Jaskaran Kooner/iStock via Getty Images

The article was first published to members of my service on the 20th of October 2022.

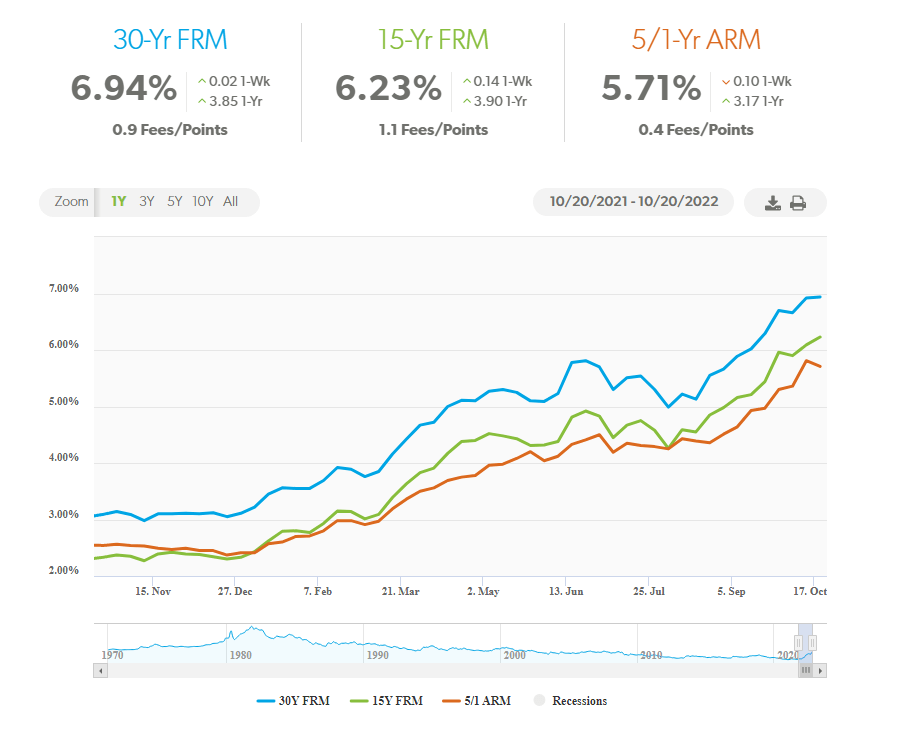

Before starting our article on Sachem Capital Corp. (NYSE:SACH), I would like to just remind you what has happened to mortgage rates in 2022:

Mortgage Rates (Google Search)

The USA standard is to have a fixed rate on your mortgage. All else being equal a person willing to buy a home with a 30-yr mortgage would have to pay a 60% higher monthly installment. Even though I am not an economy expert, I am 100% positive that the average US citizen has not increased his income by 60% since the beginning of the year. All related parties to residential homebuilding will be affected somehow and the effect will hardly be positive.

SACH’s business

The company has said it best on its website:

At Sachem Capital, we are a Connecticut-based real estate finance company that specializes in originating, servicing and managing a portfolio of first mortgage loans. We offer short-term (typically 12 to 36 months), secured, non-banking loans (sometimes referred to as “hard money” loans) to real estate investors to fund their acquisition, renovation, rehabilitation, development or improvement of residential or commercial properties located across the United States eastern seaboard while also including Texas and Ohio.

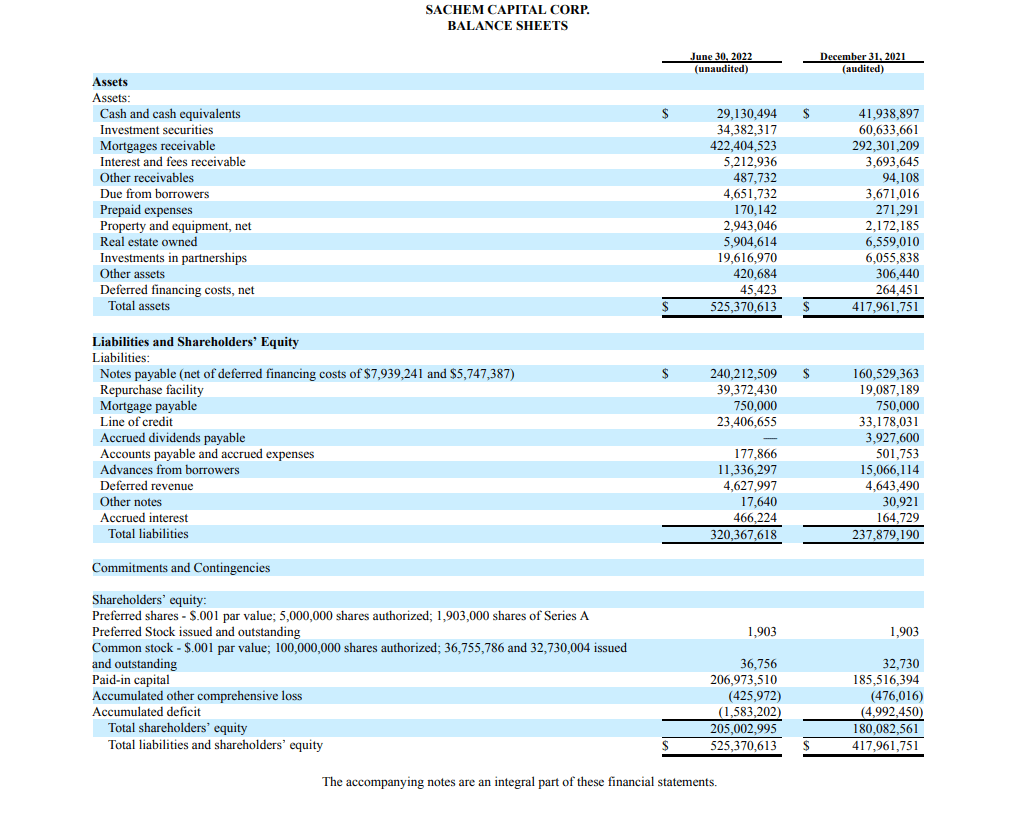

The “Hard Money” business is not called like this without a reason. The loans being made by SACH are high credit risk ones with very low duration. It is a niche business that is supposed to boom with a booming economy and cheap financing costs. The company started its balance sheet expansion at a time that does not seem quite favorable for the business model. At the time of writing, based on the last reported data by the company, we can see the balance sheet here:

SACH Reports

The Book Value Equity of the company is around $205 mln with liabilities of around $320 mln. The Equity market cap consists of the common stock ($150 mln) and the preferred stock SACH-A ($37 mln at a price of 19.50 and a nominal value of around $47 mln.) The biggest part of the liabilities are the baby bonds issued by the company:

SACH ETD (Proprietary Software)

The nominal value of the bonds is around $240 mln and the nominal yields range from 6% to 8% depending on the date of issuance. The average weighted nominal yield of the notes is around 7% and the expected annual interest expense is around $16.8 mln.

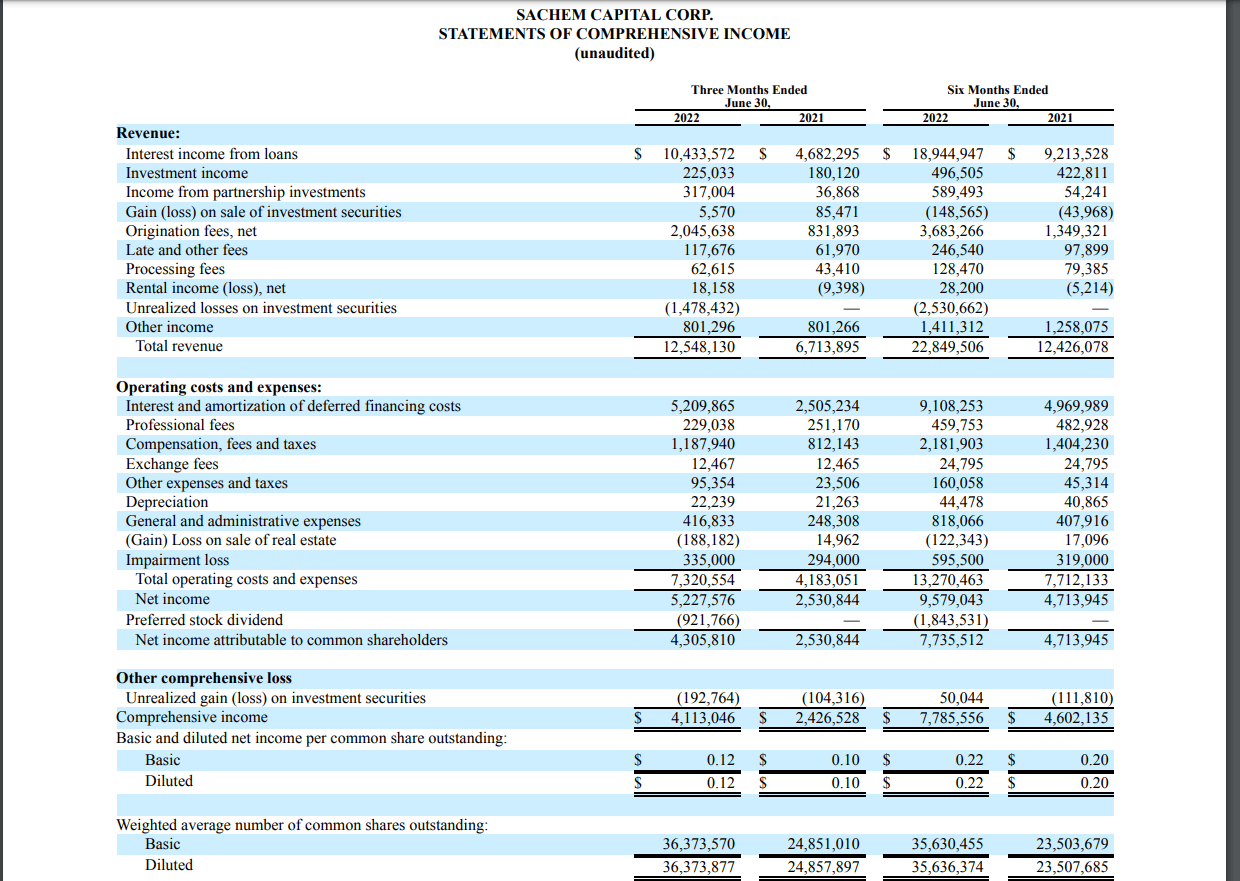

The income statement

SACH Reports

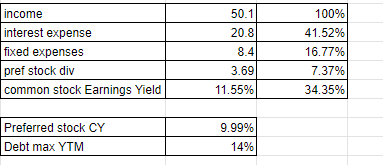

Based on total assets and total revenue the company was able to produce an “assets yield” of around 9.5% annualized. 42% of the income is needed to cover the interest expenses of the company. Around 17% of the income is needed to cover the fixed expenses of the business, while 7.5% of the income is needed to cover the preferred stock dividend. 34% of the projected revenue is what is then left for the common stock to be distributed and to fight any asset value erosion. At the time of writing if we take a screenshot of the business this would represent a common stock earnings yield of around 11.5%. The simplified earnings model can be seen here:

Simplified Income Statement (Author’s calculations based on last report)

The simple assumption is that if nothing changes for the company one can expect an 11.5% return from the common stock. At the time of writing SCCF – a 7.13% bond maturing in 4.75 years has a yield to maturity of 13.7% at a price of 19.81. The bond pricing (which can be seen at the beginning of the article) does not state that nothing has happened to the company. All of the bonds trade as if the company is deeply distressed. Any person who has dug just a little into finance knows that risk and reward are supposed to be correlated. The common stock earnings potential is absolutely limited by the macro environment to a point where the bonds of the company trade at teenager yields. Just a few days ago SCCF was trading at a 15% YTM. If an investor expects that by some miracle SACH will be able to increase its revenue while reducing overall expenses all of the bonds of the company will have to trade at “normal” yields. There will definitely be a capital appreciation in the baby bonds in a positive scenario for the company. The bonds being priced as they are present a higher capital appreciation potential fundamentally, compared to the common stock.

Book value per share of SACH

The typical article promoting high-yielding common stocks sounds like this:

15% yield (distribution) at a deep discount to NAV.

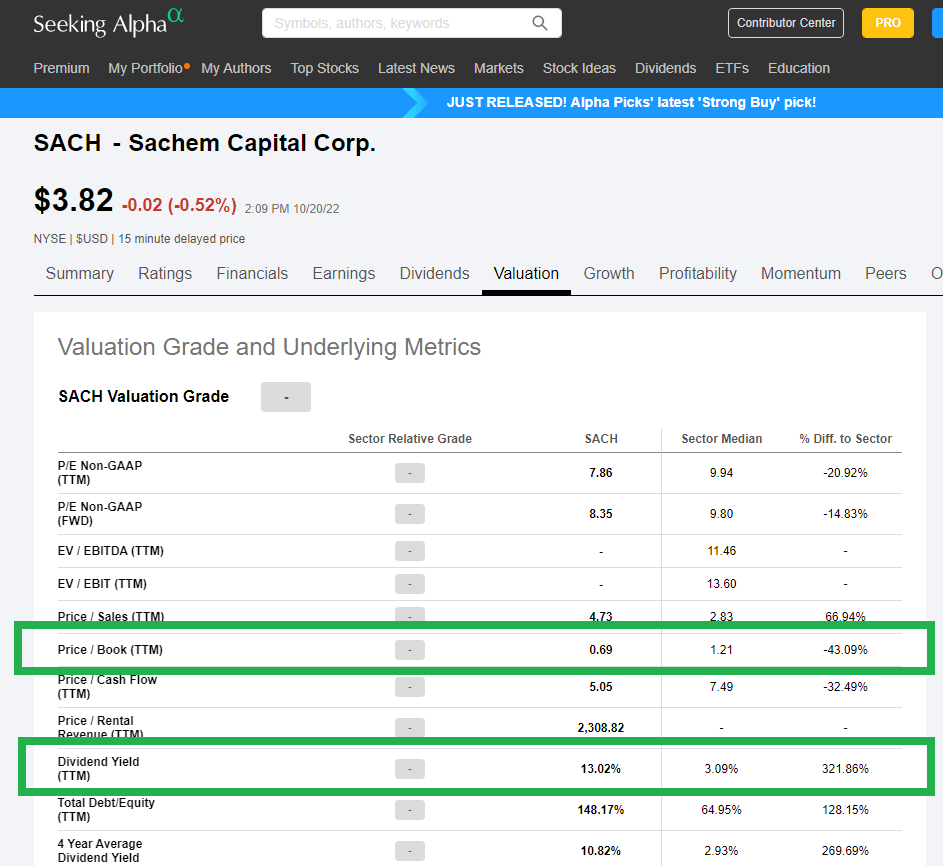

The case can be made for SACH as well only if you look at some popular sources:

Seeking Alpha (included):

Seeking Alpha

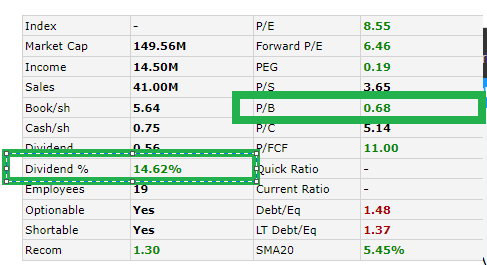

FINVIZ:

Finviz

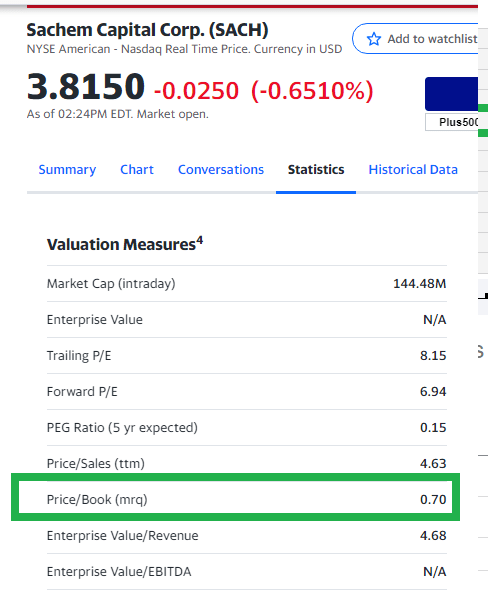

Finance Yahoo:

Finance Yahoo

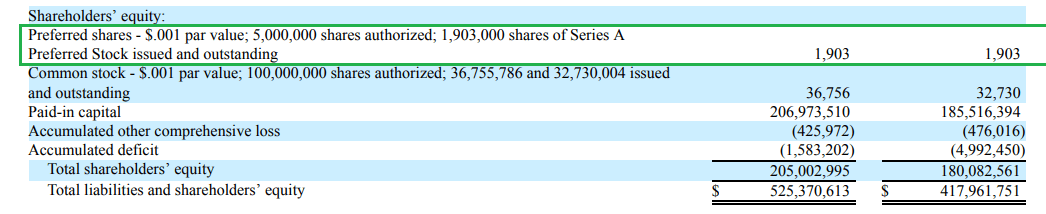

I hope you get the picture. SACH is a deeply discounted high-yielding REIT that is undervalued because of its small size and the market fails to see its real value, so the average investor has to load up on this fat yield and use the “the more it drops, the more I buy” approach. In fact, all the sources are missing the way the preferred stock is accounted for in the balance sheet. Based on company information there are around $1.9 mln shares of SACH-A being issued and outstanding. This is a nominal value of around $47.5 mln. It looks in the balance sheet like this:

Preferred Stock BV (SACH Reports)

The Preferred stock is perpetual and the company does not have the obligation to redeem it at any point in time. In any case, the preferred stock stands higher in the capital structure compared to the common stock. If we subtract the $47.5 mln. nominal value of the preferred stock from the equity book value of the company, the common stock is left with a book value of $157.5 mln. The discount does not seem that deep now at 93%. In fact, the preferred stock, which is also completely overvalued in comparison to the baby bonds, trades at a way higher discount to book value (not that book value means anything for a perpetual preferred).

The bond, the preferred, or the common

The current environment makes all of these investments quite risky, which can easily be seen by their yields. The risk-free high yields can be found only in motivational speeches, SA articles, and Ponzi schemes. When you buy a 13% 5-year bond, there has to be something wrong with the company. The strange case of SACH is that the bonds trade as if the company is distressed while the common stock trades as if it is business as usual. In this case, there is some Alpha to be earned but it is really hard to know if the common stock will get crushed or the bond will rise. There is only one scenario in which the common stock will outperform the bonds on a risk-adjusted basis and this includes scams, as is the case of CDR and its preferreds, for example, or LTS and its bonds.

The idea

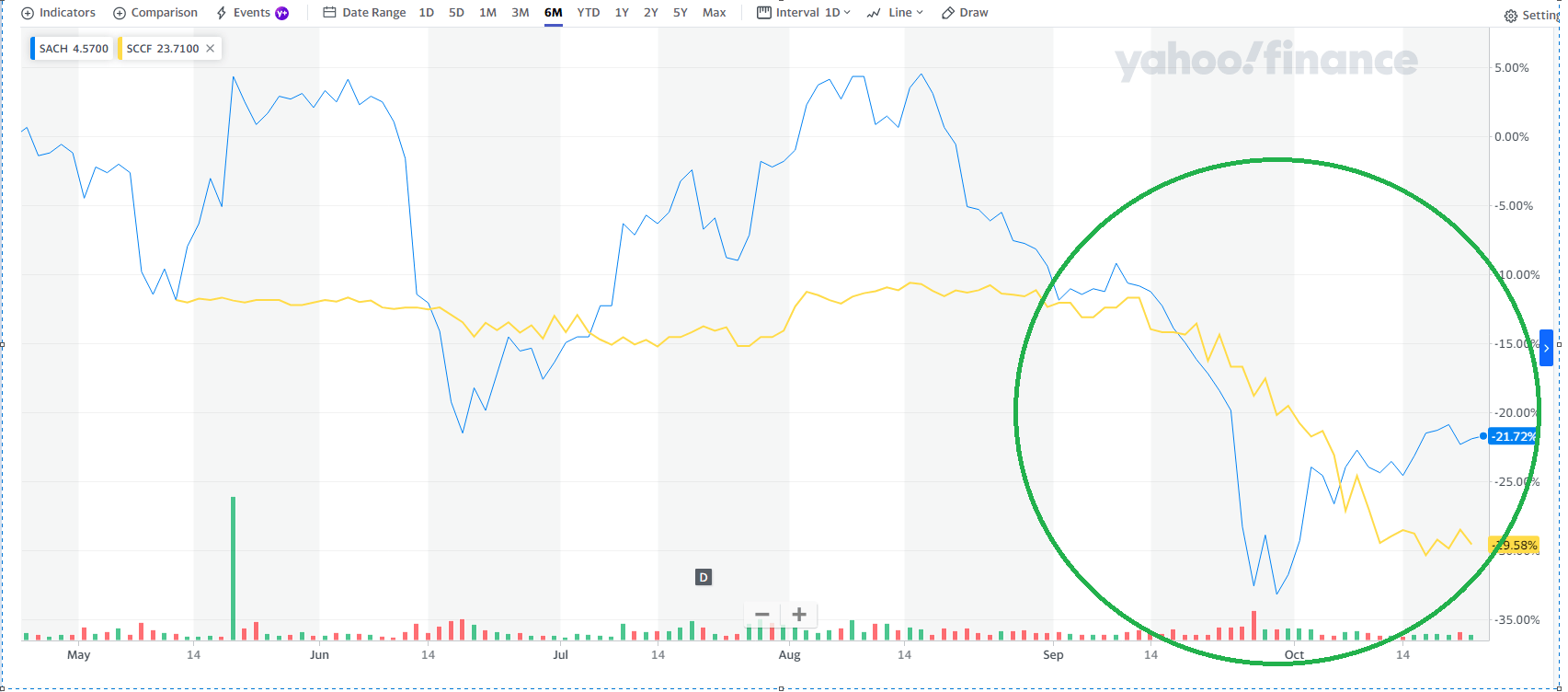

Long the bonds (SCCF the highest YTM) until they reach the CY of the preferred stock or until the market realizes how distressed the company is and smashes the common stock. The common stock valuation can be used as a trigger to sell the bond or as a direct hedging reaction because the common stock has been extremely strong lately as compared to the bonds of the company:

SACH vs SCCF (Finance Yahoo)

When the common stock is rallying it is a very bullish sign for the bonds. It is counterintuitive that a lower part of the capital structure will be the first to rally but this is how the market works. This very often gives us a laggard that is full of “Alpha”.

Conclusion

The SACH capital structure can be used in universities to show how theory and practice are always the same in theory but never in practice. In the meantime, we can only hope that what is to come will not mess with our 13% yield to maturity from SCCF.

Be the first to comment