jewhyte/iStock Editorial via Getty Images

(Note: All amounts in Canadian dollars unless otherwise indicated)

One might say I have a rather mixed relationship towards banks and banking stocks. I own Svenska Handelsbanken (OTCPK:SVNLF) and I consider several other banks undervalued – as most banks are trading for very low valuation multiples. Nevertheless, I am not willing to invest in banks right now as I consider it a horrible idea to invest in banks at the eve of a global recession.

However, when I start investing in banks, Canadian banking stocks are definitely on the list and the Royal Bank of Canada (NYSE:RY) is probably taking the top stop. My last article about the Royal Bank of Canada I was rather bullish about the stock and although the stock is now trading about 10% lower, I will rather take a neutral stance right now.

Quarterly Results

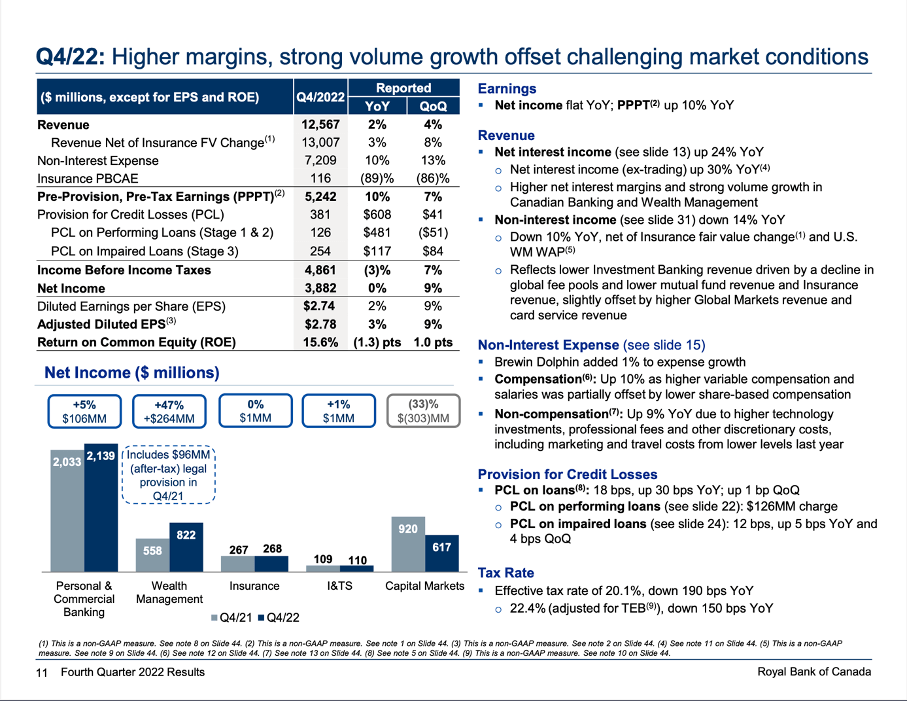

While the Royal Bank of Canada did not report great results for the fourth quarter or full year fiscal 2022, we are also far away from seeing any troubles right now. In Q4/22, the bank reported a total revenue of $12,567 million and compared to $12,376 million in revenue in the same quarter last year this is an increase of 1.5% year-over-year. And diluted earnings per share also increased 2.2% year-over-year from $2.68 in Q4/21 to $2.74 in Q4/22.

Royal Bank of Canada Q4/22 Presentation

When looking at the full year results, revenue declined slightly from $49,693 million in 2021 to $48,985 million in 2022 – resulting in a decline of 1.4%. Diluted earnings per share were exactly the same as one year earlier – $11.06 in 2021 as well as in 2022. And this is quite an accomplishment when considering that the Royal Bank of Canada could reduce provision for credit losses by $753 million in 2021 and reported a (positive) provision for credit losses of $484 million in 2022. The reason were mostly the lower insurance policyholder benefits, claims and acquisition expenses – instead of $3,891 million in 2021 it was only $1,783 million this year.

HSBC Canada Acquisition

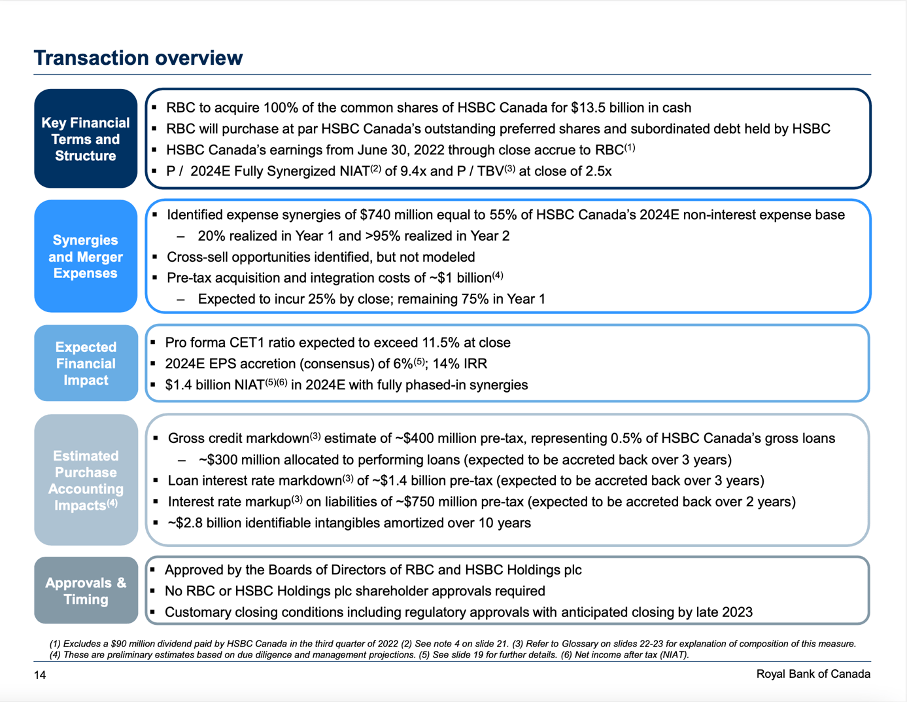

At the end of November 2022, HSBC and the Royal Bank of Canada announced that HSBC will sell its banking operations in Canada to the Royal Bank of Canada for $13.5 billion in cash. The deal is expected to be completed in late 2023.

RY HSBC Canada Acquisition Presentation

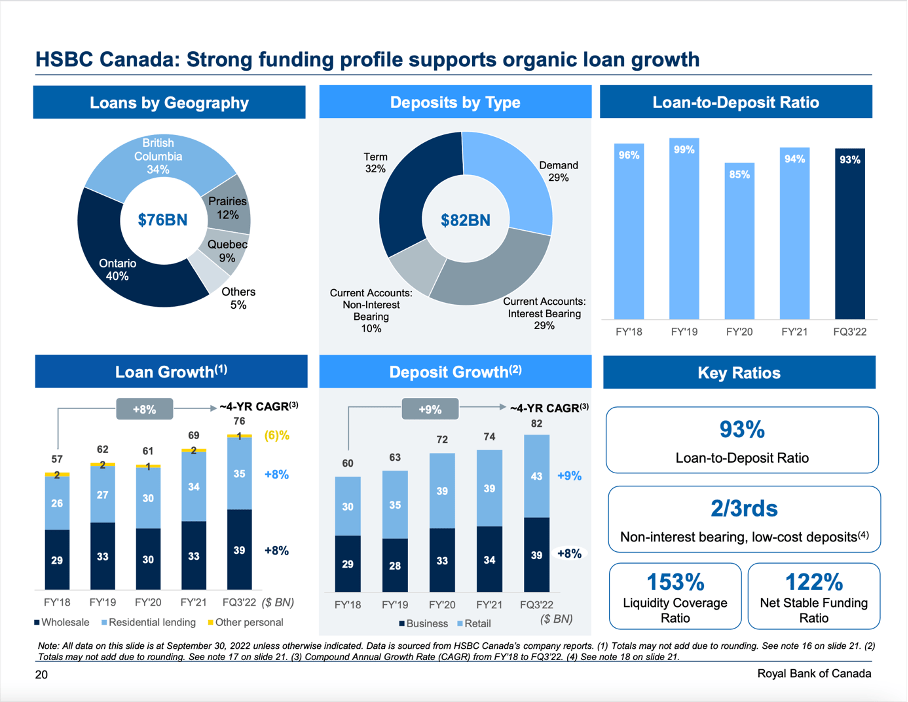

HSBC Canada is operating since 1981, has about 130 branches and about 4,200 employees. Right now, the company has about 780,000 retail and commercial customers and as of September 30, 2022, HSBC Canada had $134 billion in assets and about $19 billion in assets under management. Additionally, the company has about $76 billion in loans and about $82 billion in deposits (both growing in the high single digits in the last few years).

RY HSBC Canada Acquisition Presentation

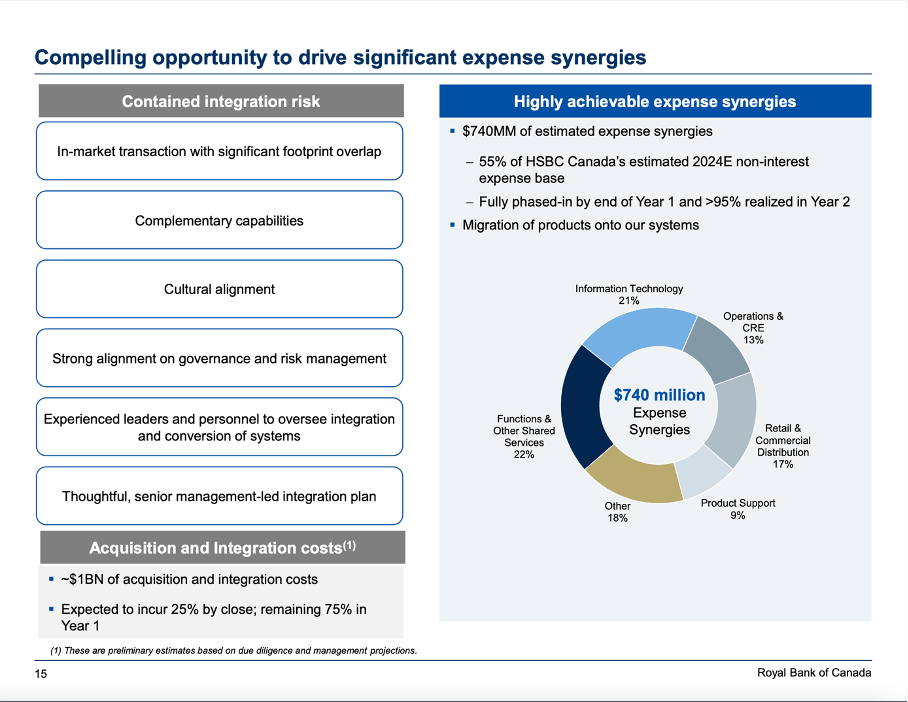

The Royal Bank of Canada is expecting adjusted earnings to be around $1.4 billion in 2024, which would result in about 9% higher earnings for the bank. This means that the Royal Bank of Canada paid about 9.5 times expected (!) earnings for the business, which is certainly acceptable if these earnings materialize.

It seems like the Royal Bank of Canada is paying a premium, but if expected 2024 earnings per share materialize, the valuation seems reasonable. The problem is that the expected earnings per share are already including synergy effects and we should always be a little cautious if expected synergy effects during acquisitions actually materialize.

RY HSBC Canada Acquisition Presentation

Dividend

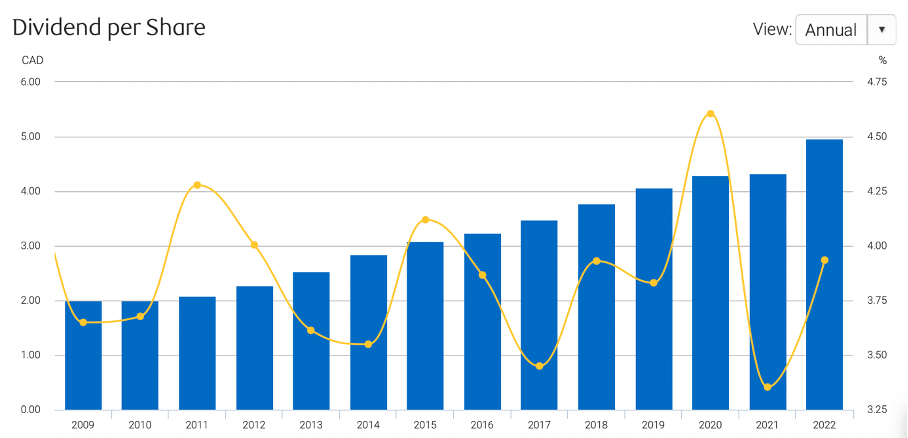

And of course, the Royal Bank of Canada – like many other banks – is interesting for its dividend. Right now, the company is paying a quarterly dividend of $1.32 resulting in an annual dividend of $5.28 and in a solid dividend yield of 4.1%. After the dividend was already increased two quarters ago (from $1.20 to $1.28), the Royal Bank of Canada increased the dividend again – like the Bank of Nova Scotia (BNS) did – but this time the dividend increase was “only” 4 cents.

When using the forward annual dividend and comparing it to earnings per share for fiscal 2022 ($11.06), we get a payout ratio of 48%, which is rather at the top end of the targeted payout range (between 40% and 50%). Hence, I don’t think we will see a huge dividend increase next year – especially as we must assume lower earnings per share in the coming quarters, which will lead to a higher payout ratio (even if the Royal Bank of Canada is keeping its dividend only stable – also a possibility).

RY Investor Relations

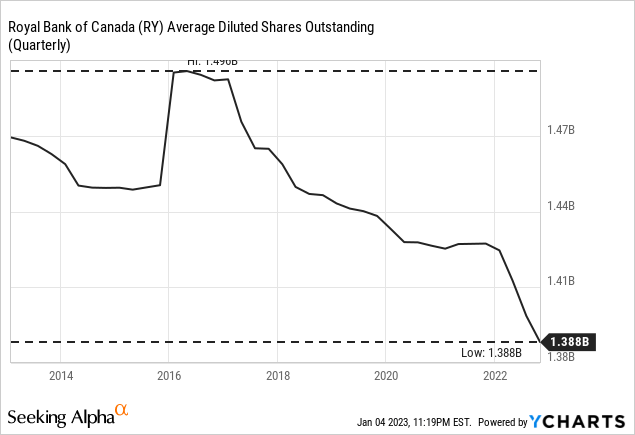

The Royal Bank of Canada also started buying back shares in the last few years – something the company did not really do during the past decade. In the fourth quarter of 2022, the company bought back 7.9 million shares (for $1 billion) and in fiscal 2022 the company bought back 41 million shares (for $5.4 billion).

And this does not make the Royal Bank of Canada an aggressive buyer of its own shares, but since 2016 the number of outstanding shares was reduced about 7% and in the last 12 months the number of outstanding shares was decreased by 2.6%.

Intrinsic Value Calculation

And like many other banks, the Royal Bank of Canada not only has an above-average dividend yield, it is also trading for low valuation multiples.

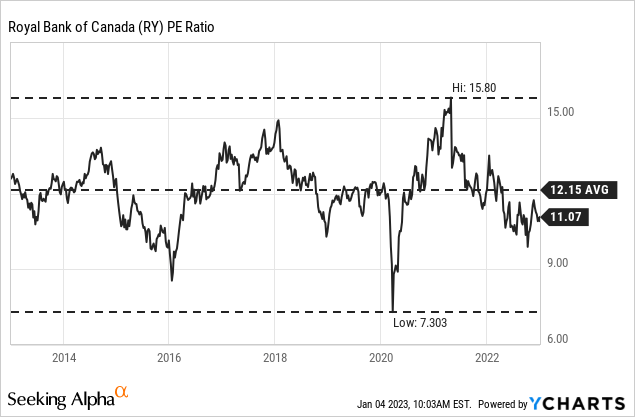

At the time of writing, the Royal Bank of Canada is trading for 11 times earnings and as the stock has always been trading for low valuation multiples in the last decade, this is only slightly below the average P/E ratio of 12.15 in the last ten years.

RY Investor Presentation November 2022

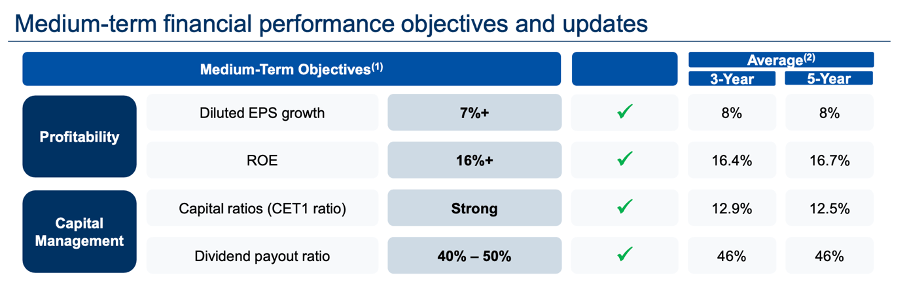

When trying to calculate an intrinsic value by using a discount cash flow calculation and the medium-term objectives for the bank, the stock is deeply undervalued. We are cautious in our assumption and assume a 50% decline in earnings per share for fiscal 2023 (due to a global recession). Let’s also assume it takes until fiscal 2026 before the Royal Bank of Canada is able to generate the same net income as in 2022. For the following years we assume 7% growth (according to medium-term objectives) and after 10 years from now we assume a growth rates of 6% till perpetuity. When calculating with these assumptions (and 1,389 million outstanding shares and 10% discount rate) we get an intrinsic value of $243.15 while the stock is trading for $128 right now. And when looking at the growth rates in the last decades, 6% to 7% growth seem achievable.

|

Since 2012 |

Since 2002 |

Since 1990 (reported loss in 1992) |

|

|

EPS CAGR |

8.33% |

8.99% |

8.78% |

Recession-Resilient

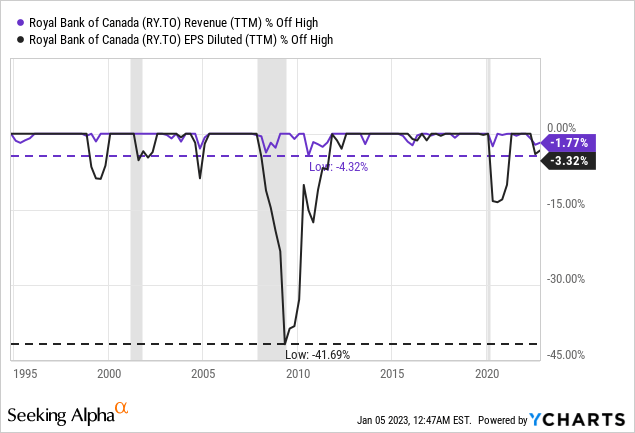

Not only is the Royal Bank of Canada paying a solid dividend and trading for an extremely low valuation multiple – the stock also seems to be rather recession-resilient (at least when compared to other banks). When looking at the last 30 years we see a very stable performance. While other banks had to report losses in several years during the last decades, we must go back until 1992 to find a reported annual loss for the Royal Bank of Canada.

And when looking at the recessions in the last three decades (the chart is showing recessions in the United States and the years following the 2000 Dotcom bubble are not seen as a recession in Canada), the Royal Bank of Canada was reacting – but we also see these reactions were rather moderate. Revenue did not decline steeper than 4.3% since 1995 and during the Great Financial Crisis, earnings per share declined about 40% (also a modest decline compared to most other banks.

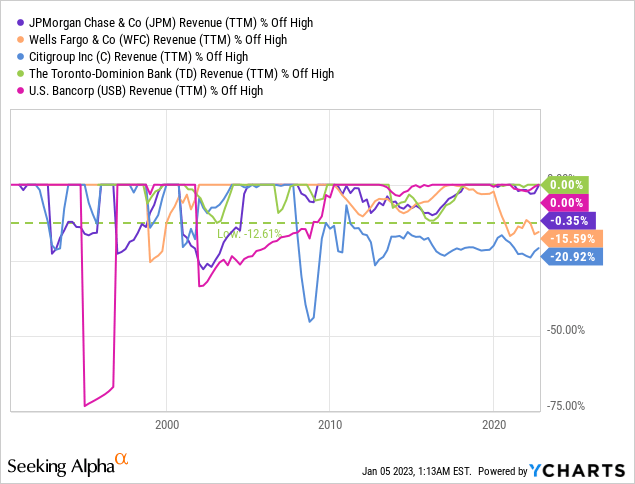

When comparing this to other banks, a decline of only 3% is extremely modest. Even the Toronto-Dominion Bank (TD), which can be seen as similar stable as the Royal Bank of Canada has seen a 12% decline during the last three decades – and most other American banks saw much steeper declines.

Problem: Housing Market

We saw above that the Royal Bank of Canada was performing quite well during past recessions. However, we also know that recessions are a challenging time for banks as these businesses also struggle when the economy struggles. Therefore, I am quite cautious about buying banks right now. I already talked about this in my article about U.S. Bancorp (USB) as well as the Bank of Nova Scotia.

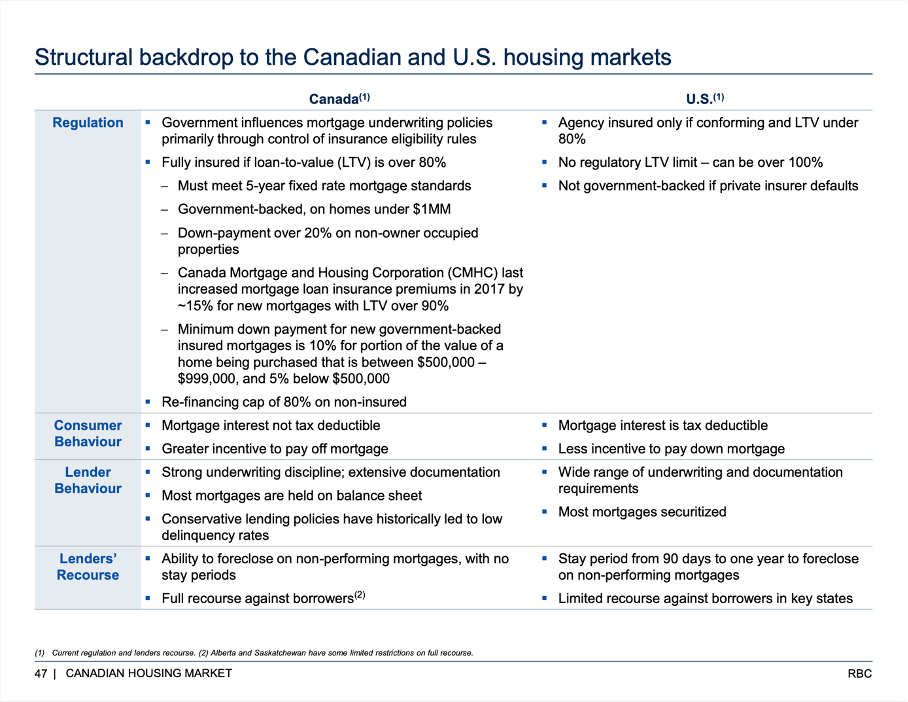

Especially the extremely expensive Canadian housing market is often seen as reason for concern. And while we must not necessarily fear a housing crash like 2007 in the United States (however, I would also not rule out such a scenario), we are looking at a combination of factors that could be problematic. First, mortgage rates in Canada are usually fixed for only 5 years (see Royal Bank of Canada page for example). I could not find any reliable statistics, but it seems that only very few mortgage contracts have rates fixed for more than 5 years. And this is posing a risk as everybody must refinance now at much higher rates than the last time they had to refinance (or signed a loan agreement).

Second, the extremely high housing prices right now is making a decline more likely. Especially in the last two years, housing prices increased with an extremely high pace and decoupled from economic growth rates – a development that is usually not sustainable.

A third issue is the declining disposable income and people getting unemployed during recessions and economic downturns – making it more difficult to meet payments and increasing the likelihood for delinquencies.

But it is good to know, that the Royal Bank of Canada is well positioned to withstand challenging times.

RY Investor Presentation November 2022

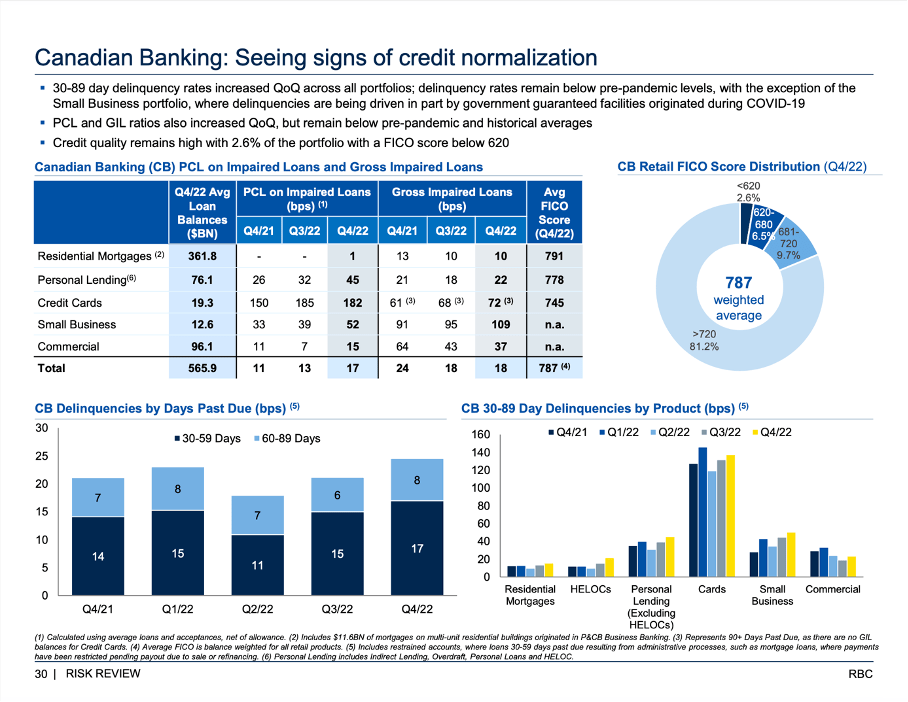

While fixing mortgages rates for 5-years on average is not a long time, it is good to know that every mortgage with less than 20% down payment must be insured by a mortgage loan insurance. And this is only one aspect of the different regulations making the Canadian housing market more resilient to crisis. And knowing that any mortgage with loan-to-value above 80% is not only insured but backed by the government (for homes under $1 million) is leading to stability. It seems like declines in housing prices up to at least 20% should not lead to any major risks.

RY Investor Presentation November 2022

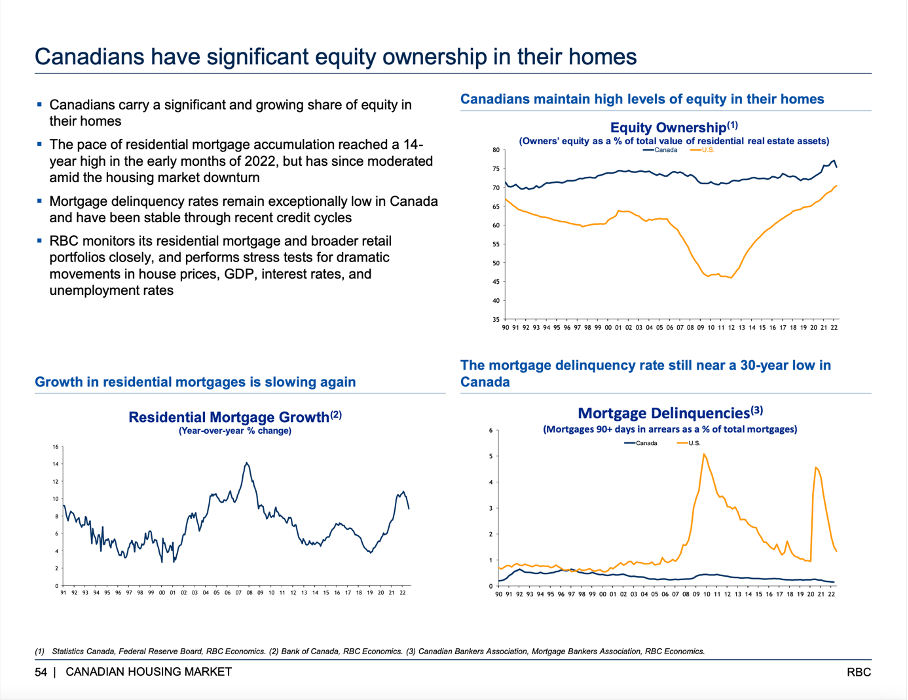

Equity ownership is also much higher in Canada than in the United States. This is probably one of the reasons why mortgage delinquencies in Canada have been low – even during the COVID-19 crash as well as during the Great Financial Crisis.

RY Investor Presentation November 2022

And with an average FICO score of 787 and 81.2% of mortgages having a FICO score above 720, the Royal Bank of Canada should be able to withstand a declining housing market without running in any major troubles (although the Royal Bank of Canada is forecasting housing prices to decline 8.9% in 2023).

RY Investor Presentation November 2022

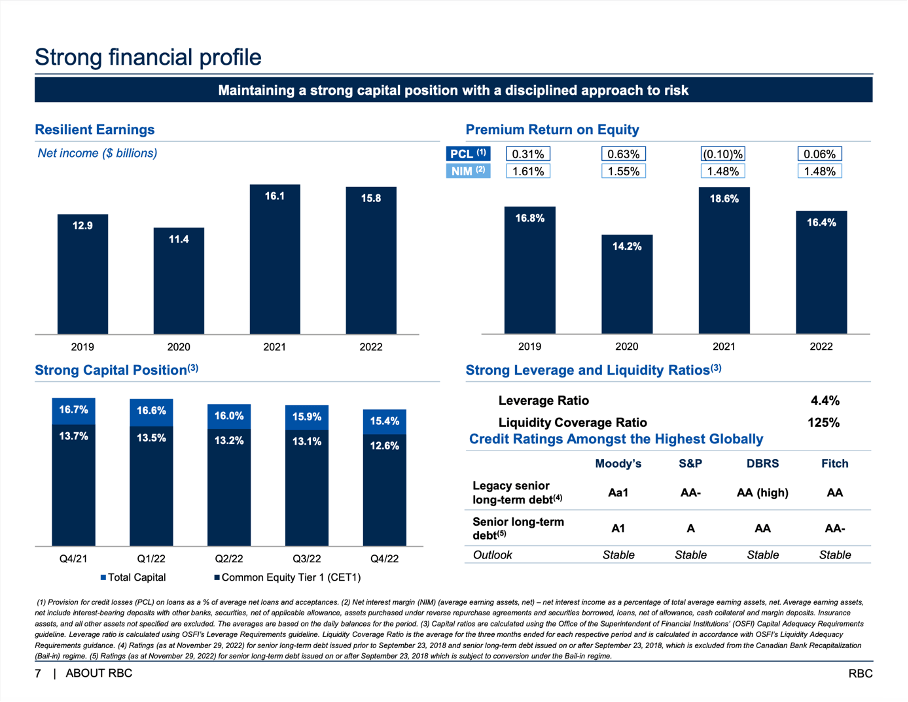

And although the Common Equity Tier ratio declined a little bit in the last few quarters, 12.6% is still very solid and not really reason for concern. Additionally, the Royal Bank of Canada is receiving strong credit ratings from all major credit rating agencies.

When looking at further ratios to measure the quality of the balance sheet, the Royal Bank of Canada is also performing very well. We can for example look at the loan-to-deposit ratio and with $811.6 billion in total loans and $1,203.8 billion in total deposits we get a ratio of 67%. Usually, every ratio below 80% is seen as solid and no reason to worry. Or when looking at the loan to asset ratio (total assets are $1,991.5 billion), we get a ratio of 0.4 and here ratios below 0.6 are seen as acceptable.

When Will I Invest?

At this point, one might ask why I am so reluctant to invest in banks – despite the solid dividend yield, the low valuation, and the high quality of the business for some banks – including the Royal Bank of Canada. The answer is not so simple and not just based on fundamental aspects. My reservations are based on two different aspects.

First, fundamental problems which are not visible yet. We established above, that the Royal Bank of Canada has a solid balance sheet, great metrics and seems to be stable for several decades, which is certainly reassuring. However, I know what I don’t know – and I simply don’t know enough about banking to detect underlying issues a bank might have. And I know that not just the economy, but our society is an extremely complex system with feedback loops, unintended consequences, chain reactions and interdependences that could lead to outcomes nobody – and I mean nobody – could have foreseen. And banks are a prime candidate for such negative outcomes due to a high level of complexity.

Second, sentiment and typical bear market behavior. While the Royal Bank of Canada is already trading for a low valuation multiple, I have troubles to imagine that banks will withstand a global recession and bear market. It could happen – due to the rather low valuation multiples – but in my opinion we will see at least a 20% to 30% drawdown for most banking stocks (and this is including stable banks like the Royal Bank of Canada).

To answer the question when I will invest: When the crisis is already in an advanced stage – maybe with housing prices significantly down, maybe delinquencies increasing and unemployment already at a high level. When the Royal Bank of Canada is still performing solid at that stage (and revenue as well as earnings per share can decline), I will start investing.

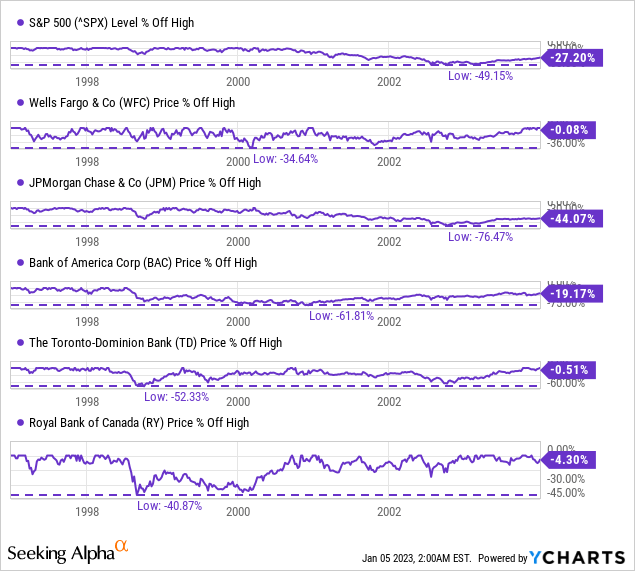

And I honestly don’t think banks will bottom several quarters before the S&P 500 finds its bottom. In the years 1998 and 2000 several banks actually bottomed before the Dotcom bubble found its low.

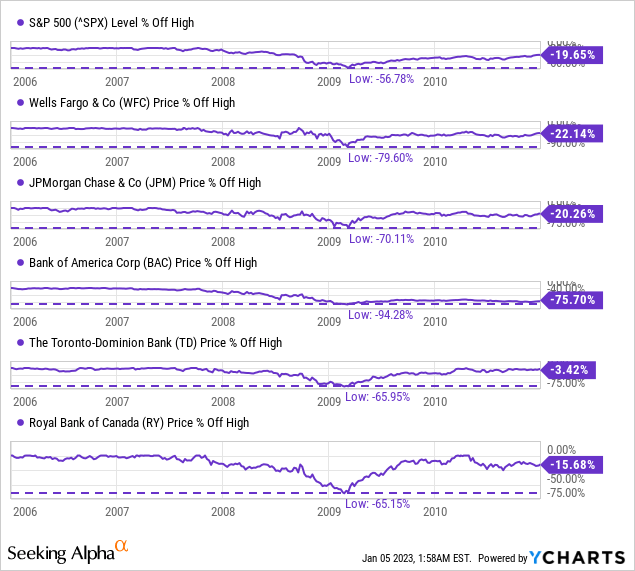

But in 2009, almost every bank bottomed together with the S&P 500.

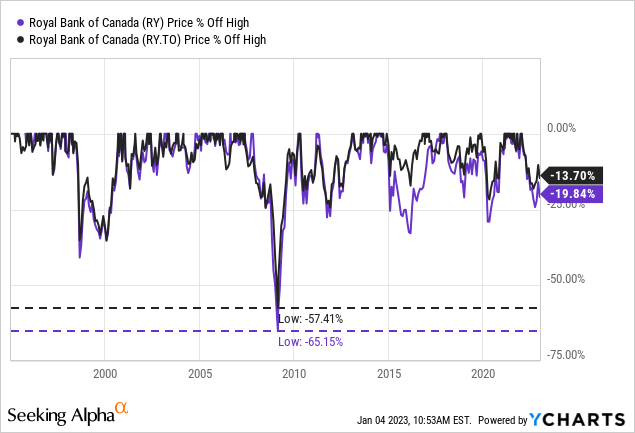

We don’t have to see an extremely steep decline for the Royal Bank of Canada, but the stock declining 30% to 40% from its previous high is not unlikely. In the years following 1998 the stock declined about 40%, during the Great Financial Crisis it declined 57% – and I expect a more or less similar decline this time as well.

Conclusion

The Royal Bank of Canada is a great business with a wide economic moat, a solid dividend yield and trading for a rather low valuation multiple. And while the overheated Canadian housing market is posing a threat, the Royal Bank of Canada is in a good position to withstand troubles. Nevertheless, I will still wait with an investment as I expect the stock price to decline further, and I like to see some proof that the Royal Bank of Canada can really withstand the next potential crisis. And once, the Royal Bank of Canada has proven that, I will buy as the stock is really cheap.

Be the first to comment