stevecoleimages/E+ via Getty Images

Before I get to the happy talk of the future what happened last week?

I won’t hide behind the warning that I made last week that we will have residual volatility going forward. The market of the Friday before had the S&P rally back to nearly even, which gave me hope that this past week will rally into the PPI. Instead, on Monday the Service PMI was strong, and that seemed to send the market to the downside – hard. That was the catalyst, the sell-off was technical.

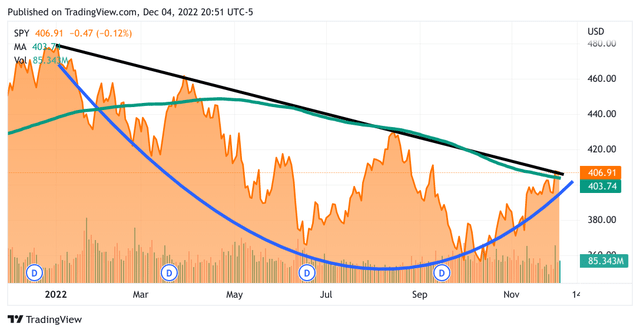

So we went from this SPY chart of last week

TradingView

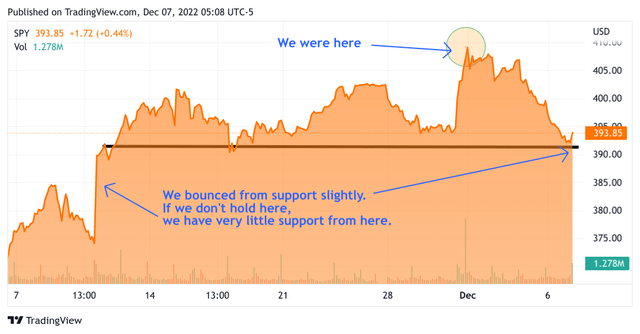

To this chart last Thursday

TradingView

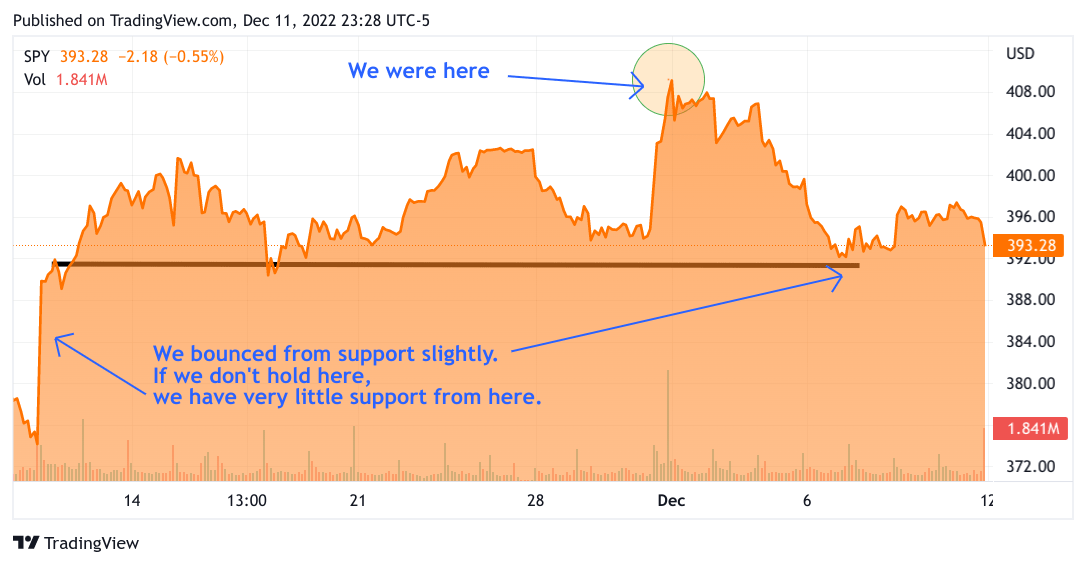

To this chart this past Friday

TradingView

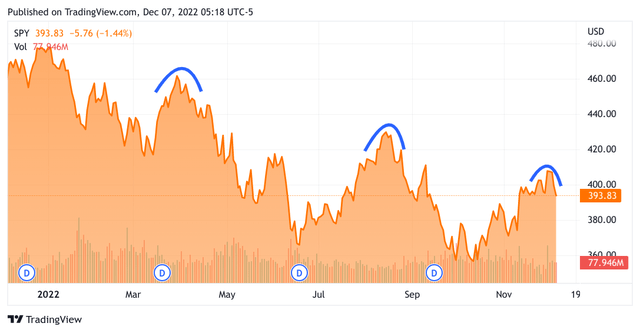

This black line is still offering support but I would not be surprised if we break support and the gap-up at the left side gets filled as we approach Tuesday’s CPI reading perhaps approaching 3800. Bears are pointing to the long-standing pattern below which shows a very well-defined downtrend all year.

TradingView

My optimism took the back seat this past Monday the moment we faltered from the Service PMI data, as good still is bad news with ISM’s Employment Index registered at 51.5%t, up 2.4% from the October reading of 49.1 percent. The “algo” traders focused on the negative and sold the market down hard. If we would have gotten better inflation data on the PPI our rally should have restarted. It seems like a century ago but the prior Friday the strong employment data initially caused a sharp sell-off but then it came all the way back. The optimistic scenario was that market participants will recognize that healthy employment does NOT cause inflation. Yes, many companies are announcing layoffs, and most seem to be prophylactic in nature. That means they are trimming fat, raising productivity. The excess manpower is going to where it is needed most, to the unfilled jobs of smaller and medium-sized companies. This is VERY healthy for the economy and inflation! Not as the lazy financial media constantly repeat. Powell said as much in his last public statement. He wants to target all those open jobs previously unfilled. Well the PPI didn’t cooperate to the extent of the number expected. In fact on a month-over-month basis, the number ticked up! Have you ever seen a chart consistently go down in a straight line? Well, the market wants what the market wants. Let’s look at the data now that a few days have gone by and we can look at this rationally. Take a look that BLS’s own chart. At the top, we have the month-to-month, and yes it did tick up. However, look at the year-over-year, which should be the more important number, and we are still on a downslope!

Bureau of labor statistics

So I believe that we may have a volatile week and some losses again, but the Fed is still going to raise by .50% and Powell will still play the hawk. He will have to explain why they decided to go with .50% instead of .75%, and that means we are almost done. We could very well rally into year-end, and reach for 4300.

What worked in spite of the selling this week? My Trades

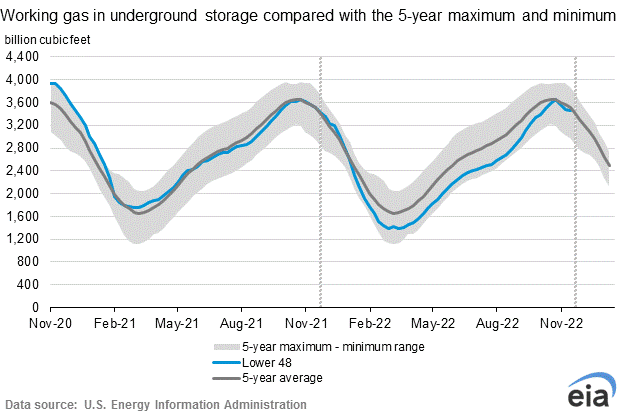

Ok, so what worked this week? Did you notice NatGas surged last week? It didn’t help every driller but Natgas reserves are falling greater than expected, and below the 5-year average to start. See the chart below from the US Energy Information Agency.

US Energy Information Agency

This is the EIA Conclusion: Working gas in storage was 3,462 Bcf as of Friday, December 2, 2022, according to EIA estimates. This represents a net decrease of 21 Bcf from the previous week. Stocks were 51 Bcf less than last year at this time and 58 Bcf below the five-year average of 3,520 Bcf. I believe that with the Freeport LNG opening up at the end of this month traders will once again bid up US NatGas as there will be even less gas available for storage. It is worth noting that production should rise for NatGas for later this year which should moderate NatGas prices but I see it rising well above 6 bucks in short order. Why? Well for one reason China has scrapped the mobile app that tracks Chinese citizens’ movement attaching it to the dismantling of their Covid-zero regime. While this movement tracking app was initially required for Covid, I would think the CCP loved to have this tracking on permanently. I think they are working very hard to calm the populace after years of cracking down on personal freedoms in China such as they were.

With China reopening faster than anyone would have believed Oil consumption is sure to rise. We have the possibility that China will once again be an engine of growth. First, it will have to dig out of its recession, and then kick in with incentives to drive internal consumption and growth. They can’t rely on export growth. The most they can hope for is not to lose more factories. This will mean a kinder gentler China once again – well maybe if Xi gets smart. The Dual Mind Community got long with BOIL as it was crashing all last week, until Friday when it jumped 10%, and we of course expect it to go higher. I have the 3X Bull NatGas ETF (BOIL) equity and in addition, I have several long Puts At The Money with a January EXP. This past week Oil did not rise, though I believe that will change with China reopening in full bloom I expect WTI to begin to rise back to the mid-80s once again. So I have the usual suspects that I always talk about Apache (APA), Coterra (CTRA), and Devon Energy (DVN), for NatGas I have EQT (EQT), and Range Resources (RRC). I started a position in Nutanix (NTNX) an old favorite of mine that is finally turning in good financial results. Rumors about HPE kicking the tires didn’t hurt. I am also very excited to add Textron (TXT) to my aviation/defense names. They were awarded the next-generation VTOL for the US Army, ultimately to replace the 2,000 Blackhawks and the 1200 Apache attack helicopters. No one seems at all impressed all they see is the initial payment of $1.2B, and not the $120B the ultimate revenue this will bring over the next several decades. Remember that this is a cost+ contract. Guess what the market cap of TXT is right now? $100B? $50B, $40B?? How about under $15B? Isn’t that nuts? Also, they will likely come out with a commercial version, which will disrupt the entire helicopter industry with a much longer range and faster top speed, let’s not forget, a much larger cabin.

The rest of my activity is devoted to hedging using Call options on SDOW, SPXS, HIBS, and puts on TQQQ. Well, that’s it. Hopefully, the market is volatile enough to make both the bulls and bears happy this week.

I conclude that we still have a shot at 4300 for the year-end

My conclusion is that once we get past the CPI with a decent chance that the CPI is favorable. Why? Because the CPI has items that are different than the PPI like rents which have been coming down, and big ticket items are no longer scarce so their prices have come down. More new cars are sitting in dealerships, so at least they can’t charge over book. Gasoline is down, and while energy prices aren’t core they creep into other prices. So overall I am once again optimistic. Good luck everyone!

Be the first to comment