andresr

Recommendation

The online gaming industry has seen significant growth recently due to increasing legalization and privatization, as well as rising consumer use of digital entertainment platforms. I believe Rush Street Interactive (NYSE:RSI) is well positioned to take advantage of this growth.

RSI owns their own online gaming platform, which allows them to quickly implement new features and improve the player experience. This proprietary platform is also more cost-effective and generates higher ARPU than competitors who license their technology. RSI also has control over their underlying technology stack, which allows them to scale efficiently and offer a user-friendly interface.

Overall, I believe RSI is a good investment opportunity due to the growth potential of the online gaming industry, their strong presence in key markets, and their proprietary platform and technology stack.

Business

RSI is a gaming business that focuses on the American and Latin American markets for online casino and sports betting. They offer a variety of services to their consumers, including social gaming, e-sports betting, and a traditional online casino.

Online gaming is on fire

Recently, online gaming’s popularity and reach have skyrocketed. As far as I’m concerned, there are a lot of things pushing this market forward. Examples include the proliferation of legal frameworks for internet gambling and sports betting in both the United States and internationally, as well as the trend toward privatizing these sectors. Consumers’ use of digital entertainment like casinos and sportsbooks has also increased with their legitimization by government. However, surprisingly, the U.S. gaming business is just getting started with digitalization, although many other significant US industries have been doing so for over a decade.

The worldwide online gambling business has seen substantial regulatory impetus during the past decade. This pattern is most pronounced in wealthy nations, where people have more discretionary income to spend on leisure activities like video games. The United Kingdom, France, Spain, and Italy are just some of the European countries that have legitimized and regulated internet casinos and online sports betting. In the United States in particular, I think this trend will persist.

Focus on iGaming and Sports Betting

With its dual emphasis on iGaming and Sports Betting, RSI is positioned to capitalize on one of the gaming industry’s most significant industries. My expectation is that the business model will eventually scale at a pleasing cadence due to its over-indexing to the more lucrative iGaming niche. The concurrent emphasis on sports, as well as the emerging possibilities in social gaming, as springboards for cross-selling into online casino, strikes me as genuinely encouraging, especially in light of the far more favorable unit economics.

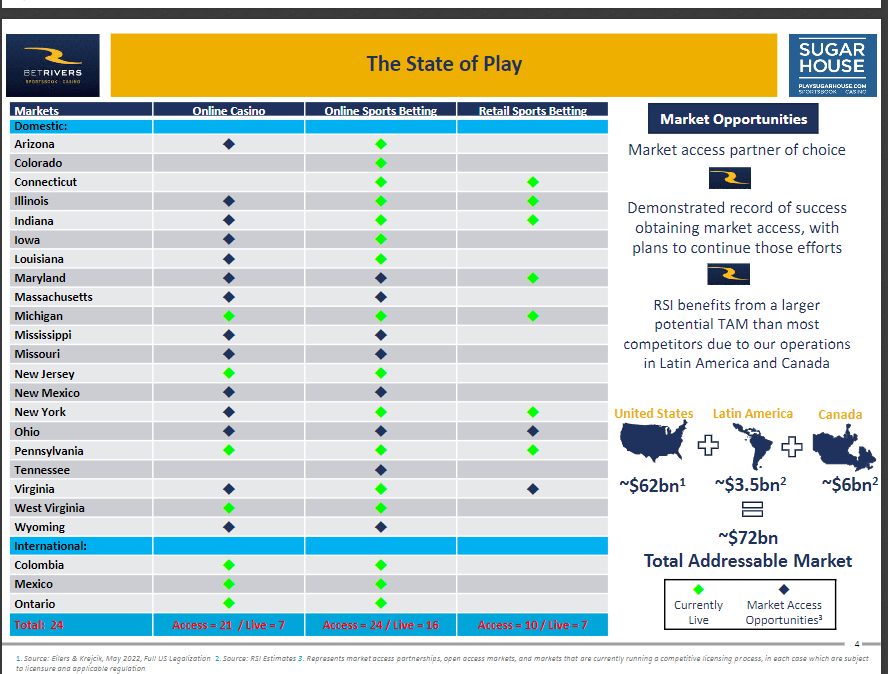

Presence in key states

RSI provides its services to states with populations of over 50 million people for online gambling (refer to states cited below). In addition, RSI has gained foothold in multiple states with combined populations of more than 10 million, provided that these governments implement online gaming regulations. More importantly, RSI has proven over and again that it can swiftly infiltrate regulated markets. The S-1 states that RSI was one of the first companies to offer sports betting in states where it was legal to do so, including New York and Illinois for land-based sportsbooks and Pennsylvania, Indiana, Colorado, Michigan, and Illinois for online betting. This is an important point to note as I believe there will be a lot more opportunities across the globe. Having the capability to act swiftly to capture the opportunity is a core part of my assumption on RSI long-term growth.

Nov 22 investor presentation

Proprietary gaming platform with long-term benefits

RSI owning its own online game platform, in my opinion, has many benefits. As an example, this has allowed RSI to rapidly implement new features aimed at improving the player experience. From what I’ve seen, these additions have led to an increase in both new signups and first-time deposits, as well as in customers’ willingness to stick around and spend money. Online gaming is a rapidly expanding market in the United States, and I expect RSI proprietary platform will allow it to better meet the demands of its customers as the market evolves. Long-term, I believe the RSI platform will outperform competitors who license their technology as it is more cost efficient and generates higher ARPU.

Underlying tech stack is an advantage

RSI’s ability to manage its own technological stack puts it in a good position to scale at a cheap cost and offers the firm control the most essential features to iGamers: the UI/UX and the simplicity of use. Like I said before, I think RSI’s ability to advance from a strong starting point is supported by the proprietary platforms it has established. By keeping the player accounts and front-end structure in-house, RSI is in a stronger position to innovate and navigate the industry trends than peers. These integral parts of the tech stack eliminate the need for external service providers, allowing for faster, more reliable rollouts. However, the value of analytics and data truly shines when it’s used to inform more tailored approaches to client retention through a company’s own technology stack.

Presence in social gaming

RSI’s participation in the social gaming market is beneficial, in my view. Firstly, the young but rapidly expanding market is one of the game industry’s most promising prospects. To put things into perspective, an estimated $8.7 billion will be wagered on the worldwide social casino industry by 2026, according data from Research and Markets.

The previous decade has seen a number of attempts for social casino initiatives in the traditional, hard-asset parts of the industry, with varying degrees of success. As an example, in 2012, IGT bought DoubleDown to supplement its mainstay slot machine and technology operations. DoubleU Games acquired DDI for $825 million in 2016 after IGT joined with Lottomatica. Churchill Downs, separately, acquired Big Fish Games in 2015 for $885 million. Although social casino has seen mixed results as a standalone branch of more established companies, it has proven to be a fruitful field for IT and gaming companies and is likely to do the same for RSI.

But perhaps more importantly, it can be released even before legalization takes effect. The advantage of lower cost of player acquisition and higher player LTVs can be realized through the early cultivation of brand awareness and databases in preparation for product launches. I think there’s a lot more opportunity to upsell these customers to sports betting and online casinos. I expect that the growth of social gaming will resemble the establishment of fantasy sports for sports betting operators, where they saw reduced churn rates and better customer acquisition metrics.

3Q weak earnings and guide down is not helpful for the stock

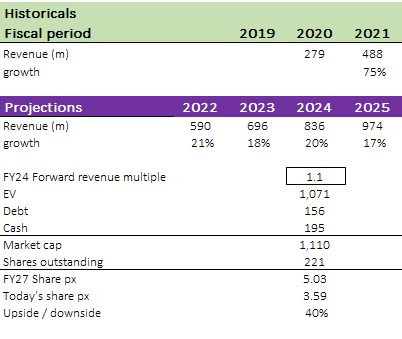

Revenue projections for FY22 have been lowered from $600 million to $630 million to $580 million to $600 million. This is mainly due to weaker-than-anticipated iGaming retention and negative FX effects.

Falling casino hold percentages and currency fluctuations contributed to a shortfall in third-quarter revenue. When added to the downward revision in revenue guidance, I expect the stock to face near-term overhang. This quarter’s reduced loss reflects the company’s disciplined approach to customer acquisition and execution. The significant share of the Ontario market that RSI has attained, among other markets, is further evidence of the company’s execution prowess. The enhanced results have led me to believe that RSI will become profitable in terms of adjusted EBITDA in the second half of FY23E, and I maintain that outlook.

Valuation & model

I believe that RSI is currently undervalued in the market, and I expect it to be worth roughly 40% more in FY24. While the macroeconomic environment is weak at the moment, I believe that RSI will continue to see strong revenue growth due to favorable industry trends and the company’s successful initiatives to capture more market share.

It’s worth noting that RSI is currently trading at a low multiple of forward revenue, close to its all-time low. I believe that this low valuation is largely due to a negative near-term outlook, which has been exacerbated by poor guidance from the company. However, I believe that this narrative does not accurately reflect the long-term intrinsic value of RSI. If the company can continue to post rising profits faster than expected, I believe we will see an inflection in valuation multiples.

Even considering the current valuation and my projected growth rates, I still see a lot of upside potential for RSI over the next two years.

Author’s own calculations

Risks

Regulatory

The regulatory risk for this stock will always be present. If fewer states legalize mobile sports betting and online gaming than expected, or if the tax rates for these activities are higher than anticipated, it could negatively impact RSI’s.

Online gaming might not be as great as I thought at maturity

The online gaming and sports betting industry in the US is still relatively new and uncharted, so we don’t have a lot of information about it yet. Things like the competitive landscape, market share for different operators, consumer spending habits, and long-term profit margins are all mysteries. My projections for RSI’s long-term success could be easily swayed by small changes in how I estimate these unknown factors.

Summary

I expect the online gaming industry to continue growing. RSI is a gaming company that operates in the online casino and sports betting markets in the U.S. and Latin America. They have a strong presence in key states and have proven to be able to quickly enter new markets as they become regulated. They own their own online gaming platform, which allows them to quickly implement new features and improve the player experience, leading to an increase in new signups and customer retention. They also have control over their underlying technology stack, which allows them to scale efficiently and offer a user-friendly interface for online gamers.

Be the first to comment