sasacvetkovic33/E+ via Getty Images

Ring Energy (NYSE:REI) is a small Texas oil producer with horizontal and vertical wells in the less well-known Central Basin Platform and Northwest Shelf of Texas.

It has made a good acquisition with Stronghold Energy reinforcing its asset position, cash flow, and production. However, it has considerable debt via a revolving line of credit relative to its market capitalization.

The company doesn’t pay a dividend and so will not appeal to dividend investors.

The company may be a speculative buy for bargain-hunting investors looking for potential capital appreciation or as an acquisition target itself.

I recommend Ring Energy as a “hold.”

Stronghold Acquisition

Ring Energy closed the acquisition of private Stronghold Energy on August 31, 2022.

According to the company, the transaction was a) about $168 million cash, b) a $15 million deferred cash payment at the end of February 2023, c) $20 million to assume a Stronghold hedge liability, and d) issuance of 21.3 million shares of common stock and 153,176 shares of Convertible Preferred Stock, convertible into approximately 42.5 million shares of common stock upon a stockholder vote. Shareholders approved the conversion on October 27, 2022.

Total consideration was $405 million.

The cash part of consideration was funded through the company’s revolving credit facility.

Warburg Pincus was the majority owner of Stronghold and so became the largest equity-holder in Ring.

3Q22 Results and Guidance

For the third quarter of 2022, Ring Energy reported net income of $75.1 million, or $0.49/share, compared to $41.9 million or $0.32/share for 2Q22.

In 3Q22, the net income of $75.1 million included a $47.7 million pre-tax non-cash unrealized commodity derivative gain while in 2Q22, the net income of $41.9 million included a $12.2 million pre-tax non-cash unrealized commodity derivative gain.

Cash flow from operations was $48.9 million and free cash flow was $9.7 million.

Sales volumes were 13,300 BOE/D comprising 76% oil, 13% natural gas, and 11% natural gas liquids.

As noted above, Ring closed the acquisition of Stronghold.

For 4Q22, the company anticipated making capital expenditures of $42-$46 million (15% under prior estimates), and to achieve sales volumes of 18,000-19,000 BOE/D comprising about 70% oil, 17% natural gas, and 13% natural gas liquids. This is about a 40% volumetric increase from 3Q22 sales volumes. Note that while higher-valued oil was projected to be lower on a percentage basis, on an absolute volume basis oil was projected to be higher by about 3000 BPD.

According to CEO Paul McKinney, for 2023, the company’s initial goal is to “maintain or slightly grow average sales volumes” from anticipated 4Q22 levels. At oil prices of $75-$90/barrel the company expects to use excess free cash flow to pay down debt. Estimated capital expenditures are $150 to $175 million.

However, projects and estimates (in November 2022) were based on WTI oil prices of $75-$90/bbl and Henry Hub gas prices of $5-$6/MCF but the forward curves for both are now lower, suggesting a likely change in project priorities and funding.

The company did not have any natural gas hedges in place for 2023 but has oil derivatives for 2023 and 2024 covering approximately 5000 BPD and 3000 BPD respectively.

Per the company’s 10Q, its largest customer accounted for 69% of its first nine months’ revenues and 58% of its 3Q22 revenues.

Ring Energy Reserves and Production

At December 31, 2021, so thus excluding the Stronghold acquisition, Ring Energy owned proved reserves of 65.8 million barrels of oil and condensate and 71.8 billion cubic feet (BCF) of natural gas, or 85% oil on a barrels of oil equivalent basis.

About half of the reserves were proved undeveloped and half were proved developed producing.

The SEC PV-10 value of the reserves was $1.33 billion.

The value of reserves at December 31, 2022, is expected to be higher due to both the inclusion of the Stronghold Energy reserves and moderately higher oil and gas prices. The pro forma PV-10 with Stronghold included is $1.74 billion.

Combined acreage position is 101,000 acres.

Combined production is estimated to be about 13,000 BPD of oil; 19,000 MCF/D of gas; and 2400 BPD of natural gas liquids.

Production (virtually all in Texas) is via:

*horizontal drilling in the Northwest Shelf (Yoakum County-TX, Lea County-NM);

*vertical drilling in the Delaware sub-basin of the Permian (Culberson and Reeves Counties);

*horizontal drilling in the Central Basin Platform (Andrews, Gaines, and Crane Counties).

EIA

Macro and Oil Prices

Supply and demand factors point to downward pressure on oil and especially natural gas prices in 2023. For oil and gas, these include low oil volumes in the US Strategic Petroleum Reserve but very moderate winter temperatures in the northern hemisphere, especially in Europe. China’s pace of recovery remains a question mark, and global economies are generally recessionary. In the US, natural gas production is higher and will not be much offset by additional LNG demand until late 2024. Due to the Russian invasion of Ukraine, the EU is seeking new, non-Russian energy sources for 2023 and forward while Russia is redirecting its (discount-priced) exports to China and India.

In the US, continued inflation may lead the Fed to raise rates further. The Fed has already said it will not lower rates in 2023.

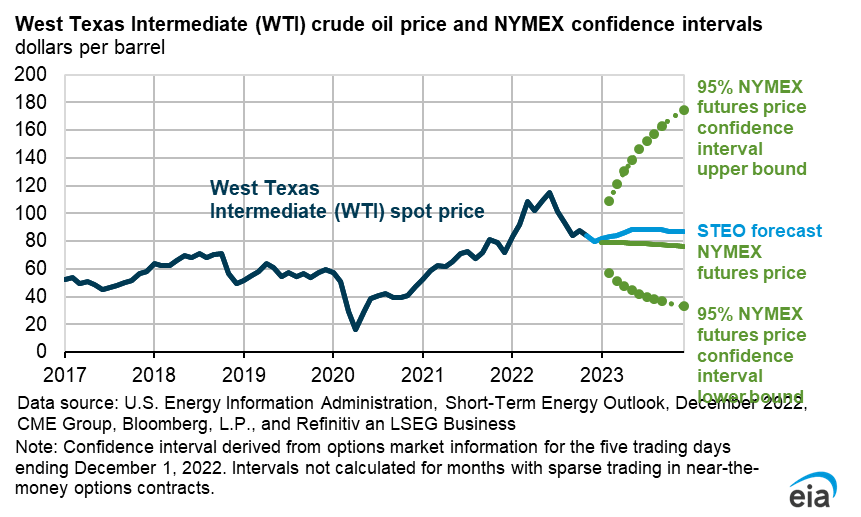

The EIA’s 5-95 confidence interval charts for both oil and gas prices through the end of 2023 are shown below.

EIA

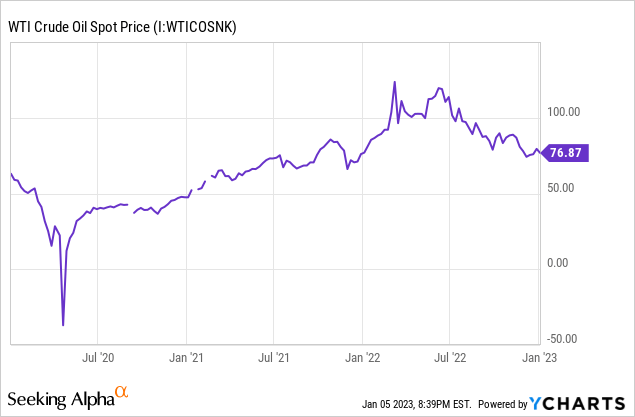

The January 5, 2023, closing oil price for West Texas Intermediate (WTI) crude oil at Cushing, Oklahoma for February 2023 delivery was $73.67/barrel. Natural gas price for February 2023 delivery at Henry Hub, Louisiana was $3.72/million British Thermal Units (MMBTU).

Competitors

Ring Energy is headquartered in The Woodlands, Texas. It competes with all producing companies in all sub-basins of the Permian.

The company also has significant competition from private companies.

Competition extends throughout its business, from hiring executives and expert professionals, to competing for takeaway capacity and service contractors, to selling oil and gas.

Governance

On December 28, 2022, Institutional Shareholder Services ranked Ring Energy’s overall governance as 4, with sub-scores of audit (10), board (6), shareholder rights (3), and compensation (2).

Ring Energy’s beta is high at 1.98, representing more volatility than the overall market but in line with upheaval in oil supply, demand, and prices, particularly for a small company.

Insiders own 15.15% of the stock. At December 15, 2022, 12.8% of floated stock was shorted.

At September 29, 2022, the three largest institutional holders were Warburg Pincus (28.5%) BlackRock (3.3%), and Vanguard (2.5%).

Since Warburg Pincus was the majority owner of Stronghold Energy, it became Ring’s largest shareholder. Additionally, Ring’s board of directors was expanded from seven to nine members, with the two additional members proposed by Stronghold.

Financial and Stock Highlights

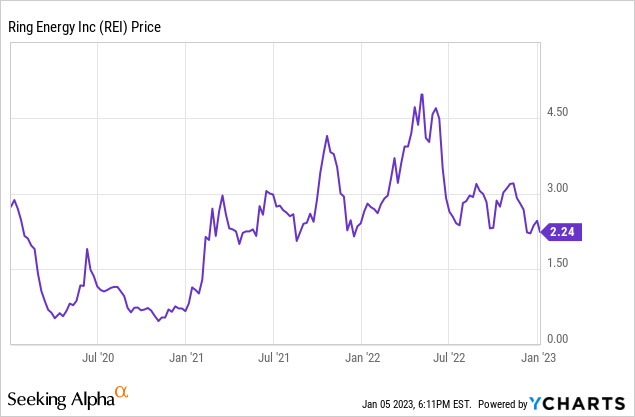

The company’s 52-week price range is $2.14-$5.09 per share, so its January 5, 2023, closing price of $2.24 is 44% of the high and gives a market capitalization of $391 million. Ring Energy’s one-year target price is $5.50/share, so its closing price is 41% of that level.

Trailing twelve months’ earnings per share is $1.11 for a price/earnings (P/E) ratio of a scant 2.0. The average of analysts estimated 2023 earnings per share (EPS) is $0.96, yielding a bargain forward P/E ratio of 2.3.

Return on assets is 11.1% and return on equity is 32.2%.

At the end of the third quarter of 2022, Ring Energy had $607 million in liabilities and $1.25 billion in assets for a liability-to-asset ratio of 49%. A large part of the liabilities was a line of credit of $435 million.

On September 30, 2022, a portion of the company’s equity was mezzanine equity-convertible preferred stock with a balance sheet value of $137.8 million. However, per the transaction agreement, Ring Energy’s stockholders approved the conversion of the preferred to 42.5 million shares of common equity.

Still, it is important to note that the interest rate on the company’s line of credit is the Standard (or Secured) Overnight Financing Rate (SOFR) PLUS 3-4%. The current 180-day SOFR is 2.99%.

Trailing twelve months’ operating cash flow was $156.5 million and levered free cash flow was $47.9 million.

The company’s mean analyst rating is 1.8–a “buy” leaning toward “strong buy”–from ten analysts.

Ring Energy does not pay a dividend.

Notes on Valuation

The company’s book value per share of $3.85, more than its current market price, indicates negative market sentiment.

Reflecting its debt, small size, and recent downward trajectory of oil and gas prices, Ring Energy’s market capitalization per unit of production is lower than many of its peers at $21,100/flowing BOE and $30,000 per flowing barrel of oil.

The company’s ratio of debt to market capitalization is high at 1.1.

Ring Energy’s enterprise value is $826 million and its market capitalization is $391 million at a January 5, 2023, stock closing price of $2.24 per share. The year-end 2021 PV-10 value of reserves was $1.33 billion. Its enterprise/EBITDA ratio of 3.8 is well below the maximum of 10.0 or less, thus suggesting a bargain.

Positive and Negative Risks

Negatives are the 15% of shares shorted and the 28% owned by Warburg Pincus, which may cap upward price movement for common shares. Additionally, Warburg Pincus’ large equity position may put its interests at odds with those of smaller shareholders.

Investors should consider their US oil and gas price and general stock market expectations as the factors most likely to affect Ring Energy. However, Ring Energy has relatively favorable hedges in place for 2023.

The biggest political risk to Ring Energy is from the US administration’s anti-hydrocarbon stance and the effect on operations.

Inflation has increased costs throughout global supply chains, including for oil and gas production.

Given two serious (5.4) earthquakes and many smaller ones in the Midland and Delaware sub-basin areas–although some of Ring’s operations in the Northwest Shelf and the Central Basin Platform are somewhat remote from these areas–expect Ring Energy’s production to be subject to higher wastewater handling and recycling costs as saltwater disposal wells are volume-limited or closed.

Recommendations for Ring Energy

While Ring Energy is not appropriate for dividend seekers, the company has interesting assets and production.

Warburg Pincus has significant ownership at 28% and insiders own another 15%. This has the potential to cap upside.

The company has good hedges and oil-focused production and will see a significant uptick in production and reserves starting with 4Q22 reporting. Based on the ratio of enterprise value to EBITDA and price/earnings ratio, its equity is a bargain. Its stock price is low relative to the 52-week range and the one-year target.

However, it also has high ratio of debt to market capitalization. Moreover, its debt-a line of credit-has a fairly high interest rate that will continue to go up if interest rates continue to increase, as expected.

I recommend the stock as a “hold.” It may be of interest to speculative investors who expect significant capital appreciation or that Ring may become an acquisition target itself.

Be the first to comment