RichVintage

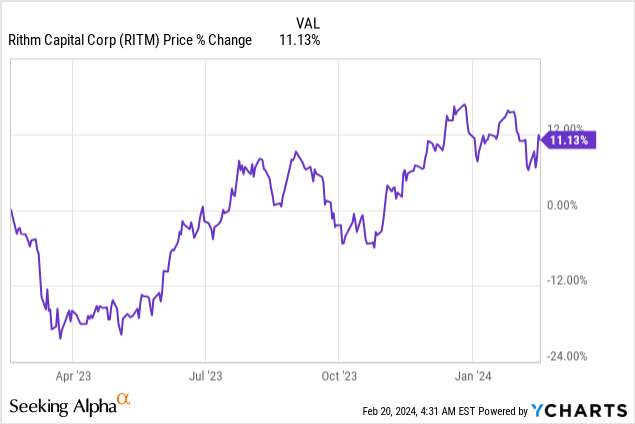

Rithm Capital’s (NYSE:RITM) shares fell after a hotter than expected inflation report last week that caused doubts about the Federal Reserve’s plan to lower interest rates in FY 2024. Since Rithm Capital also just reported fourth-quarter results and is heavily invested in mortgage servicing rights, which are rate-sensitive mortgage assets, I believe the drop is a new engagement opportunity for dividend investors. With shares now again priced at an 11% discount to book value, I believe the risk profile for this mortgage REIT is especially favorable. While I don’t expect to see a dividend raise in FY 2024, Rithm Capital provides a very well-supported 10% dividend yield!

Previous rating

I recommended Rithm Capital as a buy for dividend investors in November 2023 — A Magnificent, Bargain-Priced 10% Yield — due to the mortgage REIT’s good dividend value and potential for an upside revaluation. Rithm Capital last week submitted its earnings card which showed even better dividend coverage metrics than in the quarter before. With new inflation concerns causing the share price to dip, I believe dividend investors have an opportunity here to load up the truck with a discounted value deal.

A top mortgage REIT with a well-supported 10% dividend yield

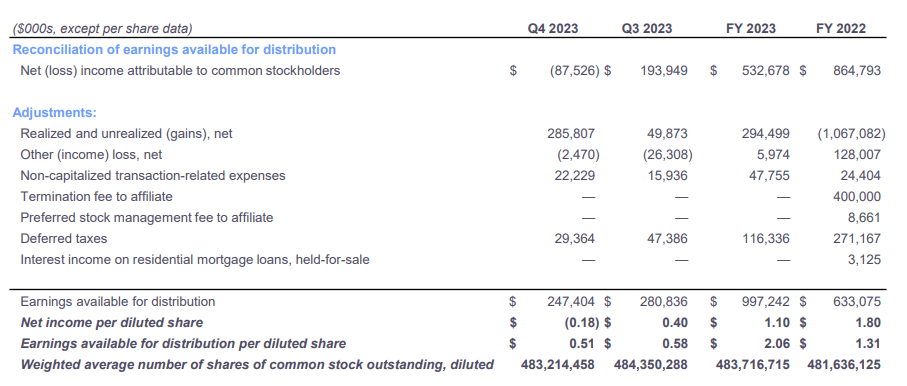

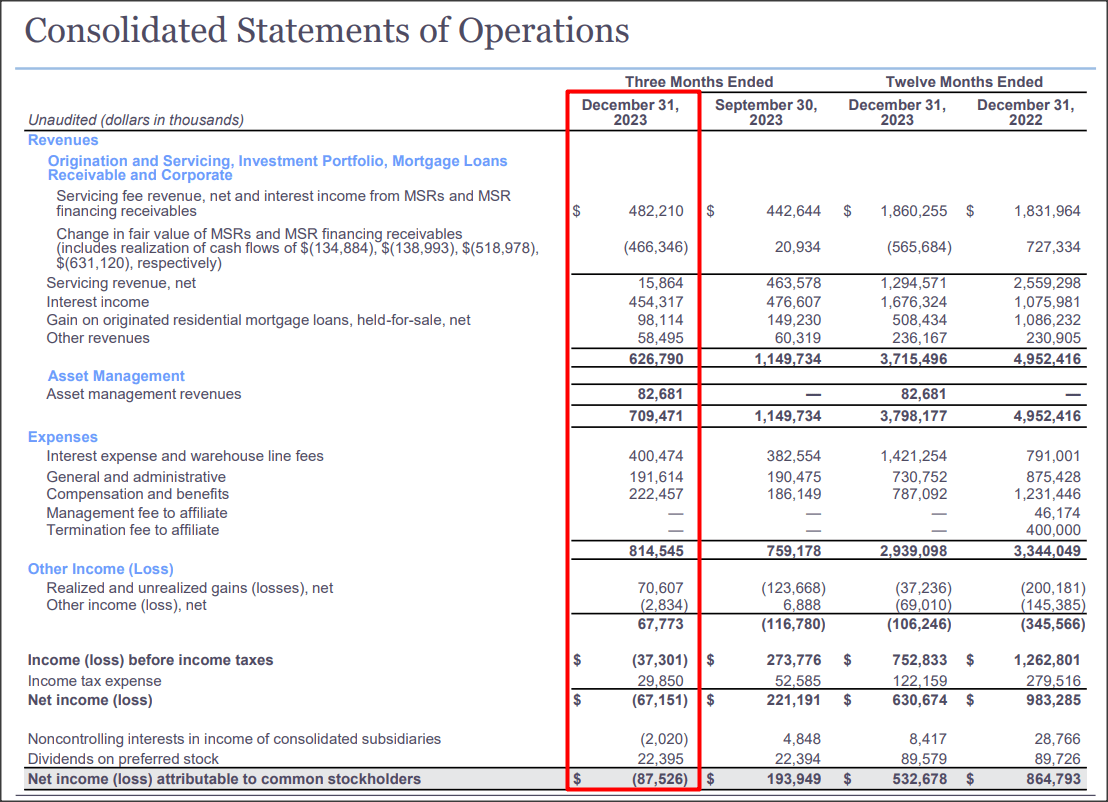

Last week, Rithm Capital submitted its earnings sheet for the fourth-quarter that showed earnings available for distribution (EAD) of $247.4M compared to $156.9M for Q4’22, showing an increase of 58% year over year. For the full-year, Rithm Capital had earnings available for distribution of $997.2M compared to $633.1M, showing an equally impressive year over year growth rate of 57%.

Rithm Capital

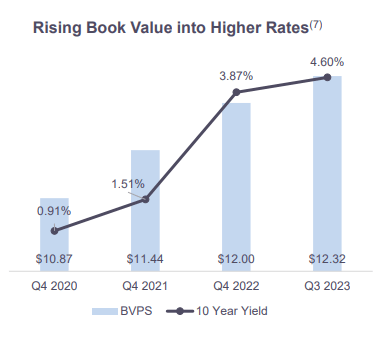

Rithm Capital’s success as a mortgage REIT and strong growth traces back to the company making smart capital decisions with regard to mortgage servicing rights. These rights generate higher fee income for the owner of a mortgage servicing right when interest rates rise and, vice versa, become less valuable during a down-turn in interest rates.

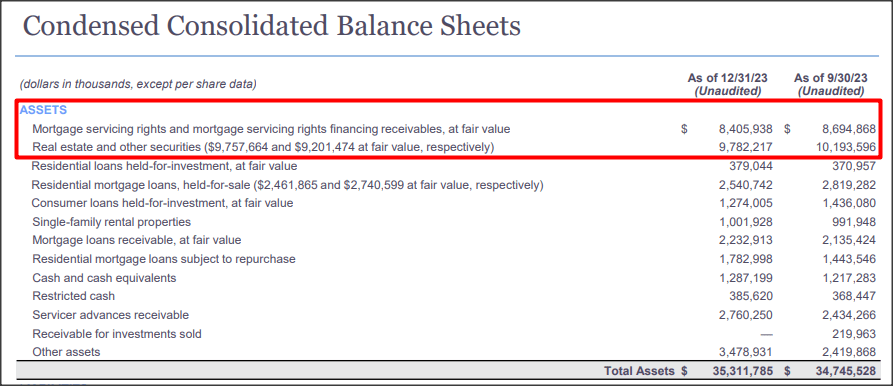

Mortgage servicing rights are the second-largest asset on Rithm Capital’s balance sheet with a total value of $8.4B. Only real estate securities with a combined value of $9.8B surpassed mortgage servicing rights in total investment value. Other assets on the company’s balance sheet include single-family rental properties, (residential) mortgage loans and services advances.

Rithm Capital

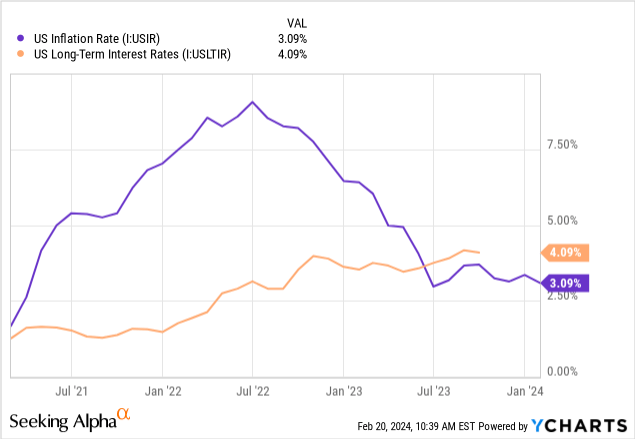

Rithm Capital’s investment portfolio is very much diversified, and includes a hedge against a reacceleration of inflation rates — inflation coming in hotter than expected in January (3.1% actual vs. 2.9% expected) — through its exposure to mortgage servicing rights.

It is this investment in mortgage servicing rights that has paid off nicely for the mortgage REIT due to the last two years… which is when the Federal Reserve tightened its interest rate policy to offset soaring inflation rates. As a result, Rithm Capital has been able to grow its book value while maintaining a decent distribution.

Rithm Capital

Rithm Capital has a diversified investment portfolio that, like I mentioned, includes servicer advances, residential mortgage loans, mortgage servicing rights, real estate securities and, due to the acquisition of Sculptor Capital, an asset management fee income stream. With interest rates set to go into a down-cycle in FY 2024, Rithm Capital is attempting to diversify its business. The asset management business already a positive revenue contribution of $82.7M in the fourth-quarter. Due to fair value changes related to mortgage servicing rights (totaling $466.4M), however, Rithm Capital’s net income was negative $87.5M in the fourth-quarter.

Rithm Capital

Expectations for FY 2024

Interest rates are likely to come down in FY 2024, but only in the second half of the year. A down-cycle in interest rates would therefore hurt the REIT’s mortgage servicing rights which makes me believe that Rithm Capital will want to sell some of its mortgage servicing rights and potentially recycle the capital into new investments outside the mortgage market. Rithm Capital could acquire new asset management businesses or investment funds as well in order to build out its third-party asset management segment and further diversify its revenue streams.

Very well-supported distribution

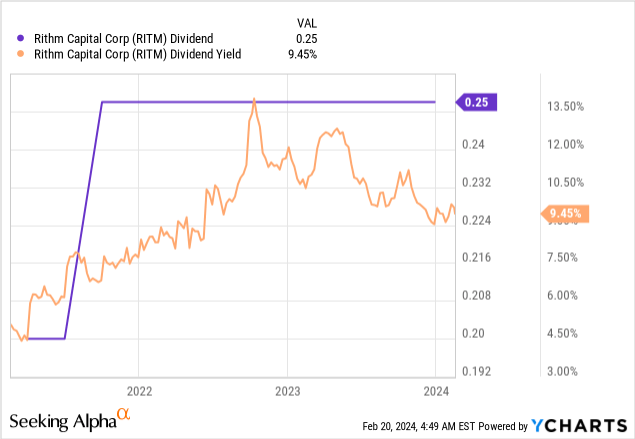

Rithm Capital’s investment portfolio generated earnings available for distribution of $0.51 per share in Q4’23 and $2.06 per-share in FY 2023. This calculates to an EAD-based dividend coverage ratios of 204% and 206%. In FY 2022, the distribution coverage ratio calculated to 131%. The coverage ratio is therefore excellent and allows for the stable payment of Rithm Capital’s current $0.25 per-share quarterly dividend. Since Rithm Capital has not raised its dividend since FY 2021, I do not expect a raise in the dividend in FY 2024 either.

Rithm Capital’s valuation

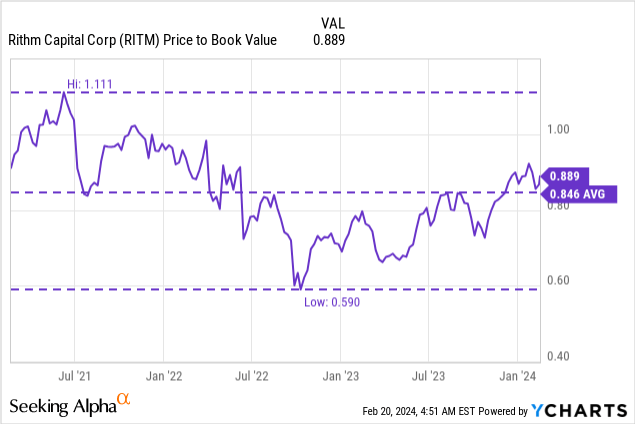

Rithm Capital is a fairly differentiated and diversified mortgage REIT due to its very non-traditional investment portfolio which has obvious value for dividend investors. However, Rithm Capital’s book value fell 3.4% quarter over quarter to $11.90 per-share in Q4’23 which was due to fair value changes related to mortgage servicing rights. My fair value estimate for Rithm Capital is equal to the REIT’s book value since accounting rules require fair value accounting.

Shares of Rithm Capital right now are priced at 0.89X book value which represents a 5% premium to the 3-year average price-to-book ratio. Rithm Capital is selling at a discount to book value, in my opinion, chiefly because the mortgage REIT owns a large set of different mortgage assets while other REITs are more straightforward, like Annaly Capital Management (NLY), which owns almost exclusively mortgage-backed securities. Given the REIT’s excellent distribution coverage ratio, not just for Q4’23 but for FY 2023, I believe Rithm Capital is a very attractive income play for investors and the 11% discount to book value is not deserved.

Risks with Rithm Capital

Rithm Capital’s investments are concentrated chiefly in mortgage servicing rights which are investments for a high-interest world. If the Federal Reserve starts to cut interest rates, investors should expect to see the valuation multiples for mortgage servicing rights to contract which will pose headwinds for the REIT’s valuation. Given the very solid distribution coverage ratio presented by Rithm Capital for Q4’23 and FY 2023, I believe the dividend is really well-supported.

Closing thoughts

I have loaded up the truck with shares of mortgage REIT Rithm Capital after shares dropped last week. There is still an opportunity for investors to buy into Rithm Capital at a decent 11% discount to book value and secure an 10% yield that is supported by earnings available for distribution, in my opinion. I like Rithm Capital’s well-diversified investment portfolio and very impressive distribution coverage ratio. The REIT now also owns an asset management business which further diversifies Rithm Capital’s revenue streams and makes the company less dependent on the mortgage market for income. I believe the risk profile is still favorable here and I continue to rate Rithm Capital a buy after the release of fourth-quarter earnings last week!

Be the first to comment