Kameleon007

Investment Thesis

Roper Technologies, Inc. (NYSE:ROP) is poised to do well despite slowing macros, thanks to its recurring revenue base, a business portfolio with higher margins, and a continued shift of its customers from on-premise maintenance to cloud solutions. Furthermore, healthy demand and a robust backlog for water and medical products, along with the company’s strategy of expanding and acquiring businesses with high levels of recurring revenue, should also support its revenue growth.

The company is expected to see margin improvement due to improving supply chain conditions, operating leverage, and a mix shift towards a higher-margin business portfolio. The company is currently trading at a lower valuation compared to its historical average and given its good growth and margin expansion prospects in the long term, I believe it’s a good buy.

Revenue Outlook

In recent years, Roper Technologies’ revenue growth has benefited from its transformation from low-margin, cyclical businesses to a portfolio with high levels of recurring revenue and a focus away from project-oriented businesses.

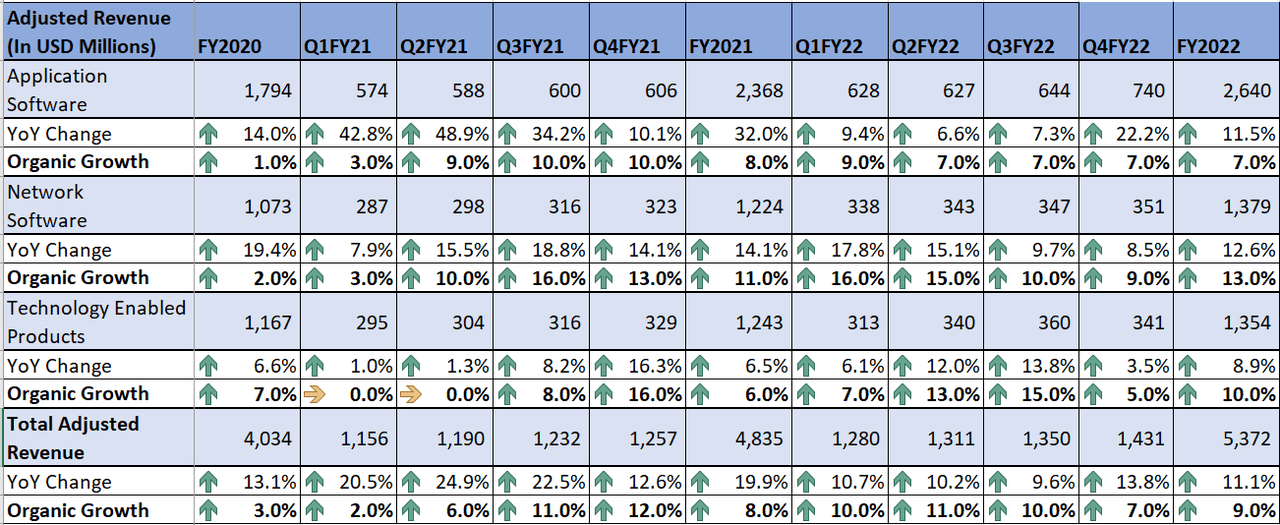

In Q4 2022, the company continued to see growth with a 10% increase in software recurring revenue. ROP reported overall revenue growth of 14% YoY, helped by strong SaaS bookings, high retention rates, and solid demand for water and medical products. The growth included an 8- percentage point benefit from acquisitions and a 2-percentage point headwind from foreign exchange. Organic revenue grew by 7% YoY.

ROP’s Historical Revenue (Company Data, GS Analytics Research)

Looking ahead, I expect ROP to sustain its revenue growth in the future. This growth should be driven by strong demand and a robust backlog for the medical and water products in the Technology Enables Product segment. Additionally, with high retention rates, a 60% Annual Recurring Revenue (ARR) as a % of total revenue, and a 75% recurring revenue in its software businesses, the company is relatively better positioned to overcome any macro slowdown.

Furthermore, the company is focused on cross-selling and up-selling to increase its revenue from existing customers. The company currently derives $900 million in revenue from its on-premise maintenance customers. Roper Technologies plans to transition these customers to its cloud solutions over the next 5-10 years, and estimated $1 billion-plus in additional revenue from these customers post-transition. To achieve this the company is expanding its Software-as-a-Service (SAAS) offerings in its Application Software segment. In Q4, the PowerPlan business launched its first SaaS solution, Tax Fixed Assets, which combines financial and asset tracking systems. These types of offerings should help increase the company’s ARR over time. The company is improving its offering in other segments as well. For example, in the Network Software segment, the company recently introduced a subscription model for Foundry Business’ Nuke product, a visual effects application software.

In addition to good long-term organic growth prospects, the company’s M&A strategy which focuses on growing its portfolio in niche markets through acquiring and expanding high-margin, high-recurring revenue businesses, should also help its growth. Last year the company divested the majority of its cyclical industrial business and acquired Frontline Education, a provider of SaaS software targeted at the U.S. K-12 education market. The company still has a favorable balance sheet, with a net debt-to-EBITDA ratio of 2.7x and the ability to leverage up to 4x. This healthy balance sheet and good FCF generation profile give Roper approximately $4 billion in acquisition capacity and the company plans to remain active in the M&A market throughout 2023. This should support continued revenue growth in the years to come. So, I am optimistic about the company’s growth prospects.

Margin Analysis and Outlook

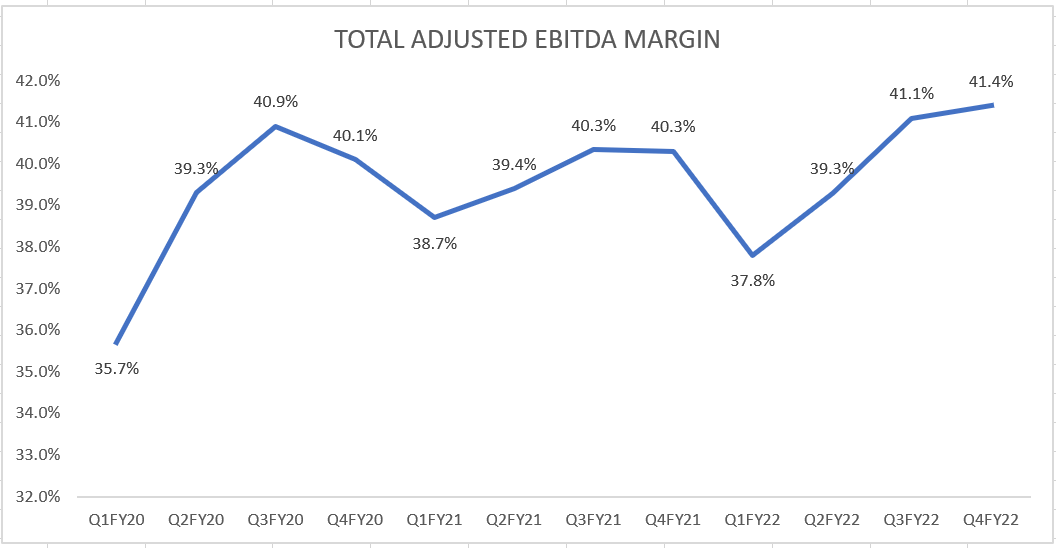

After seeing a dip in 1H22 due to increased labor costs and disruptions in the supply chain for the Technology Enabled Products segment, ROP’s adjusted EBITDA margin improved in the second half of the year as supply chain constraints ease and the company experienced benefits from operating leverage.

In the fourth quarter of 2022, the adjusted EBITDA margin rose by 110 basis points YoY to 41.4%, thanks to easing supply chain conditions, lower incentive-based SG&A, and lower employee medical costs.

ROP’s Historical Adjusted EBITDA Margin (Company Data, GS Analytics Research)

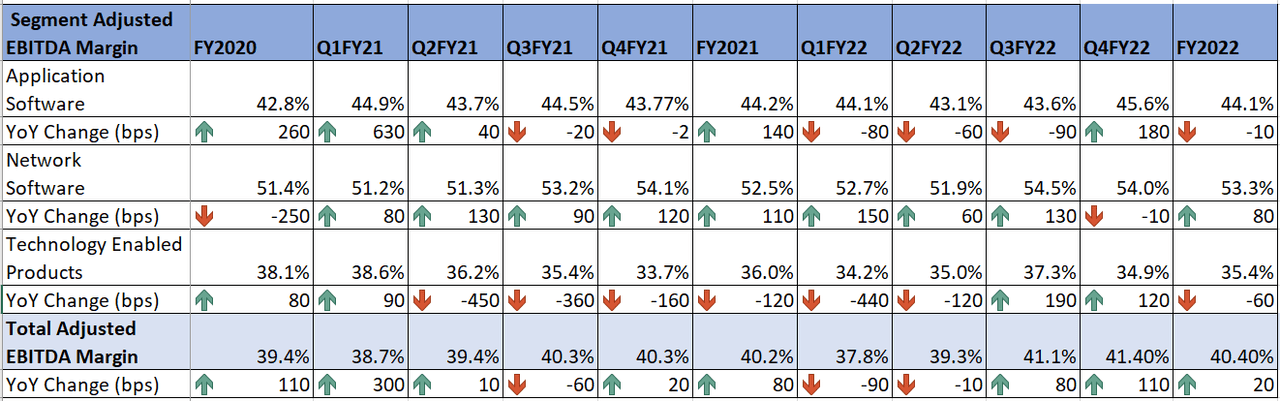

ROP’s Segment-wise Historical Adjusted EBITDA Margin (Company Data, GS Analytics Research)

Looking ahead, I believe ROP is poised to deliver growth in its adjusted EBITDA margin. Management has noted that supply chain conditions in the Technology Enabled product segment continue to improve and they expect remaining supply-related issues to be resolved in 2023. This coupled with operating leverage from continued revenue growth should contribute to margin improvement in the segment. Additionally, the company’s focus on acquiring higher-margin businesses as part of its growth strategy should also drive margin growth in the medium to long term.

Valuation and Conclusion

ROP is trading at 26.57x FY23 consensus EPS estimate of $16.17 and 24.55x FY24 consensus EPS estimate of $17.51. The stock is currently trading at a discount compared to its 5-year average forward price-to-earnings ratio of 28.42x. While the stock has seen some P/E multiple contractions due to the challenging macroeconomic environment, I am not worried about it. I believe the company can take advantage of the current slowdown to do bolt-on acquisitions at an attractive valuation and emerge stronger on the other side of the cycle. Hence I have a buy rating on the stock.

Be the first to comment