JHVEPhoto

Introduction

As a dividend growth investor, I constantly seek new income-producing assets to invest in. I add to current positions when attractively valued and start new positions when I seek to diversify my holdings further. I also use market volatility to my advantage by increasing dividend income with less capital.

The industrial sector is an exciting area for investors due to its diverse range of companies and products, mostly overlooked as they don’t have the appeal that other sectors have. One such company is Stanley Black & Decker (NYSE:SWK), which operates in industrial tools and household hardware. With a solid track record of growth and innovation, the company is a dividend aristocrat going through a business transformation.

I will analyze the company using my methodology for analyzing dividend growth stocks. I am using the same method to make it easier to compare researched companies. I will examine the company’s fundamentals, valuation, growth opportunities, and risks. I will then try to determine if it’s a good investment.

Seeking Alpha’s company overview shows that:

Stanley Black & Decker engages in the tools and storage and industrial businesses in the United States, Canada, the rest of the Americas, France, the rest of Europe, and Asia. Its Tools & Storage segment offers professional products, including professional-grade corded and cordless electric power tools and equipment, pneumatic tools and fasteners, and consumer products, such as corded and cordless electric power tools. The company’s Industrial segment provides engineered fastening systems and products to customers in the automotive, manufacturing, electronics, construction, aerospace, and other industries.

Fundamentals

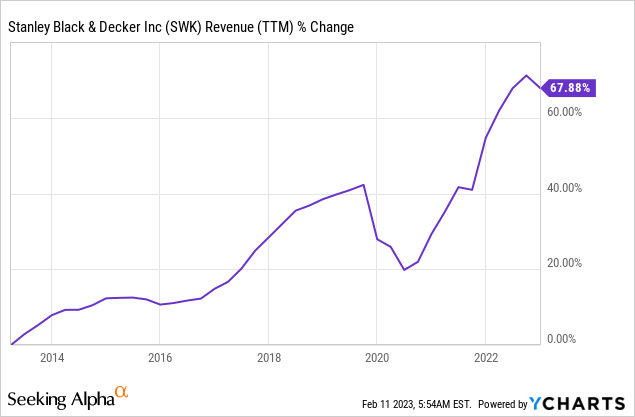

Revenues of Stanley Black & Decker have increased by almost 70% over the last decade. Sales have been impacted by organic sales and activity in the M&A markets. The company has been going through a business transformation to focus its business. Thus, it has divested some side businesses, such as security. In the future, as seen on Seeking Alpha, the analyst consensus expects Stanley Black & Decker to keep growing sales at an annual rate of ~1% in the medium term as the company focuses on shaping its portfolio.

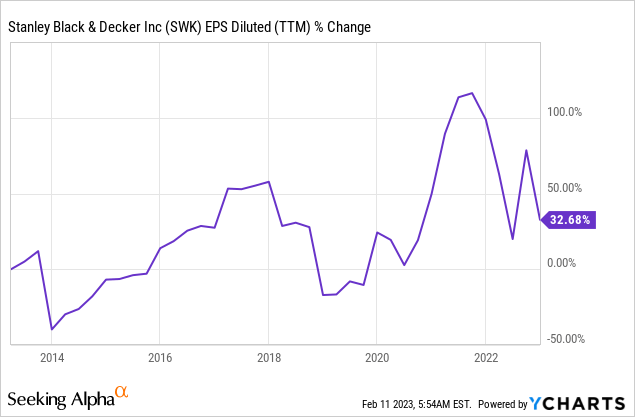

The EPS (earnings per share) has grown much slower over the same decade. The EPS has increased by 33% in a decade. During that decade, the company saw an increase of 100% in its EPS. The business transformation, high inventories, and lower margins have pressured the company’s EPS. A successful change should return the company to a growth path. In the future, as seen on Seeking Alpha, the analyst consensus expects Stanley Black & Decker to keep growing EPS at an annual rate of ~20% in the medium term.

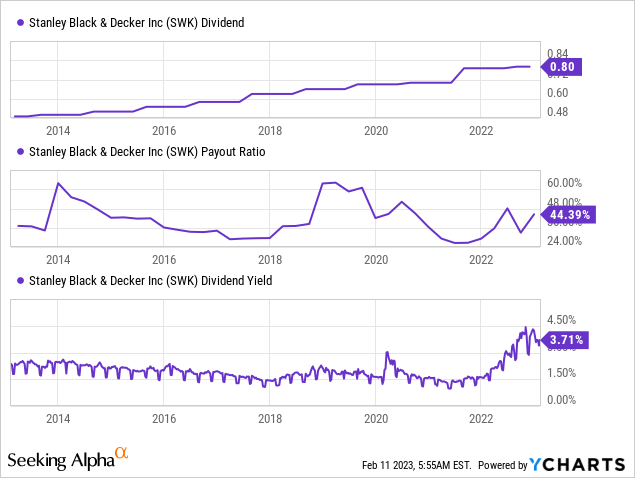

The dividend is the crown jewel of the company. Stanley Black & Decker is a dividend king with a record of 55 years of dividend increases. The dividend is a priority for the company, and the company can pay the dividend as the payout ratio is below 50%. The current yield is attractive at 3.7%, yet investors should expect higher short-term pressure on the dividend as the expectation is for a much lower EPS in 2023 as the company guided for $0-$2 EPS. The company intends to maintain the dividend, yet increases should be small in the medium term.

On the dividend, that is a very good question. Thank you for asking that. The dividend continues to be a very important part of our capital allocation strategy. We believe that it’s necessary to maintain the level of the dividend that we have today. We’ll continue to evaluate that through the remainder of the year, but there’s no change in that strategy at this stage.

(Don Allan – President & Chief Executive Officer, Q4 Earnings Call)

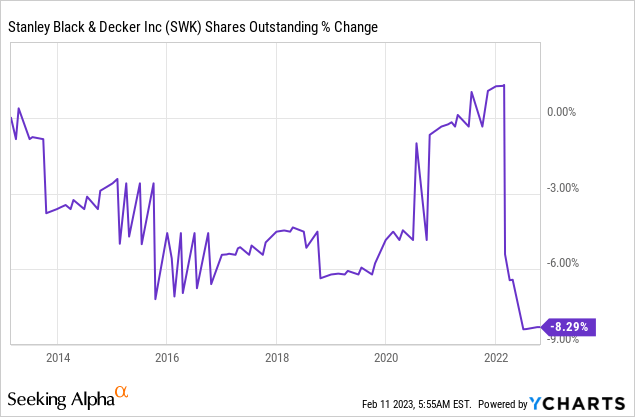

Buybacks are another method for companies to return capital to shareholders. They improve the company’s EPS by lowering the number of outstanding shares. Over the last decade, the company managed to decrease the number of shares by 8%. Buybacks are a discretionary move that is more useful when the balance sheet is healthy, and the share price is attractive. The company does not intend to buy back more shares as it prioritizes deleveraging.

Buying back stock is not an opportunity for us, given the leverage, we have on our balance sheet. And so, therefore, returning value to our shareholders, the main lever we have today is our dividend.

(Don Allan – President & Chief Executive Officer, Q4 Earnings Call)

Valuation

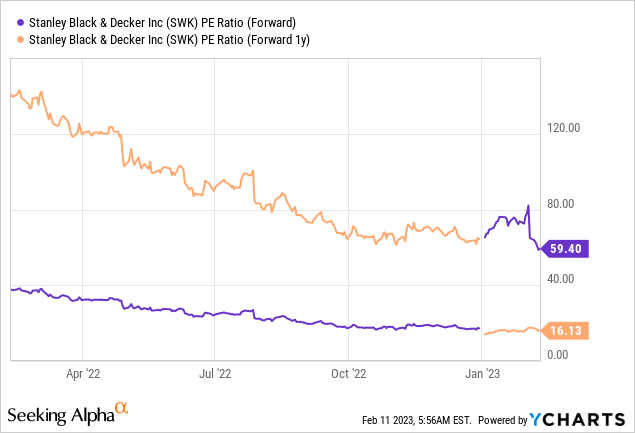

The P/E (price to earnings) can be a bit misleading as the company is going through a business transformation, and if successful, its EPS may increase significantly. The current price-to-earnings ratio stands at almost 60 when using the 2023 EPS but at only 16 when using the forecasted 2024 EPS. However, 2024 is far, and plenty of unknowns make it hard for me to rely on it. While I believe that the EPS will recover, the scope of the recovery is unknown.

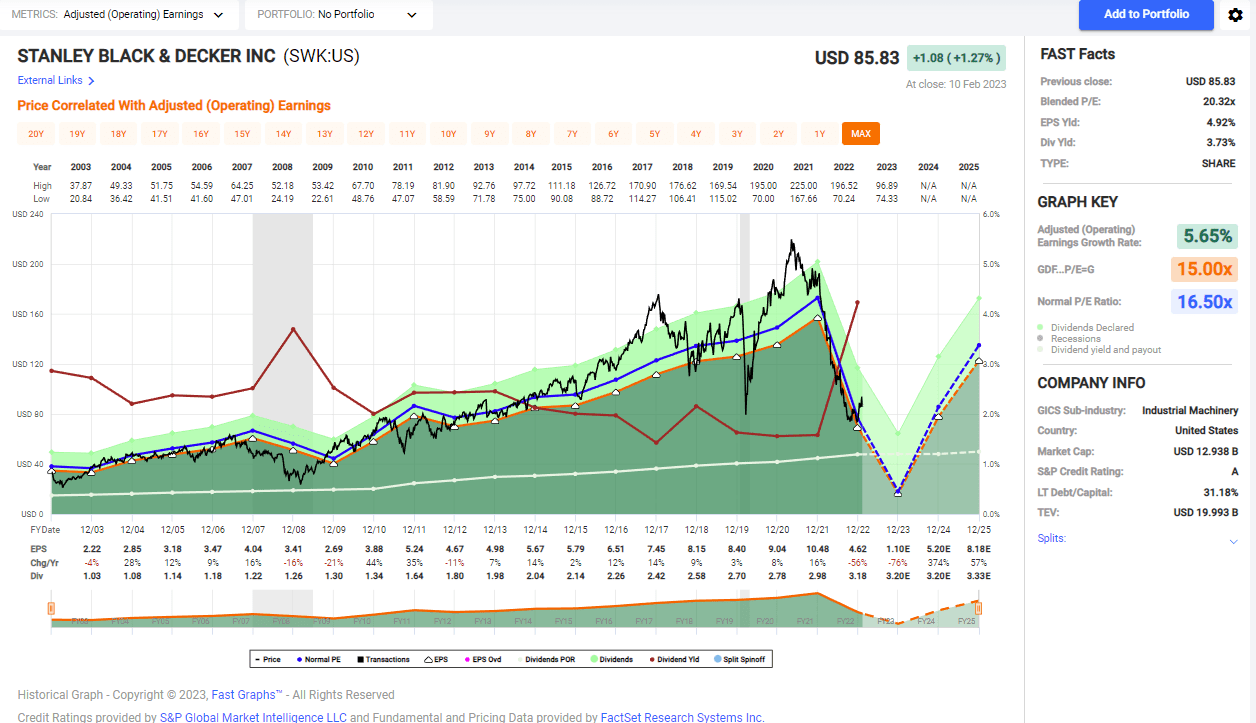

The graph below from FAST Graphs shows that the company is not fairly valued. During the past two decades, the average P/E ratio of the company was 16. The current P/E ratio for 2024 is 16, with all the uncertainties of the business transformation. If the transformation succeeds, the historical growth rate will be slower than the expected growth rate. However, this is a big “if,” and there is not enough margin of safety at the current valuation.

FAST Graphs

Stanley Black & Decker has solid fundamentals, yet they are deteriorating due to the weaker balance sheet and the need to transform the business, focus it and prepare it for the future. A successful transformation will bring the company to a healthy position, yet it is a complex and lengthy process. Moreover, the company’s current valuation does not offer enough margin of safety when looking at the challenging fundamentals.

Opportunities

Firstly, the company has a strong global presence with operations in over 60 countries. This international diversification helps mitigate the risk of regional economic downturns and provides access to a wide range of markets with varying levels of growth potential. Furthermore, the company’s well-established international distribution network can be leveraged for efficient supply chain management and ensures that its products are available to customers worldwide.

Secondly, the company has a current transformation plan focused on cost-cutting, debt and inventory reduction, and divestitures, along with innovation to the product lines. These measures are designed to drive operational efficiency and optimize profitability, which will help create long-term shareholder value. Additionally, the company’s focus on innovation, particularly in digital transformation and sustainability, is critical to maintaining its competitive advantage in the global market. This approach to innovation is demonstrated in its investment in the electrification of its tools and the usage of new technologies, such as 3D printing.

Finally, Stanley Black & Decker has a long track record of performance, including overcoming past challenges. The company has weathered economic downturns, recessions, and industry-specific challenges, demonstrating its resilience and ability to adapt to changing market conditions. In recent years, the company has successfully navigated the COVID-19 pandemic, with its innovative and diversified product offerings allowing it to remain competitive and profitable. Additionally, the company has a history of making strategic acquisitions that have helped it to expand its product offerings and market share.

Risks

There are also significant risks to consider. The company’s ongoing transformation plan carries the risk of a failed turnaround. Although the company has a history of successful acquisitions and product innovations, turnarounds can be risky and challenging. Examples of companies that have struggled with turnaround plans include IBM, which faced a prolonged transformation, and General Electric, which ultimately failed to turn the company around. As with any turnaround, there is a risk that Stanley Black & Decker’s transformation plan may not be successful, which could negatively impact the company’s financial performance and stock price.

Moreover, the current economic environment risks Stanley Black & Decker, particularly with the potential for higher interest rates and reduced consumer spending. The company’s home improvement products are sensitive to changes in interest rates and consumer spending, and any significant economic downturn could impact demand for these products. With interest rates expected to remain higher than average in the coming years and consumers potentially having less capital to invest in home improvements, there is a risk that demand for Stanley Black & Decker’s products could decrease.

In addition, the company’s readiness to adapt to a changing environment may be insufficient, as it has a significant amount of debt and inventory but little cash. This implies challenging short-term execution, especially in times of market volatility. The company’s high debt levels also increase the risk of financial distress, mainly if it cannot generate sufficient cash flows to service its debt obligations while paying the dividend. In addition, the company’s inventory levels may become outdated or unsold, leading to significant write-downs and negatively impacting the company’s financial performance.

Conclusions

Overall, investing in Stanley Black & Decker offers exposure to a well-diversified, global company focused on operational efficiency, innovation, and creating long-term shareholder value. With a proven track record of performance and a commitment to adapting to changing market conditions, the company is well-positioned to benefit from continued growth in the global market.

However, the potential for a failed turnaround, an economic environment with higher interest rates, and reduced consumer spending cannot be overlooked. I would expect the company’s valuation to be lower to account for these significant risks, as the company has little balance sheet flexibility to deal with them. Therefore, I believe that the company is a HOLD, and I would not buy shares until there are signs of improvement or when the price is more attractive at around $70.

Be the first to comment