Miro Nenchev

Star Bulk Carriers (NASDAQ:SBLK) will release its fourth-quarter financial results on 16 February. In its 3Q 2022 financial results, the company reported a net income of $110 million, compared with $200 million in 2Q 2022 and $220 million in 3Q 2021. Due to the high-interest rates in the United States and European countries, the war in Ukraine that has boosted trade disruptions, and China’s lockdowns, the demand for dry bulk shipping services decreased further in the fourth quarter of 2022. Thus, I expect SBLK’s 4Q 2022 net income to be lower than in 3Q 2022. Here is the link to my previous analysis on SBLK. Also, despite the sudden reopening of China that sparked hopes for the recovery of iron ore shipping, the Baltic Dry Index decreased for the sixth consecutive week in the week ending 10 February 2023. However, it is important to know that in the past two weeks, China’s steel production and consumption increased significantly. Also, due to the favorable market condition in 2021 and the first half of 2022, the company was able to improve its financial performance, and with a relatively good liquidity position, even with the current market condition, SBLK will remain profitable and can remain financially healthy. The SBLK stock is a hold.

The market outlook

On 2 February 2022, the Federal Reserve increased its key rate by 0.25 percentage point to 4.50% (it was the eighth rate hike since the Fed started increasing the federal funds rate a year ago to combat inflation). The interest rates in the United States are now at their highest levels within the last 15 years, and as the inflation rate in the United States is still high, Jerome Powell, the Fed’s chair, has said that to control inflation, further interest rate increases are needed.

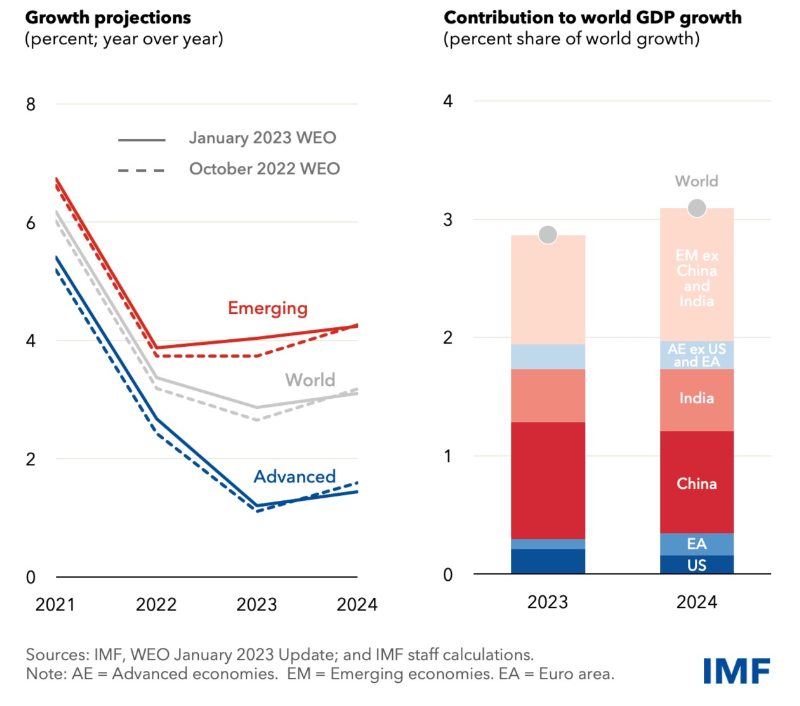

Due to the central banks’ measures to combat inflation in Major economies and the continuing war in Ukraine which weighs on economic activities, the contributions of the United States and European countries to global economic growth are not significant in 2023. However, the reopening of China may support global economic growth. According to IMF, global growth will slow from 3.4% in 2022 to 2.9% in 2023 and then rebound to 3.1% in 2024. It is important to know that based on IMF’s estimations, China may experience a significant growth rate of up to 5.2% in 2023 (see Figure 1).

Figure 1 – Global growth outlook

IMF

As a result of the weak global demand for dry bulk vessels in the past few months, and despite the hopes for iron ore demand recovery in China due to reopening, the Baltic Dry Index recorded its sixth consecutive weekly fall for the week ending 10 February 2023 (see Figure 2). As of 10 February 2023, the Baltic Dry Index is down 69% YoY. The decreasing Baltic Dry Index in the past six weeks could be explained partly by the cold weather and new year celebrations. Thus, the slightly positive effect of China’s reopening on iron ore demand and dry bulk shipping activities could be expected in the next few weeks. However, it is important to know that iron ore shipment in the first three weeks of 2023 was significantly lower than in previous years, implying that we cannot expect significant growth of iron ore shipping because of the end of the new year celebrations and winter season.

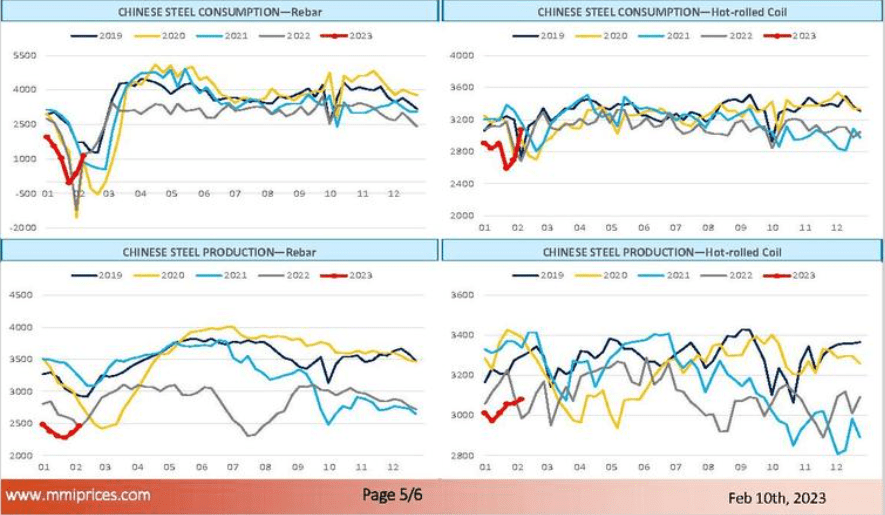

Figure 3 shows that Chinese rebar production increased sharply in the past two weeks. For the week ending 10 February 2023, Chinese rebar production was just about equal to the same week a year ago. Also, it shows that Chinese hot-rolled coil production in the week ending 10 February 2023 was more than the same week last year. Furthermore, Chinese rebar and hot-rolled coil consumption increased sharply in the past three weeks.

Figure 2 – The Baltic Dry Index

tradingeconomics.com

Figure 3 – Chinese steel production and consumption

mmiprices.com

SBLK performance outlook

I looked at Star Bulk Carrier’s profitability and liquidity ratios in this thorough article to assess how well the company can turn a profit and use its assets to make money for its investors. I have examined the profitability ratios for margin and return ratios to provide useful insights into the financial health of the company. I calculated the ratios in comparison to earlier quarters to be more helpful.

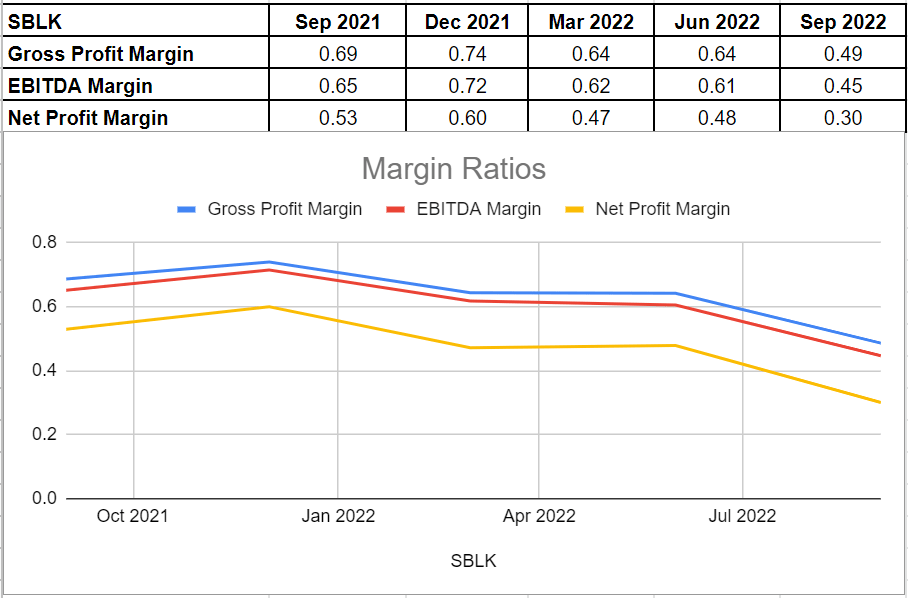

In general, margin ratios evaluate the ability of the company to turn revenues into profits in a number of ways. Overall, due to the shortcomings of the dry bulk market in 2022, this shipping company had weaker gross profit, EBITDA, and net profit margins compared with the end of 2021. In minutiae, the total revenue of Star Bulk declined by 12% from $417.3 million in 2Q 2022 to $364 million in 3Q 2022. A decline in revenue combined with the lower level of profits and EBITDA led to lower margin ratios in the second quarter of 2022.

SBLK’s gross profit was 0.49 in the third quarter of 2022, which is far lower than its amount of 0.64 at the end of 2Q 2022. Also, the company’s EBITDA margin was 0.45 in 3Q 2022, which is about 30% lower year-over-year compared with its amount of 0.65 at the same time in 2021. Moreover, Star Bulk’s net profit margin, which is the final picture of how profitable the company is after all expenses, dropped considerably to 0.30 in 3Q 2022 versus its previous amount of 0.48 at the end of the second quarter of 2022. As a result, the weakening market conditions in the preceding year affected Star Bulk Carrier’s revenue and declined its margin ratios (see Figure 4).

Figure 4 – SBLK’s margin ratios

Author (based on SA data)

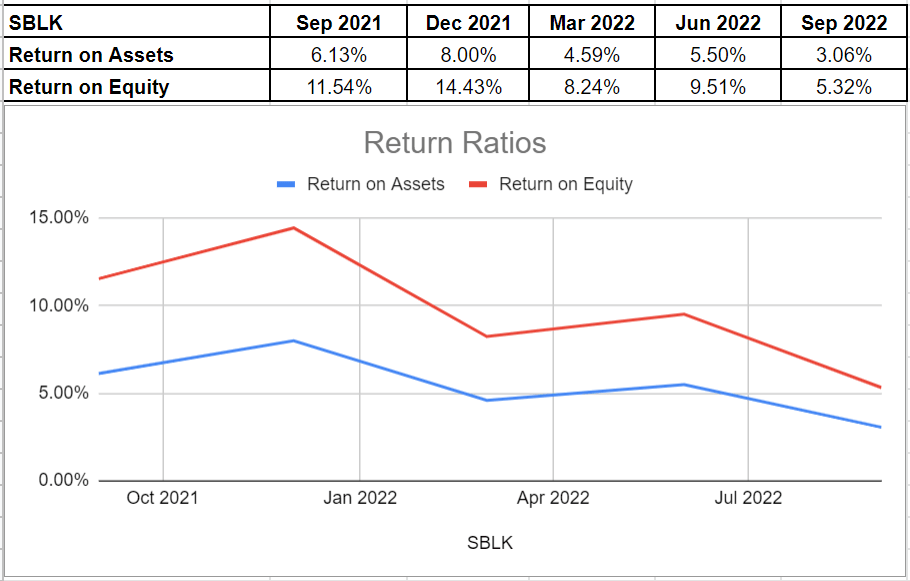

I looked into SBLK’s return on equity and return on assets ratios to show how well the company can tailor returns to its shareholders. The ROA ratio illustrates the amount of profit a company may produce for each dollar of its assets. The ROA ratio of 3.06% for Star Bulk Carrier in 3Q 2022 decreased by 307 bps year-over-year compared with its level of 6.13% in 3Q 2021. Additionally, its return on equity of 5.32% in the third quarter of 2022 is far lower than 9.51% and 11.54% in 2Q 2022 and 3Q 2021, respectively. ROE ratio shows the company’s net income concerning shareholders’ equity and is important since it calculates the rate of return on the capital invested in the business. The company’s net income of $200 million dropped considerably in the second quarter of 2022 to $109.7 million in the third quarter of 2022 and thus affected its return ratios. It means that the return ratios of Star Bulk could indicate that the return circumstances of the corporation weakened due to the deficiency of the dry bulk market; to be honest, I anticipate similar results for the fourth quarter of 2022 (see Figure 5).

Figure 5 – SBLK’s return ratios

Author (based on SA data)

To wrap up the company’s performance outlook, I analyze Star Bulk’s liquidity by considering its cash and current ratios. Notwithstanding shortcoming profitability results, SBLK’s liquidity analysis indicated a better picture. A slight increase in SBLK’s assets and a decrease in liabilities affected the company’s current ratio of 2.10 in 3Q 2022 to increase by 16% year-over-year compared with its amount of 1.81 at the same time in 2021.

Furthermore, for an 8% increase in the company’s cash balance in 3Q 2022 year-over-year compared with 3Q 2021, its cash ratio improved slightly to 1.33 in the third quarter of 2022 from 1.23 at the same time in 2021. In short, Star Bulk’s liquidity position paved a constant path with a slight increase during the previous year (see Figure 6).

Figure 6 – SBLK’s liquidity ratios

Author (based on SA data)

Summary

I expect Star Bulk’s fourth-quarter financial results to be weaker than in 3Q 2022. Also. The sudden reopening of China has not been able to offset the negative effects of global inflation and the war in Ukraine on dry bulk shipping demand. However, even with the current market conditions, SBLK is financially healthy enough to remain profitable. SBLK is a hold.

Be the first to comment