Wand_Prapan/iStock via Getty Images

A Quick Take On Sacks Parente Golf Inc.

Sacks Parente Golf, Inc. (SPGC) has filed to raise an undisclosed amount in an IPO of its common stock, according to an S-1 registration statement.

The firm designs and sells a range of golf products for consumer use.

SPGC is still at a very early stage of development and management hasn’t shown its ability to grow revenue in any appreciable sense.

When we learn more IPO details, I’ll provide an update.

Sacks Parente Overview

Camarillo, California-based Sacks Parente was founded to develop ‘technology-forward’ premium quality golf equipment for sporting enthusiasts.

Management is headed by co-founder, president and Chief Executive Officer Timothy L. Triplett, who has been with the firm since inception in March 2018 and was previously CEO of Nippon Xport Ventures [NXV], the company’s largest shareholder and was co-founder, president and CEO of Brass Ring Spirit Brands.

The company’s primary offerings include:

-

Putting instruments

-

Golf shafts

-

Golf grips

-

Other golf-related products

The company designs its products to fit all skill levels within golf, from amateur to professional.

Sacks Parente has booked fair market value investment of $2.4 million as of March 31, 2022 from investors including Nippon Xport Ventures and Parcks Design LLC.

Sacks Parente – Customer Acquisition

The firm sells its products worldwide via its direct ecommerce website, through distributors, subsidiaries, and via online and offline retailers.

Management intends to expand its production in the United States and to grow its marketing in Japan, South Korea and Mexico in the coming years.

Selling, G&A expenses as a percentage of total revenue have fluctuated as revenues have increased, as the figures below indicate:

|

Selling, G&A |

Expenses vs. Revenue |

|

Period |

Percentage |

|

Three Mos. Ended March 31, 2022 |

284.6% |

|

2021 |

179.5% |

|

2020 |

330.2% |

(Source – SEC)

The Selling, G&A efficiency multiple, defined as how many dollars of additional new revenue are generated by each dollar of Selling, G&A spend, fell to 0.0x in the most recent reporting period, as shown in the table below:

|

Selling, G&A |

Efficiency Rate |

|

Period |

Multiple |

|

Three Mos. Ended March 31, 2022 |

0.0 |

|

2021 |

0.1 |

(Source – SEC)

Sacks Parente’s Market & Competition

According to a 2019 market research report by Grand View Research, the global golf equipment market size was an estimated $6.5 billion in 2018 and is forecast to reach $7.6 billion by 2025.

This represents a forecast CAGR of 2.2% from 2019 to 2025.

The main drivers for this expected growth are growing disposable income from consumers, increasing golf tourism and a rising desire for consumers to play outside sports for health reasons.

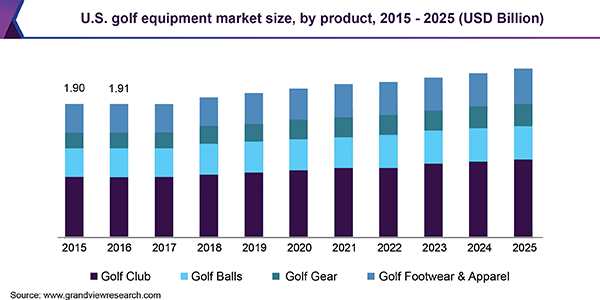

Also, below is a chart showing the historical and projected future growth trajectory for the U.S. golf equipment market:

U.S. Golf Equipment Market Size (Grand View Research)

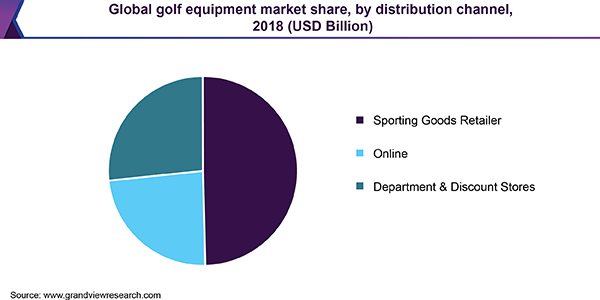

The chart below shows that in 2018, approximately 55% of golf equipment was sold through sporting goods retailers:

Global Golf Equipment Market Share (Grand View Research)

Major competitive or other industry participants include:

-

Callaway Golf Company (ELY)

-

SRI Sports

-

Acushnet Holding

-

Taylormade

-

Mizuno

-

Wilson

-

Ping

-

Fujikura Composites

-

Mitsubishi Chemical

-

Graphite Design

-

Paderson Kinetixx

-

Others

Sacks Parente Golf Inc. Financial Performance

The company’s recent financial results can be summarized as follows:

-

Growing topline revenue from a tiny base

-

Increasing gross profit but variable gross margin

-

Growing operating loss

-

Higher cash used in operations

Below are relevant financial results derived from the firm’s registration statement:

|

Total Revenue |

||

|

Period |

Total Revenue |

% Variance vs. Prior |

|

Three Mos. Ended March 31, 2022 |

$ 65,000 |

6.6% |

|

2021 |

$ 200,000 |

9.9% |

|

2020 |

$ 182,000 |

|

|

Gross Profit (Loss) |

||

|

Period |

Gross Profit (Loss) |

% Variance vs. Prior |

|

Three Mos. Ended March 31, 2022 |

$ 45,000 |

104.5% |

|

2021 |

$ 84,000 |

-40.4% |

|

2020 |

$ 141,000 |

|

|

Gross Margin |

||

|

Period |

Gross Margin |

|

|

Three Mos. Ended March 31, 2022 |

69.23% |

|

|

2021 |

42.00% |

|

|

2020 |

77.47% |

|

|

Operating Profit (Loss) |

||

|

Period |

Operating Profit (Loss) |

Operating Margin |

|

Three Mos. Ended March 31, 2022 |

$ (142,000) |

-218.5% |

|

2021 |

$ (294,000) |

-147.0% |

|

2020 |

$ (473,000) |

-259.9% |

|

Net Income (Loss) |

||

|

Period |

Net Income (Loss) |

Net Margin |

|

Three Mos. Ended March 31, 2022 |

$ (144,000) |

-221.5% |

|

2021 |

$ (302,000) |

-464.6% |

|

2020 |

$ (479,000) |

-736.9% |

|

Cash Flow From Operations |

||

|

Period |

Cash Flow From Operations |

|

|

Three Mos. Ended March 31, 2022 |

$ (125,000) |

|

|

2021 |

$ (171,000) |

|

|

2020 |

$ (228,000) |

|

(Source – SEC)

As of March 31, 2022, Sacks Parente had $210,000 in cash and $857,000 in total liabilities.

Free cash flow during the twelve months ended March 31, 2022, was negative ($238,000).

Sacks Parente Golf Inc. IPO Details

Sacks Parente intends to raise an undisclosed amount in gross proceeds from an IPO of its common stock.

No existing shareholders have indicated an interest to purchase shares at the IPO price.

Management says it will use the net proceeds from the IPO as follows:

approximately $2.3 million to fund marketing and professional tour related expenses;

approximately $2.0 million for working capital, to be used to add staff members including, but not limited to sales/technical, engineering, factory, quality control, and administrative staff.

approximately $1.0 million for manufacturing facilities and related capital equipment;

approximately $1.25 million for increased inventory;

approximately $3.0 million for new opportunities and expansion into Asia;

This expected use of the net proceeds from this offering represents our intentions based upon our current plans and business conditions for approximately the next 12 to 24 months

(Source – SEC)

Management’s presentation of the company roadshow is not available.

Regarding outstanding legal proceedings, management says the firm is ‘not currently involved in any dispute, pertaining to our intellectual property rights or otherwise, either as a plaintiff or a defendant.’

The sole listed bookrunner of the IPO is The Benchmark Company.

Commentary About Sacks Parente’s IPO

SPGC is seeking U.S. public capital market investment to fund its marketing and production expansion plans.

The firm’s financials have produced increasing topline revenue from a tiny base, growing gross profit but variable gross margin, higher operating loss and increased cash used in operations.

Free cash flow for the twelve months ended March 31, 2022, was negative ($238,000).

Selling, G&A expenses as a percentage of total revenue have fluctuated as revenue has increased; its Selling, G&A efficiency multiple dropped to 0.0x in the most recent reporting period.

The firm currently plans to pay no dividends and expects to retain any future earnings for reinvestment back into the firm’s growth initiatives.

The global market opportunity for golf products is expected to grow at a relatively low rate of growth over the coming years.

The Benchmark Company is the sole underwriter and IPOs led by the firm over the last 12-month period have generated an average return of 62.2% since their IPO. This is a top-tier performance for all major underwriters during the period.

The primary risks to the company’s outlook include lower golf popularity in certain regions as well as high inflation on product costs.

The firm is still at a very early stage of development and management hasn’t shown its ability to grow revenue in any appreciable sense.

When we learn more IPO details, I’ll provide an update.

Expected IPO Pricing Date: To be announced.

Be the first to comment