Thomas Barwick/DigitalVision via Getty Images

The pandemic crushed tourism, and Sabre Corporation (NASDAQ:SABR) did not avert it. Despite all these, the company showed it could withstand the blow and come back stronger. In the last year, it has shown continued recovery, with solid revenue growth and margin improvements. This year, more enticing growth prospects are anticipated as the travel upsurge persists. Even better, SABR shows its adequacy to sustain its rebound and expand. Net worth may still be negative, but fundamental stability can be seen. Likewise, the stock price is exciting, given its upside potential.

Company Performance

The pandemic has caused unexpected disruptions across all business sectors. Deemed non-essential, tourism was one of those greatly affected by restrictions. The GDS industry was no exception as it catered to travel and accommodation. Also, fuel price increases and the Russo-Ukrainian War hampered its recovery in 2022. Indeed, the past two years have been challenging for Sabre Corporation.

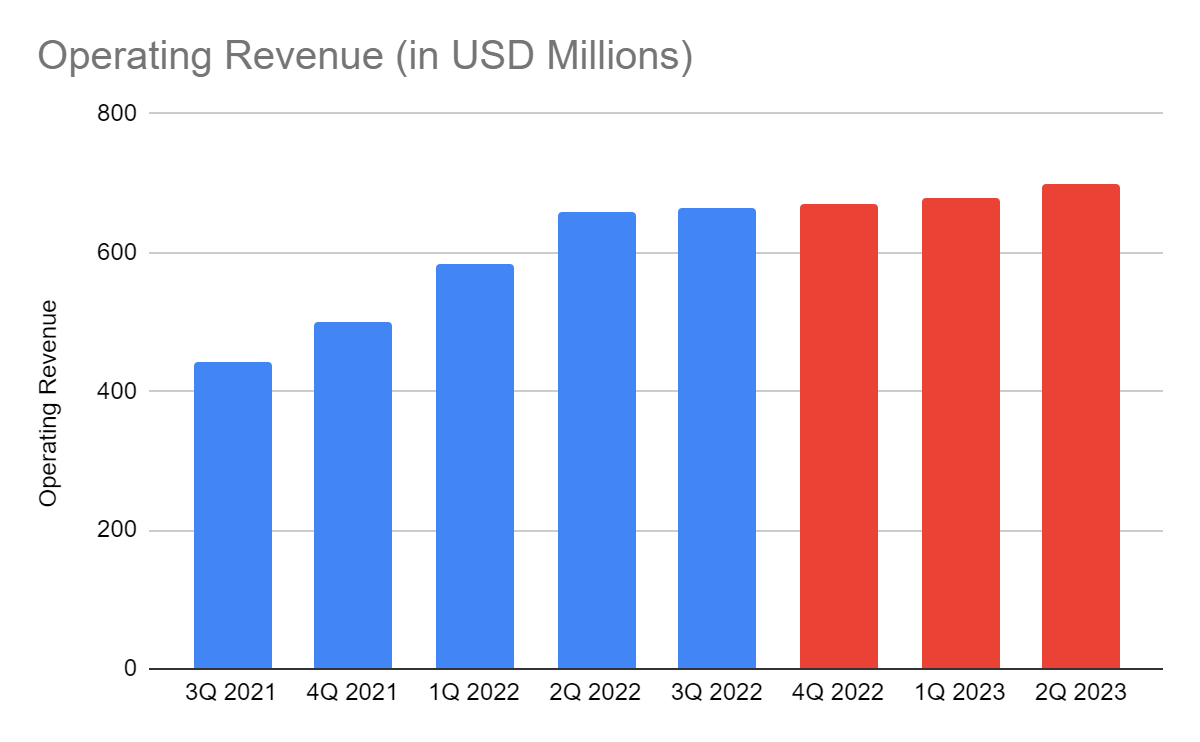

Despite all these, Sabre keeps showing its ability to withstand all these blows. Growth may have been stagnant, but operational stability remains its cornerstone. Its solid rebound may be expected, making 2023 a promising year for the company. But before that, we must analyze its current trend. Today, it shows a sustained rebound with its continued revenue increase. Its operating revenue amounts to $663 million, an impeccable 50% year-over-year growth. Also, sequential values are in a consistent uptrend, it is higher than in the first two quarters by 13% and 8%.

It is impressive to see its well-maintained revenues as inflation remains a challenge. It peaked at 9.1% before 2Q ended. Although there has been a continued decrease in 3Q, the rate remains elevated at 8.2% in 3Q. Even so, Sabre and most of the GDS industry demonstrate a robust performance. Thanks to revenge travel, business reopening, and easing of restrictions.

Operating Revenue (MarketWatch And Author Estimation)

The GDS industry enjoys a boom, given the influx of travelers on the internet. Also, we must remember that it has an efficient and timely business model. Sabre capitalizes on this advantage by ramping up its digitalization. Doing so helps streamline business processes, allowing more interactions with customers and agents. It is no surprise SABR sees higher bookings, which serves as a primary revenue growth driver.

Moreover, SABR keeps its costs and expenses low. Even if it ramped up its operations in 3Q, the sequential increase was very low at less than 1%. Its year-over-year growth is noticeable at 22%, but it is way lower than revenue growth. As such, revenue growth continues to offset the increase in costs and expenses. What’s more appealing is that SABR realizes economies of scale despite inflation. It is logical to say that the travel influx also offsets the inflation effect. Its efforts to digitalize and speed up its technology also continue to pay off.

Given all these, SABR becomes more profitable. Although its operating income stays negative, its improvement is impeccable. Its current operating margin is now -4.5% compared to -34% last year. We can see how SABR balances robust growth with operational efficiency. The operating revenue increases faster than costs and expenses, improving profitability.

This year, I expect SABR to keep thriving. Inflation will be one of the primary growth drivers of its core operations. Demographic changes may also help as more Millennials and Gen Zers are geared toward leisure travel. It is consistent with a recent survey about travel and inflation. In a recent survey, most of them said inflation strained their travel budget, but their travel plans would not decrease. They still plan to travel, but may change their itineraries to keep their budget intact. Lodging away from home shows a 2.9% increase from 2021, making our optimistic view logical. But the acceleration rate may not be as swift as we expect. We must consider massive China lockdowns and the continued tension in Europe. As such, I expect a decent increase in operating revenue and operating margin.

Operating Margin (MarketWatch And Author Estimation)

How Sabre Corporation May Fare This Year

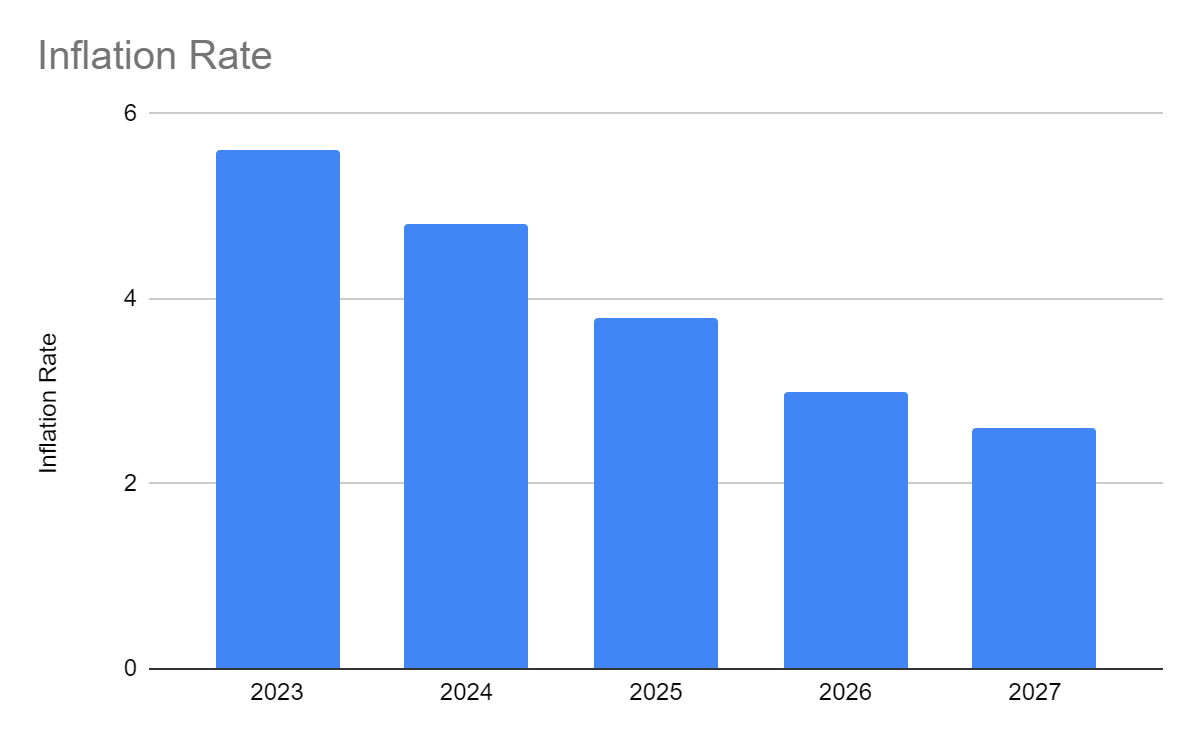

Macroeconomic indicators may become the main factor for tourism growth this year. It is consistent with the survey we discussed in the previous sections. Even so, it is nice that despite the changes, tourism rebound remains robust. With that, I expect a better year for Sabre Corporation and the whole GDS industry. Inflation lulls further in many countries, putting downward pressure on prices across industries. Fuel prices are also more stable than in the first half of 2022. In the US alone, inflation is now at 6.5% a substantial drop from 7.1%. I expect it to keep decreasing as the Fed remains conservative by sustaining interest rate increments. Most G20 countries are in the same pattern, with 15 out of 20 members seeing inflation decrease. Travelers may stick with their desired itineraries or even increase their travel plans.

Inflation Rate (Author Estimation)

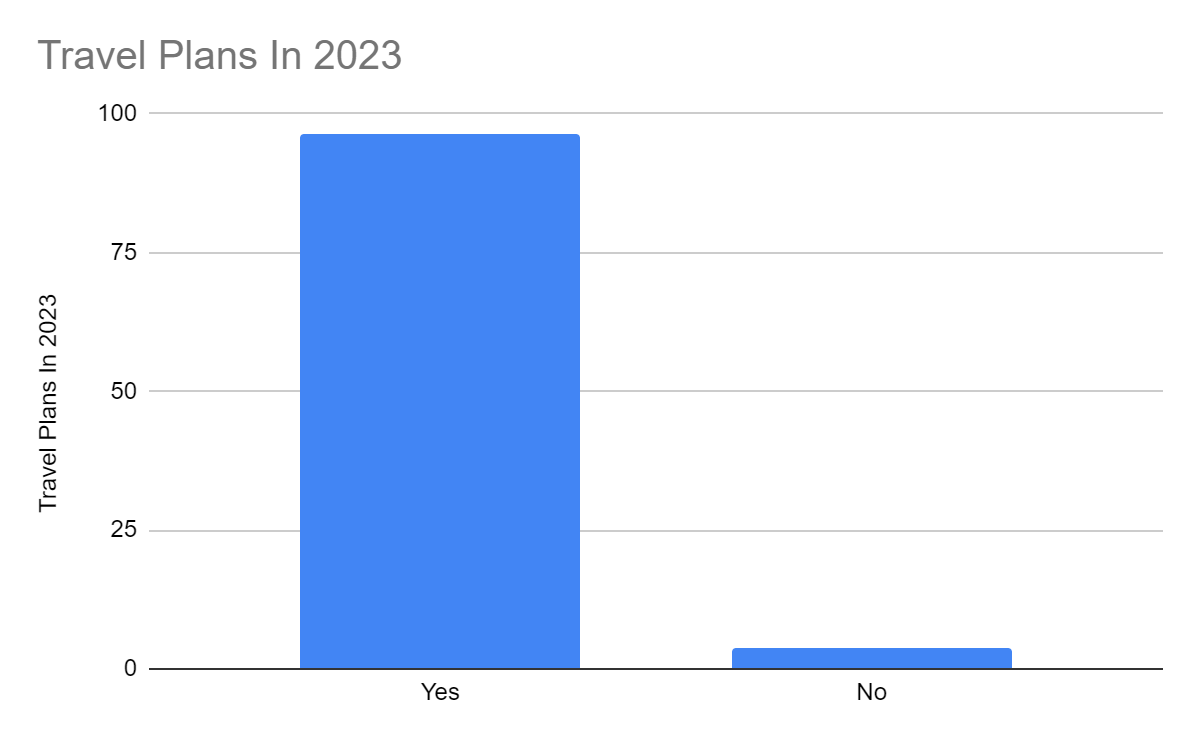

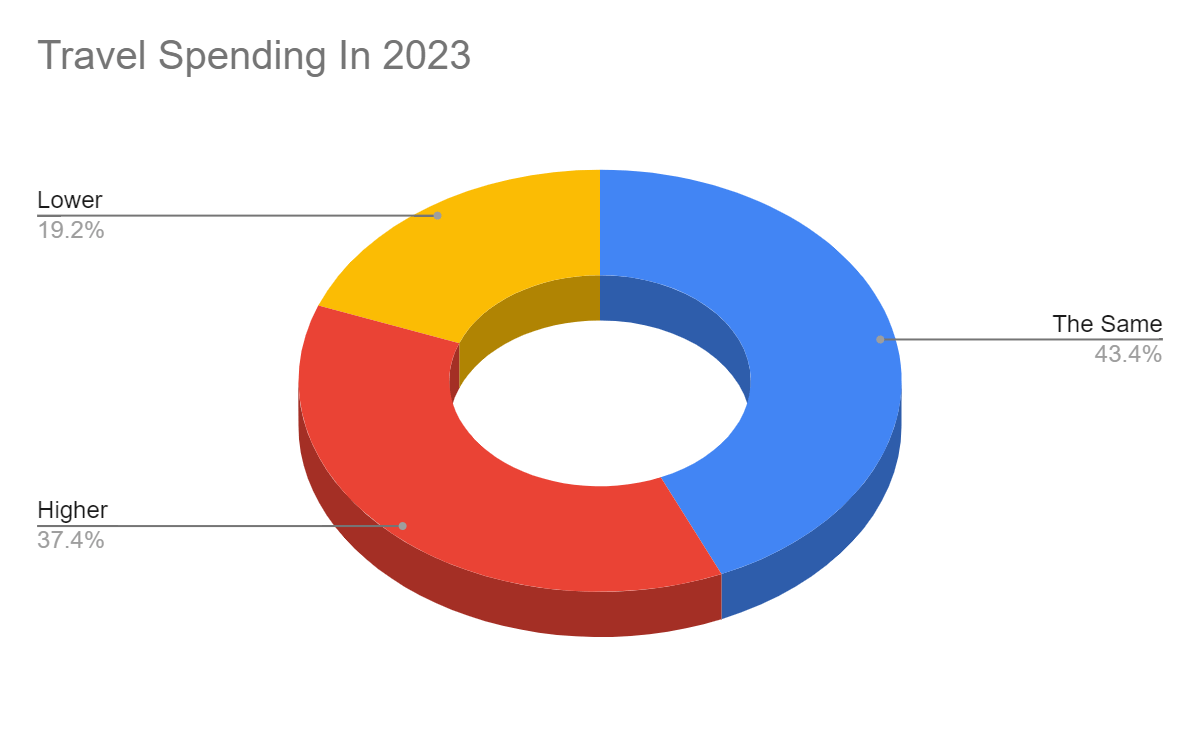

The economic improvement is consistent with the current and projected travel trends. In 2022, the GDS once again proved its vital role in travel tourism as 68% of sales were made online. Moreover, analysts expect a 30% growth in global tourism. Returns may still be lower than pre-pandemic levels, given the external factors we covered. But once the economy, European tension, and China lockdowns become stable, tourism may unleash its potential. Also, this year, most Americans have travel plans, with 96% saying yes in a survey. The same study explains that 37% of travelers will spend more on travel this year, while 43% say they will spend the same. Another desirable impact of lower inflation is the change in travel preferences. The Asia-Pacific and Europe draw a substantial increase in travel interest. Airways searches data show that international flight searches are 62% while 38% are domestic flight searches.

Travel Plans In 2023 (hopper)

Travel Spending In 2023 (hopper)

American Flight Searches (CNBC)

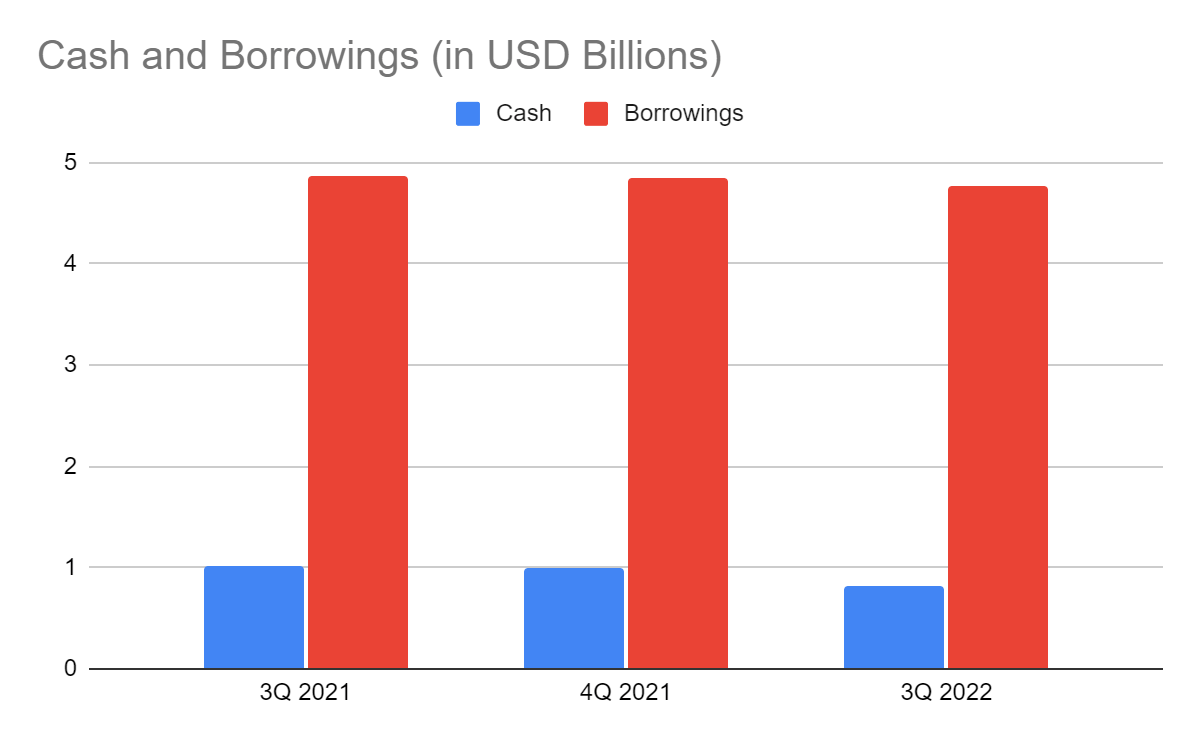

Even more essential is SABR’s capacity to sustain its operations and take advantage of the situation. It exudes fundamental stability, as shown by its stellar Balance Sheet. Cash levels are stable while borrowings are lower. This decrease is advantageous, given the continued interest rate hikes. It also shows cash burns stay manageable while increasing its operating capacity. Hence, Sabre Corporation may derive more returns as travel bounces back.

Cash And Cash Equivalents And Borrowings (MarketWatch)

Stock Price Assessment

The stock price of Sabre Corporation has been in a rally in the last two months. But it stays way lower than the 2022 highs. At $6.79, the stock price remains 30% lower than its value in 2022. While earnings and book value stays negative, prospects are more enticing this year. The current EV/Sales is 2.45x, which is better than the average of 3.81x in recent years. It is also approaching the pre-pandemic levels of 2.2x. As such, the stock price valuation becomes more attractive. We may use the average EV of $7.69 billion and compare it to the current net debt of $3.83 billion. The target price will be $11.76, a 73% upside. Even the current figures (6.42 B – 3.83 B) / 328,000 = $7.90 agree with the undervaluation of the stock price. The derived value shows there may be a 16% upside in the next 12-18 months.

Bottom Line

Sabre Corporation shows a solid recovery and enticing prospects. It balances growth with better viability and fundamental stability. It remains liquid, allowing it to cover immediate payables and borrowings. Also, business and leisure travel hype and lower inflation may drive its growth. Its adequate cash levels show it can expand to generate higher returns. Moreover, the stock price shows undervaluation, an ideal entry point for investors. The recommendation is that Sabre Corporation is a strong buy.

Be the first to comment