nightman1965/iStock via Getty Images

During the past few months, dry bulk shipping has suffered large losses due to various factors. From the monetary tightening to the Russia – Ukraine war, dry bulk companies have been hit hard. After reaching record highs in the summer of 2021, the Baltic Dry Index has been continuously declining during the recent months, with the exception of the last few weeks. The largest volatility has been observed in the larger vessel segments, and especially in the Capesizes. It has been a rollercoaster and definitely not for the faint-hearted.

In this context, there’s Safe Bulkers, Inc. (NYSE:SB), a company which owns a total of 44 vessels, from Kamsarmaxes to Capesizes while it also awaits for the delivery of 9 newbuilds (7 Kamsarmaxes and 2 Post – Panamaxes).

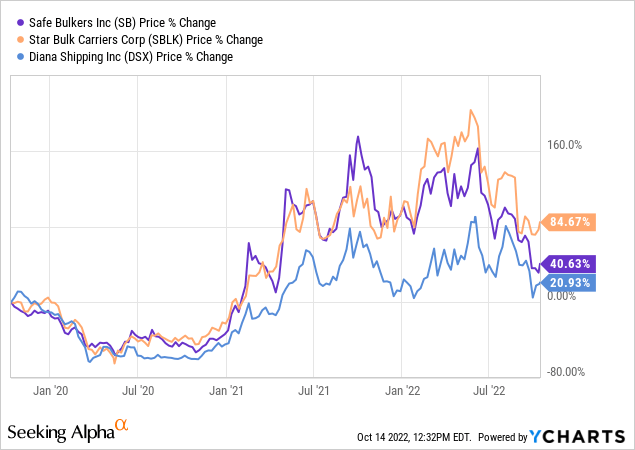

As we can see in the chart presented here, during the last three years, Safe Bulkers’ price has increased by 40%, being in the middle of our comparison group. I normally use total return in this graph, but since Safe Bulkers just recently initiated a dividend for its common shares, I believe that price appreciation is better.

SB shares valuation

I will use the same peer group in order to get a feeling of the company’s relative valuation. However, please note that the vast market cap differential between Star Bulk Carriers (SBLK) and the rest of the companies is a limitation to this comparison. As I’m writing this article, Safe Bulkers’ shares are trading at 1.9 times its forward earnings, while its peers are trading at almost double valuations. More specifically, Star Bulk Carriers and Diana Shipping (DSX) are currently trading at 3.3 and 3.6 times their forward earnings, respectively. The same is true from an operating cash flow perspective, as Safe Bulkers are trading at just 1.25 times their operating cash flow and its peers at almost two times this figure.

With regard to revenue growth, the company is lying in the middle of the peer group. During the last five years, Safe Bulkers has seen its revenues rise at a CAGR of 23%, while the respective figures for Star Bulk Carriers and Diana Shipping are 45% and 17%.

So, we can see that in every metric, the market is being quite conservative to Safe Bulkers, relative to its peers. And while from a personal standpoint, I do believe Star Bulk Carriers to be the best company in class, I really do think that such discount to Safe Bulkers isn’t justified from its financial performance so far.

Reasons to doubt the current low valuation

There are several reasons why someone could think that the market has been too harsh on this one:

- Fleet Modernization: As I wrote in the introduction of this article, Safe Bulkers are waiting for the delivery of 9 newbuild vessels. In case you didn’t know, modern vessels provide an extra advantage to companies in several ways. Firstly, they are more cost-efficient and most probably they are scrubber fitted. This means that they can operate in cheaper “heavy” oil, increasing operational margins. This becomes particularly important as the VLSFO/HSFO oil price differential widens. Right now, high/low sulfur oil differentials range from $225 to $321 per tonne. These figures, while far from $500+ observed last summer, still have a strong impact on the companies’ operational margins. From the 44 owned vessels of Safe Bulkers, 18 of them have scrubbers installed, while another 5 are in the process of scrubbers installing. Secondly, shipowners need to invest in more efficient vessels in order to comply with stricter environmental policies that will become mandatory in the future. Starting from 2023, taxes paid will be directly and positively correlated with the CO2 emissions. Currently, the tax rate per CO2 tonne is EUR 100. In this context, the company’s newbuilds M/V Vassos and M/V Climate Respect are operating in Class A energy efficiency and below Phase III environmental minima. According to the company’s CEO, Polys Hajioannou, the modernization of the fleet is the number one priority of the company. However, don’t expect any shocking fuel alteration decisions until 2024, as currently there is no clear direction on this matter.

- Attractive dividend as a second role: As I wrote earlier, the company initiated its common share dividend a few months ago, and it is currently paying $0.05 per share, which stands for a 7.4% dividend yield. Apart from that, the company is also having its C and D series of preferred stock, at an 8.4% dividend yield. While these figures aren’t so impressive compared to other shipping stocks, they definitely add some spice to the whole investment story. But still, I believe that the first role here belongs to the capital appreciation perspective.

- Interest Alignment: One thing that I look for when I’m looking into companies is if their management has skin in the game. That is particularly true for Safe Bulkers, with insiders holding 25% of the total shares and 40% of the company, while in Star Bulk Carriers, for example, there’s a single-digit figure. In addition, almost 28% of the company’s shares are in the hands of institutional investors.

Bottom line

There’s no doubt that difficult times are ahead for shippers, and especially for those exposed to larger vessel segments, such as Safe Bulkers. However, as a long-term investment, the company is significantly undervalued. In addition, the increased capital expenditures in fleet modernization will eventually come into fruition as environmental regulations become stricter and high/low sulfur oil price differential is material to the company’s operational costs. On top of that, the single-digit dividend yield could lift some of the uncertainty and provide a nice cushion to price fluctuations. It’s going to be a bumpy ride, but with ownership interests so well aligned with public investors, I believe that returns will be significant in the future.

Be the first to comment