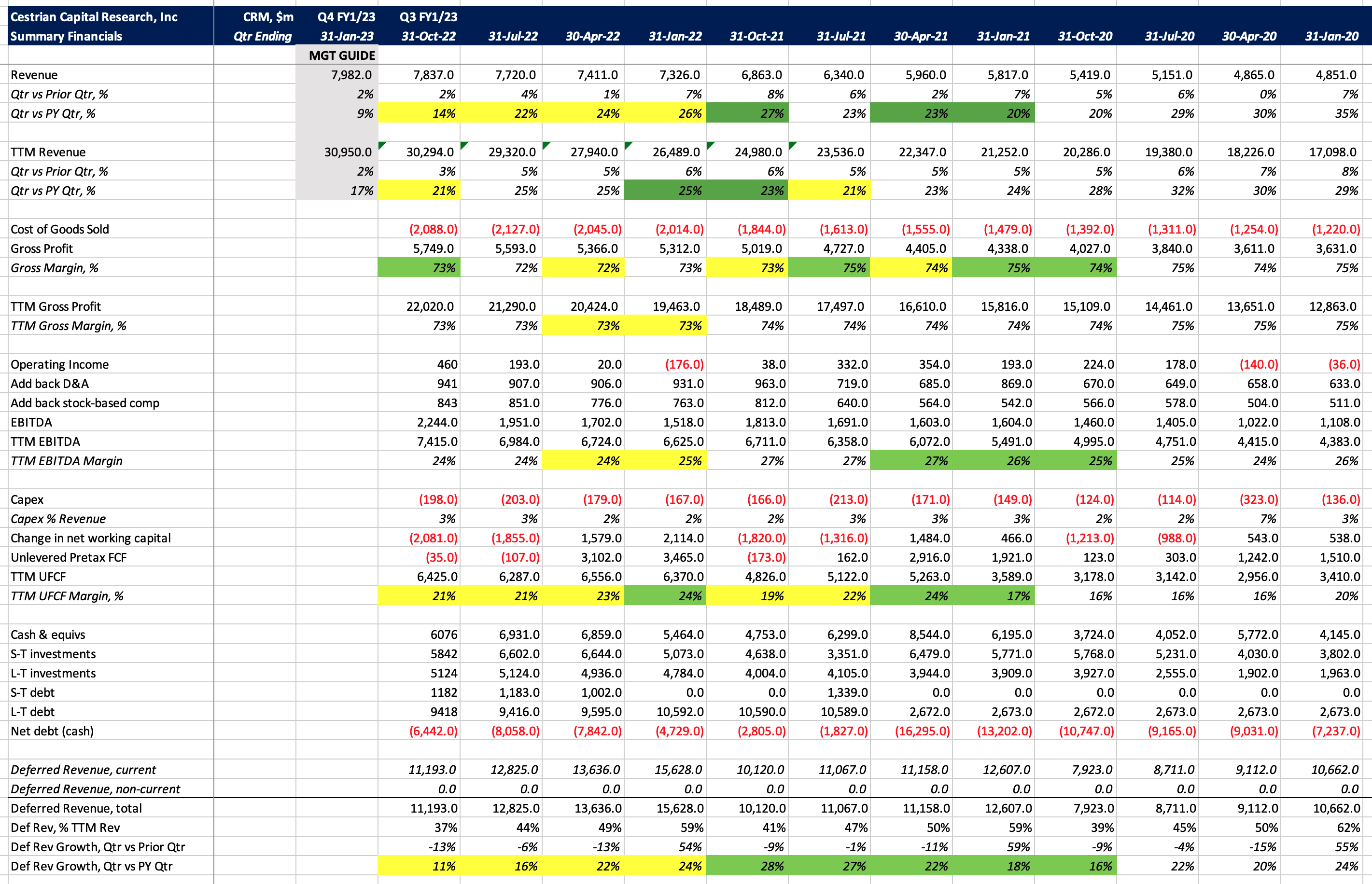

We’ll get to the numbers in a moment. They were fine. But look – this is the most important thing in the Salesforce print after the bell today:

Order Is Restored (Salesforce.com Investor Relations )

Taylor just found out he wanted to spend more time away from his family building a new business. Leaving the Big Guy back in the Big Chair. Actually, both Big Chairs, the CEO’s and the Chairman’s. Giving it the back-in-the-day governance structure, for all the progressive warrior image projected into the mean streets.

This we see as bullish. Salesforce is a subscription business which means it offers long-run visibility into the future, more so than companies with a purely contingent revenue model at least – and if you have been managing it for decades you can see way beyond the books and into the future based on all kinds of tangible and intangible inputs. If you thought this thing was headed for the abyss, you would likely keep the co-CEO thing in place thus to be able to share the blame and/or dump all the blame on The Other Guy, viz. Sheryl Sandberg’s fate at Meta Platforms (META). Or even just bail now and then you can blame all of it on the newcomers. That Benioff has simply decided to get his ball back and play on as the sole forward? That’s bullish in our view.

OK. Numbers:

CRM Financial Fundamentals (Company SEC filings, Cestrian Analysis)

- Revenue growth continued to slow – +14% in the quarter vs the same quarter last year, and the slow-burn TTM measure fell to 21% YoY. (The Q4 guide suggests a full year outturn of +17% revenue growth, down from +25% last year.)

- Gross margins held up fine in the low 70%s.

- TTM EBITDA and TTM unlevered pretax free cash flow margins also held steady at 24% and 21% respectively.

- Deferred revenue (that’s the element of customer contracts which have been signed, invoiced, but not yet delivered) growth fell to just +11% vs. prior year.

- (Not shown in the table) – remaining performance obligations, that’s the total customer contract book of signed agreements whether invoiced or not – sat at $40bn – a little under 2x TTM revenue and up around 11% on prior year. “Current” RPO – which the company expects to recognize as revenue in the next twelve months – sat at $20bn, just a little less than TTM revenue. This is why subscription businesses are so wonderful. You could fire pretty much all the salespeople and the company would still deliver next year flattish on this year. And if you focus the sales team correctly, as we expect Benioff to do, well, you have next year in the bag already so they can go win all the upside.

- Balance sheet remains rock solid with $6.4bn net cash – or if you were to write down all their “strategic investments” (which will include illiquid stakes in many companies) to zero, the balance sheet would still have $600m net cash whereas in truth they should be running a leveraged outfit here – it’s capital inefficient to not do so.

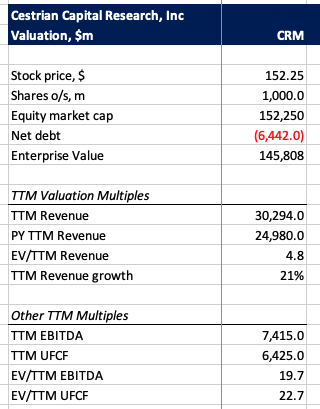

Let’s look at the valuation.

CRM Valuation (Company SEC filings, YCharts.com, Cestrian Analysis)

In fundamental analysis, this valuation is known as “meh.” Not overly expensive for the growth and margins, but not overly cheap either. Meh.

Finally the stock chart. You can open a full page version, here.

We think the stock can be accumulated at these levels and identify an upper and lower bound for such slow-burn building a position. Our chart shows the stock rising up out of a low bottom. This can form a new larger-degree Wave 3 which can read the Wave 1 high and more. Price target? $312 – the previous Wave 1 high – will do for now. We’ll keep you posted.

Accumulate rating.

Cestrian Capital Research, Inc – 30 November 2022.

Be the first to comment