Miro Nenchev

Safe Bulkers, Inc. (NYSE:SB) is in for a rough ride in 2023. The visible macro-headwinds are going to push demand down even as it invests in modernizing its existing fleet while bringing on new vessels.

Management said that it plans on increasing the number of vessels it is dry-docking in 2023 from the usual eight or nine to as many as 15 or 16, based upon the weaker freight market.

While the company should have more than enough liquidity to endure a prolonged downturn, it’s going to be a volatile year for SB as it prepares its fleet for when the economy and demand improve. And with the number of large vessels it has, it’ll be further exposed to that volatility.

In this article, we’ll look at how it did in the last quarter and what investors should expect through the next year.

Some of the numbers

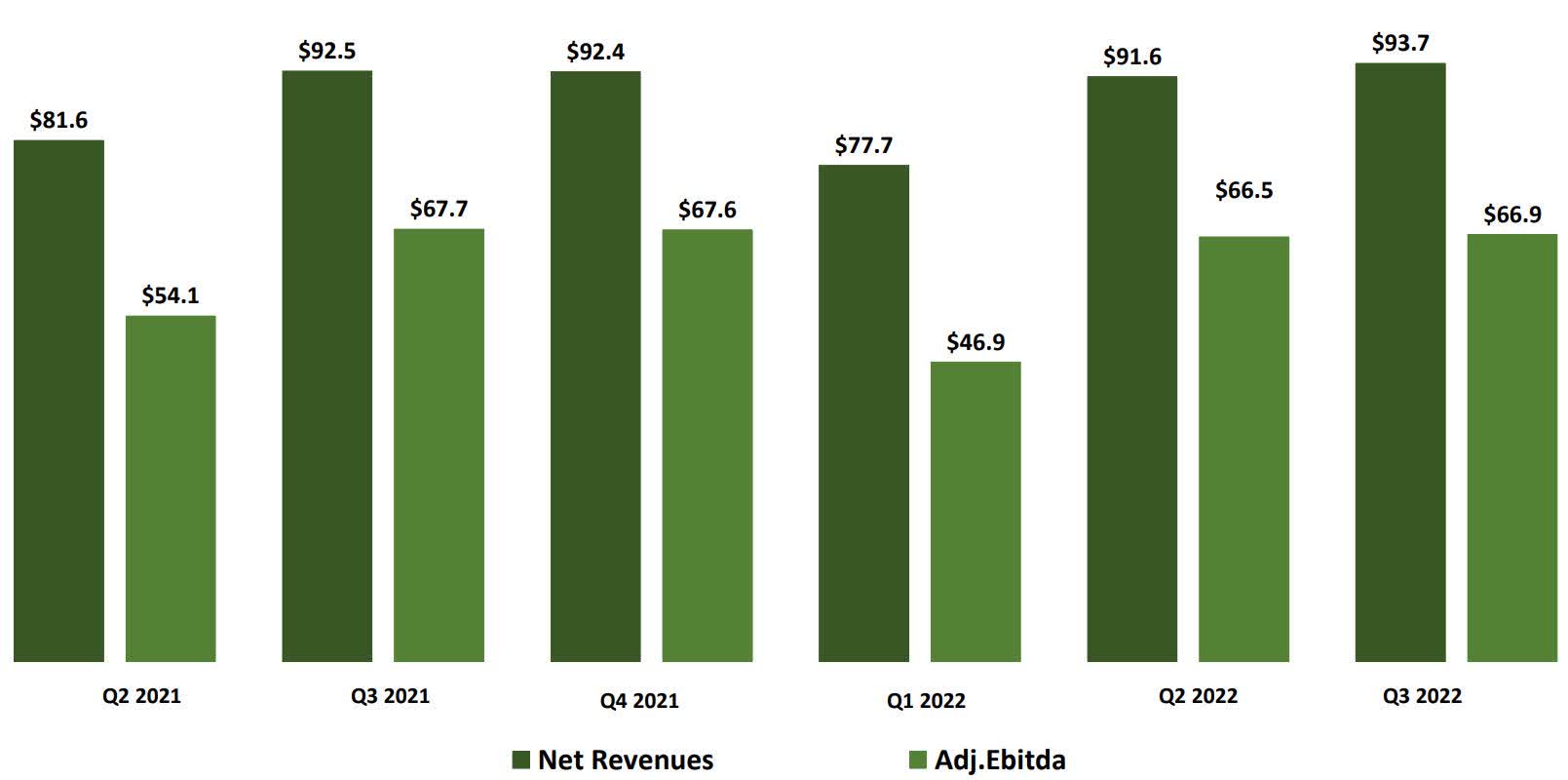

Revenue in the third quarter was $93.7 million, up $1.2 million from the revenue generated in the third quarter of 2021. Over the last four quarters, revenue has been in a tight range of $91.6 million to $93.7 million, outside of the weak first quarter of 2022 when revenue was $77.7 million.

Adjusted EBITDA in the third quarter was $66.9 million, down $800,000 from the $67.7 million in adjusted EBITDA generated in the third quarter of 2021. Other than the weak first quarter of 2022, when adjusted EBITDA was $46.9 million, adjusted EBITDA for the company was in a range of $66.5 million to $67.7 million over the last year.

Investor Presentation

Adjusted earnings per share in the reporting period was $0.39, compared to the $0.40 in adjusted earnings per share for the third quarter of 2021.

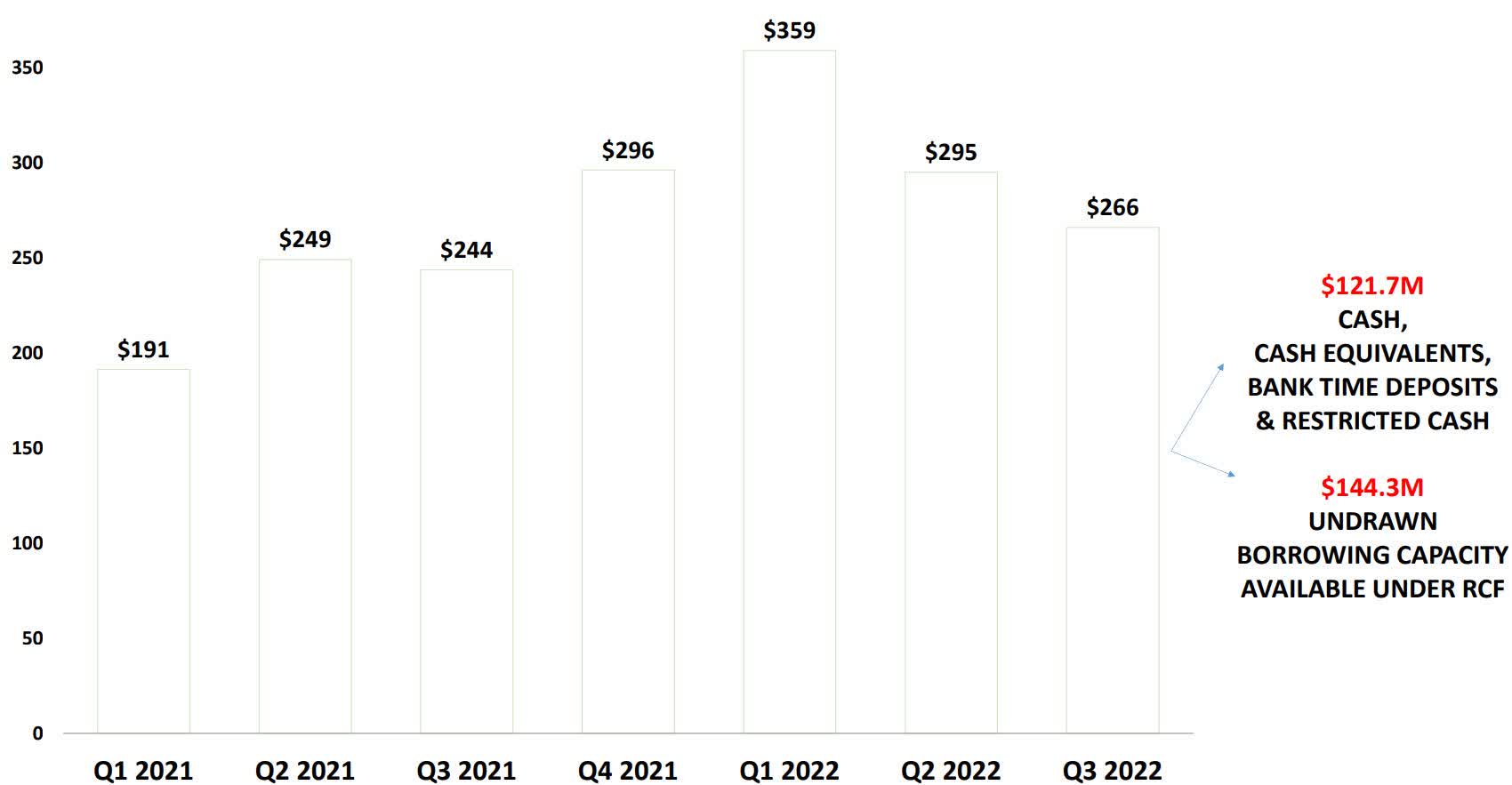

At the end of the third quarter, SB had cash and cash equivalents, bank time deposits, and restricted cash of $121.7 million, with another $144.3 million in undrawn borrowing capacity under its revolver. It held debt of $447.9 million at the end of the reporting period.

Investor Presentation

Concerning remaining CapEx requirements, Safe Bulkers has $254.3 million in total, with $249.9 million of that associated with its nine newbuilds.

Major headwinds

I think it’s possible that SB and the drybulk sector, in general, may have one more decent run in the fourth calendar quarter of 2022. However, I think it’s going to get a lot tougher in the first two calendar quarters of 2023, and could potentially get much worse as the year goes on, depending on the length and depth of the recession, uncertainties in China related to COVID policies, and other geopolitical factors like the war between Russia and Ukraine.

At the global level, inflation is expected to improve from 8.8 percent in 2022 to 6.5 percent in 2023, but that is still elevated, and rising interest rates carry their own inflation for companies with significant debt loads.

As for global dry bulk demand, the company sees that continuing to grow at a very modest pace of 1 percent in 2023.

In China, dry bulk imports for full-year 2022 were down seven percent year-over-year. With GDP in the country expected to improve in 2023, there’s a chance dry bulk imports will slightly improve with it.

As for India, that large market is expected to have GDP drop from a growth of 6.8 percent in 2022 to a growth of 6.1 percent in 2023.

The EU embargo on Russian coal and oil and oil products should remain in effect throughout 2023, which will remain a headwind in dry bulk.

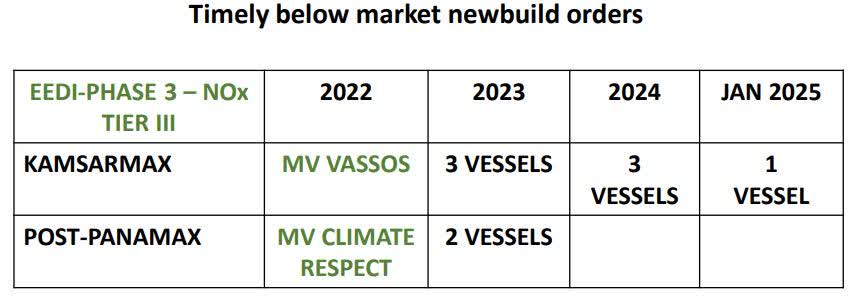

With demand expected to be lower in 2023, SB is taking steps to modernize some of its fleet while adding five new vessels as well.

Investor Presentation

Share price movement

After its share price collapsed to as low as $0.84 per share in the aftermath of the impact of COVID-19 on the sector, Safe Bulkers has started to rebound in November 2020, jumping to as high as about $5.45 per share on September 7, 2021, before pulling back as it struggled to find sustainable traction.

TradingView

Since June 6, 2022, when it traded at a little over $5.00 per share, Safe Bulkers has plunged to its 52-week low of $2.3511 per share and has found a ceiling at right around $3.00 per share. I don’t see any near-term catalysts that will sustainably push it above that level, and as the Federal Reserve continues to raise interest rates in response to inflation and the global economy weakens, demand is going to probably be level at best in 2023, and with the company’s focus on improving its existing fleet while adding some newbuilds to it in 2023, it could be positioned to rebound once economic and geopolitical factors improve.

If it takes longer than expected for that to happen, the share price of SB will come under further pressure. I think that should be considered a positive for those looking to take a position in the dry bulk sector via SB. It could also be an opportunity for existing shareholders to add to their positions while lowering their cost basis.

Conclusion

The macroeconomic and geopolitical conditions are working against the dry bulk industry at this time, and Safe Bulkers, Inc. is going to participate in that decline.

Knowing that, SB is increasing its drydocks in 2023 in anticipation and preparation for an economic rebound further out. Once that happens its improvements in its existing fleet should result in lower fuel costs, and by adding its newbuilds, the company will be prepared for more positive conditions in the industry when they emerge.

In the meantime, it will have to watch its overall spending in case the recession is deeper for longer, and the cost of debt continues to rise.

Overall, the long-term outlook for SB looks okay, but in the near term, it’s going to struggle along with its peers. With the market hesitant to reward SB’s share price in the recent past, it’s possible SB could be disproportionately hit with a drop in its share price as things get worse before they get better.

In the short term, for those interested in the dry bulk shipping industry, it’s going to be tough. However, in the case of SB, it could provide an opportunity to get in at prices unlikely to be seen again for a long time.

That said, I think it’s best to be patient, because when the Safe Bulkers, Inc. numbers come out for the next couple of quarters, I think they’re not going to be as strong as they have been over the last year. This should bring Safe Bulkers, Inc.’s share price down to a more attractive entry point, which would offer a much better risk/reward opportunity.

Be the first to comment